Labor Market

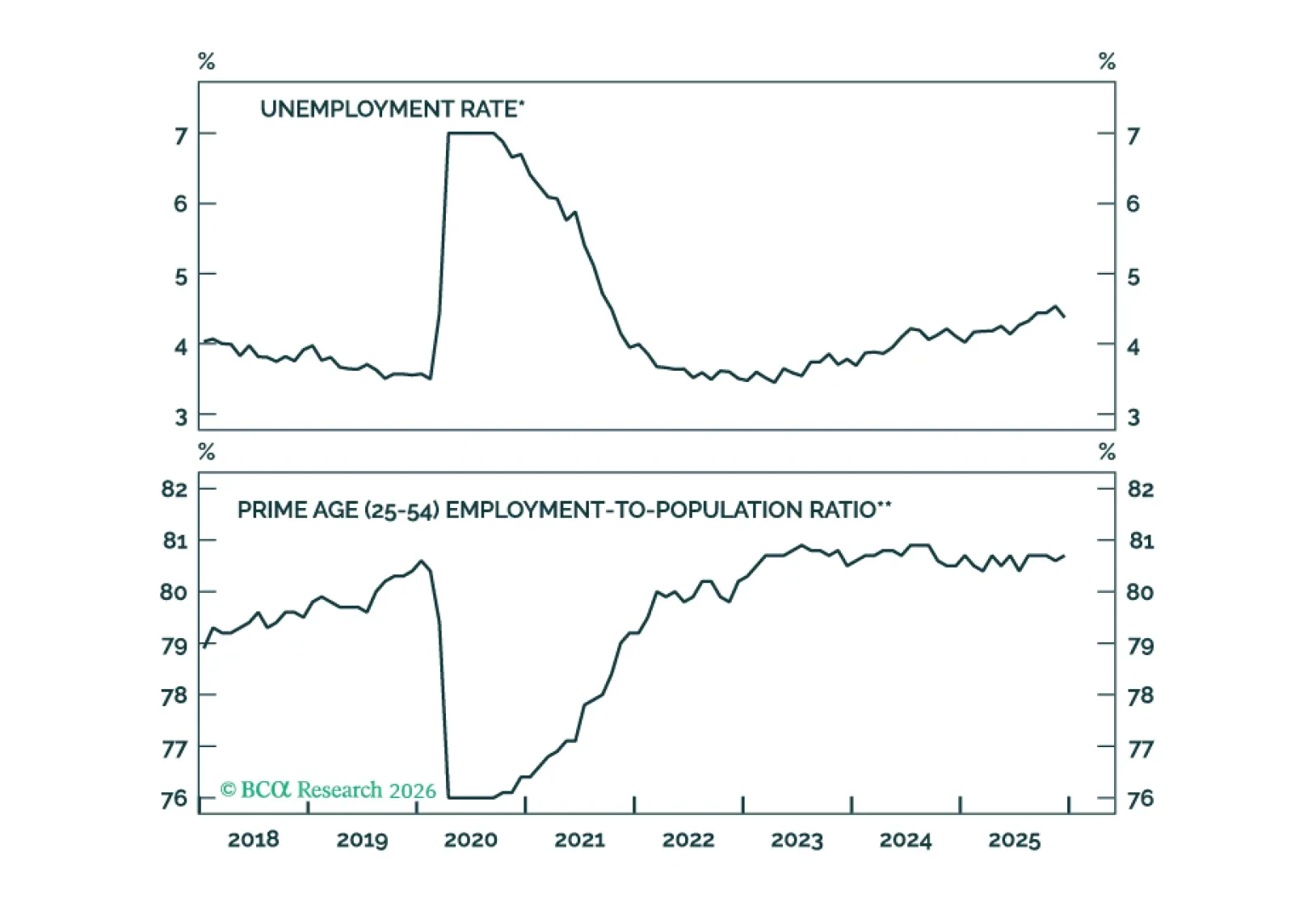

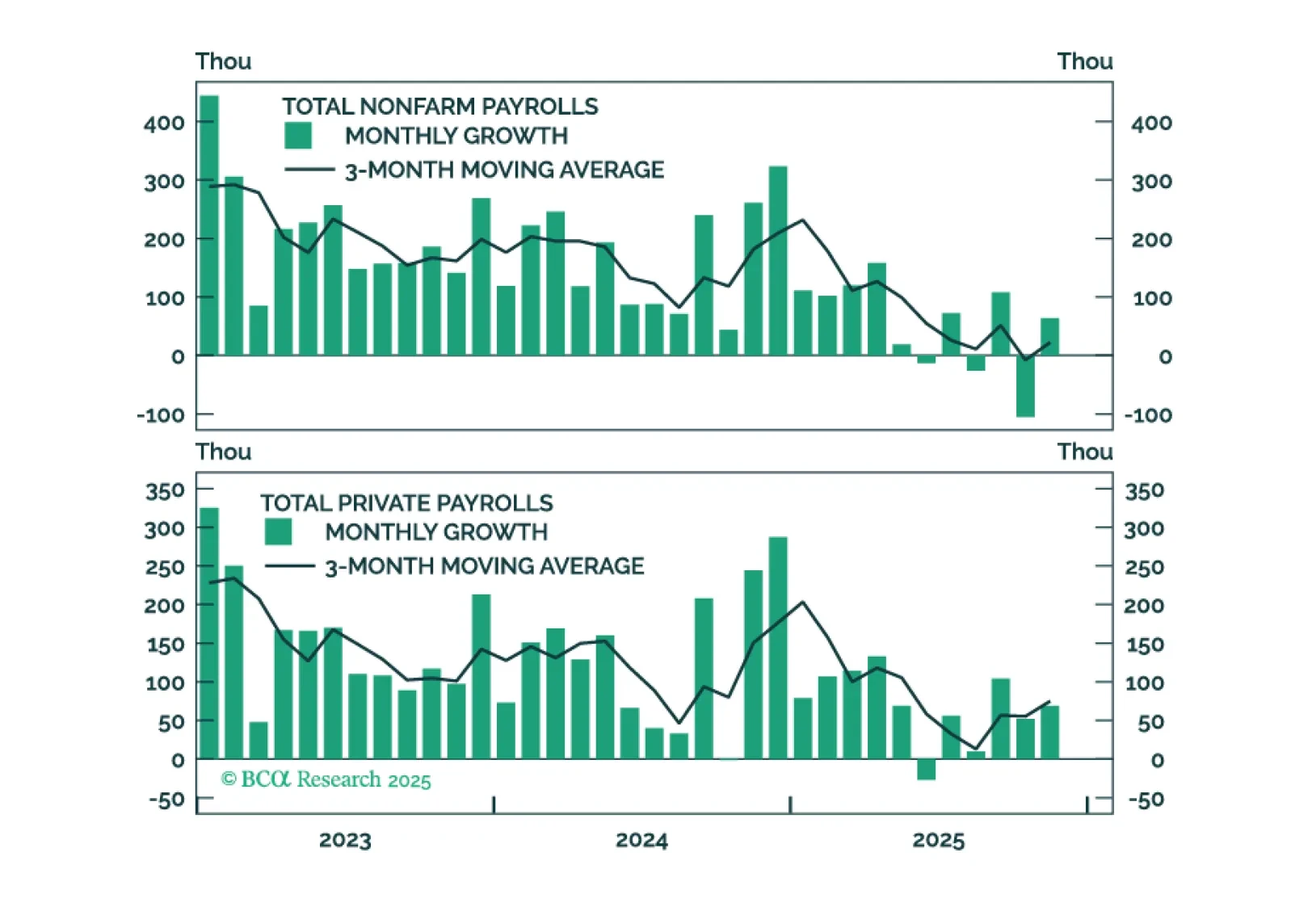

In Section I, Doug highlights the risks to US consumption if job growth does not soon recover. The US economy has yet to pass its tipping point, however, arguing against defensive positioning for now. In Section II, Jonathan examines whether the AI “scaling laws” are likely to hold. They will over the near term, but cracks are already beginning to form in the narrative of ever-improving AI.

