Materials

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

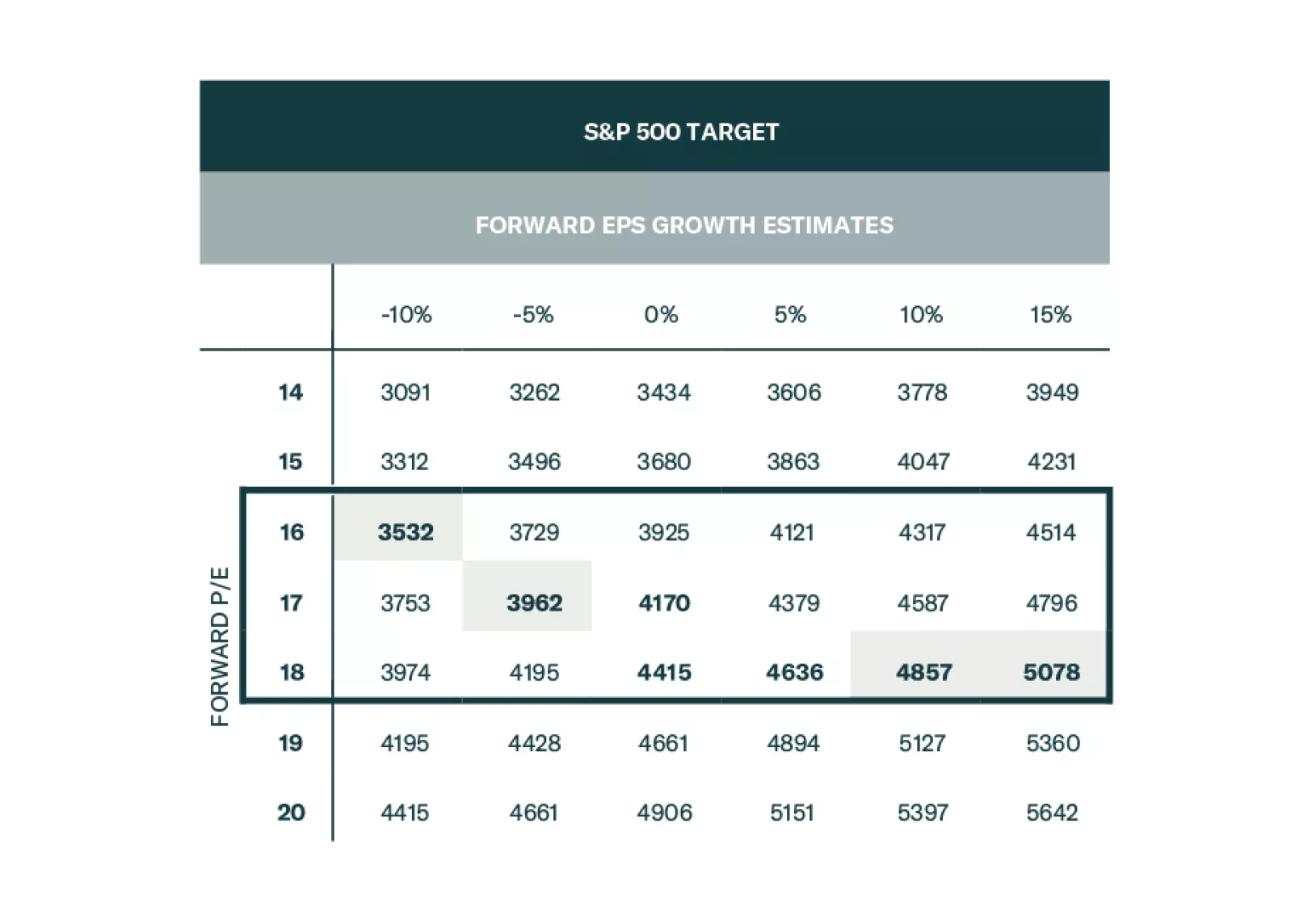

Disinflation coupled with sticky wage growth is likely to result in either a second wave of inflation or layoffs and a recession. In the meantime, market expectations for sales, growth, and margins are overly optimistic and are inconsistent with macroeconomic headwinds. We recommend gradually realigning the portfolio to a more defensive stance.

Explore the eight main themes that will drive the returns of European assets in 2024.

We expect the US economy to slow and potentially downshift into a recession sometime in 2024, as tighter monetary policy weighs on consumers and businesses. In addition, (geo)political tensions may increase market volatility. The risk/return for US equities is unfavorable. We recommend that our clients reduce portfolio beta and increase allocations to defensives and quality growth.

