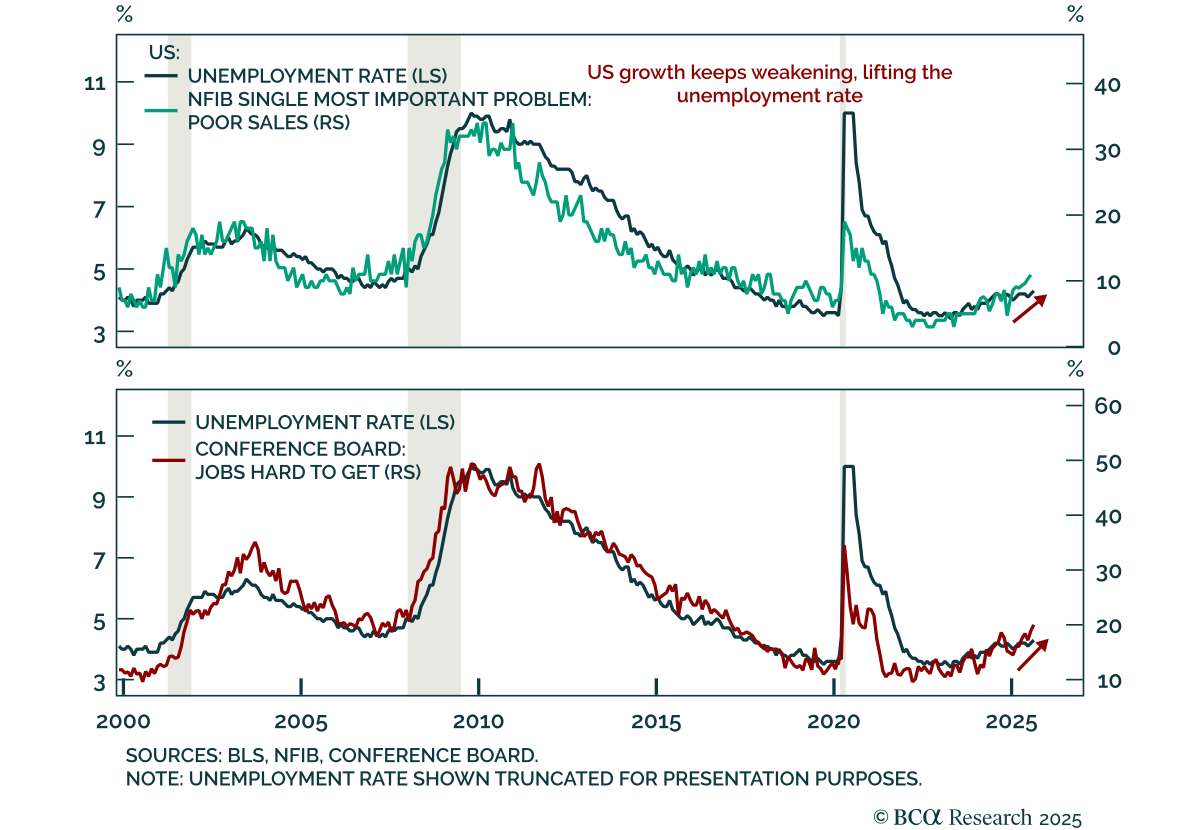

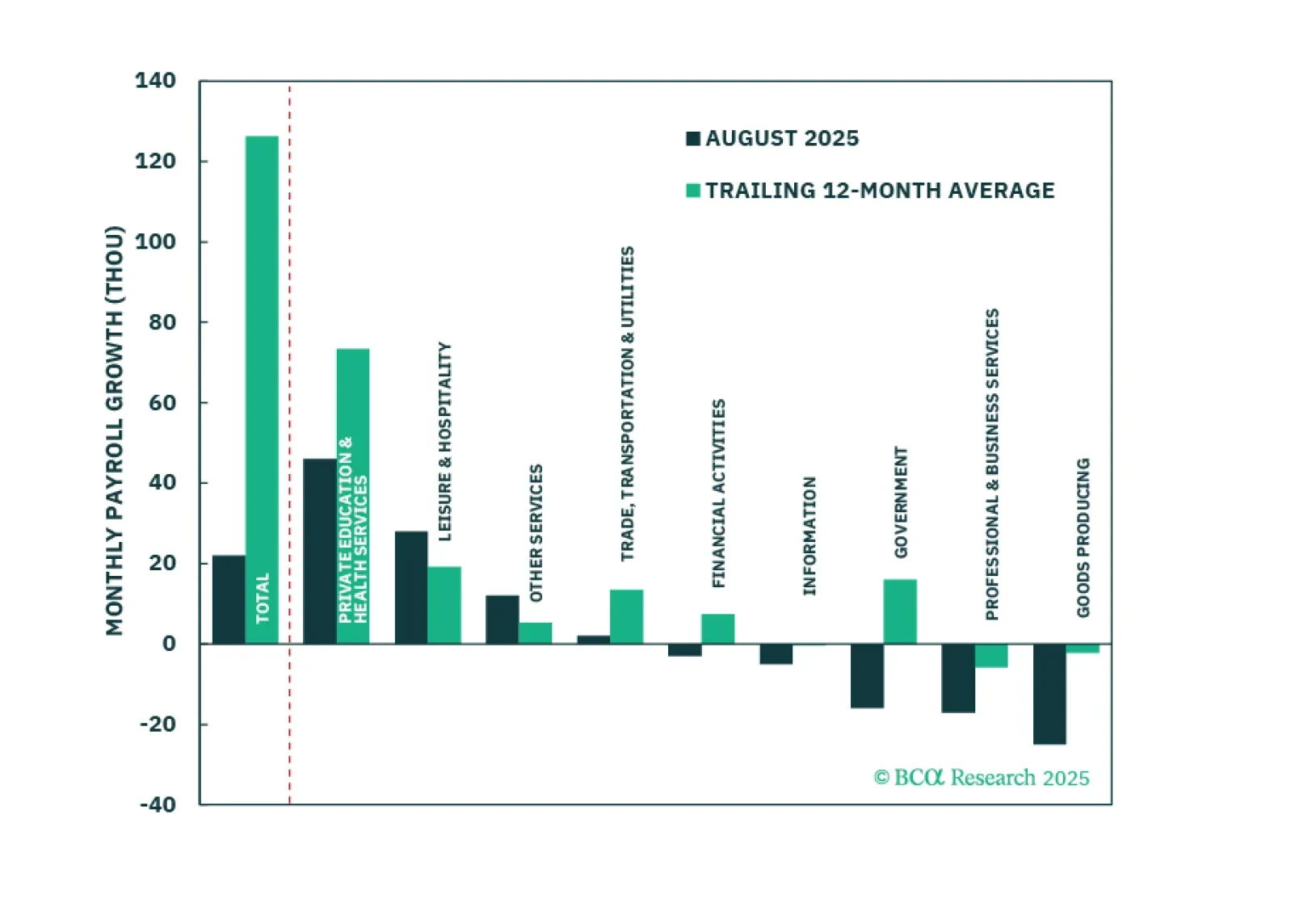

Labor Market

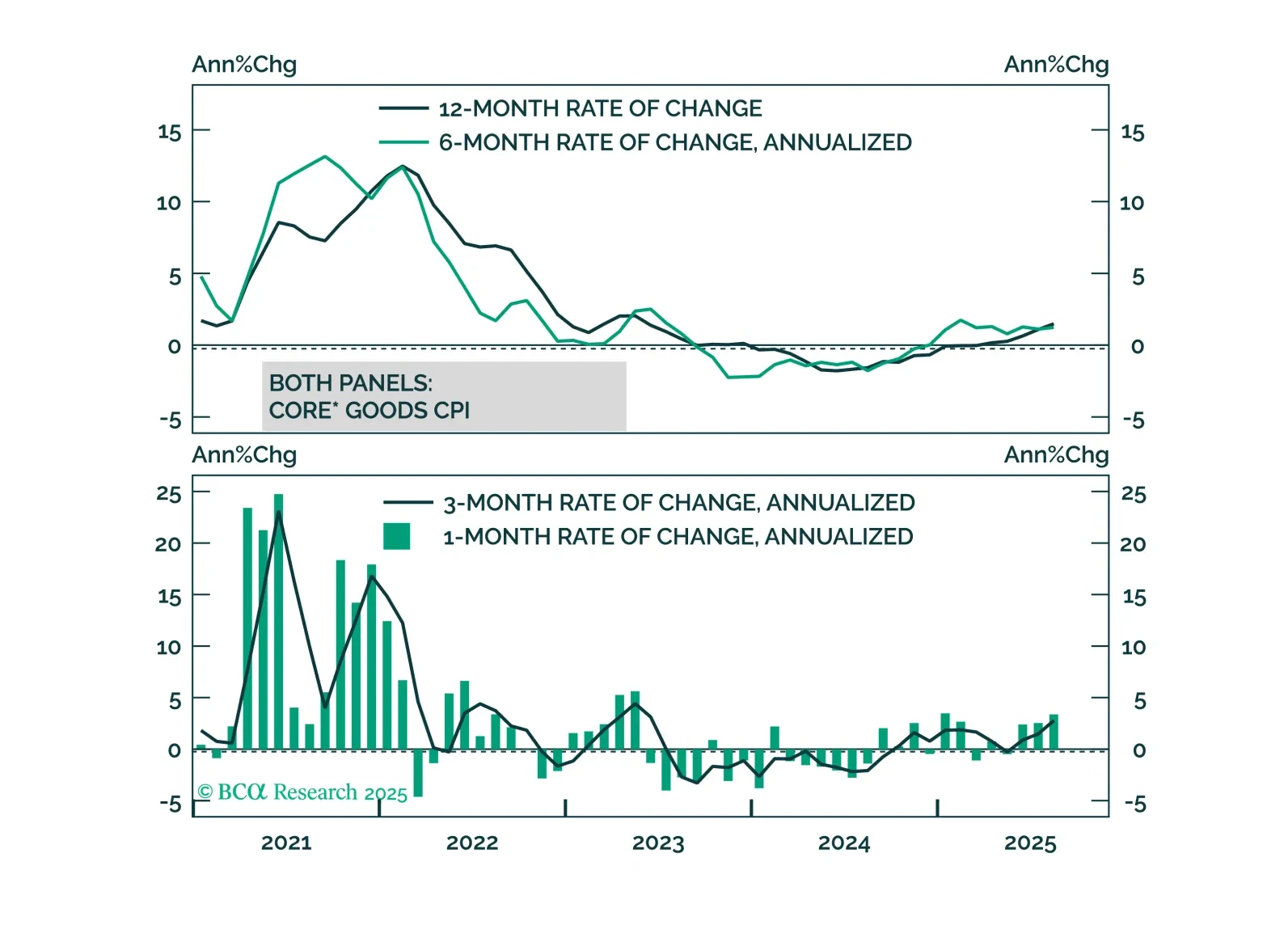

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

