Manufacturing

Emerging market stocks have outperformed their global counterparts by 4 percentage points in USD terms since February according to MSCI indices. They have gotten a boost from the bounce in the global manufacturing cycle. The MSCI Emerging Market index moves…

US industrial production stalled in April against expectations of a moderate pace of growth (0.1% m/m) and March’s growth rate was revised lower from 0.4% m/m to 0.1% m/m. Notably, pro-cyclical manufacturing production unexpectedly contracted 0.3% m/m from a…

Investor and business sentiment continues to improve in the Eurozone. The ZEW Expectations series for the Eurozone (+3.1 to 47 in May) and Germany (+4.2 to 47.1, above expectations) strengthened to 27-month highs. Moreover, the spread between the expectations…

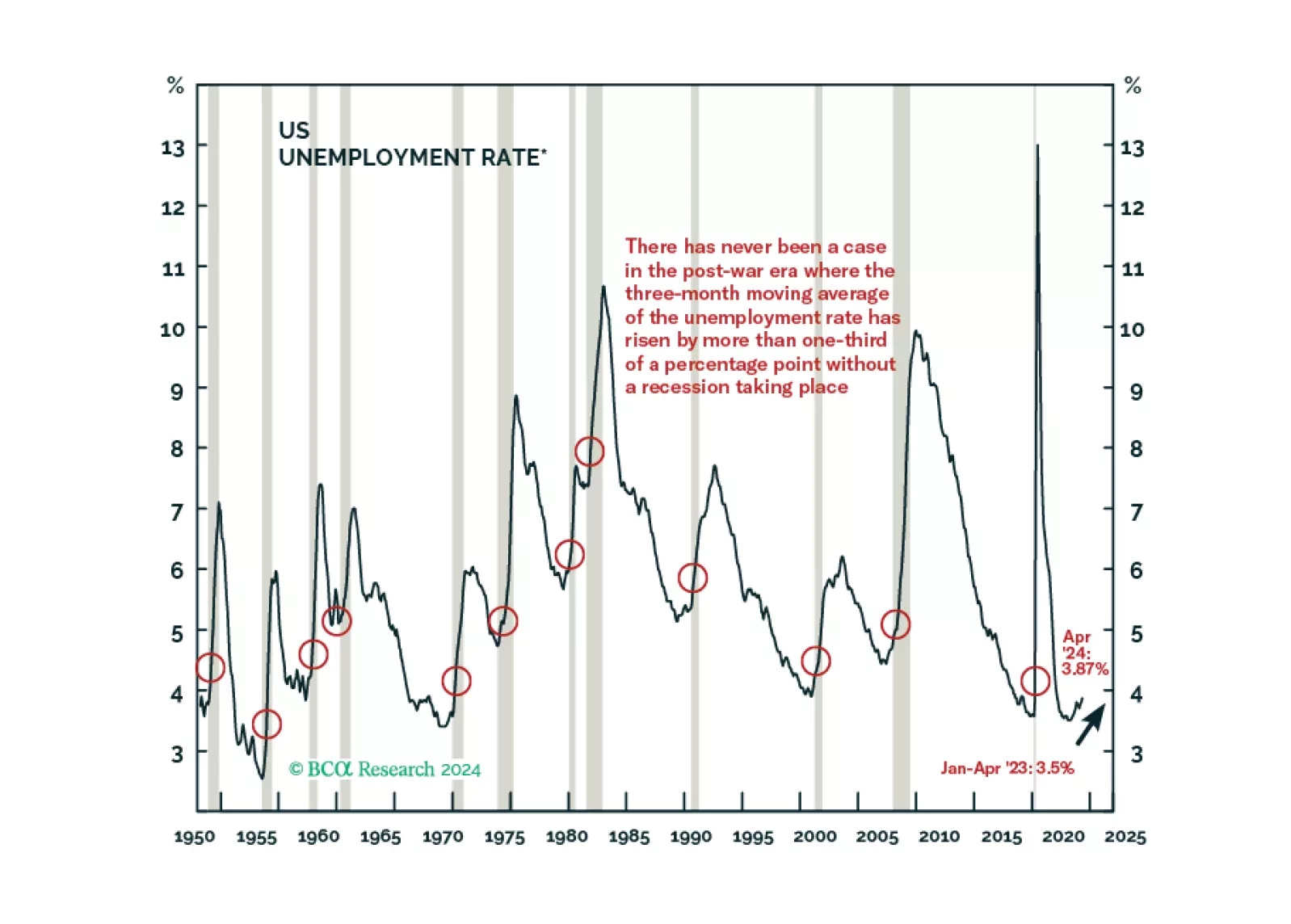

We marked the first X on our Equity Downgrade Checklist and the latest JOLTS, Employment Situation and SLOOS releases brought us closer to ticking some others. We remain tactically neutral on equities but expect that we will underweight them as excess savings are further depleted, leading labor market indicators continue to soften and consumer credit performance continues to fray.

