Monetary

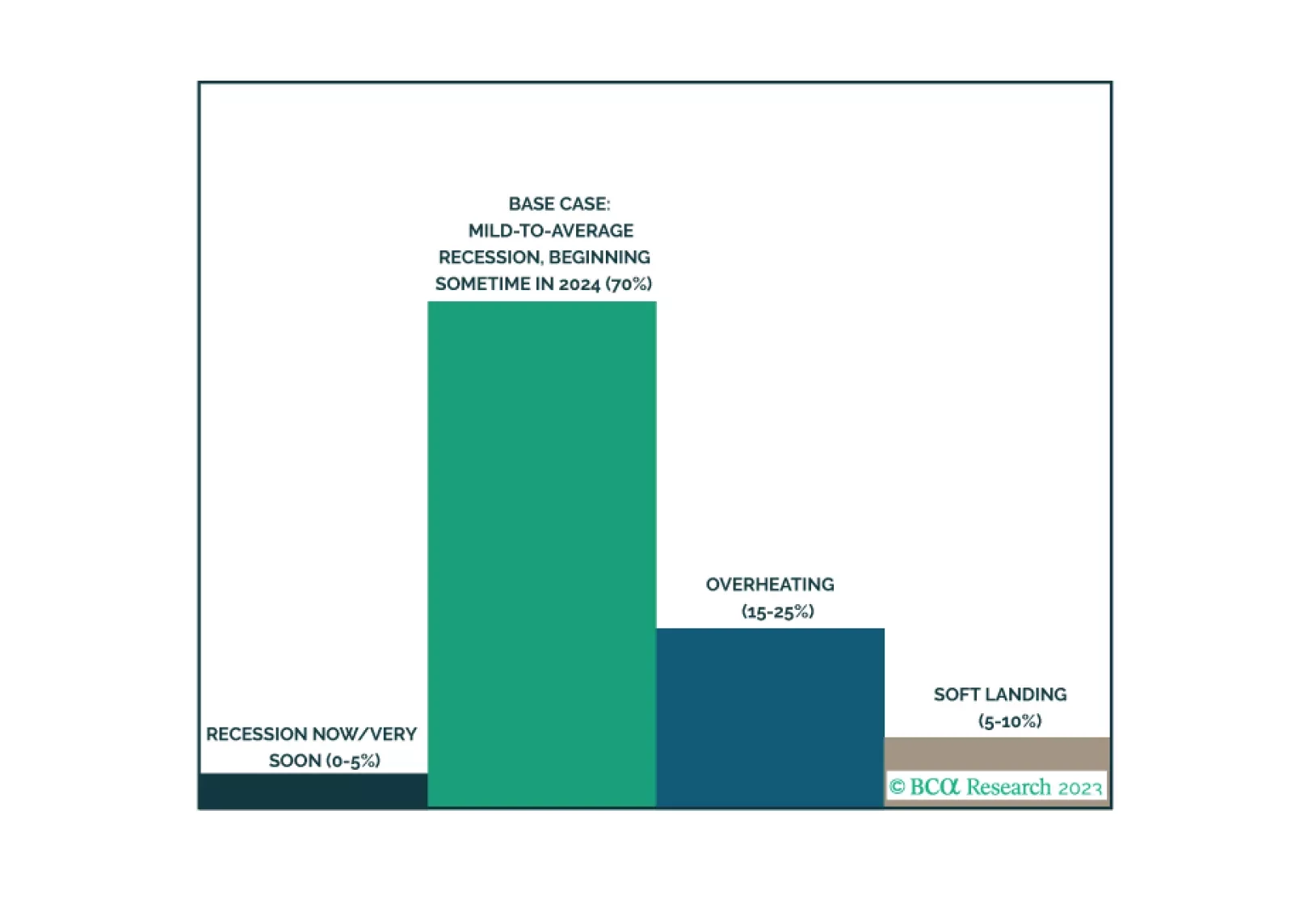

Our last publication of 2023 is an illustrated guide to our view that the economy will enter a recession around midyear. We expect equities will underperform Treasuries and cash over much of 2024, but we are waiting to turn tactically defensive until more investors are drawn into the soft-landing camp, capping the equity rally.

