Market Returns

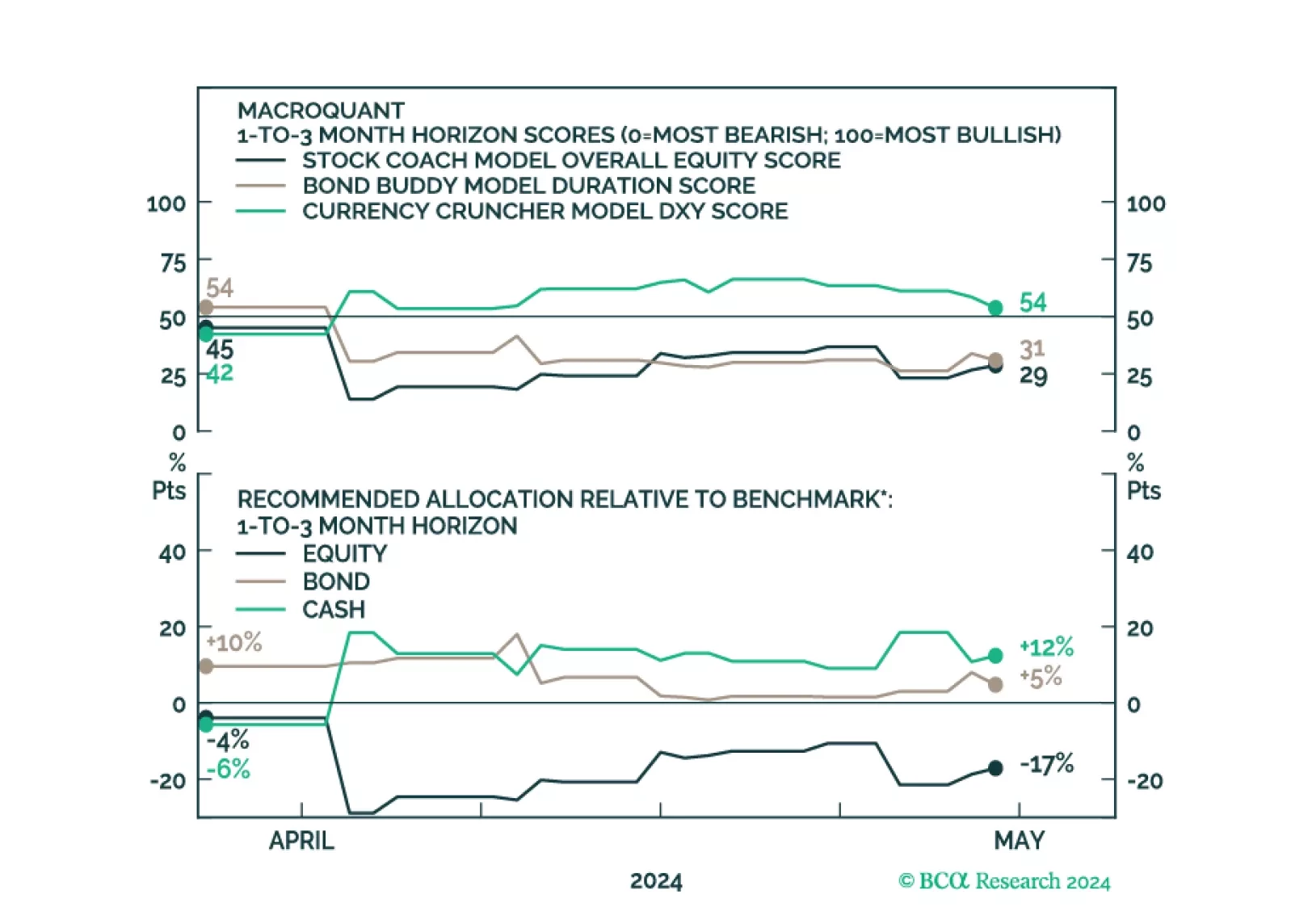

MacroQuant downgraded equities from neutral to underweight on a 1-to-3 month horizon. The model suggests increasing exposure to cash.