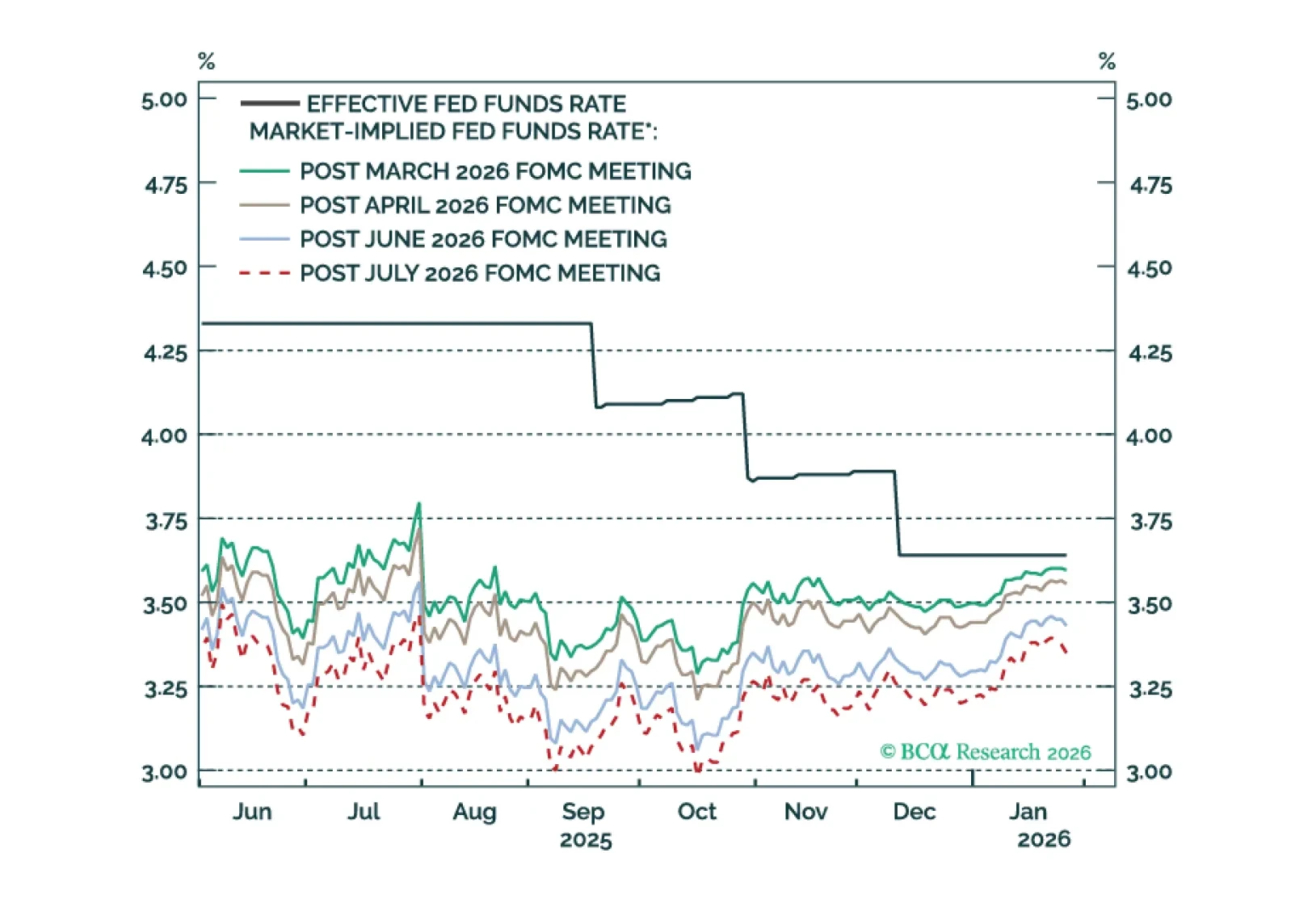

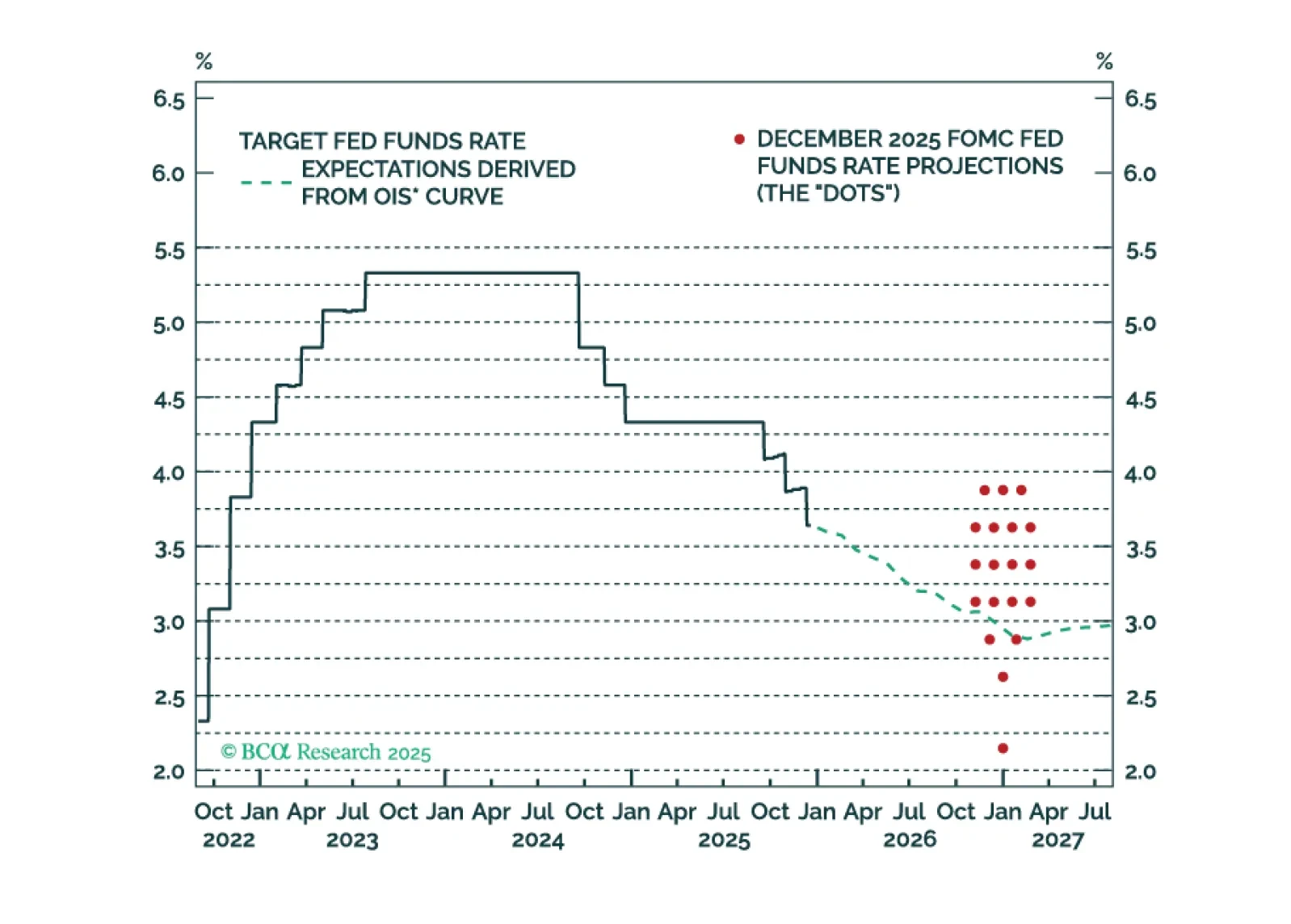

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

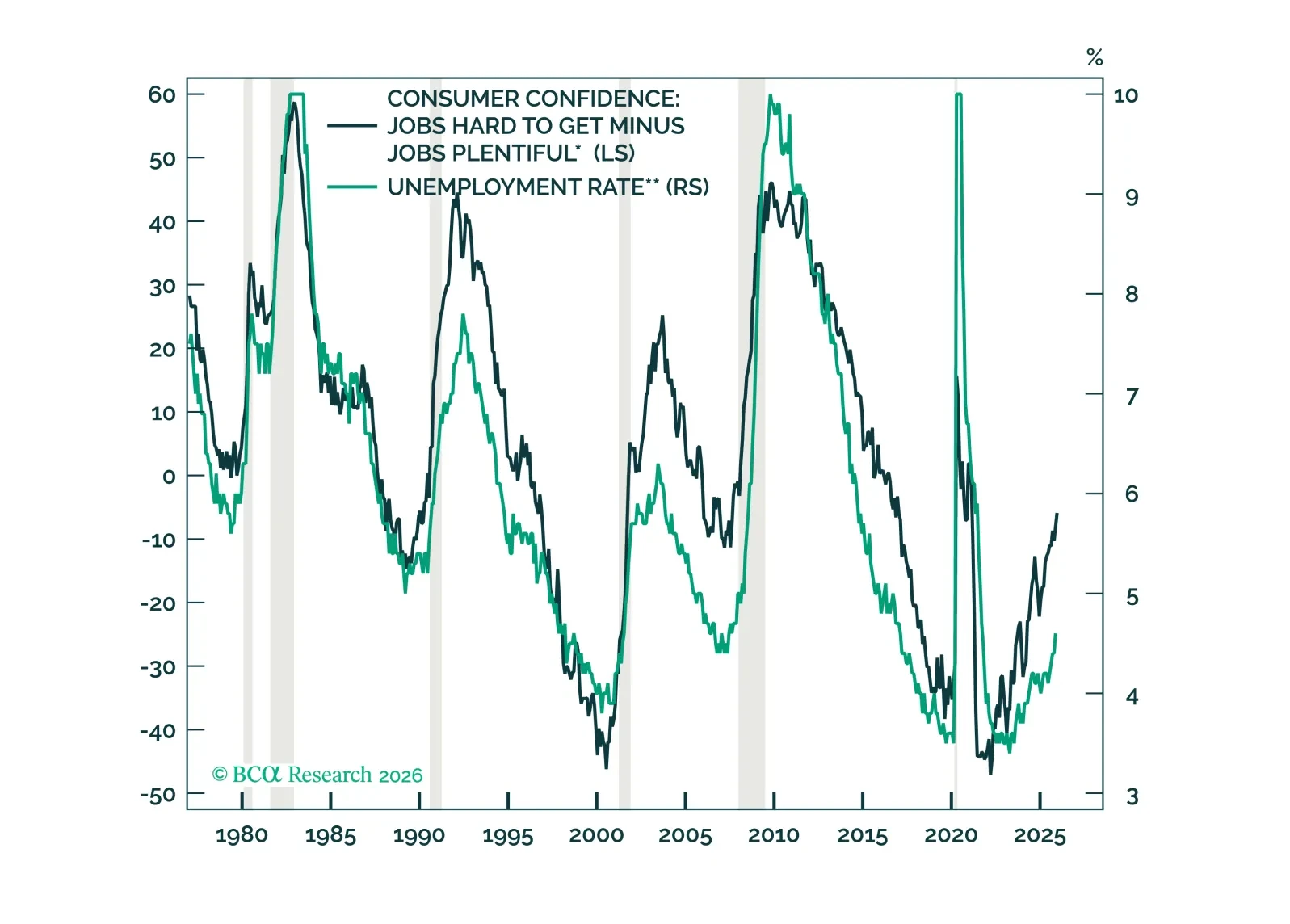

Measures of labor market utilization improved in December, ruling out a January cut and significantly reducing the odds of a March cut.

To start 2026, we answer what we believe are the most important questions facing investors surrounding the labor market, monetary and fiscal policy, and AI stocks. Overall, we reiterate our overweight views on risk assets and highlight the risks surrounding the upcoming tariff decision.

