Market Returns

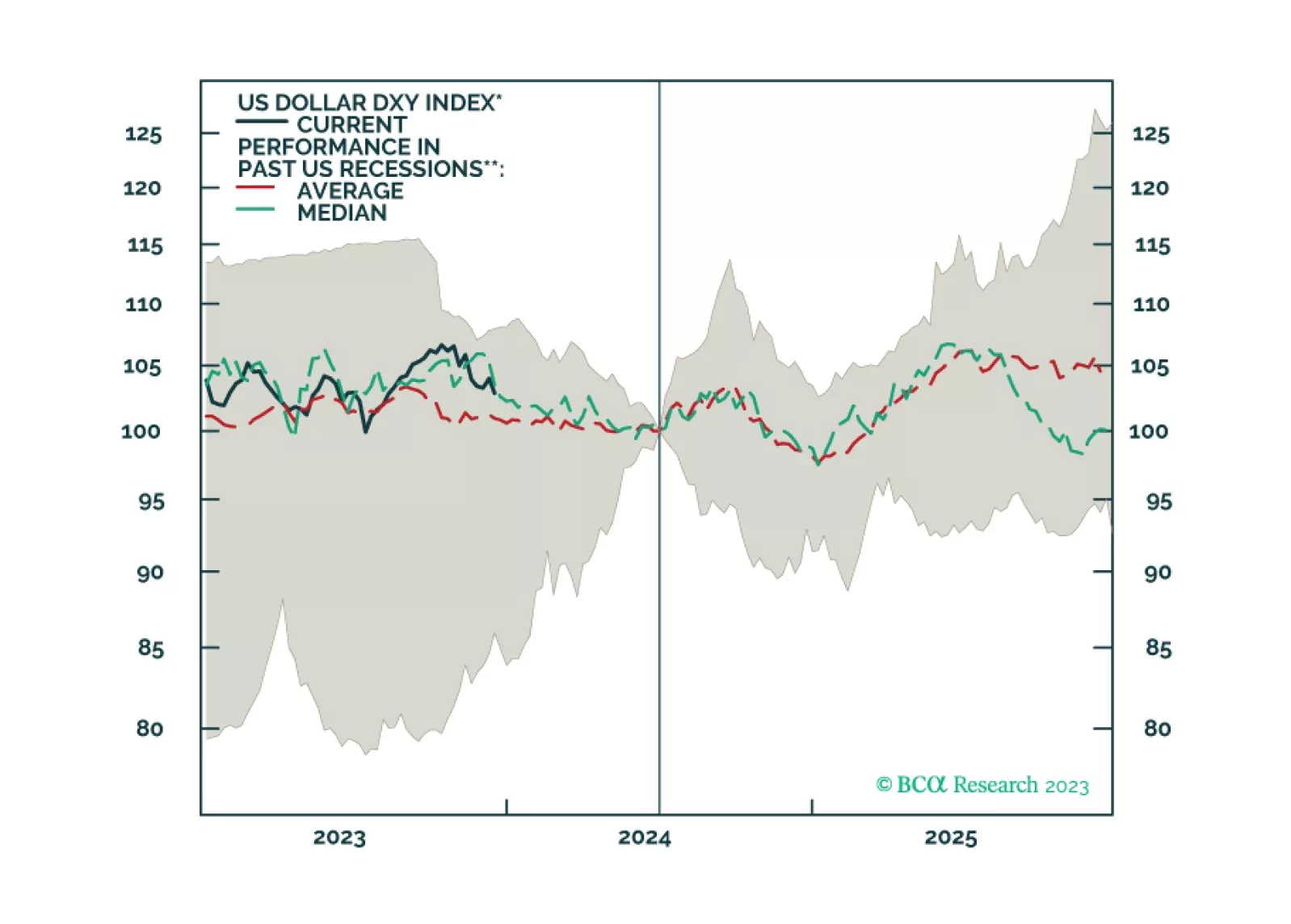

In this week’s report, we present our dollar view for 2024 and beyond, with a few trade ideas.

