Monetary

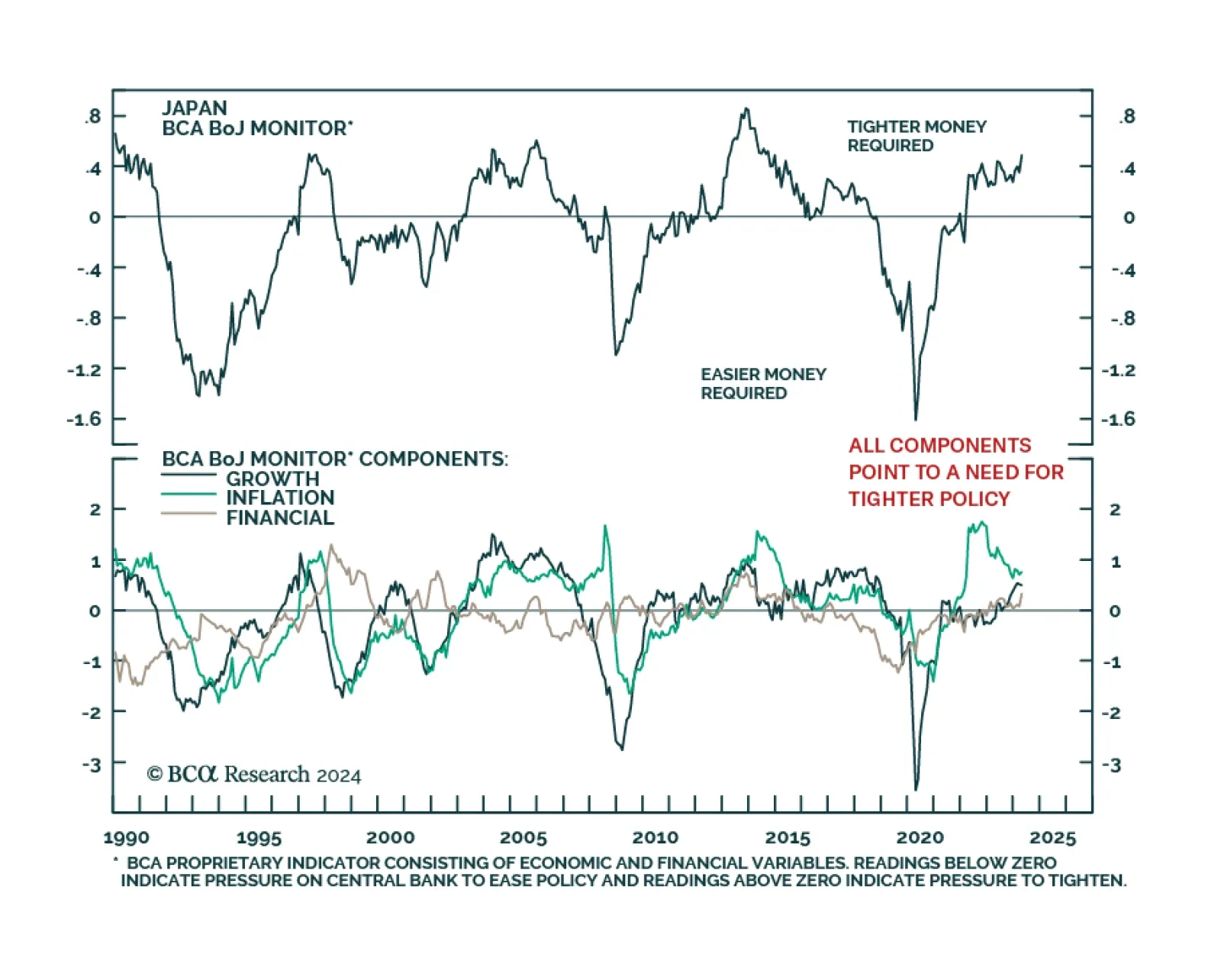

In this insight, we update our thinking on the recent BoJ move in terms of positioning for the yen and JGB yields.

