Mega Themes

The normalization of oil storage markets in the Northern Hemisphere; strong demand, aided by China stimulus this year; and continued production discipline supports our view Brent prices likely have bottomed, and will move higher from here. We raised our 2023 Brent forecast $2/bbl to $92/bbl. Our forecast for next year is revised upward by $5/bbl to $120/bbl. Price risk remains to the upside, particularly if KSA exercises its option to extend production cuts of 1mm b/d.

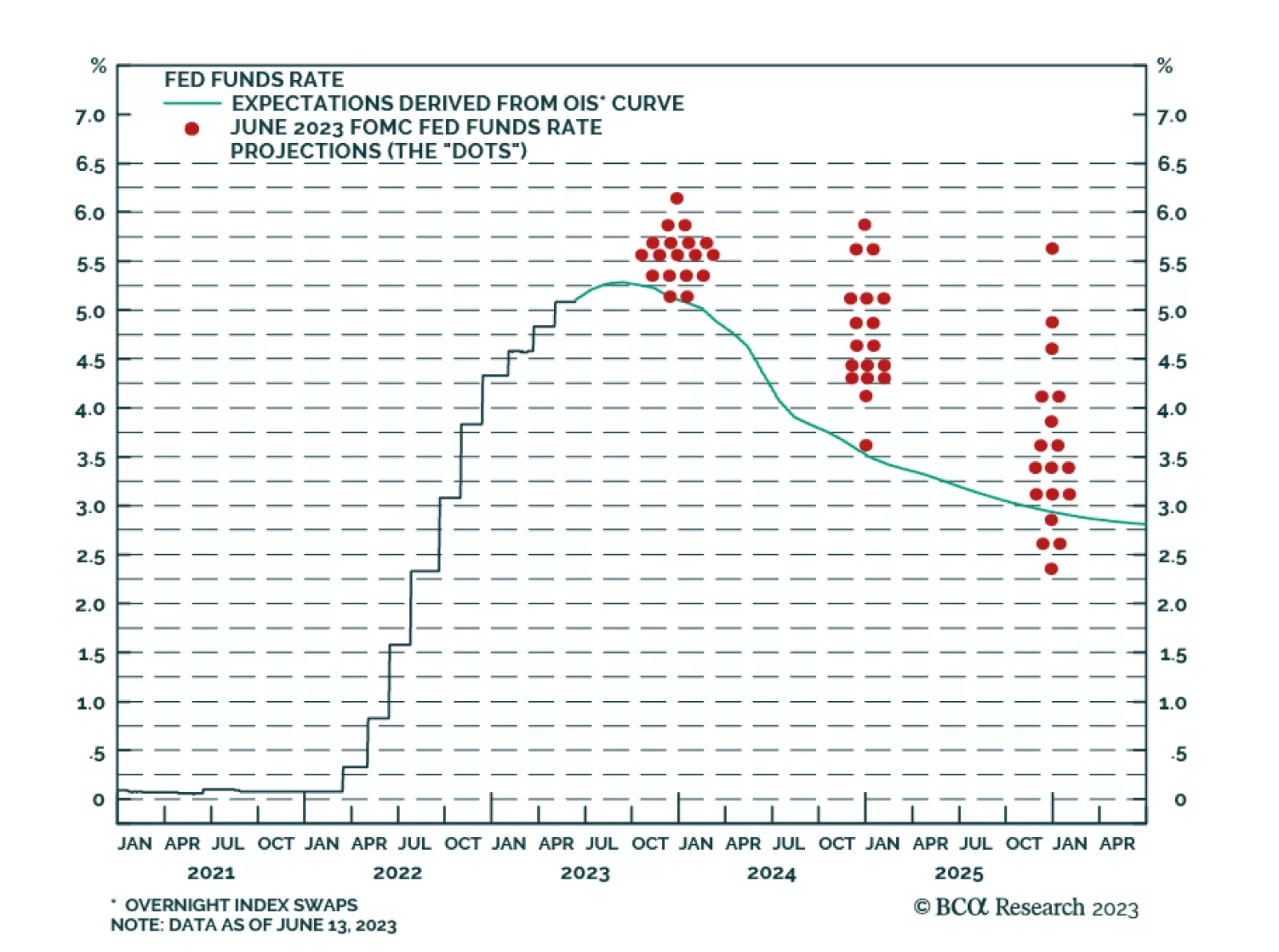

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.