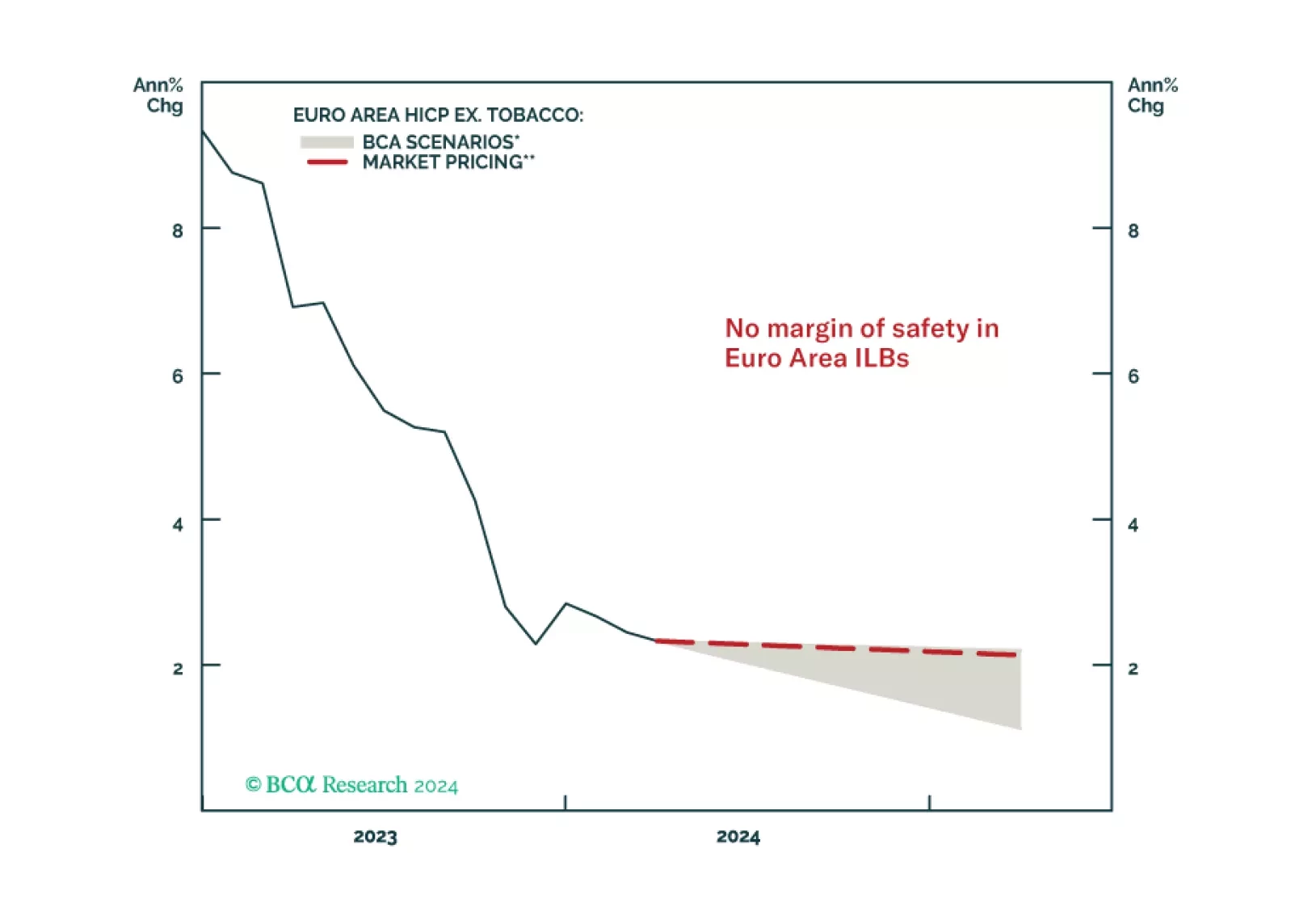

In this Special Report, we introduce our Euro Inflation-Linked Golden Rule – a framework to profitably trade and invest in Euro Area inflation-linked bonds versus nominals. The Rule is currently signaling that nominal government bonds should outperform inflation-linked bonds over the next year as disinflation in the Euro Area continues.

