Mega Themes

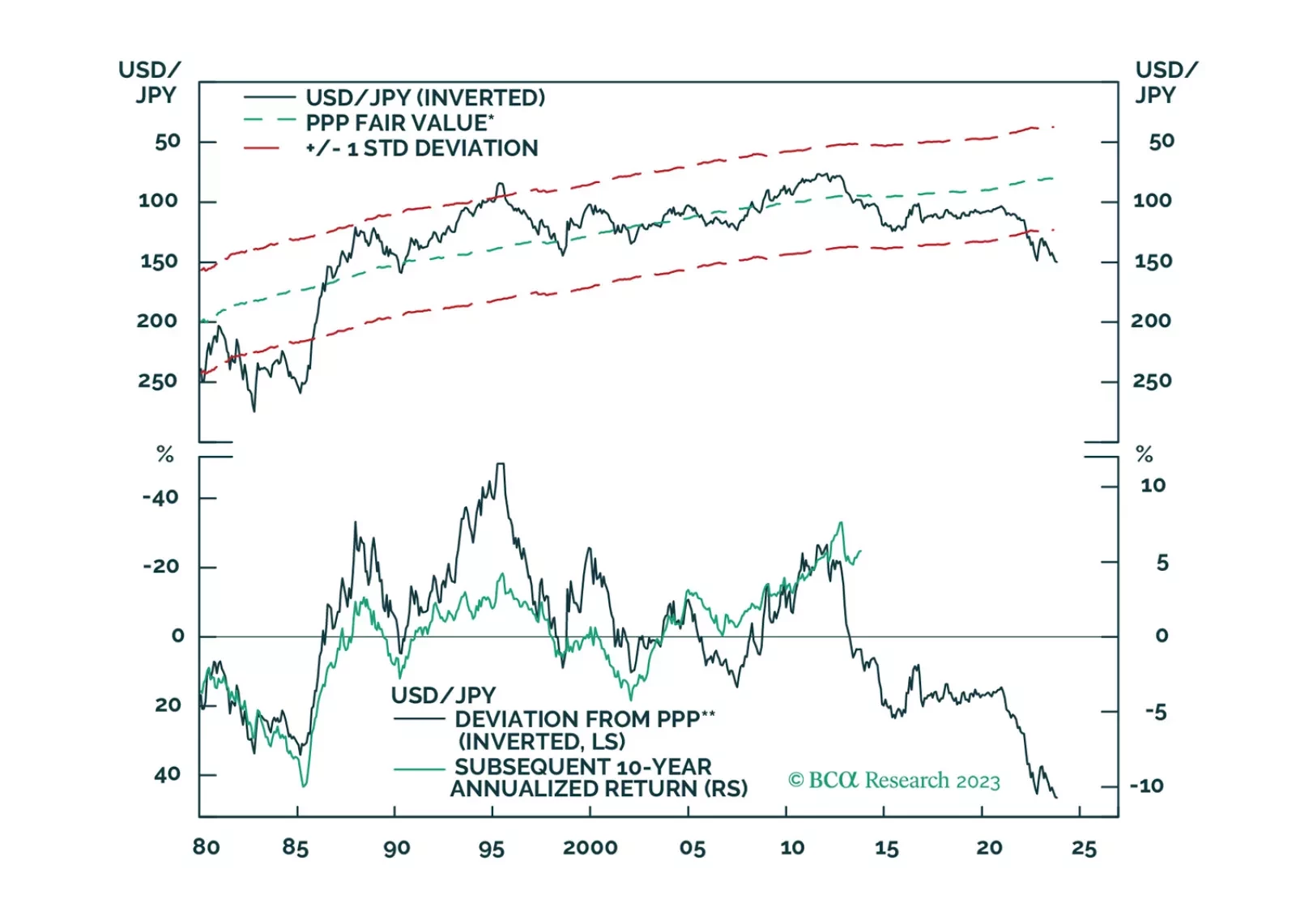

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

The Hamas attack against Israel, timed almost 50 years to the day after a similar surprise attack on Yom Kippur of 1973, has evoked parallels with the 1970s. Parallels not only with Middle Eastern geopolitics then and now, but also with inflation, economics, and financial markets. In this report, we explain what went wrong in the 1970s and whether the mistakes will be repeated. Plus: the sharp sell-offs in some Latin American currencies are reaching a potential turning-point.

In this report, we present the quarterly review of the Global Fixed Income Strategy Model Bond Portfolio. The portfolio remains positioned for slower global growth momentum over the next 6-12 months, favoring government bonds over corporate debt. The portfolio also favors government bonds in countries flirting with recession where policy rates are too high (core Europe & the UK).

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.

As global financial institutions like the IMF draw attention to the real-estate crisis in China, the CCP will be forced to step up regulatory and restructuring efforts to contain its spread and limit further contagion domestically and globally. The Party also will be forced to deliver stronger fiscal- and monetary-policy support to beleaguered banks and developers. We expect it to do so, which keeps us bullish energy and metals. Failure raises the odds of a collapse in the property markets, which would be socially destabilizing, and lead to greater risk aversion and volatility globally.

Domestic auto sales in China will likely have anemic growth over the next three years. Yet, Chinese automakers are set to gain a larger share of the global market. Go long Chinese automakers / short global ones.

The sharp sell-off in long duration bonds (ticker TLT) has reached the collapsed 130-day complexity that implies a probable and playable rebound. More strategically, long-duration bonds yielding close to 5 percent are an excellent structural investment assuming central banks choose to slay inflation and the cost is a near-term recession. We discuss how to time and how to play the potential rebound.

The market has been held hostage by surging rates. Zombie companies are “alive” and are multiplying – they are highly sensitive to surging borrowing costs. Underweight Utilities to reduce portfolio duration. Maintain neutral positioning of Basic Materials but take a granular approach to allocations within the sector.

The EU’s transition to a carbon tax launched this week via its Carbon Border Adjustment Mechanics (CBAM) will lead to higher inflation in the medium term (3 – 5 years out), and will stoke consumer (i.e., voter) antipathy if it becomes effective in 2026. As a result, the tax will be watered down. Food and energy prices are particularly at risk, as imported fertilizers, and electricity-generation and -transmission components made from steel and aluminum are affected by the CBAM. We remain long oil, gas and metals equity exposure via the XOP, XME and COMT ETFs. We also remain long gold to hedge inflation.

There is a connection between the bond market meltdown and Republican Party’s meltdown. Investors should expect more short-term financial market volatility as a result of the triple whammy of high bond yields, high oil prices, and a strong dollar.