Monetary

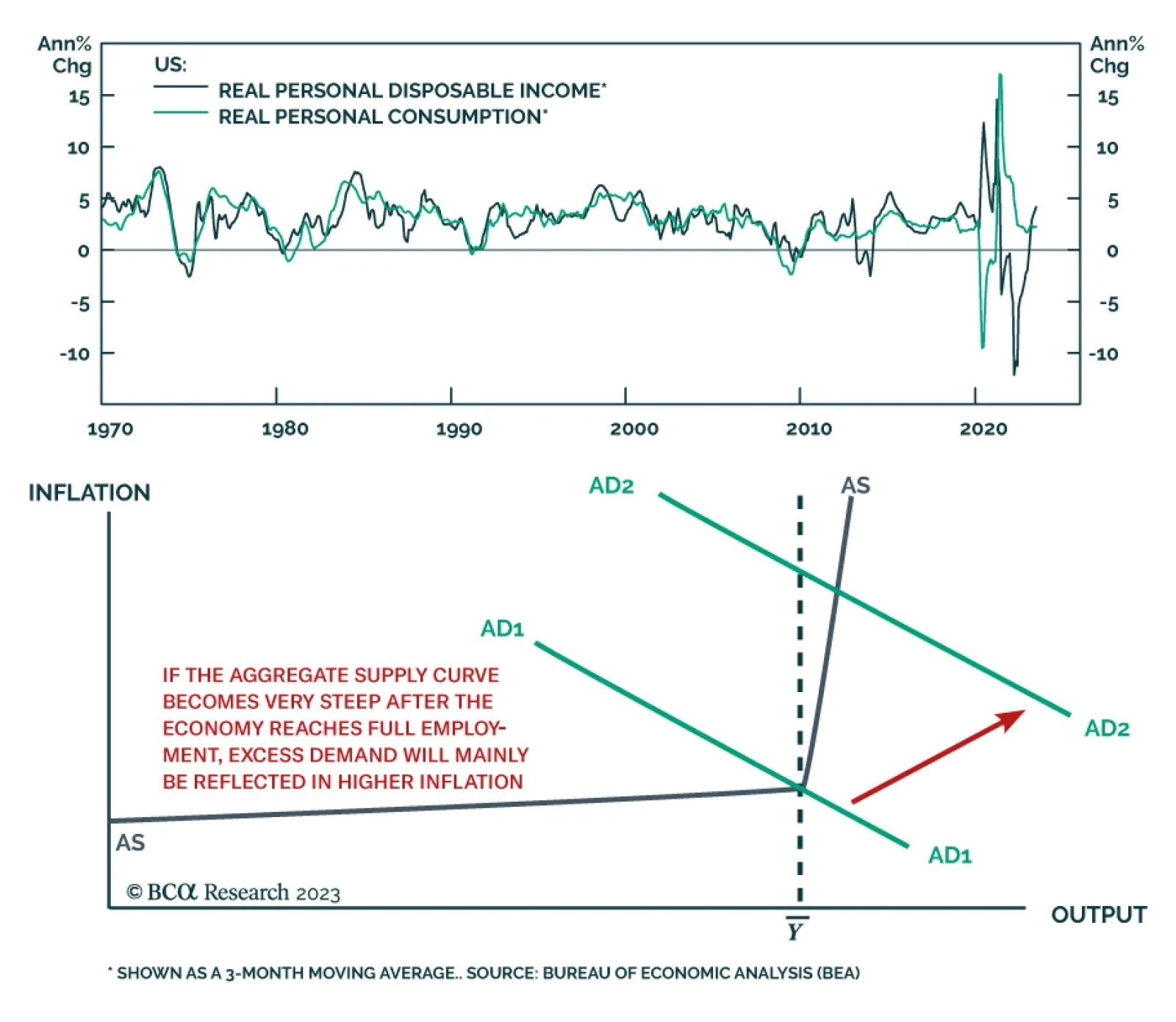

Collapsed complexity, plus the unwinding of favourable base effects and favourable seasonal adjustments to the inflation and jobs numbers, all pose a danger to the Goldilocks market.

The trajectory of China’s infrastructure investment in 2023H2 will be like what occurred in 2021H2. Growth will likely drop from the current nominal 10% to 0-2% in the next six months. China will continue promoting environmentally friendly infrastructure projects that may prevent a contraction in infrastructure investment in 2023H2.

