Labor Market

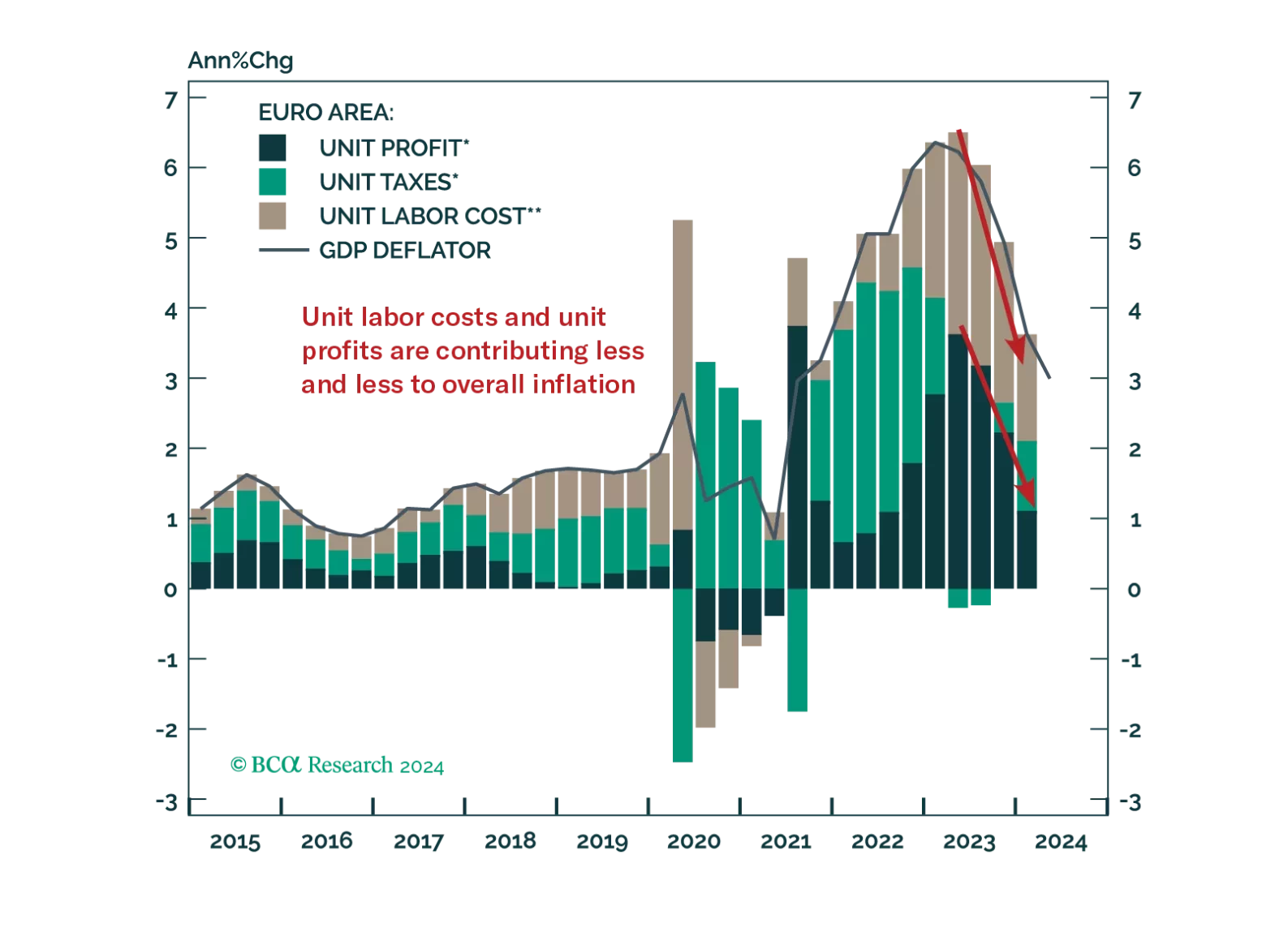

The ECB will cut rates once more this year; however, markets underprice how far it will ease next year.

Continued deterioration in labor demand underpins our expectation for a US recession, as it will lead to slower compensation growth, hobbling consumption spending’s main driver. We also previously highlighted that the outlook for bond yields currently hinges…

Some thoughts on this morning’s US claims report and a preview of next week’s FOMC meeting.

According to BCA Research’s US Political Strategy service, former President Trump still has a path to come back to power, despite his disastrous performance in the debate with Vice President Kamala Harris on September 10. A cascade of shifting opinion…

US headline CPI eased from 2.9% y/y to 2.5% in August in line with consensus predictions. However, core CPI unexpectedly accelerated from 0.2% m/m to 0.3%. Aside from airfares -- a highly volatile series which is likely to reverse in coming months given…

Following a 12-year-long bear market, Greek equities have returned a whopping 186% in EUR terms from their 2016 lows. The Greek macroeconomic backdrop has indeed improved. Since 2021, Greece’s nominal GDP growth has exceeded the pace of growth in…

Despite the disastrous performance by former President Trump in the debate with Vice President Kamala Harris, there are still paths for him to come back to power. The economy and global instability could flare up anytime between now and election day, while quirks in the Electoral College ensure that the election will be close. The race is still competitive and policy uncertainty and volatility will be elevated.

US small business optimism unexpectedly shed 2.5 points to 91.2 in August, the largest monthly decline since 2022, retracing nearly half of the index’s advance since March. The NFIB Small Business Optimism has oscillated in a tight range since 2022 but…

The BoE embarked on its easing cycle in August, delivering its first 25 bps rate cut. The decision was nowhere near unanimous, with 5 MPCs out of 9 voting in favor of lowering policy rates. Indeed, while headline inflation is sitting right on the central…

The Swedish economy’s cyclicality and sensitivity to global trade make it a reliable bellwether for global growth. Sweden is facing significant domestic weakness. Employment growth declined by 0.14% y/y in July and households’ debt burden stands at 155% of…