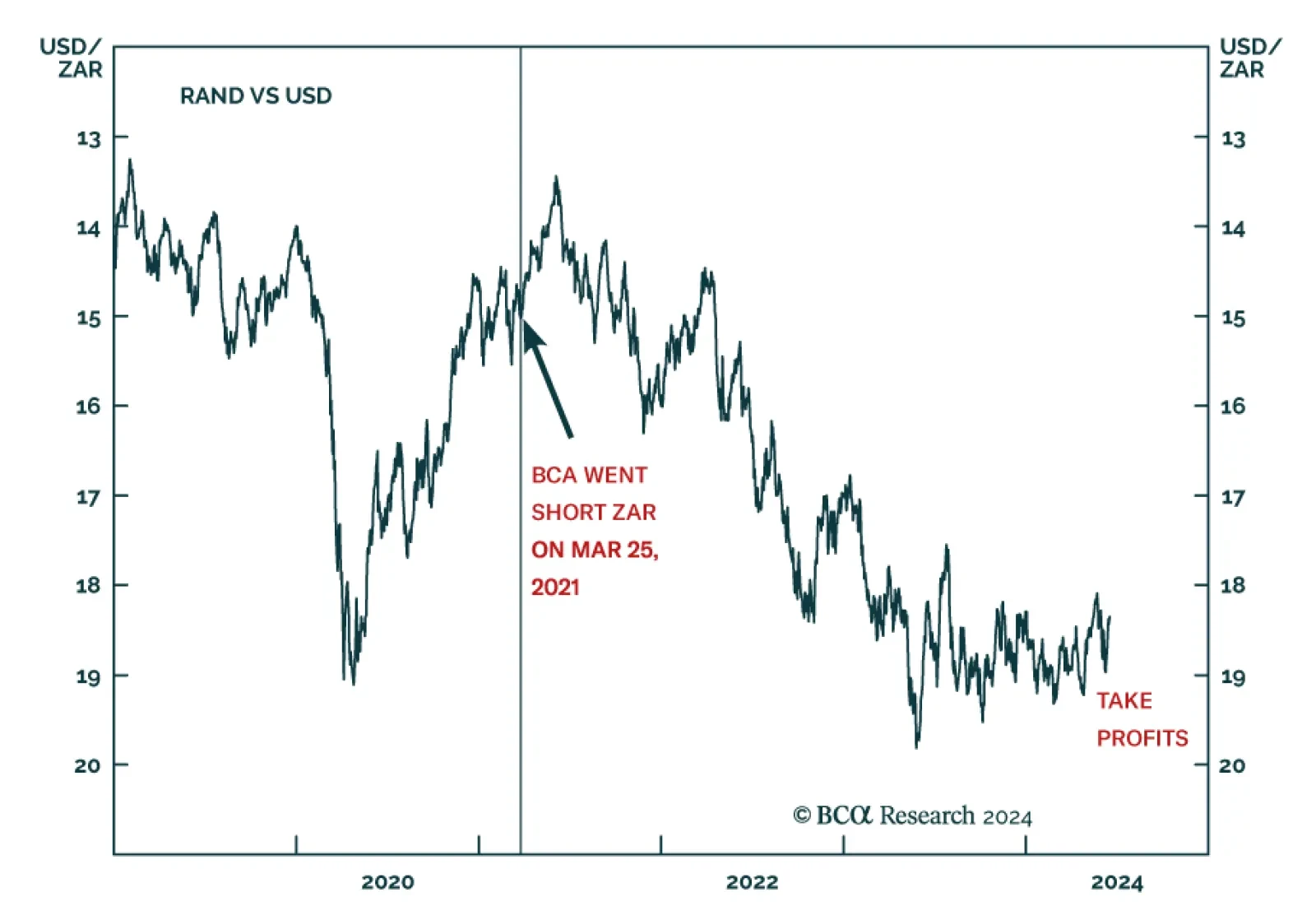

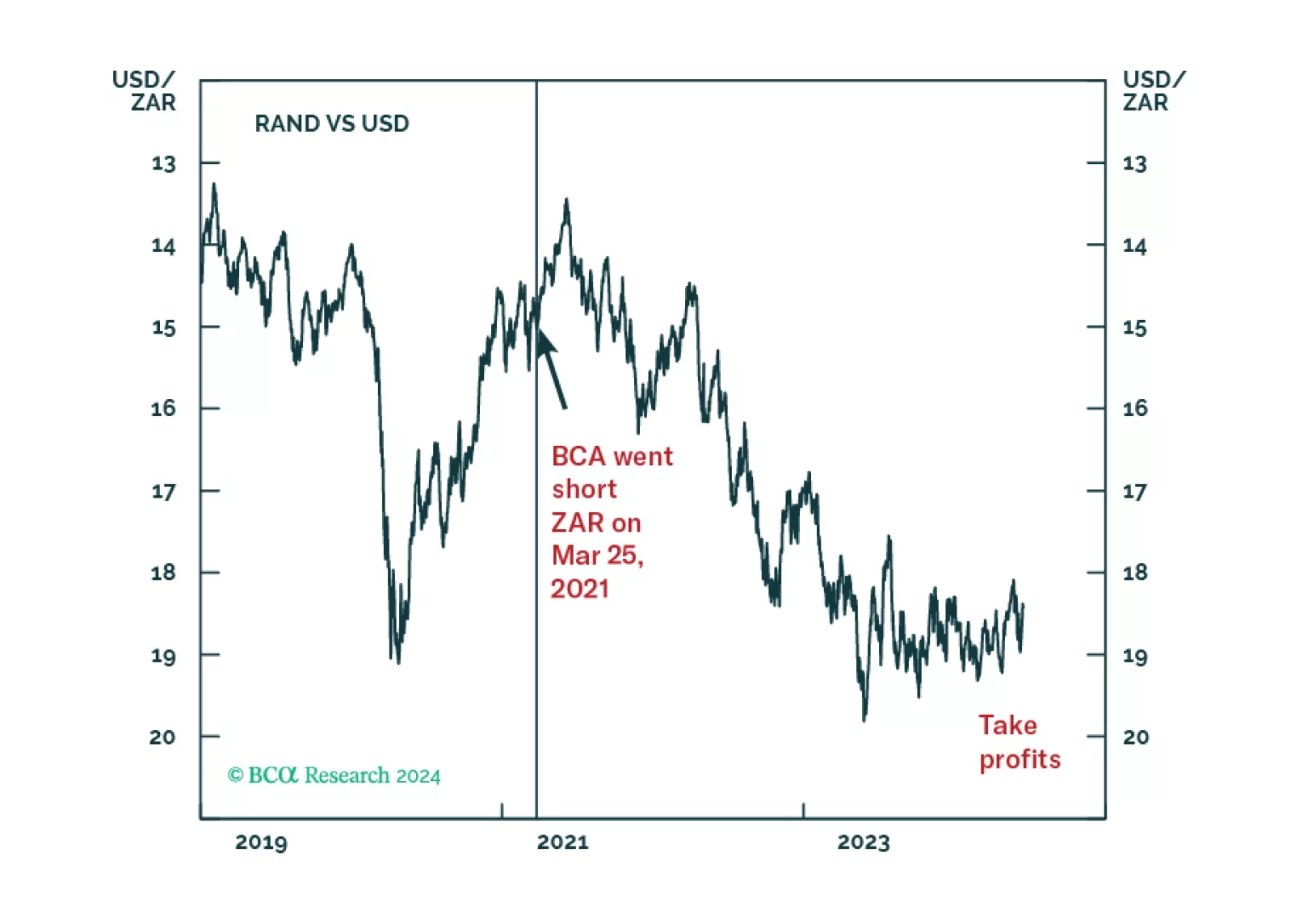

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

