Monetary

A discussion of today’s FOMC meeting and its investment implications.

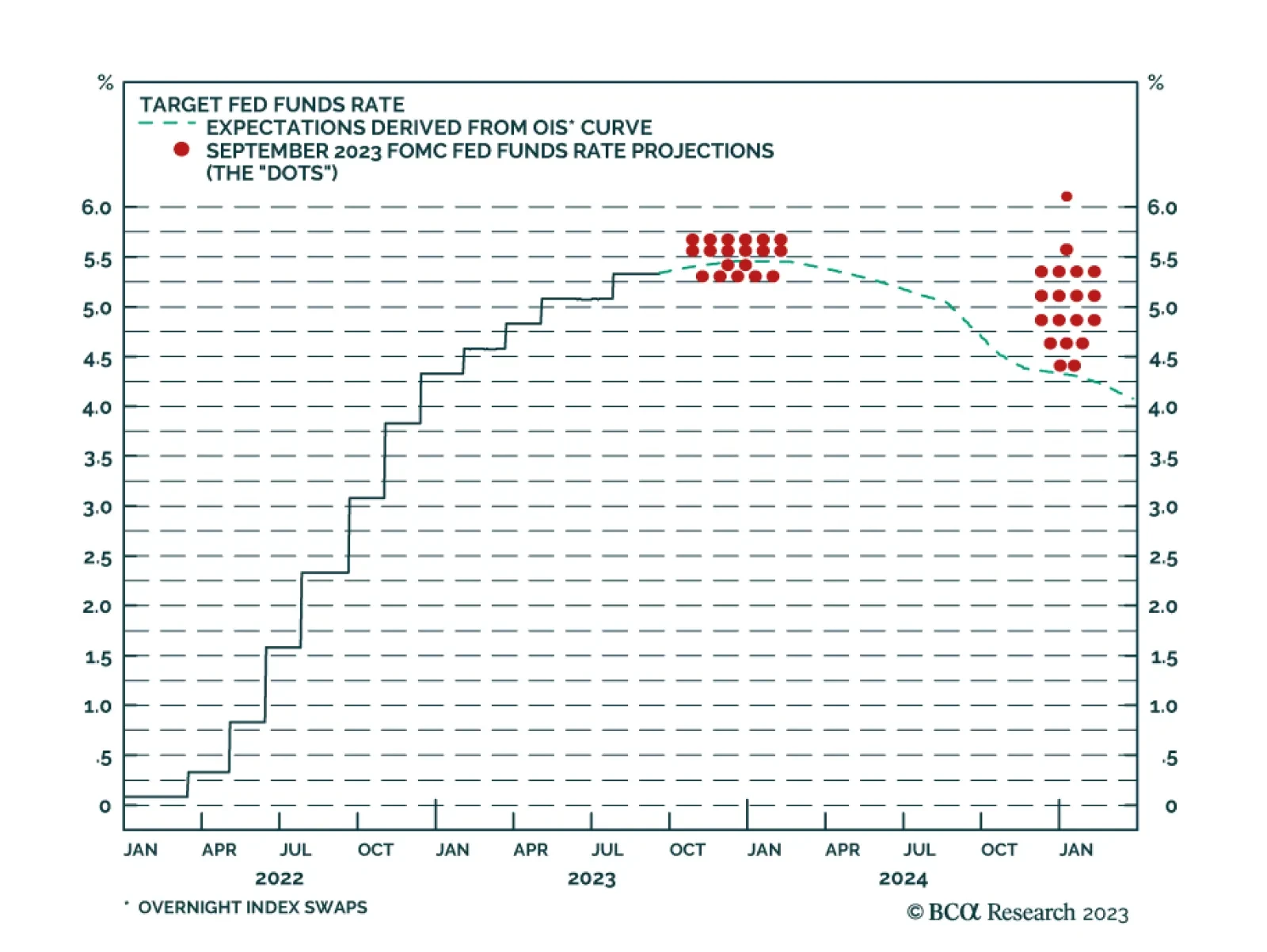

The biggest misunderstanding in the markets right now is that to keep expected inflation well-anchored at 2 percent, inflation must <i>undershoot</i> 2 percent for some time. This implies that interest rate futures curves are mispriced, and that the probability of a ‘soft landing’ is lower than assumed. Plus: we show that the rally in oil has become fractally fragile, and recommend a tactical underweight.