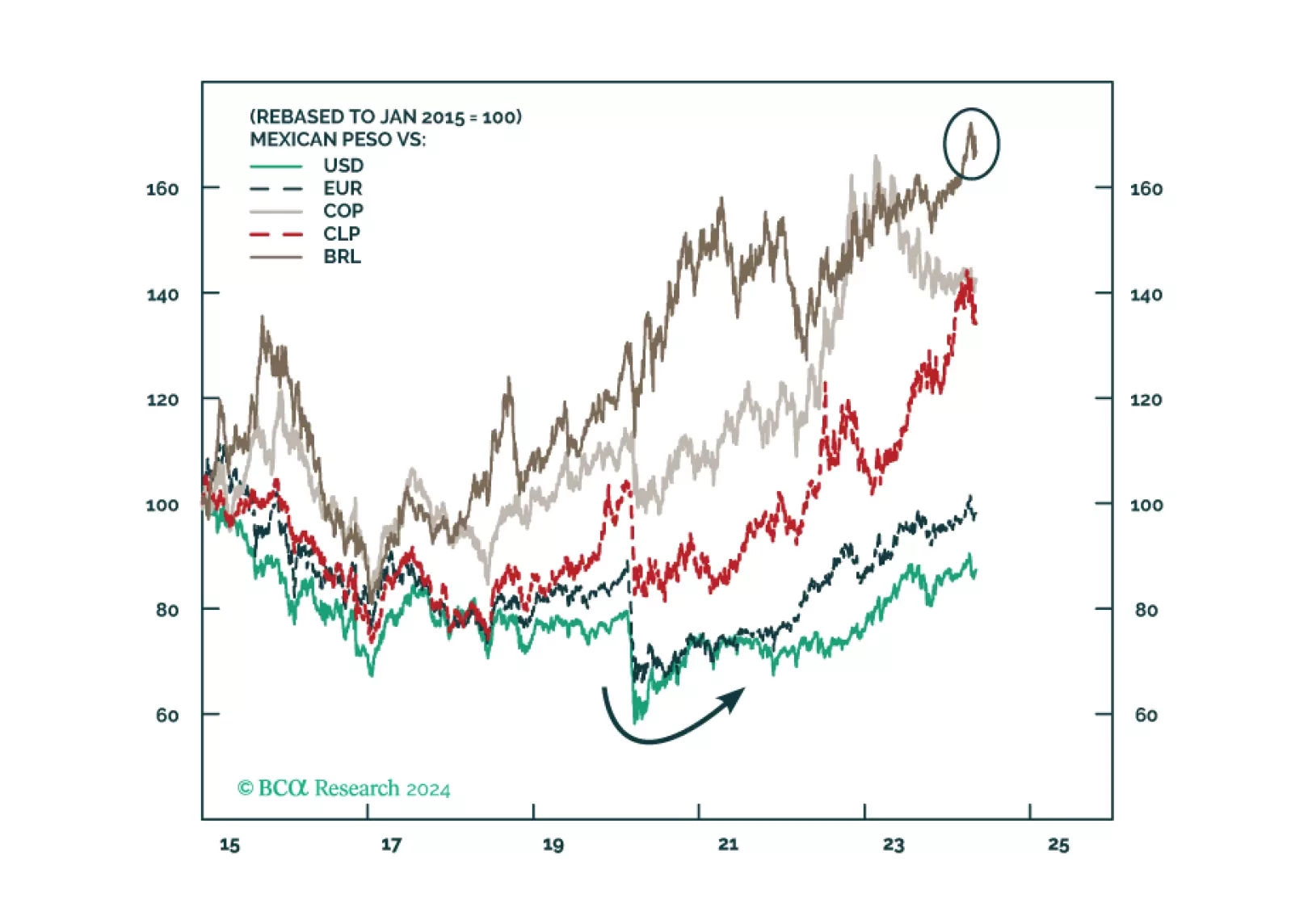

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

In a widely expected move, the Riksbank cut its policy rate by 25 basis points on Wednesday from 4% to 3.75%. The policy statement highlighted that inflation is approaching its 2% target, that leading indicators are pointing to further downside in prices and…

The revival in global growth momentum continued in April. The JPM Global Manufacturing PMI came in at 50.3, marking its third consecutive month of expansion. Details underscored solid demand conditions. Output and new orders continued to rise and new…

After briefly breaking a 16-month contraction streak, the ISM Manufacturing PMI dipped back below the 50.0 boom-bust line in April. It decreased from 50.3 to 49.2, disappointing expectations of 50.0. Notably, measures of domestic and foreign demand both…

The Chinese NBS non-manufacturing PMI came in at 51.2, below the previous month’s number of 53 and below expectations of 52.2. Moreover, the NBS manufacturing PMI also decreased to (a better-than-expected) 50.4 in April from 50.8 in March. Meanwhile, the…

Chinese industrial profit growth slowed in the first three months of the year to 4.3% YTD y/y, from 10.2% y/y in January and February. The March slowdown is meaningful since industrial profits outright contracted by 3.5% relative to March 2023. Weak…