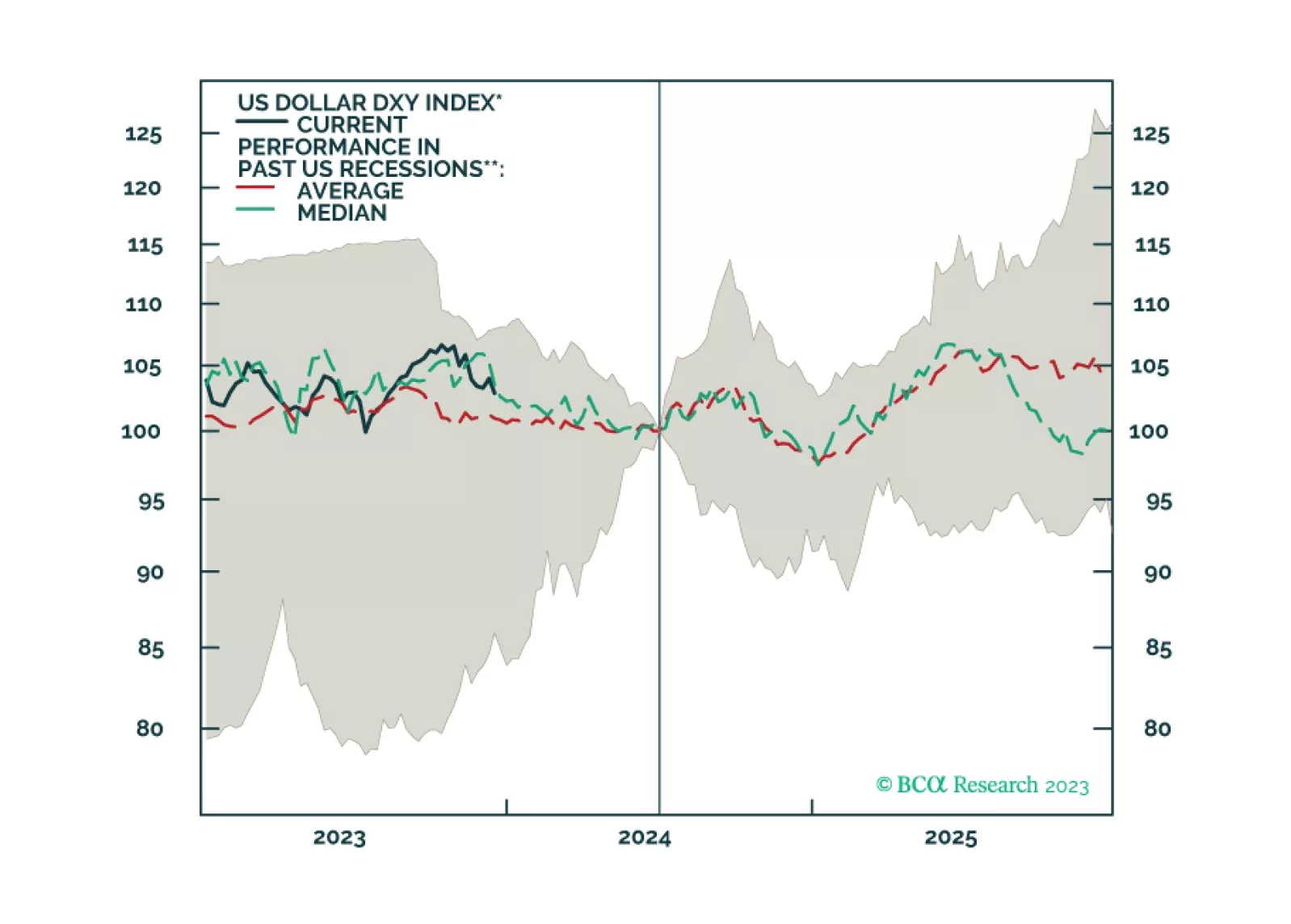

In this week’s report, we present our dollar view for 2024 and beyond, with a few trade ideas.

