Mega Themes

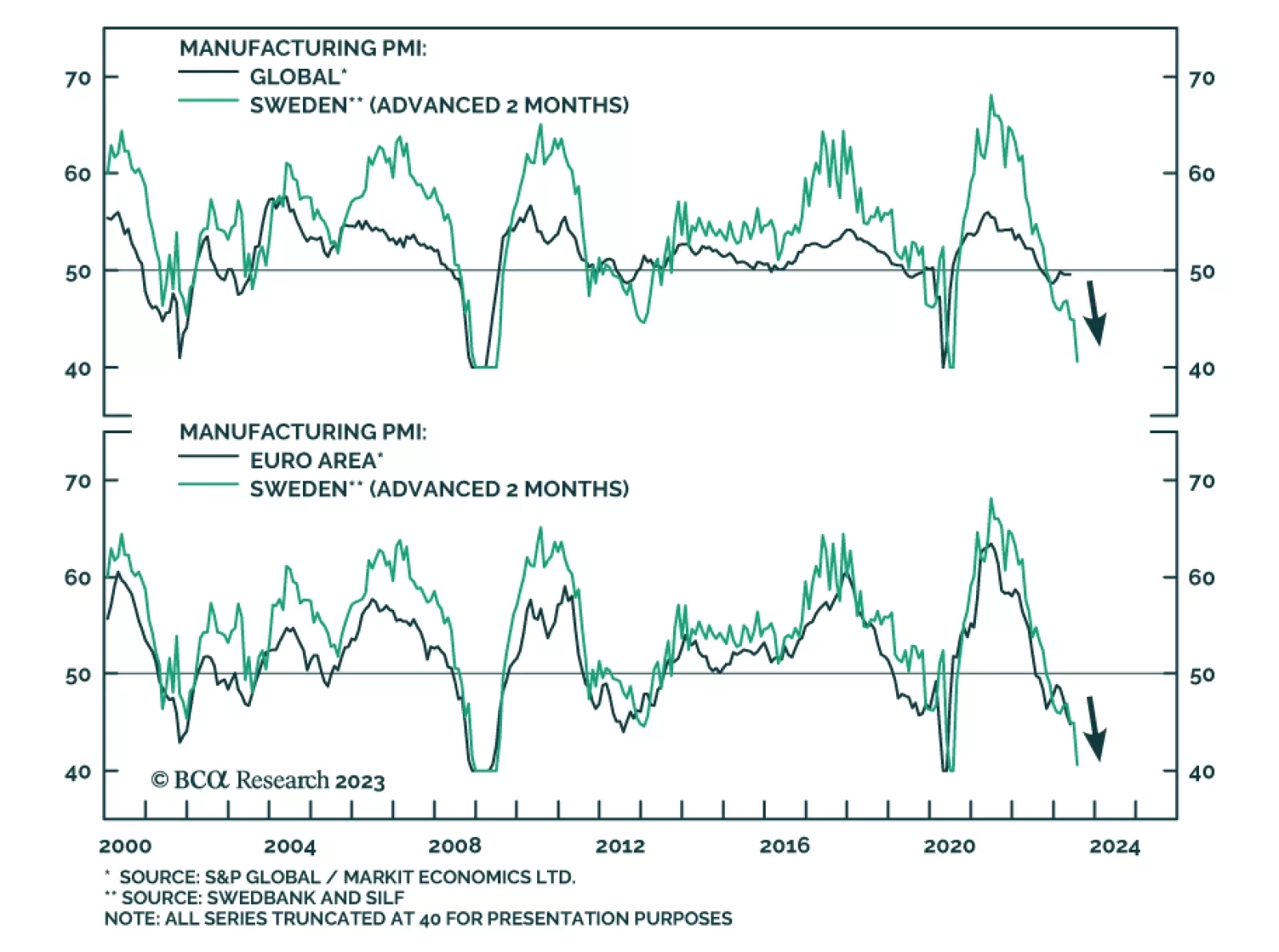

Slowing manufacturing PMI indices globally indicate the slowdown in economic activity will persist. Manufacturing demand for commodities will also soften, weighing on industrial commodity prices. Geopolitical tensions and the race to the green energy transition will upend enmeshed global supply chains, which will also impact manufacturing activity. It is possible that stimulus in China will arrest the decline in the state’s manufacturing activity, which will have positive spillover effects to its key trading partners.

What’s going on? The market-weighted stock market is up. But the equally-weighted stock market is not up. Neither is credit. Neither are industrial metal prices. Neither is the oil price, despite two waves of OPEC output cuts. We explain the dichotomy. Plus: European basic resources stocks can rebound, but Netherlands is likely to reverse.

In this report, we follow up on the upgrade to our US duration stance from last week with a review of our rates views and government bond allocations outside the US. We conclude that while we now find US Treasuries to be more attractive from a value perspective, even better value is available in euro area and UK government debt.