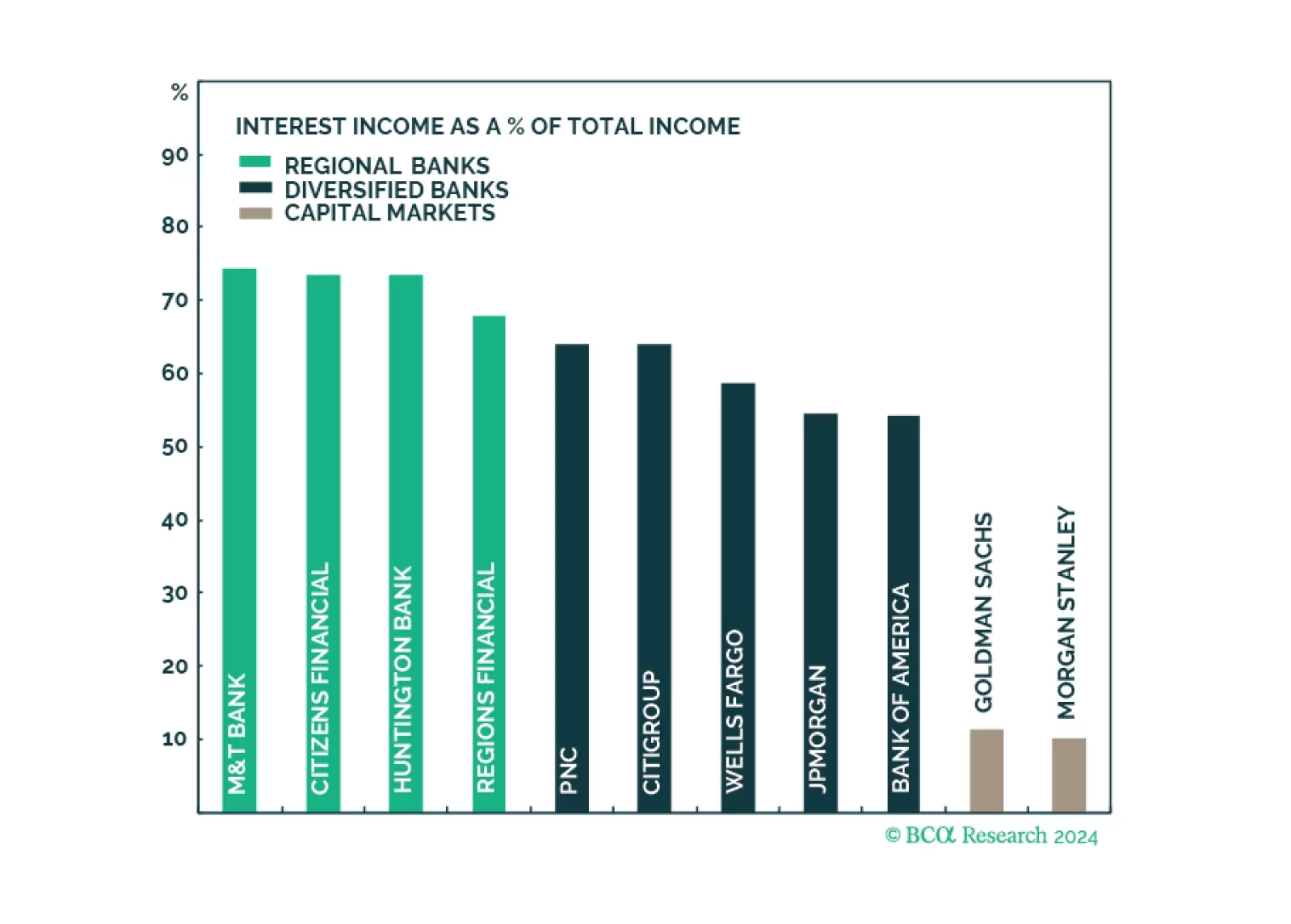

Q1 earnings results of the largest US banks have demonstrated that the engine of recent growth in profitability, NII, has faltered as funding costs are rising fast. However, the resurgence in non-NII thanks to a revival in corporate activity has been a saving grace. Earnings growth appears to have bottomed, while valuations are attractive. To play up portfolio exposure to an upcoming surge in capital markets activity, and minimize exposure to declining profitability in traditional banking services, overweight Diversified Banks and Capital Markets, and underweight Regional Banks.