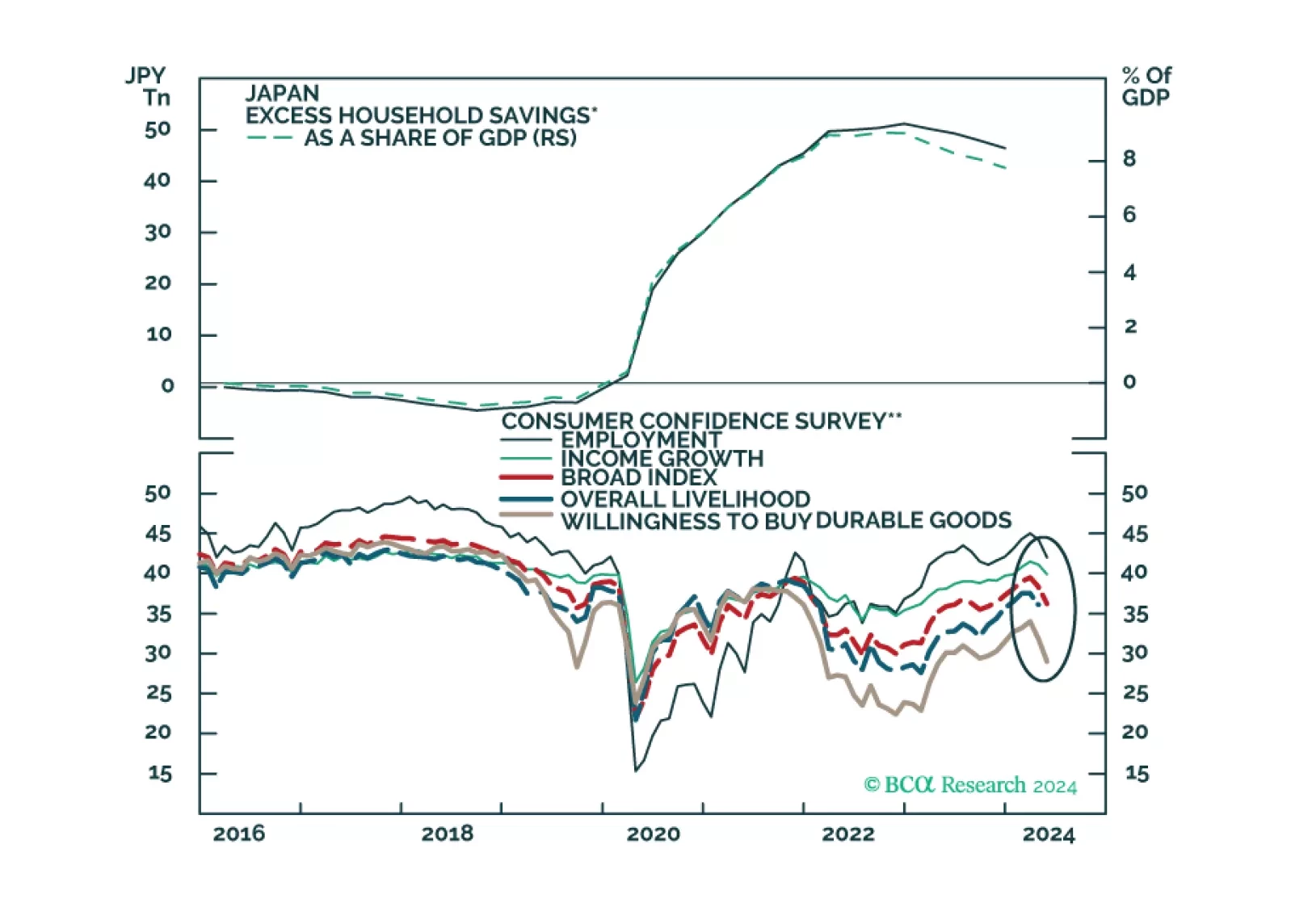

Global consumer spending is likely to slow over the coming quarters, culminating in a major economic downturn in late 2024 or early 2025. Investors should maintain benchmark exposure to equities for now but look to turn more defensive by the end of this summer.

