Manufacturing

After briefly breaking a 27-month streak of negative sentiment back in June, the Eurozone Sentix Economic index disappointed in August. The overall index worsened from July’s negative reading to -13.9, below expectations of a milder deterioration. The…

The ISM services PMI surprised positively in July. The headline index expanded 2.6 ppts to 51.4, reversing May’s fastest pace of contraction in four years. Notably, the business activity subcomponent increased 4.9 ppts to 54.5, new orders and new export…

The ISM Manufacturing PMI disappointed in July. The headline index declined at a faster pace, from 48.5 to 46.8, disappointing expectations and extending a four-month contraction streak. Details were uninspiring. New orders dipped to 47.4 from 49.3,…

Sweden’s manufacturing PMI started contracting in July, plummeting from 53 to 49.2, falling far short of expectations that growth would broaden. Weakness was broad-based. Notably, new orders and new export orders plunged a whopping 15.1 and 8.7 points in…

China’s NBS manufacturing PMI declined further in July, from 49.5 to 49.4, marking a third consecutive month of contraction. New orders and new export orders underscored continued weakness in both domestic and foreign demand conditions. Meanwhile, the NBS…

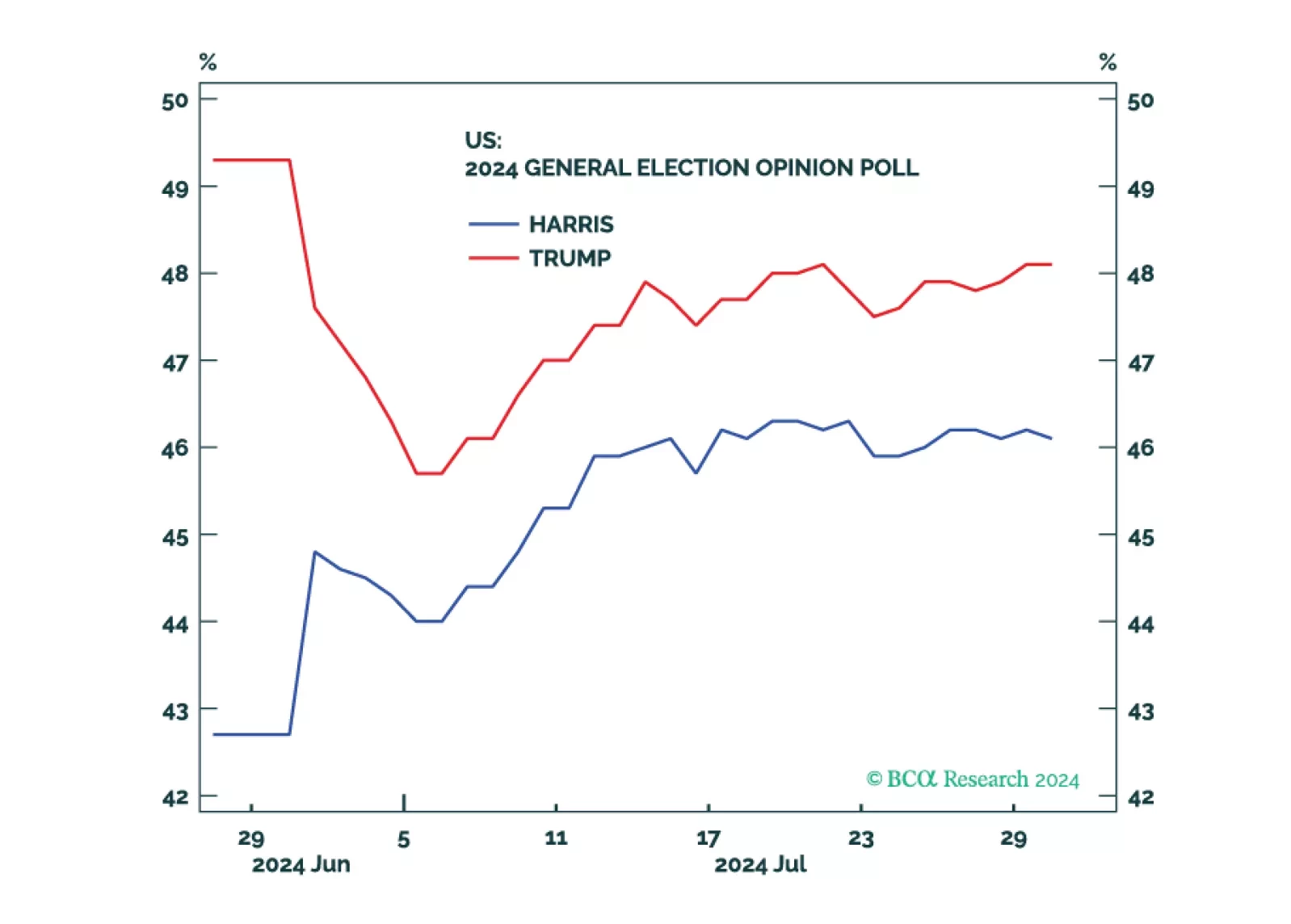

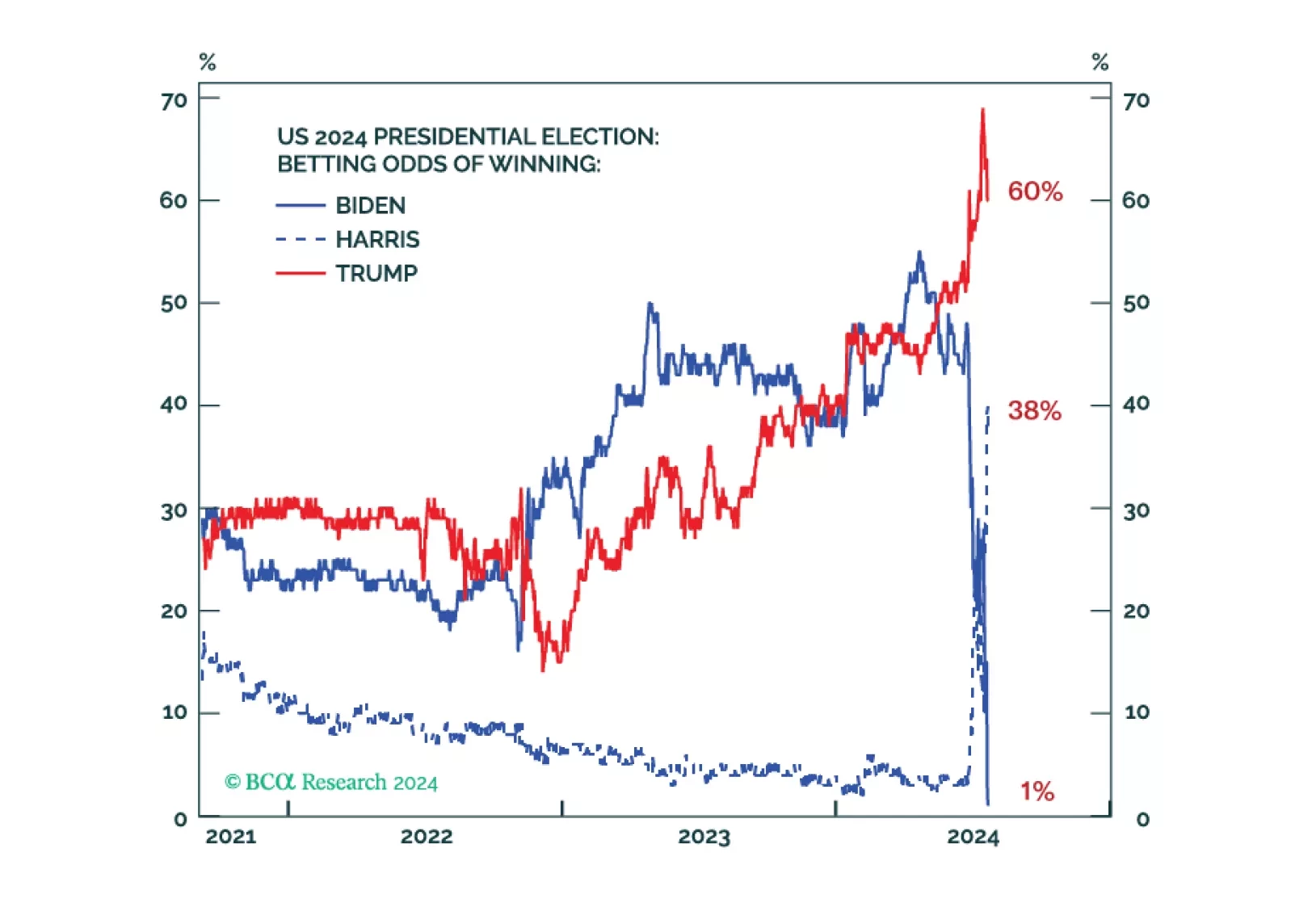

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

US job openings grew by 8.18 million in June, exceeding expectations of 8 million, but below May’s 8.23 million openings. The pro-cyclical manufacturing sector accounted for the largest drag, withdrawing 100 thousand openings, or one-sixth of its May total.…