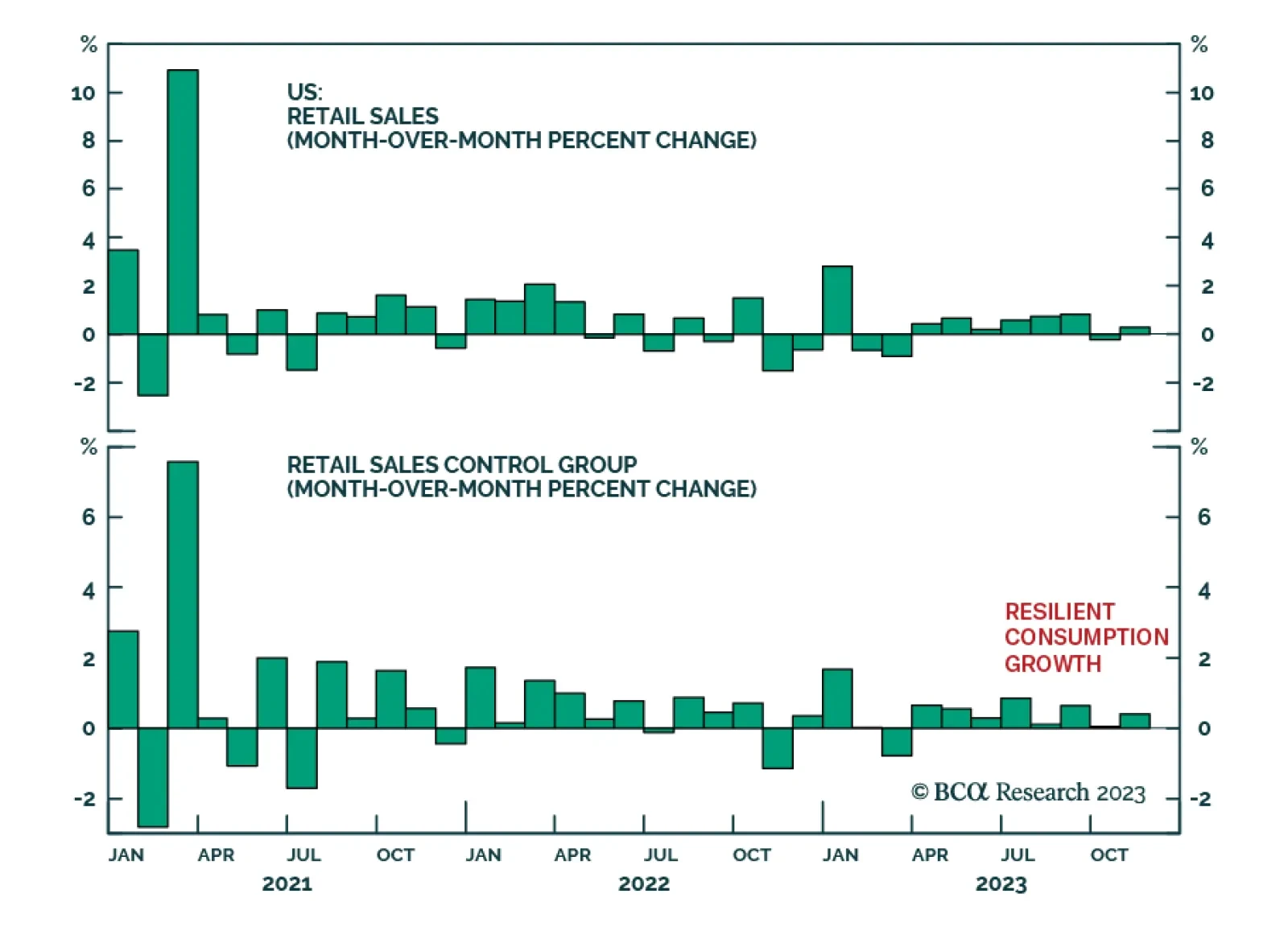

The November US retail sales release for November delivered a positive signal about consumer spending. Overall retail sales unexpectedly increased by 0.3% m/m, surprising expectations of a 0.1% m/m decline. The details of the report were also favorable. Eight…