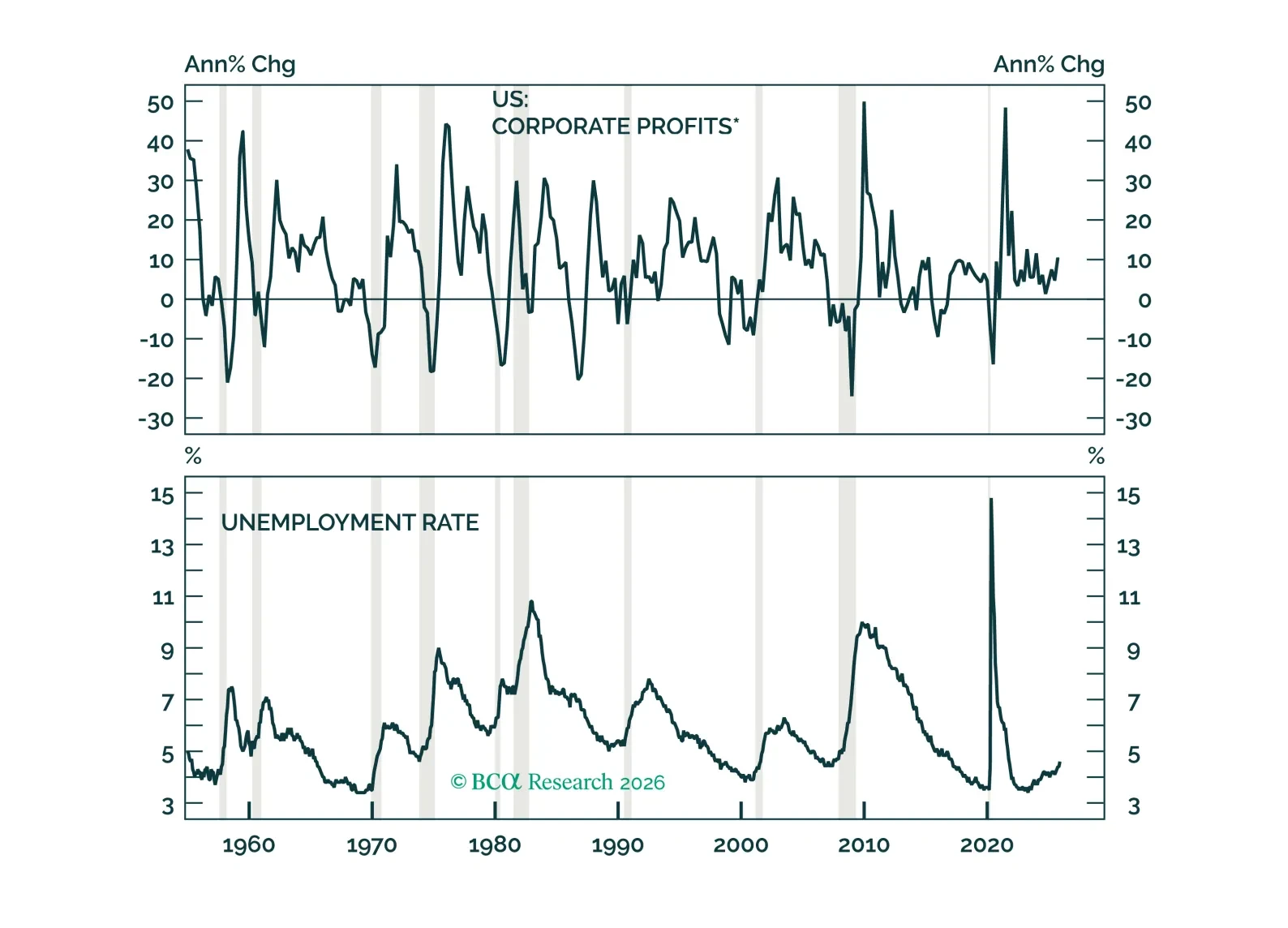

We have been surprised that consumption has held up well despite anemic payrolls growth. This brief considers ways that consumption might continue to beat our base-case expectations.