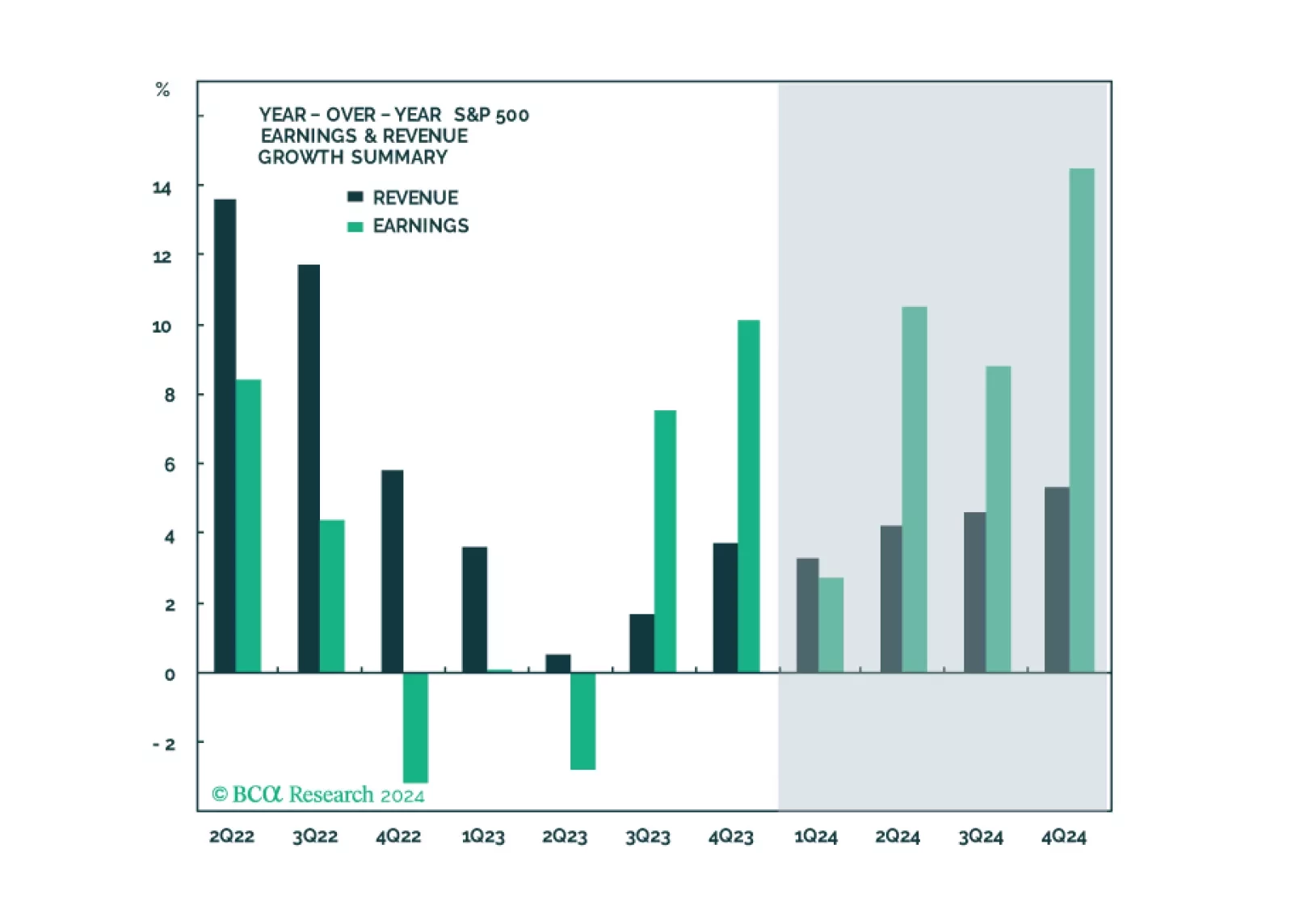

In this note, we preview the Q1-2024 earnings season, give our take on expectations and share what we will be watching.

MacroQuant downgraded equities from overweight to neutral on a 1-to-3 month horizon. The model maintains a negative view on stocks over a 12-month horizon.