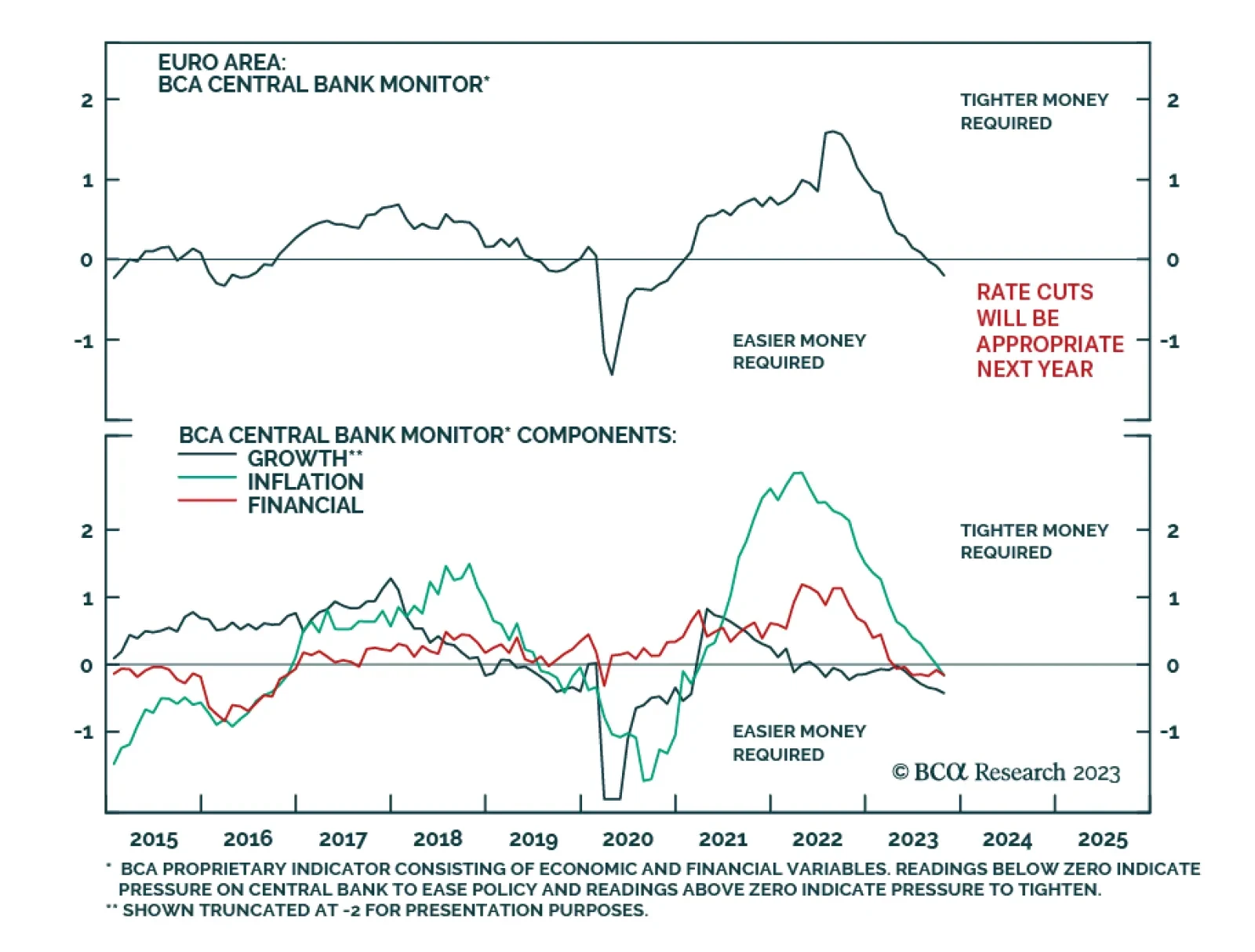

As expected, the ECB kept its policy rate unchanged on Thursday. In the updated macroeconomic projections, the central bank revised down its inflation and growth forecasts for next year. It now expects inflation to ease to 2.7% in 2024 – 0.5 percentage…