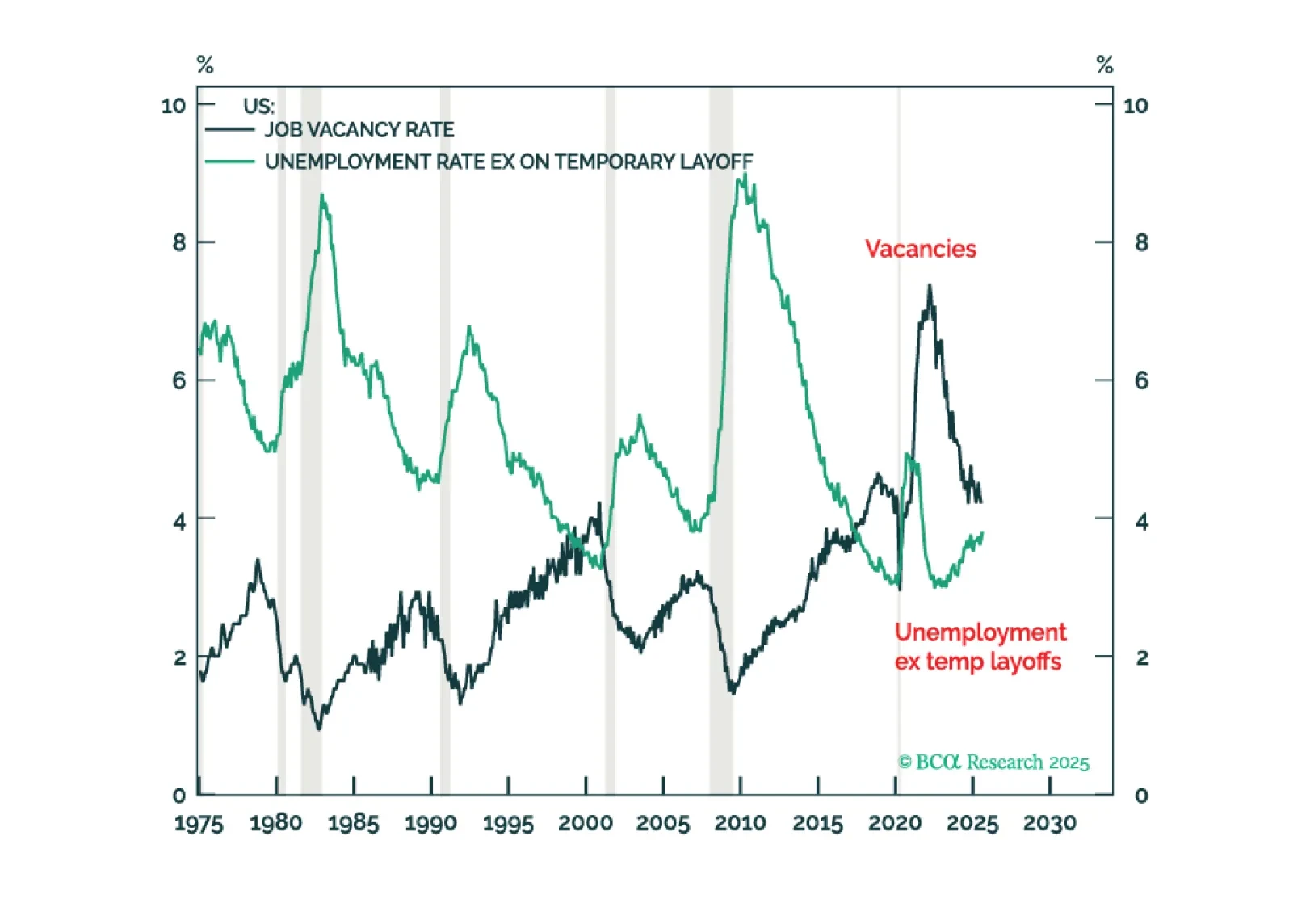

For the next few months at least, inflation risk trumps recession risk for both US markets and world markets. This because, correctly gauged, the US jobs market is still supply-constrained with ‘jobs looking for a worker’ exceeding ‘workers looking for a job’ by 0.4 percent. A still supply-constrained US jobs market cannot enter a demand-driven recession until it flips back to demand-constrained, so bond investors should underweight duration. Plus: a new tactical trade is overweight India (INDA).