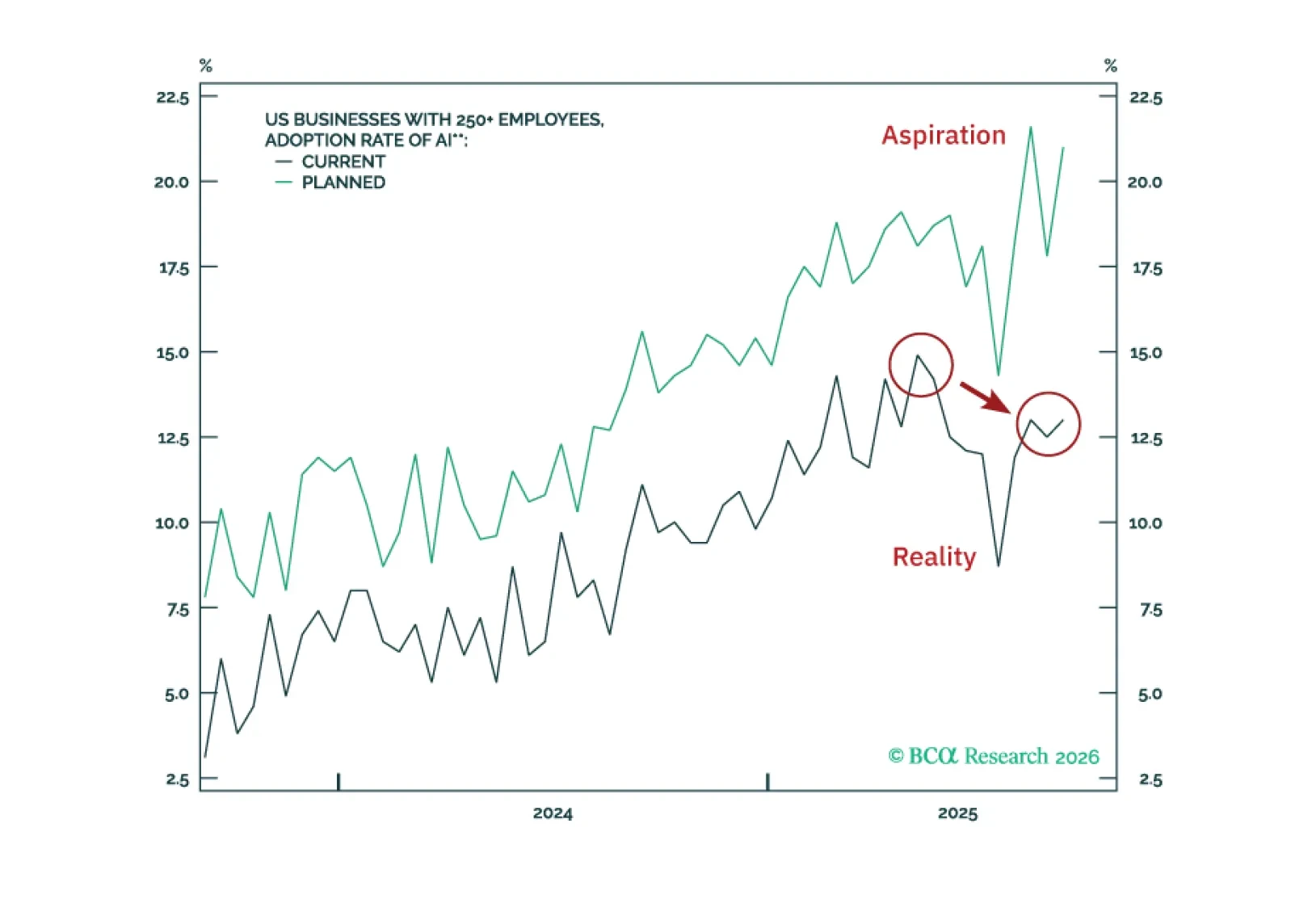

In Section II, Jonathan updates the BCA Artificial Intelligence Productivity Checklist and concludes that the evidence of an AI-driven productivity boom is not convincing.

In Section I, Doug underscores that the US labor market remains weak, crimping the outlook for disposable income growth. It is too soon to decisively bet against the bull market, but downside risks remain quite elevated. In Section II, Jonathan updates the BCA Artificial Intelligence Productivity Checklist and concludes that the evidence of an AI-driven productivity boom is not convincing.