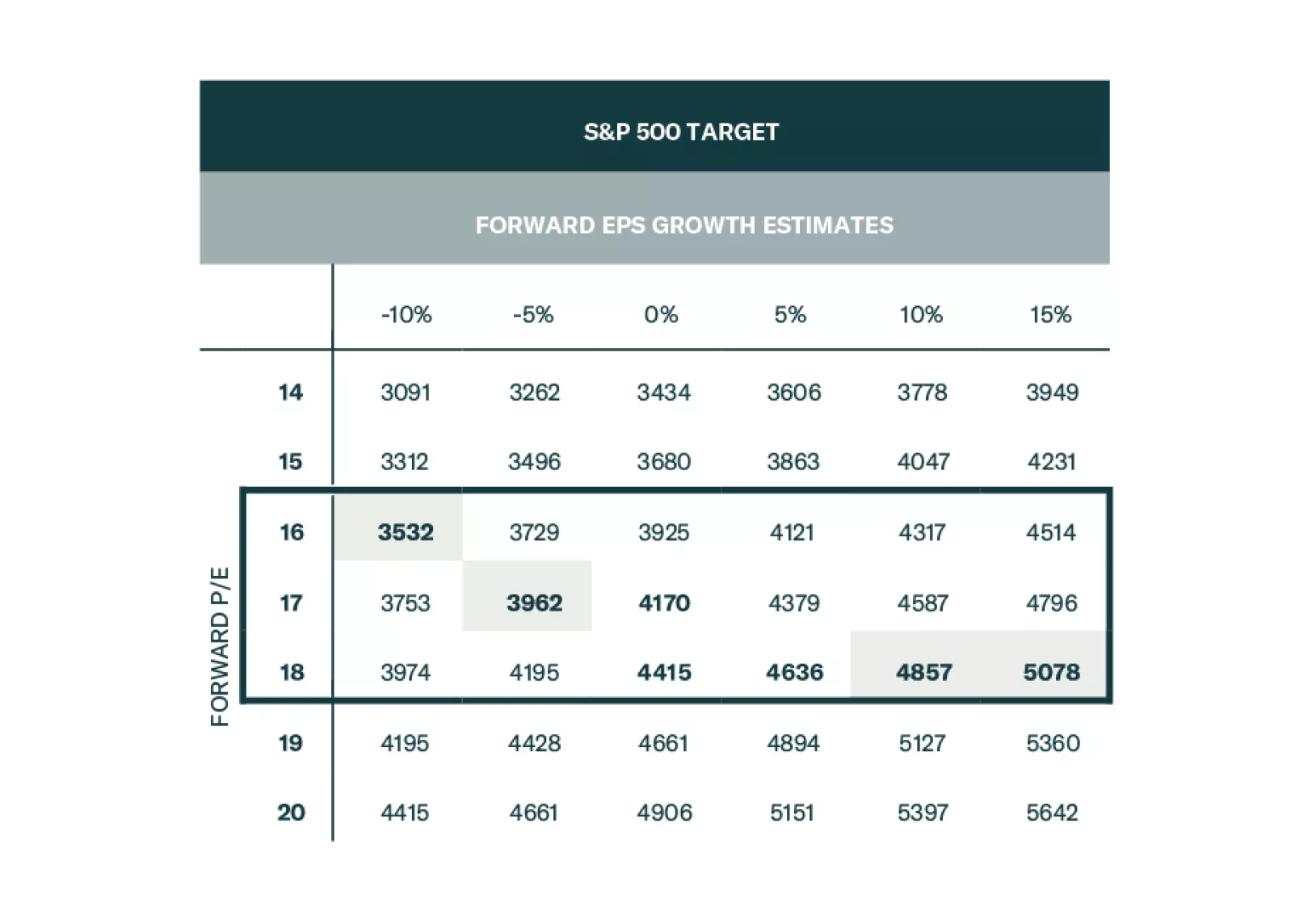

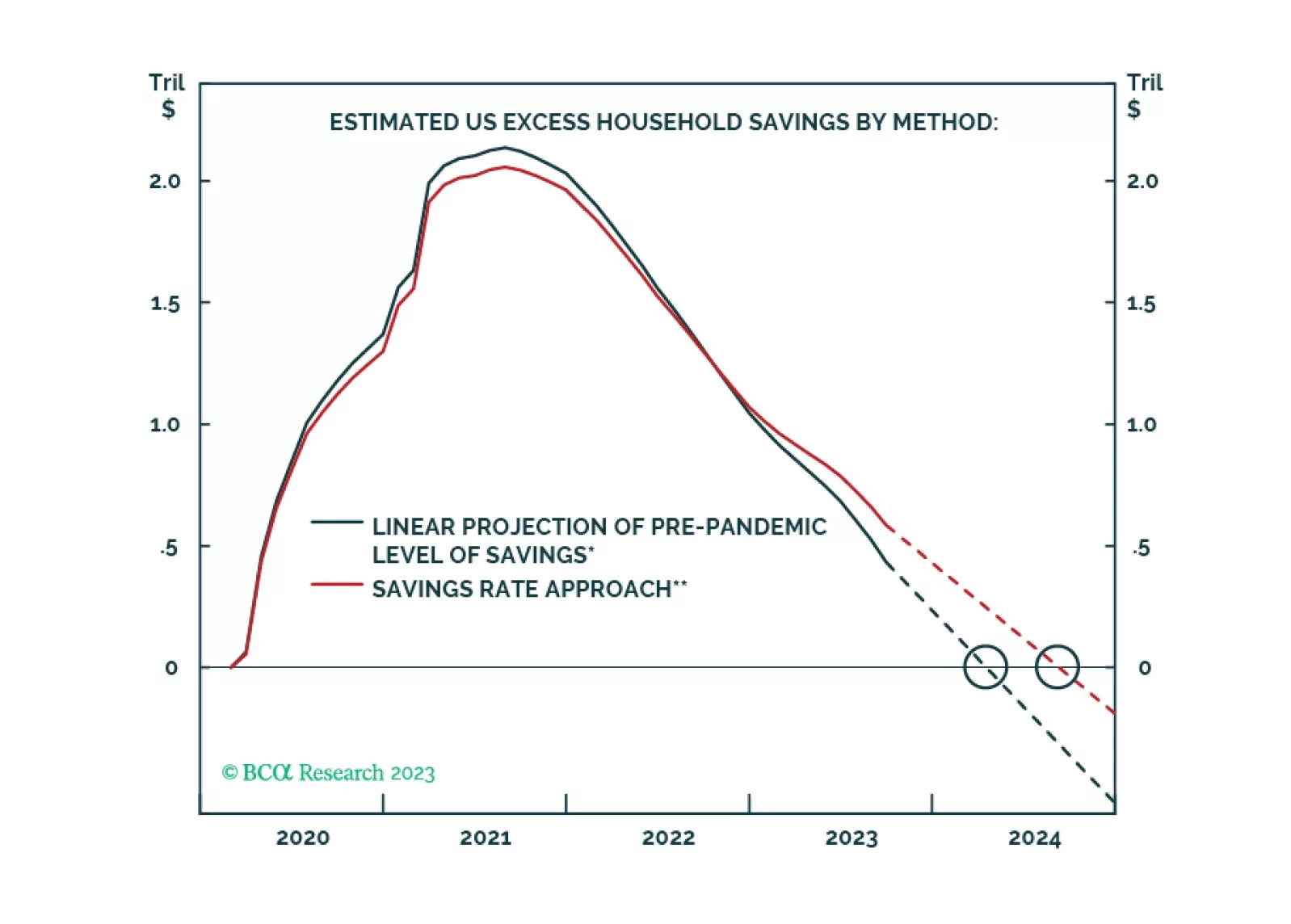

We expect the US economy to slow and potentially downshift into a recession sometime in 2024, as tighter monetary policy weighs on consumers and businesses. In addition, (geo)political tensions may increase market volatility. The risk/return for US equities is unfavorable. We recommend that our clients reduce portfolio beta and increase allocations to defensives and quality growth.