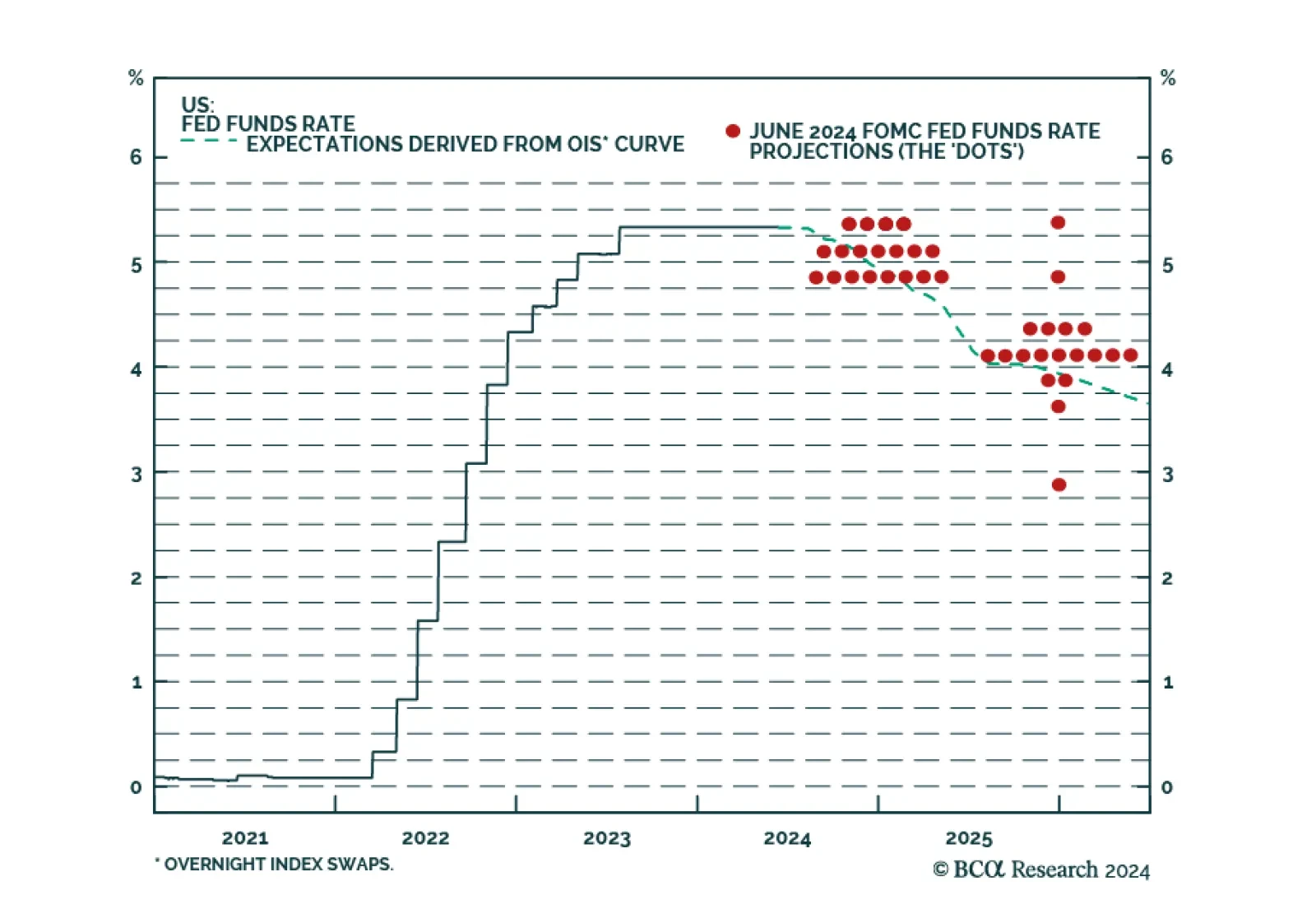

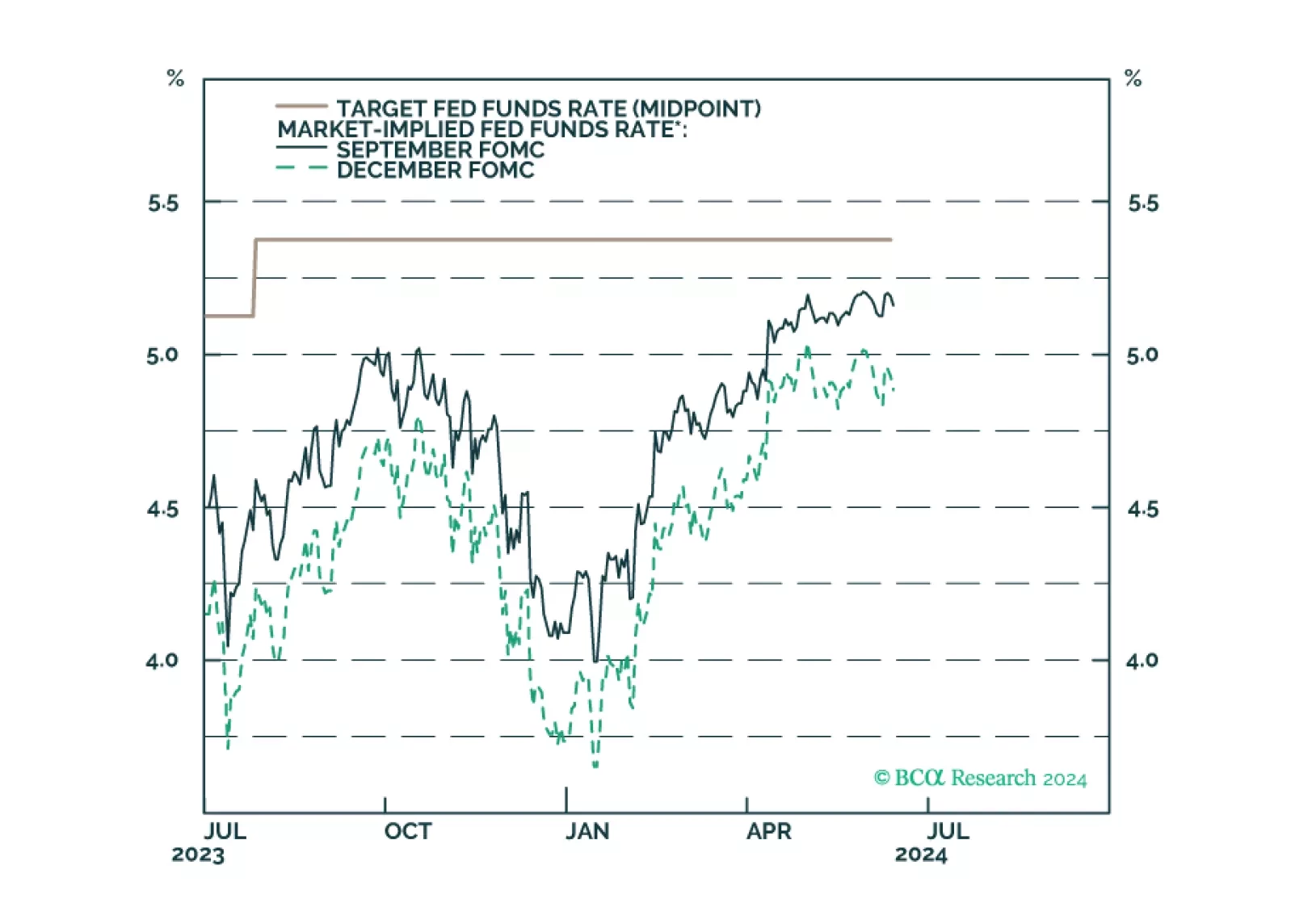

Our reaction to this morning’s CPI report and this afternoon’s FOMC meeting.