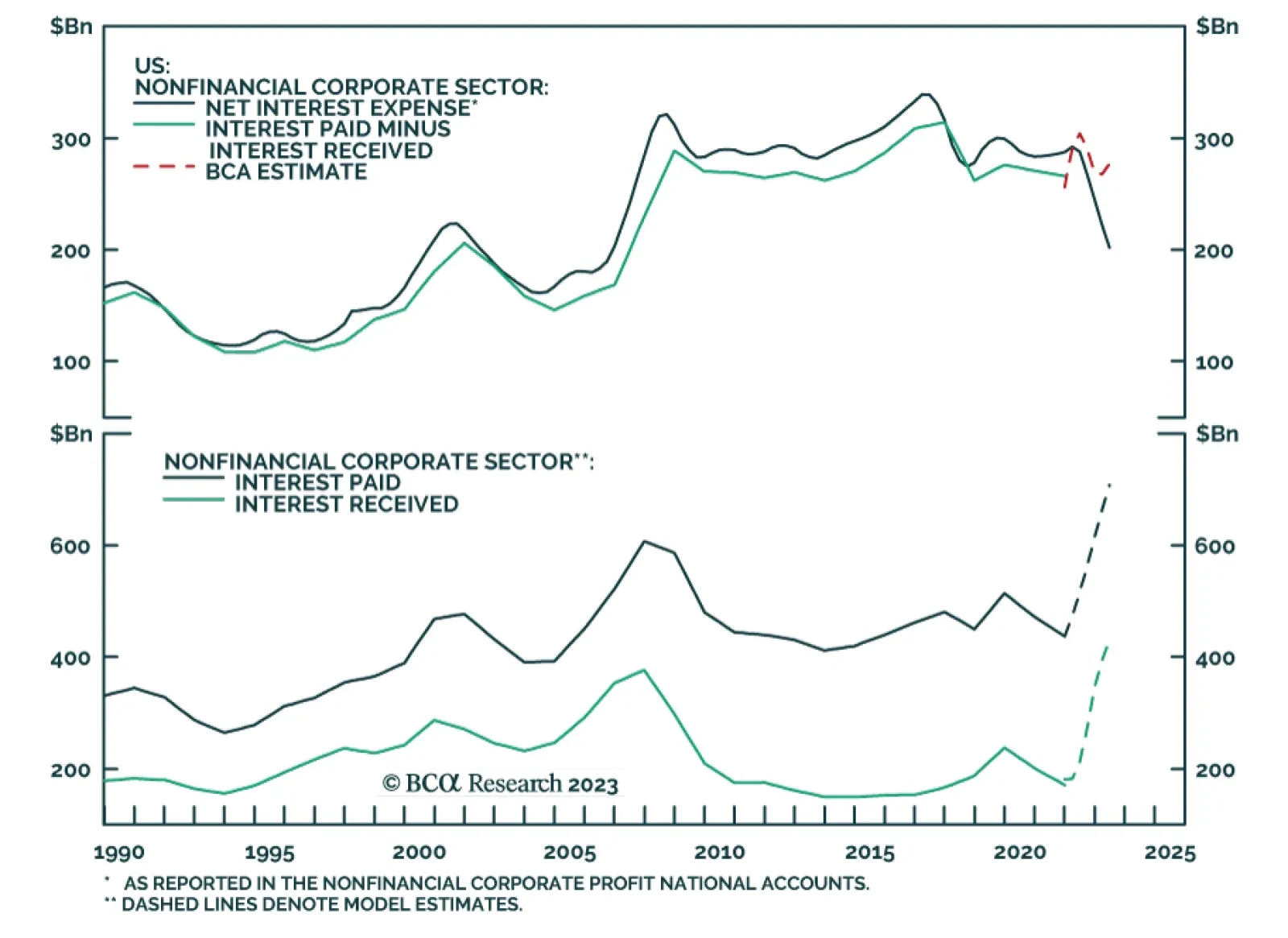

Top-down measures of nonfinancial corporate sector balance sheet health have been flattered in recent quarters by inaccurate data on interest expense. After correcting for the inaccurate data, we see that our best measures of corporate balance sheet health show a persistent steady deterioration.