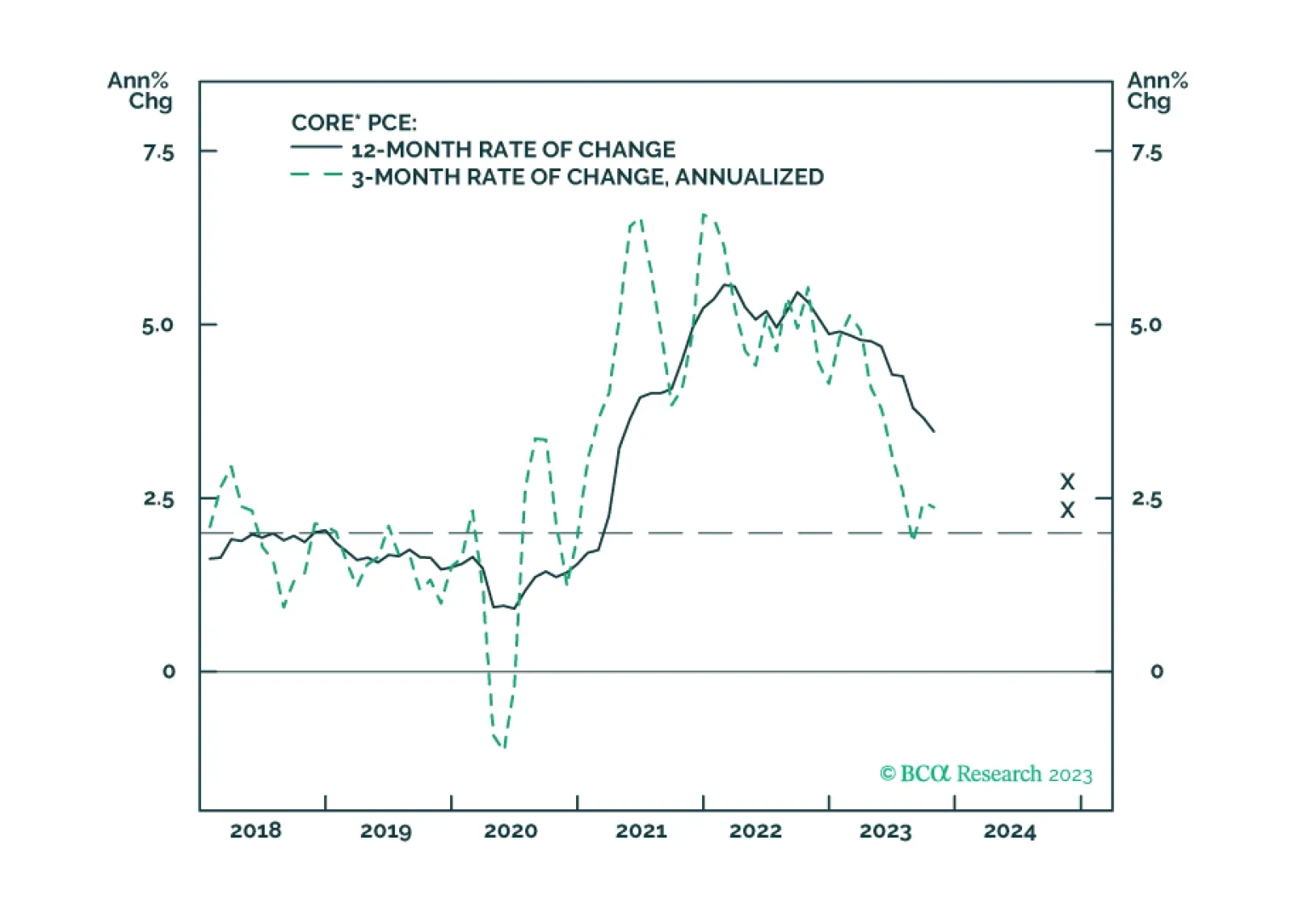

Treasury yields will sketch out a range between now and Q1 2024, with the upside determined by inflation and the downside determined by labor markets.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