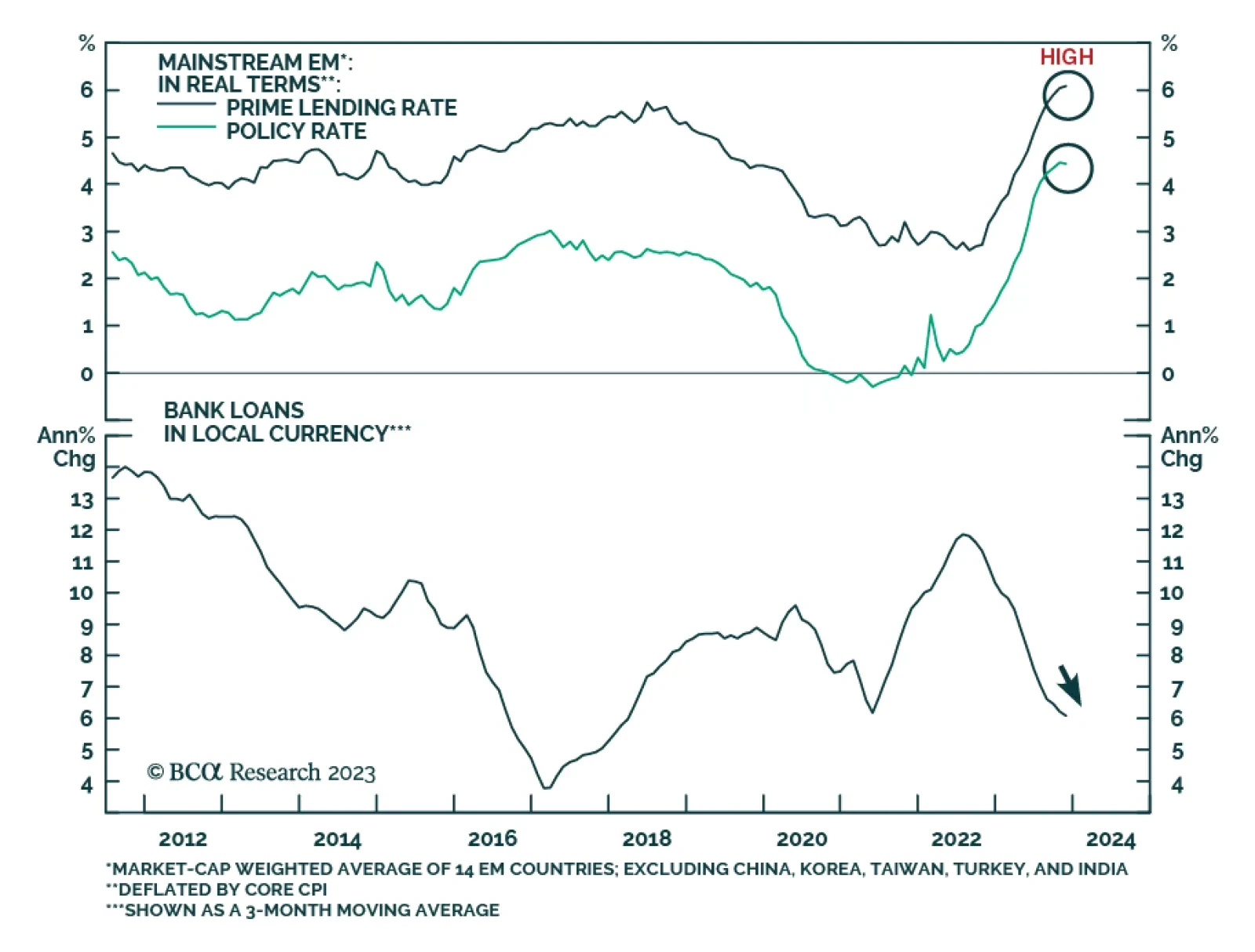

According to BCA Research’s Emerging Markets Strategy service, domestic demand and corporate profits will disappoint across mainstream Emerging Market economies (excluding China, India, Korea, and Taiwan) in H1 2024. Retail sales volume growth has been…