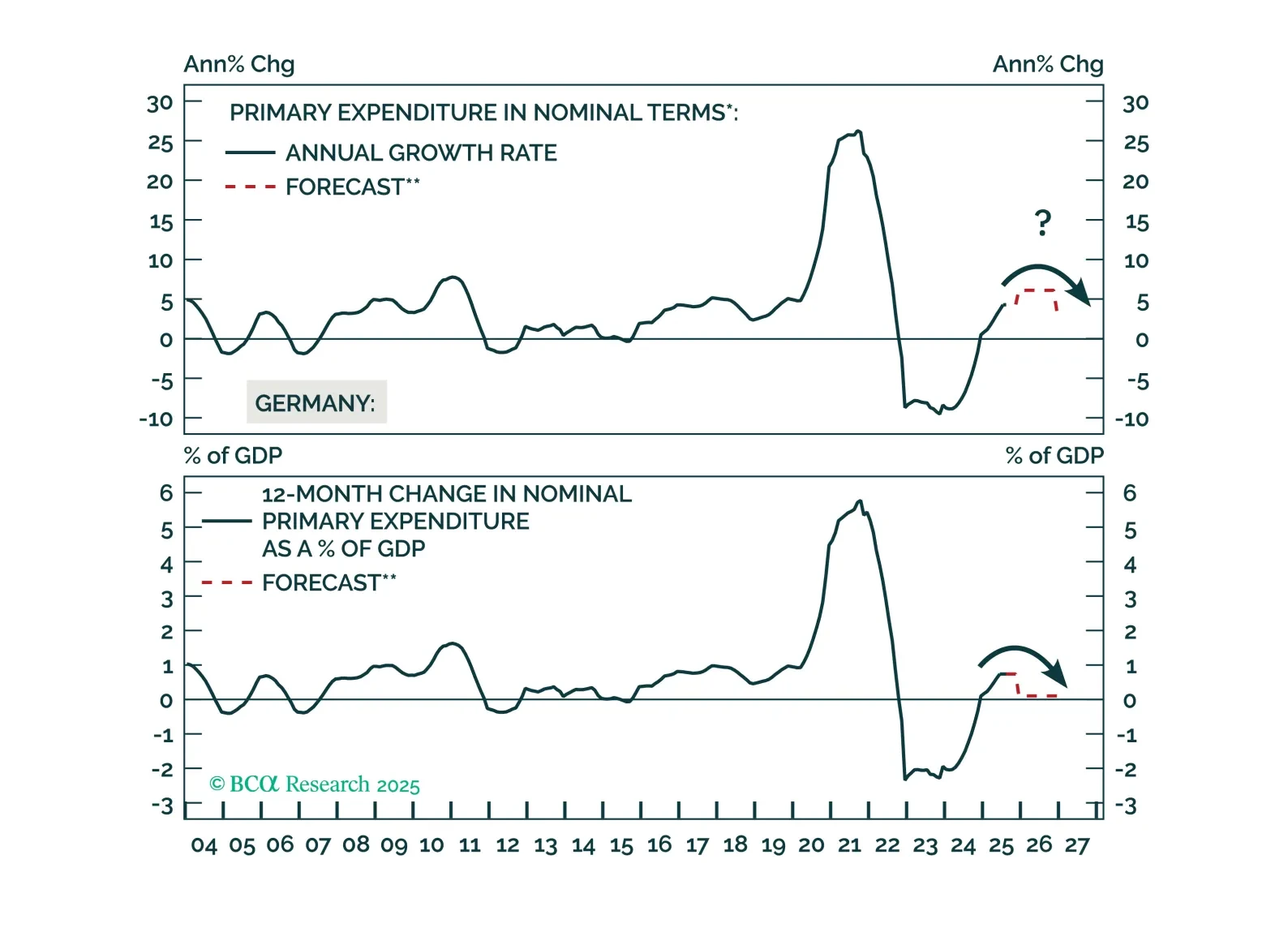

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