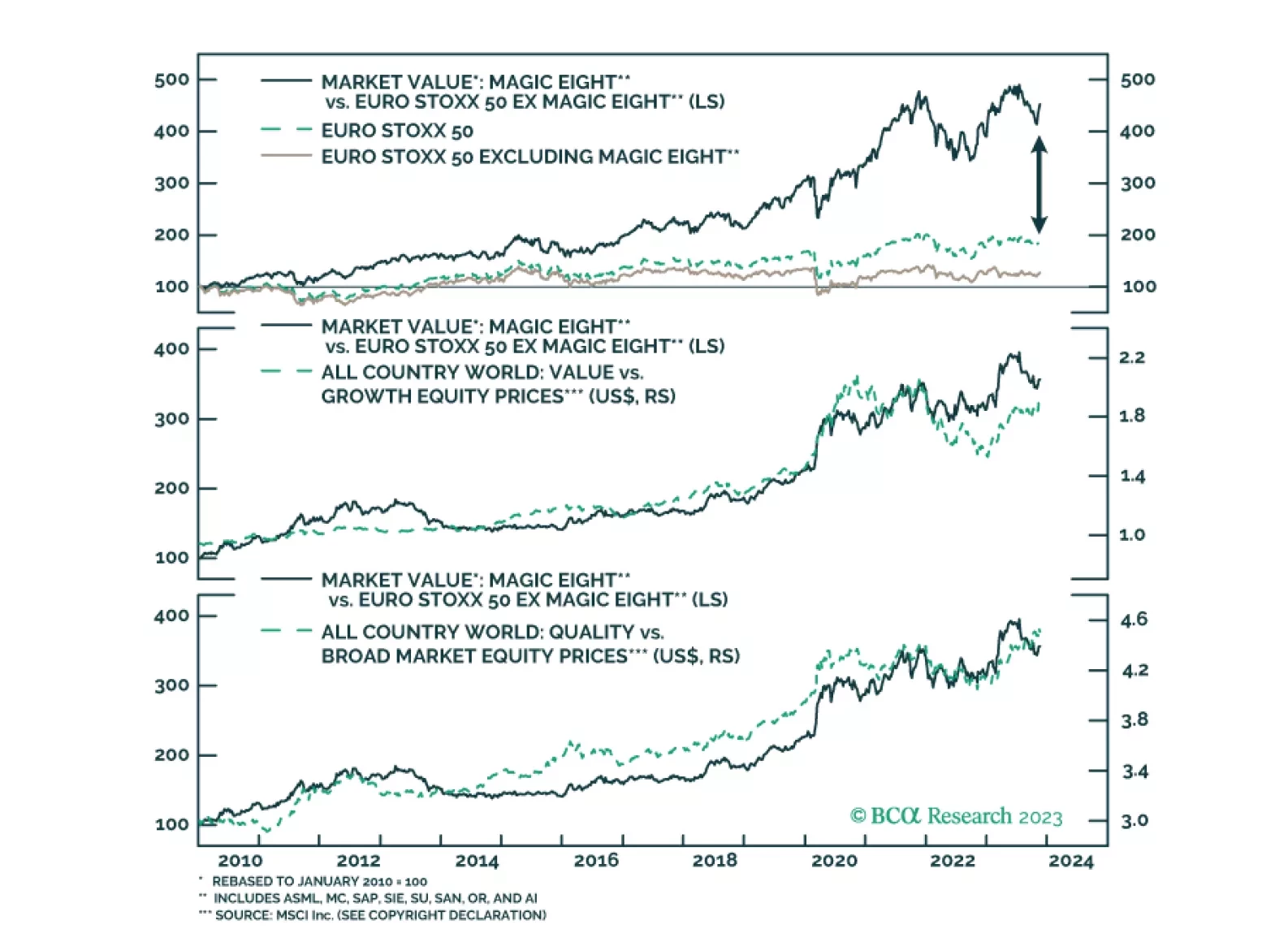

The US has the Magnificent Seven, Europe has the Magic Eight. What drives the performance of those eight stocks crucial to the European market?