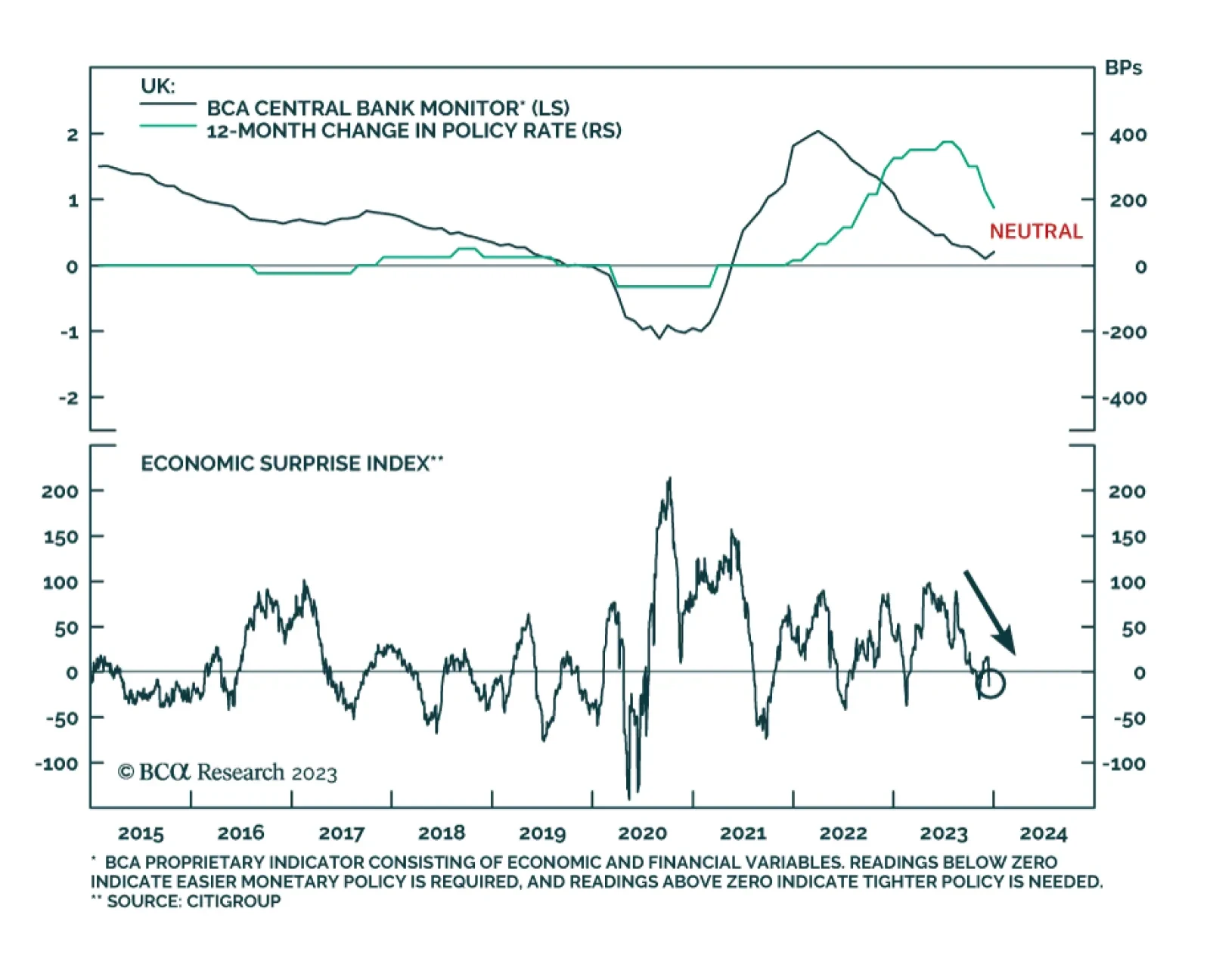

Weaker-than-anticipated economic data caused a sharp decline in UK gilt yields over the past few days with the 10 year yield now at its lowest since May. The weakness in economic data was broad-based across various sectors of the UK economy. In the…