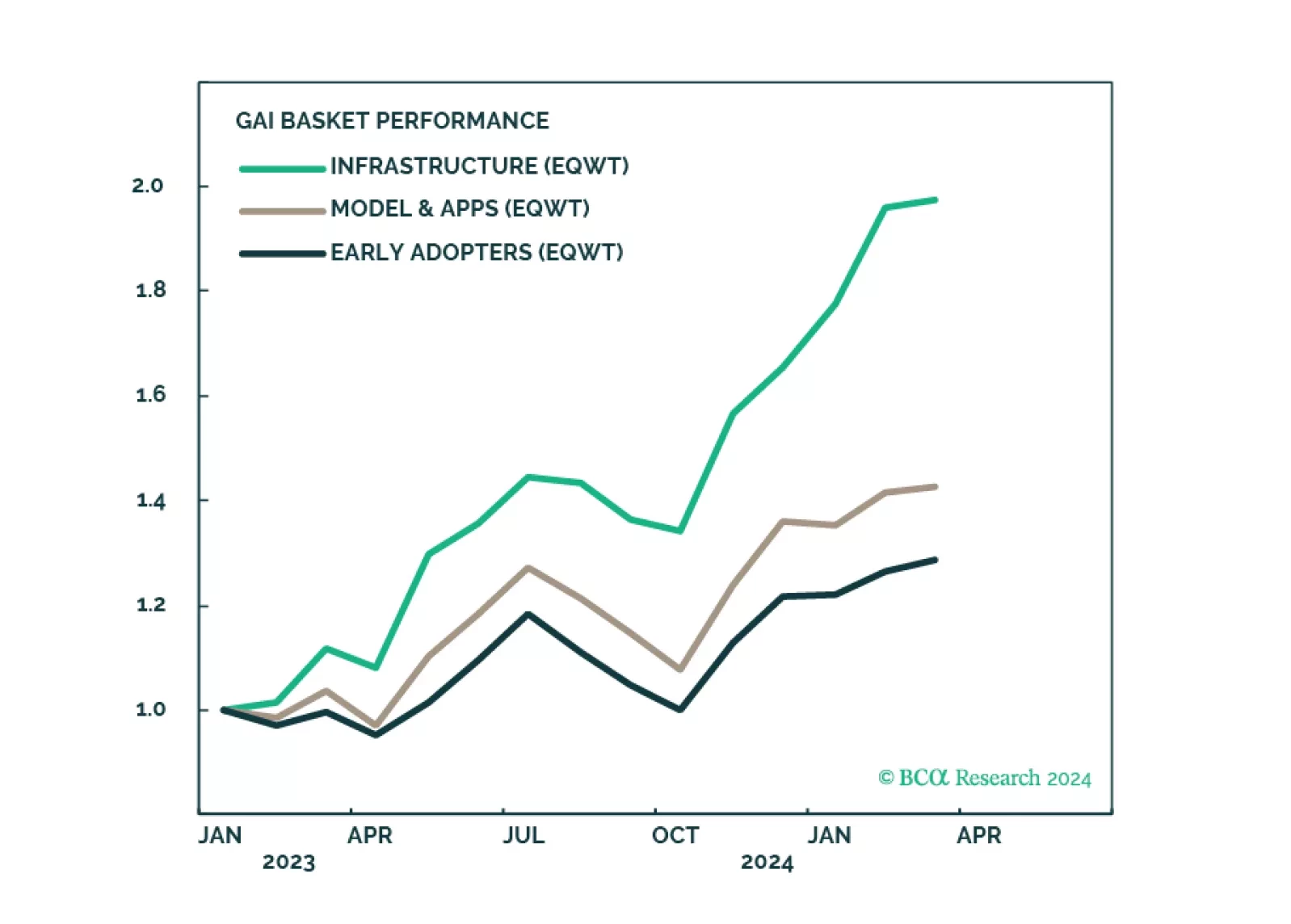

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

We assess where emerging markets debt is on a strategic and cyclical basis. We find it has benefited from local central banks boosting their inflation-fighting credentials and governments improving financial stability. As a result, EM debt is behaving less like a risk-on asset, changing the role it plays in a global portfolio. We also expand our asset allocation playbook by assessing how the asset class behaves across the business cycle. While EM debt is more than a risk-on play, we suggest investors stay cautious on a cyclical horizon.