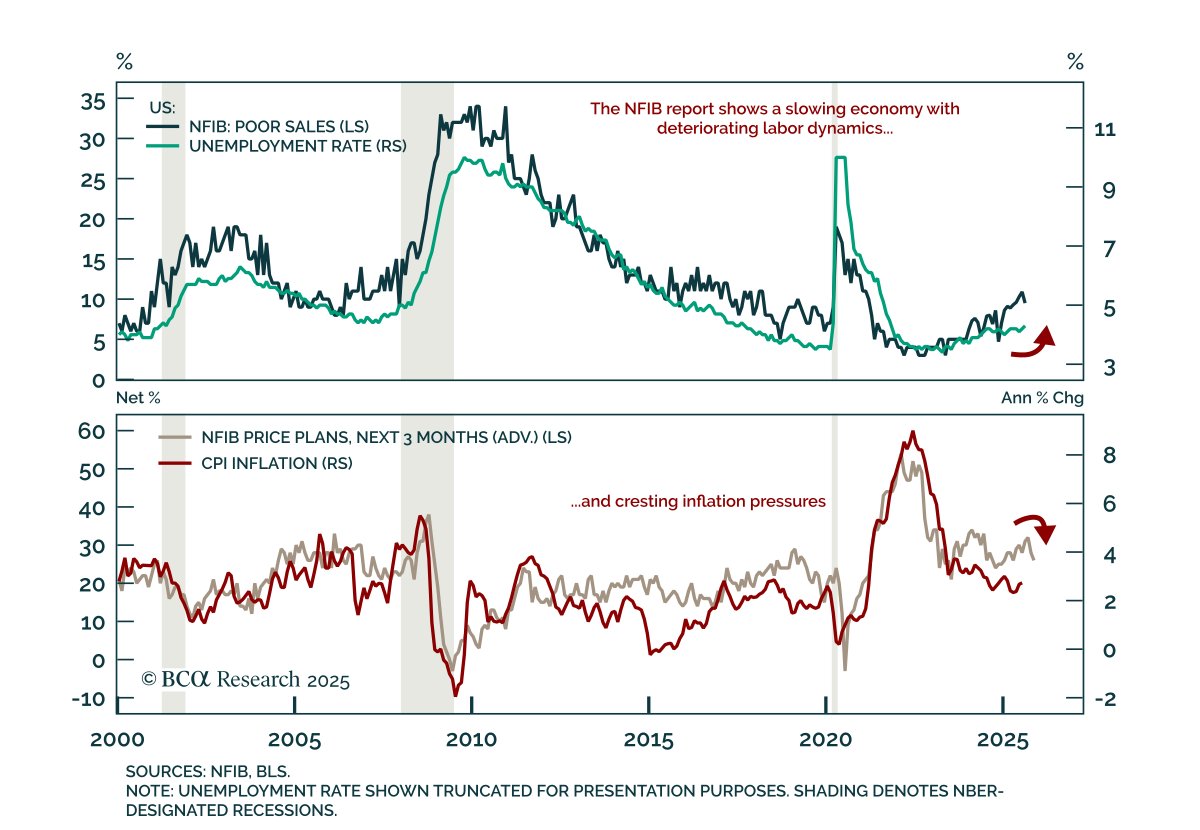

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

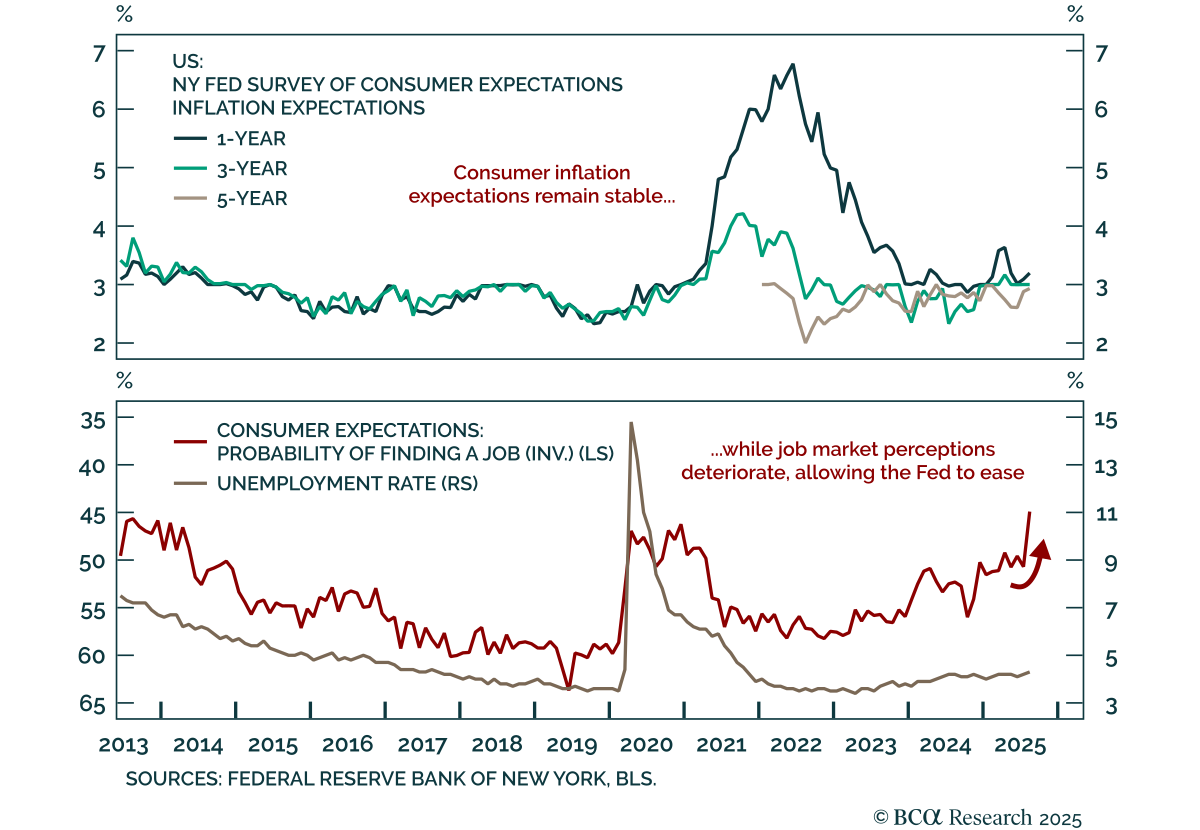