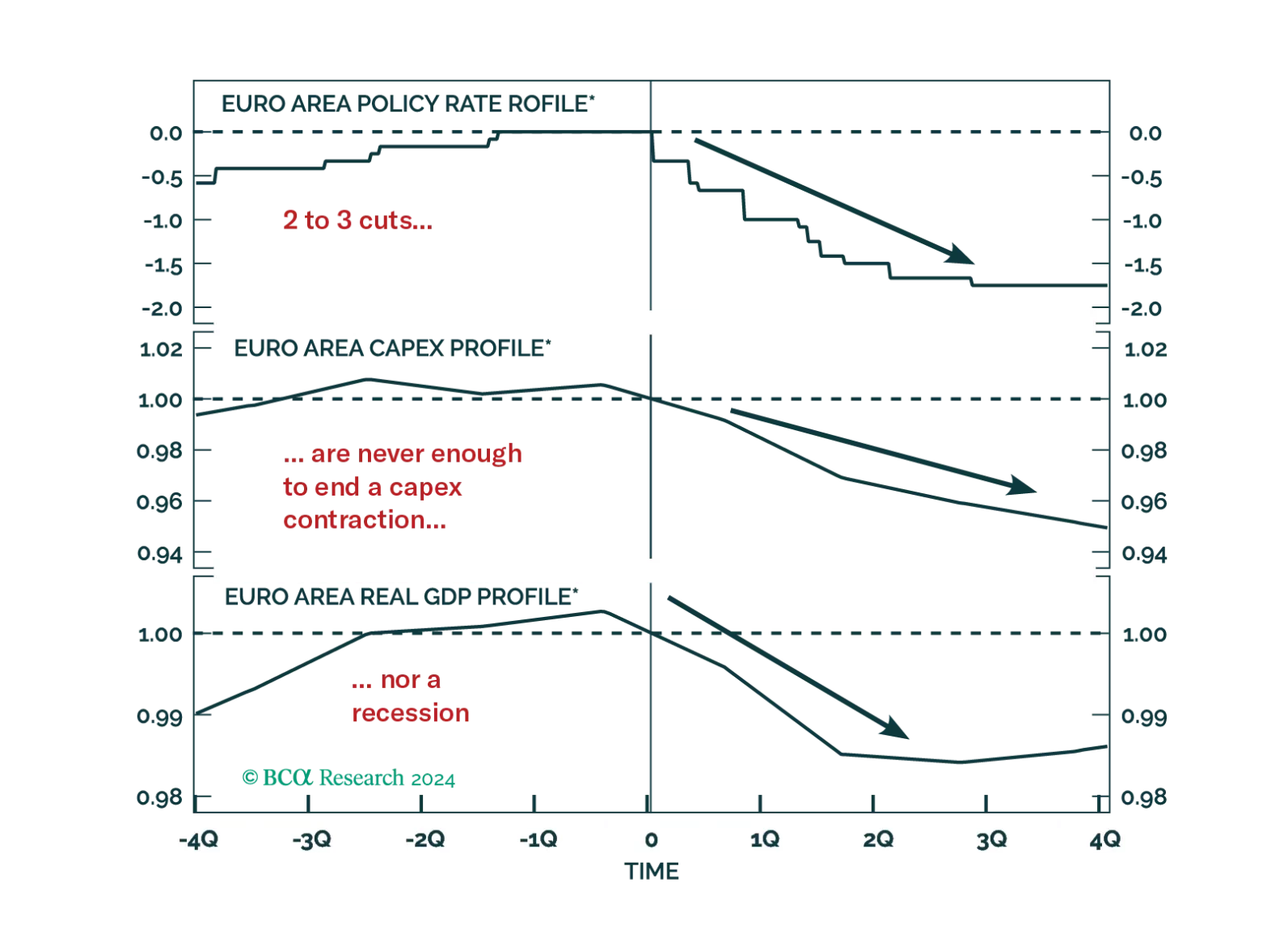

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

Preliminary PMIs suggest that, with the exception of the Eurozone, growth was still resilient in DM economies in July. Composite PMIs expanded across the board, at a faster pace in the US and the UK, and from previously contractionary levels in Japan. …

Investors should focus on growth concerns rather than the “Trump trade.” Bond yields will fall in the short run due to cyclically disinflationary economic slowdown, rather than rise in anticipation of a Republican full sweep and inflationary policies, which are likely but not yet a done deal.