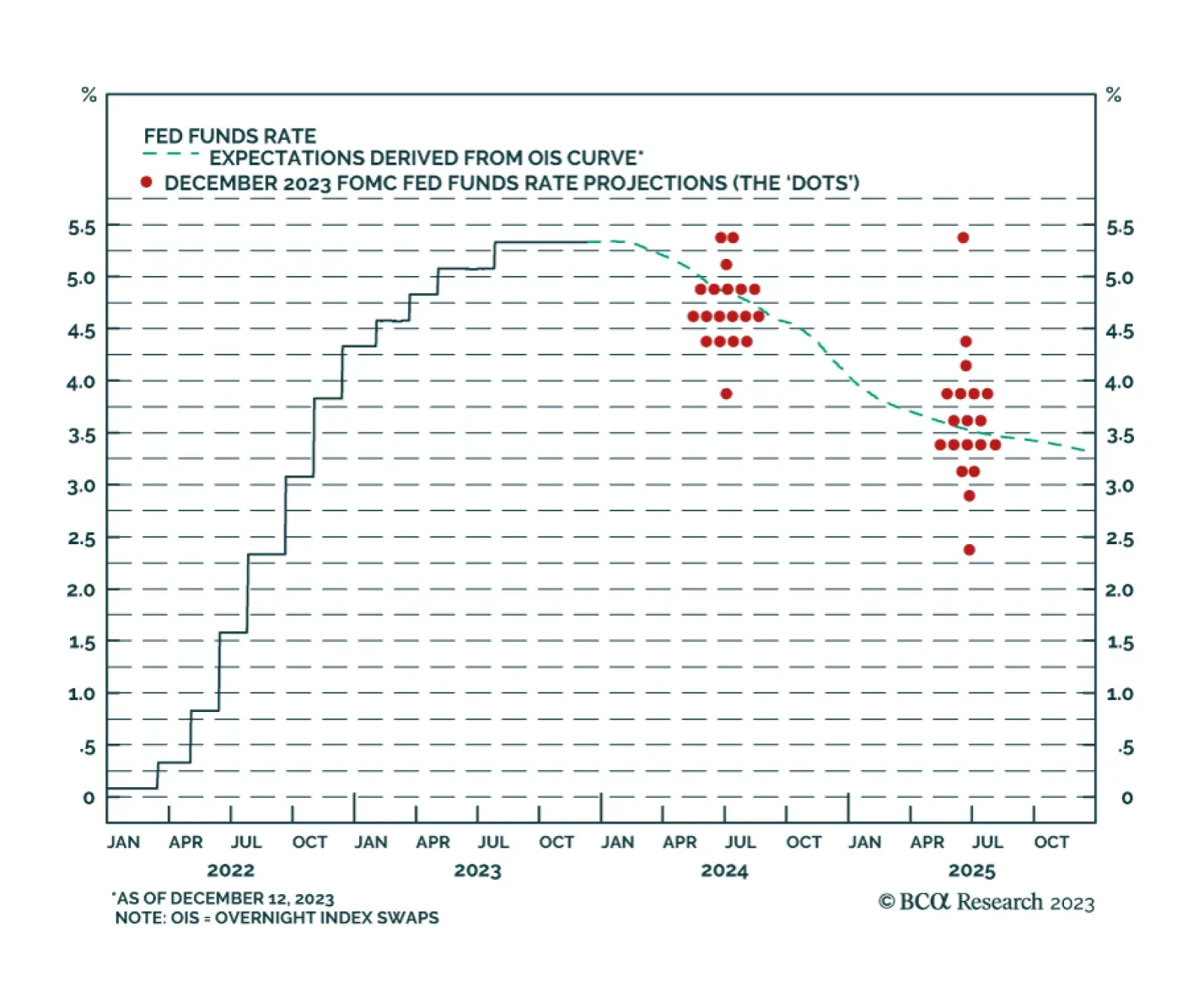

As expected, the Fed kept the policy rate unchanged in the 5.25%-5.50% range on Friday. Although the statement continued to indicate that the Fed is prepared to tighten further, it also acknowledged that there has been a slowdown in economic growth and that…

Our US bond team’s thoughts on this afternoon’s FOMC meeting and yesterday’s CPI release.

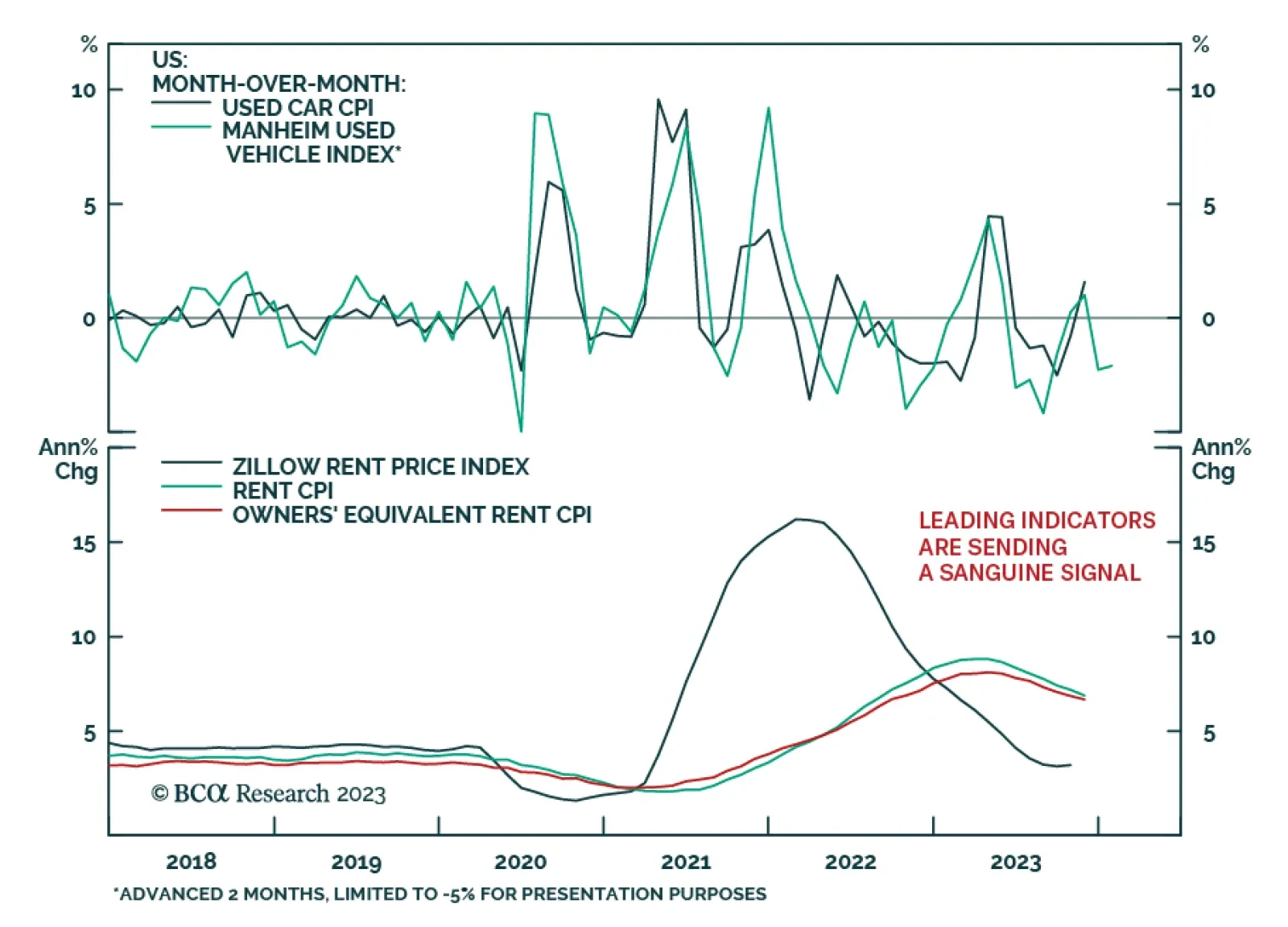

The November US CPI release came in broadly in line with consensus expectations on Tuesday. On an annual basis, headline CPI inflation eased from 3.2% y/y to 3.1% y/y while core inflation was unchanged at 4.0% y/y. On a monthly basis, both headline and core…