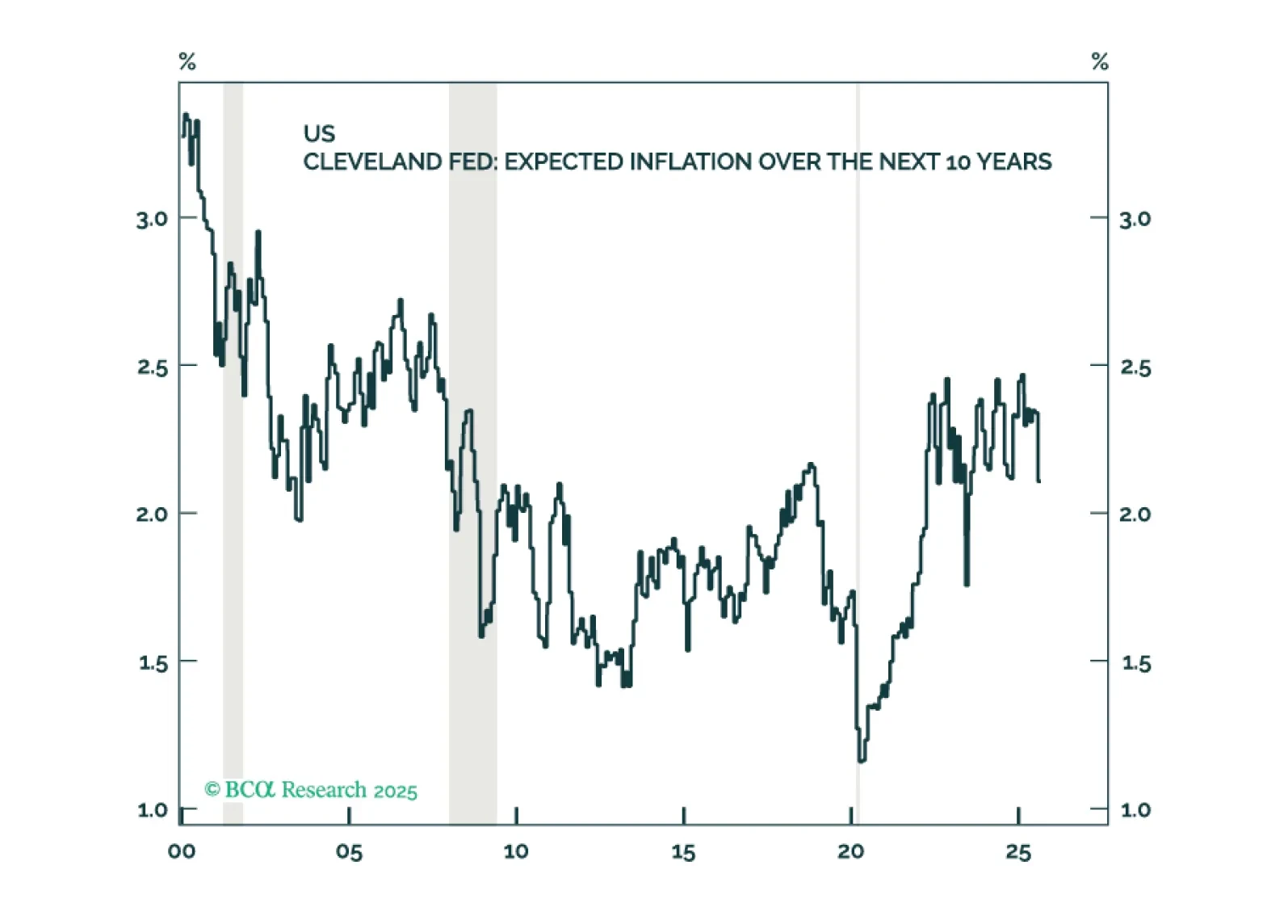

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.