History suggests that a “soft landing” is highly unlikely after such an aggressive Fed tightening cycle. The rally could continue for a little longer but, on the 12-month horizon, market risks are very skewed to the downside.

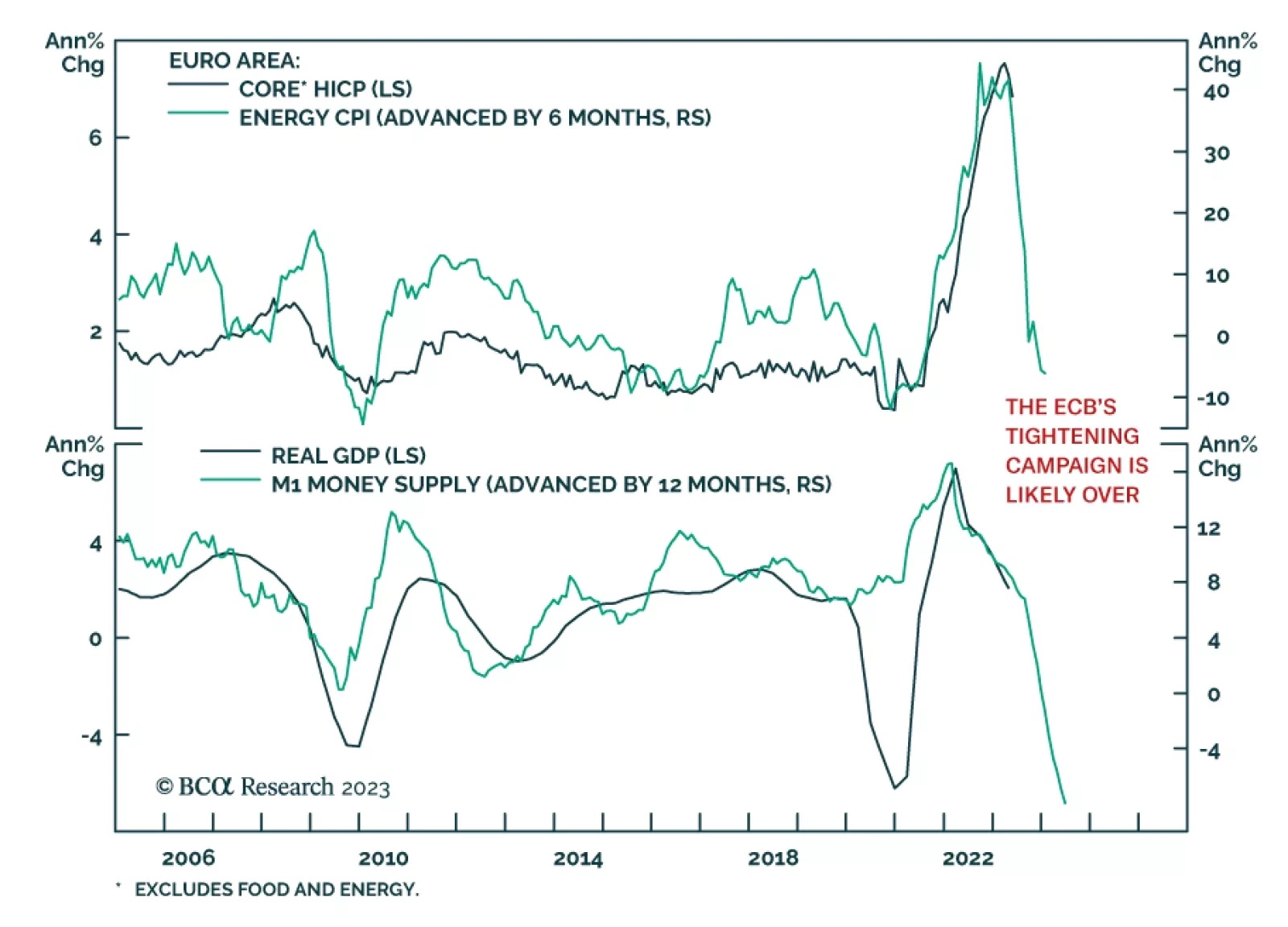

The ECB’s tone has changed decisively. Intransigent forward guidance is gone; data dependency is in. What does this transition mean for the path of European interest rates and the euro?