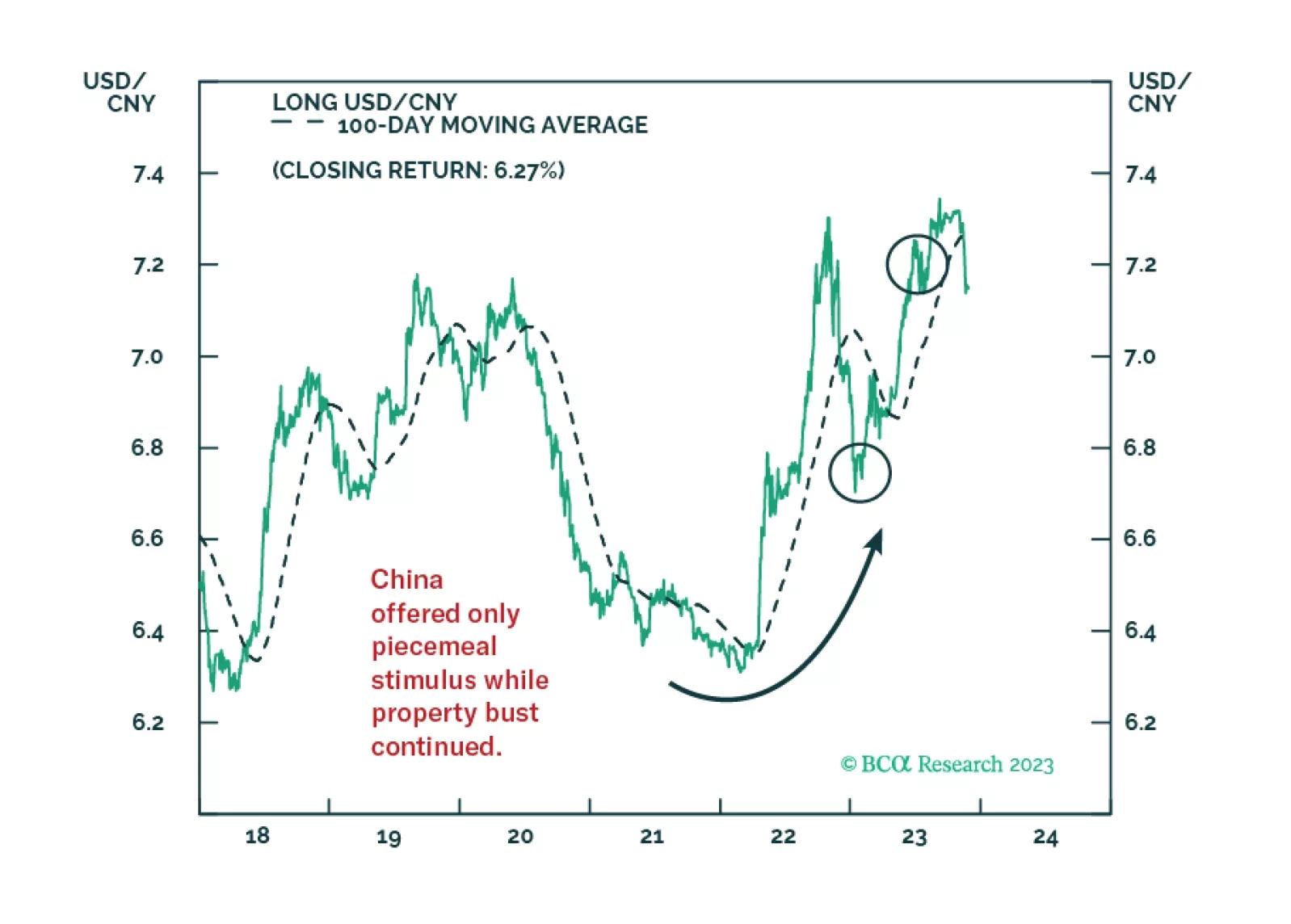

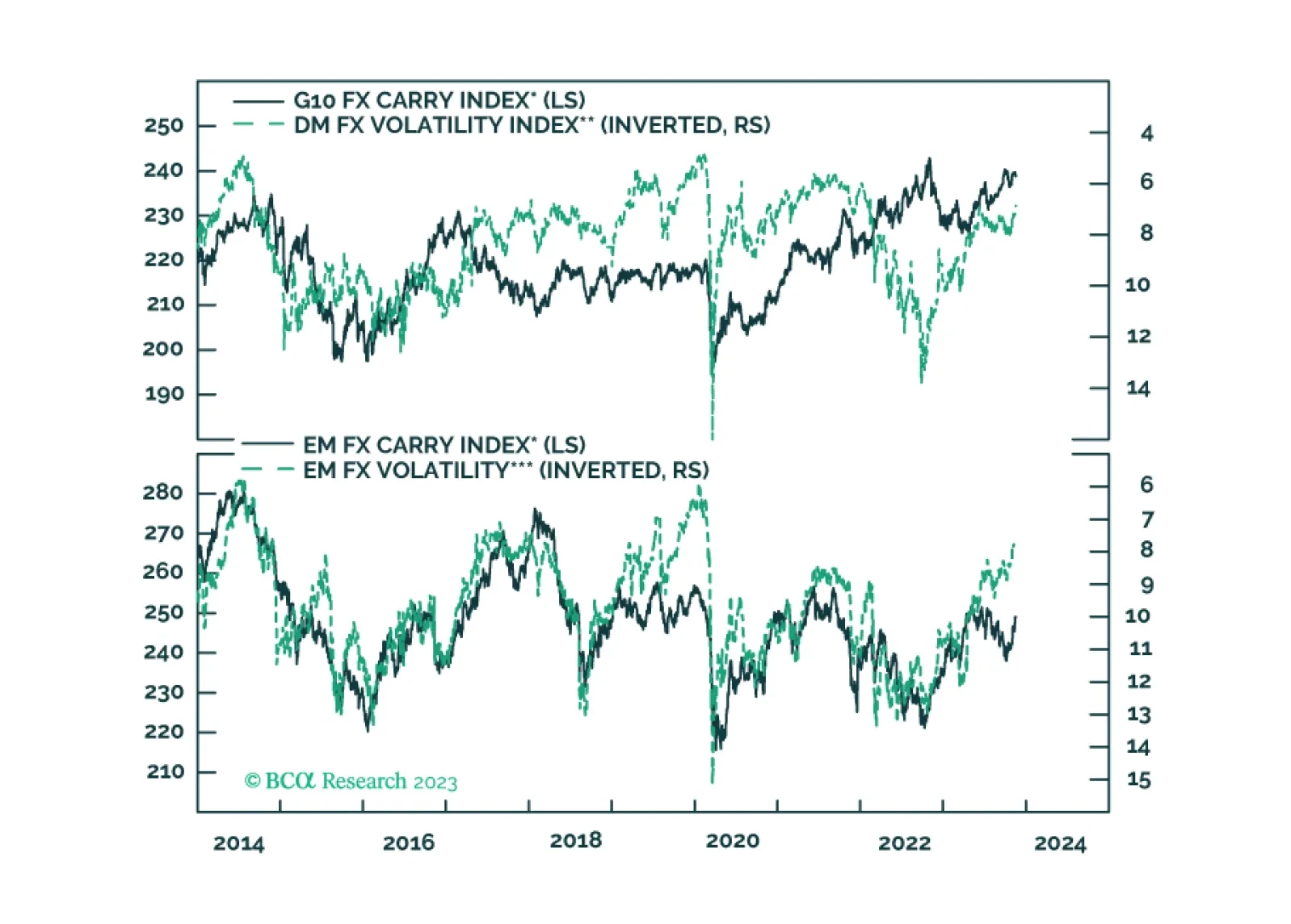

In this report, we evaluate the risk to carry trades in the coming months.