As the major central banks once again mull their policy options, they face a daunting task. They must phase-transition inflation back to imperceptible, without phase-transitioning unemployment to perceptible. This report explains why this will prove impossible, and what central banks will likely prioritise. Plus: the collapsed complexity of the recent stock market rally signals excessive trend-following. Until the complexity normalises, we are reluctant to chase the rally.

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.

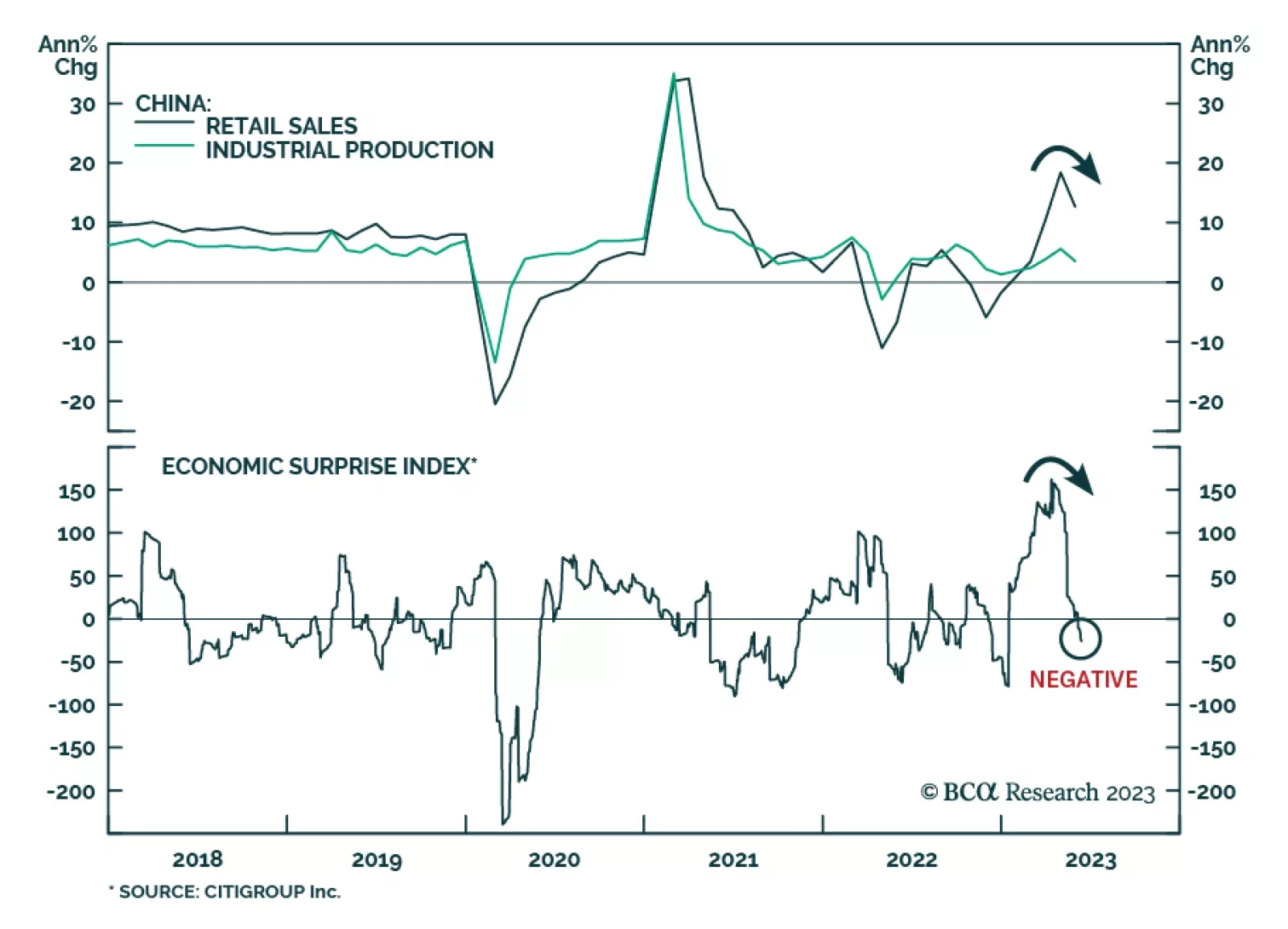

Policymakers will likely continue to stimulate domestic demand via targeted measures and piecemeal stimulus. Yet, the economy will disappoint unless Beijing provides “irrigation-style” stimulus. The latter is not our base case scenario.