Employment Data Point To Dovish Policy Surprises In 2026

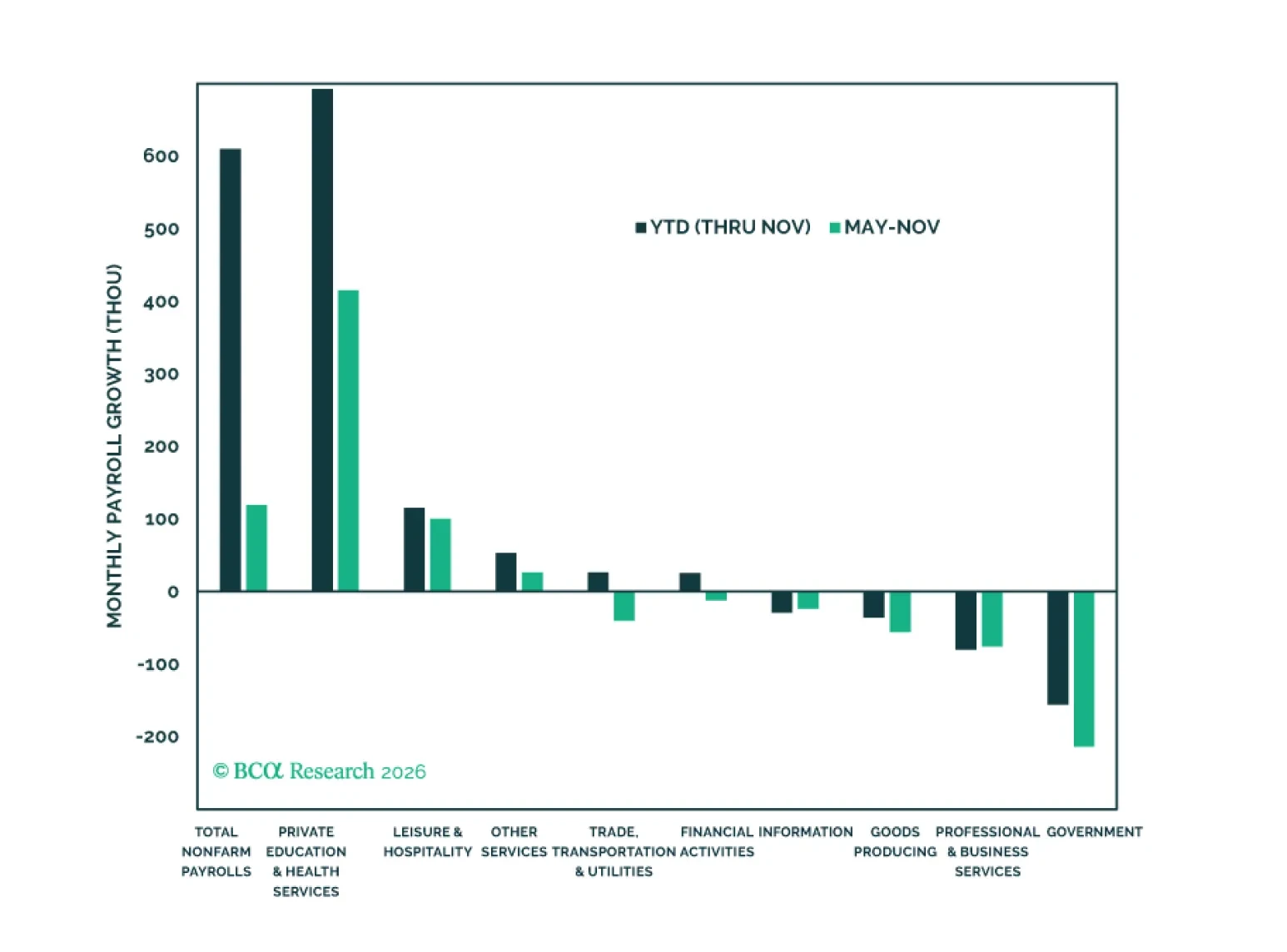

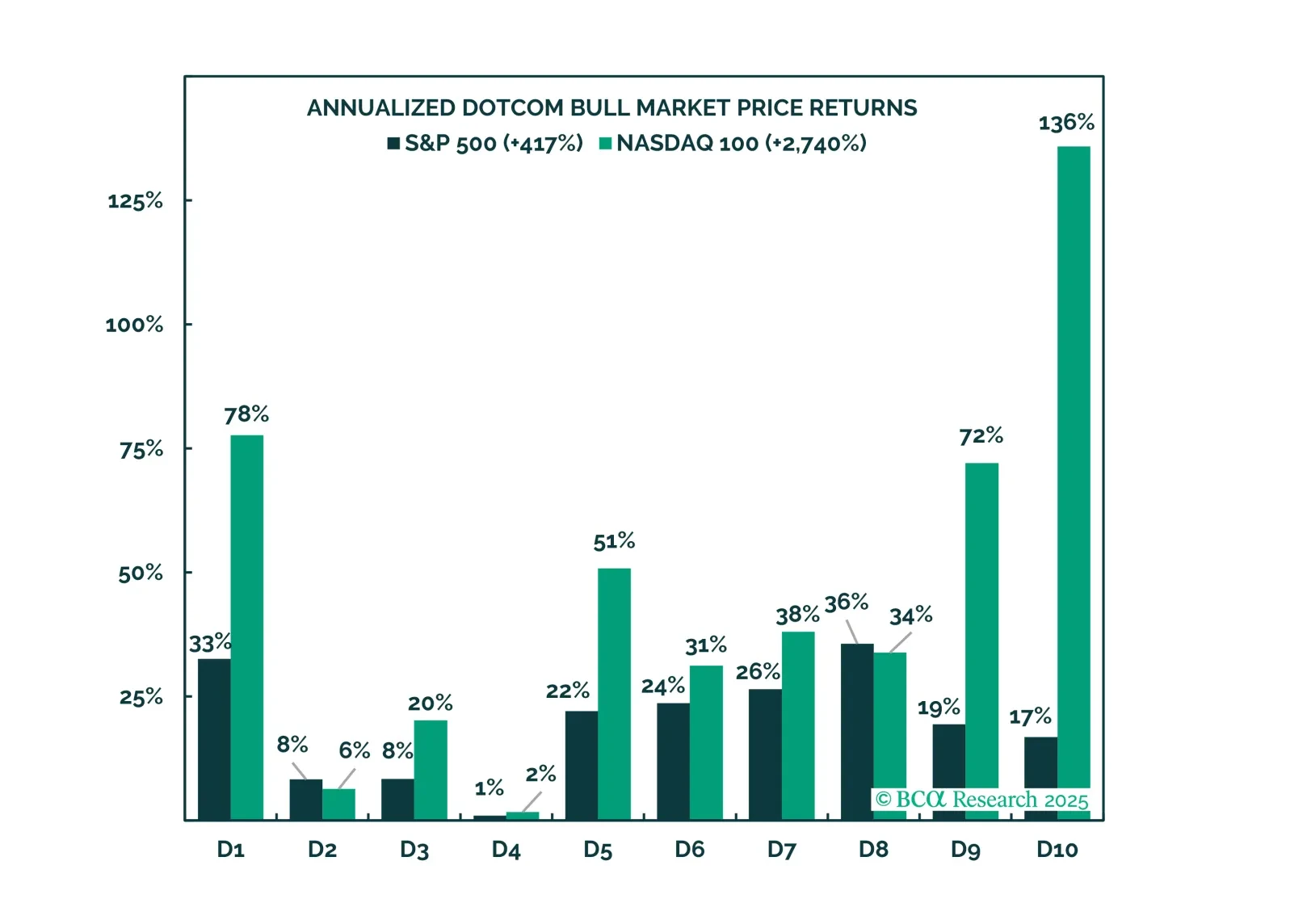

Weak, narrowly concentrated job growth in fields that pay poorly bodes ill for the economy, but we enter 2026 recommending benchmark allocations because we are wary of the potential for an AI-driven meltup. Investors should bide their time before turning defensive.