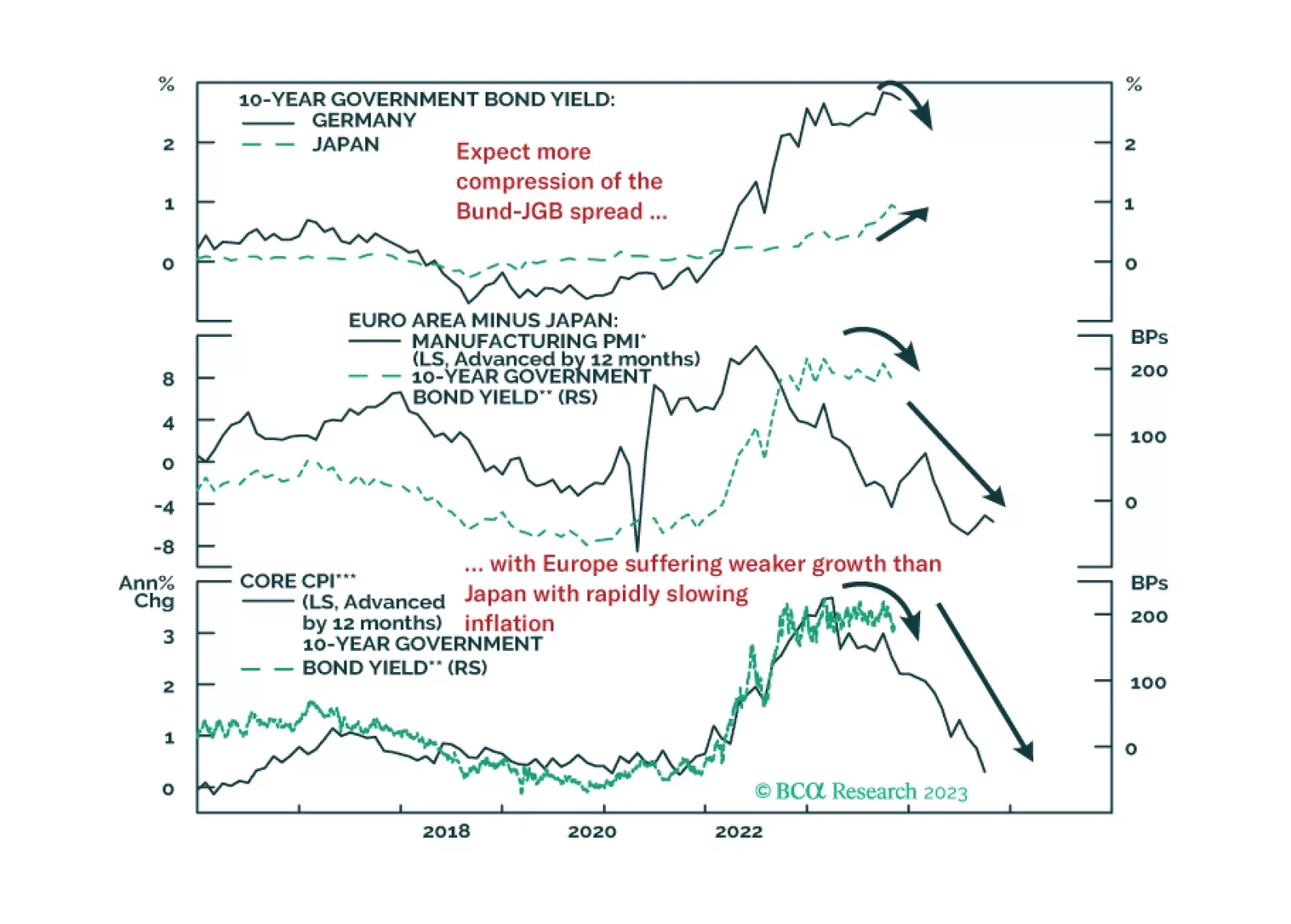

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.

Economic growth has little to no relationship with long-term country returns. But if GDP doesn’t drive long-term equity returns, then what does? To find out, we break down equity total returns of 33 countries from 1997 to 2022 into seven components. In line with other academic research, we find that, over our sample, net buybacks were a crucial factor for long-term country performance. Our research suggests that equity issuance is an underestimated driver of returns that investors should pay more attention to.

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.