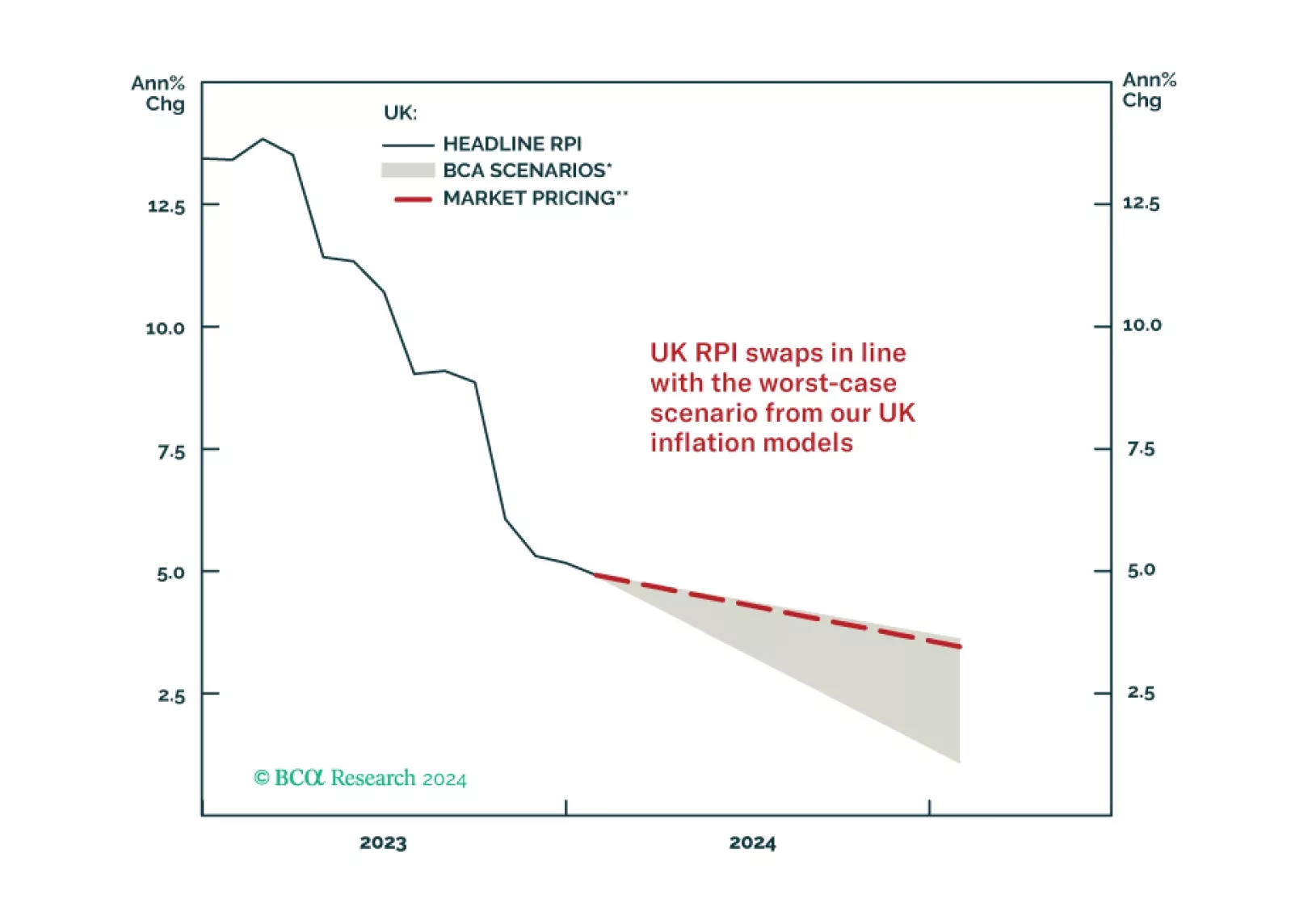

In this Special Report, we introduce our UK Linkers Golden Rule – a framework to profitably trade and invest in UK inflation-linked bonds versus nominal UK gilts. The Rule is currently signaling that nominal Gilts should outperform UK linkers over the next year as UK inflation slows.