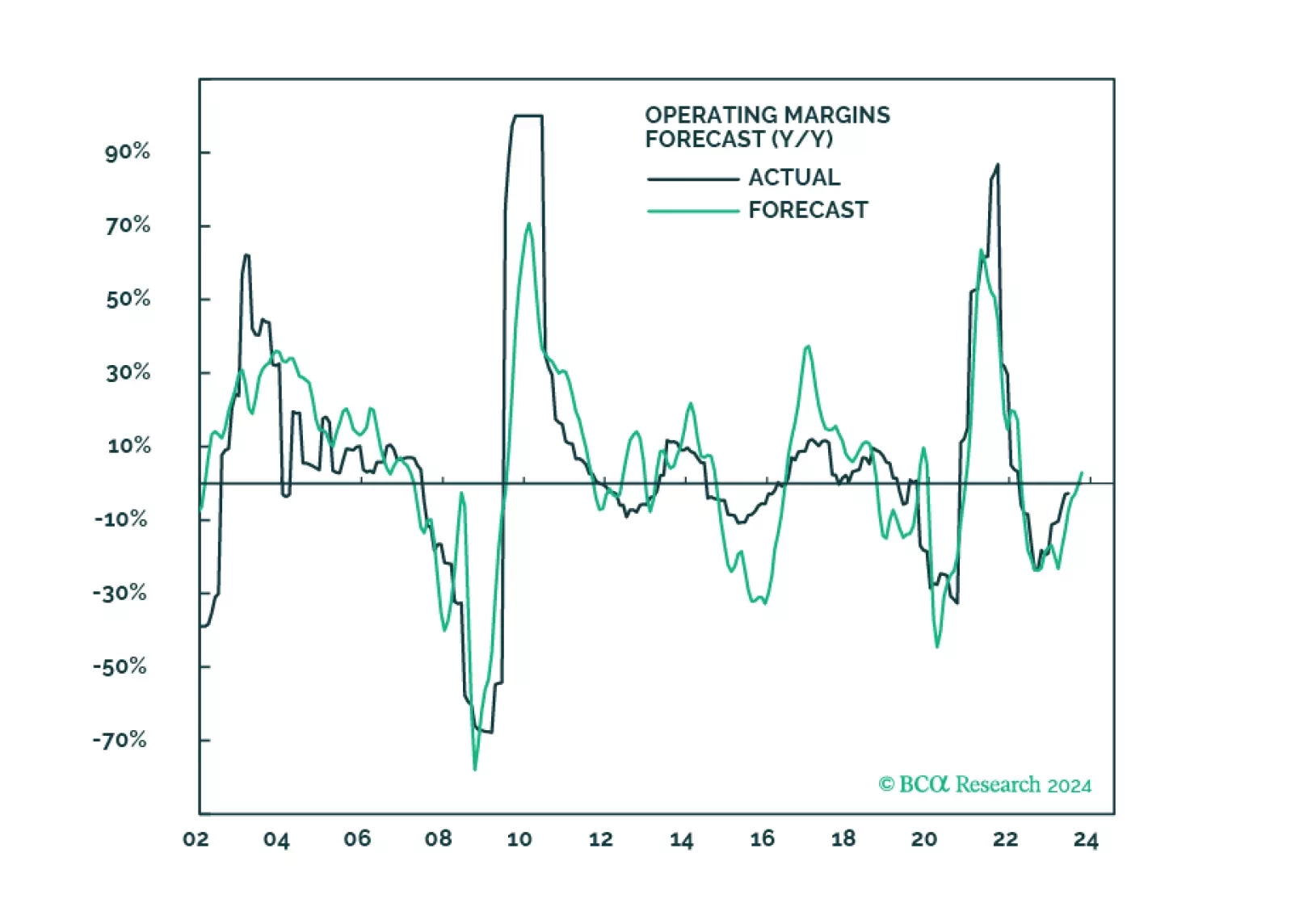

Q3-2023 is expected to mark the end of the earnings recession for the past three quarters, opening the door to positive earnings growth. Whether that would be sustainable or will sputter once the recession settles in as expected in 2024 remains to be seen. However, much of earnings growth is already priced in.

The market has been held hostage by surging rates. Zombie companies are “alive” and are multiplying – they are highly sensitive to surging borrowing costs. Underweight Utilities to reduce portfolio duration. Maintain neutral positioning of Basic Materials but take a granular approach to allocations within the sector.

European stocks and the euro continue to weaken; soon, they will test the bottom of their recent trading range. Which sectors can protect investors against this downdraft?