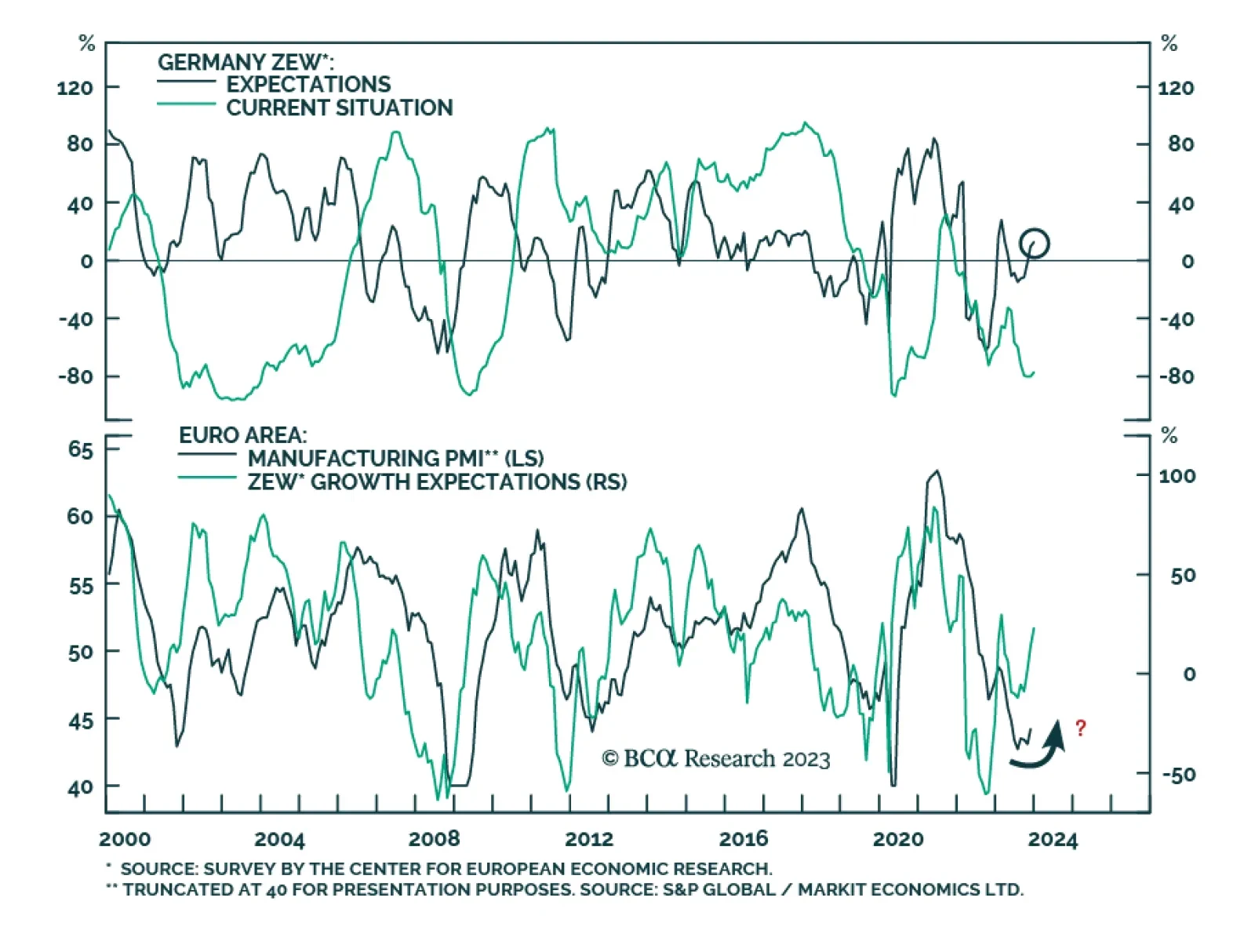

The continued improvement in German investor morale captured by the ZEW survey corroborates other indicators pointing to near-term support for Eurozone stocks. Economic sentiment jumped three points to a 9-month high of 12.8 in December, surprising…