Italy

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

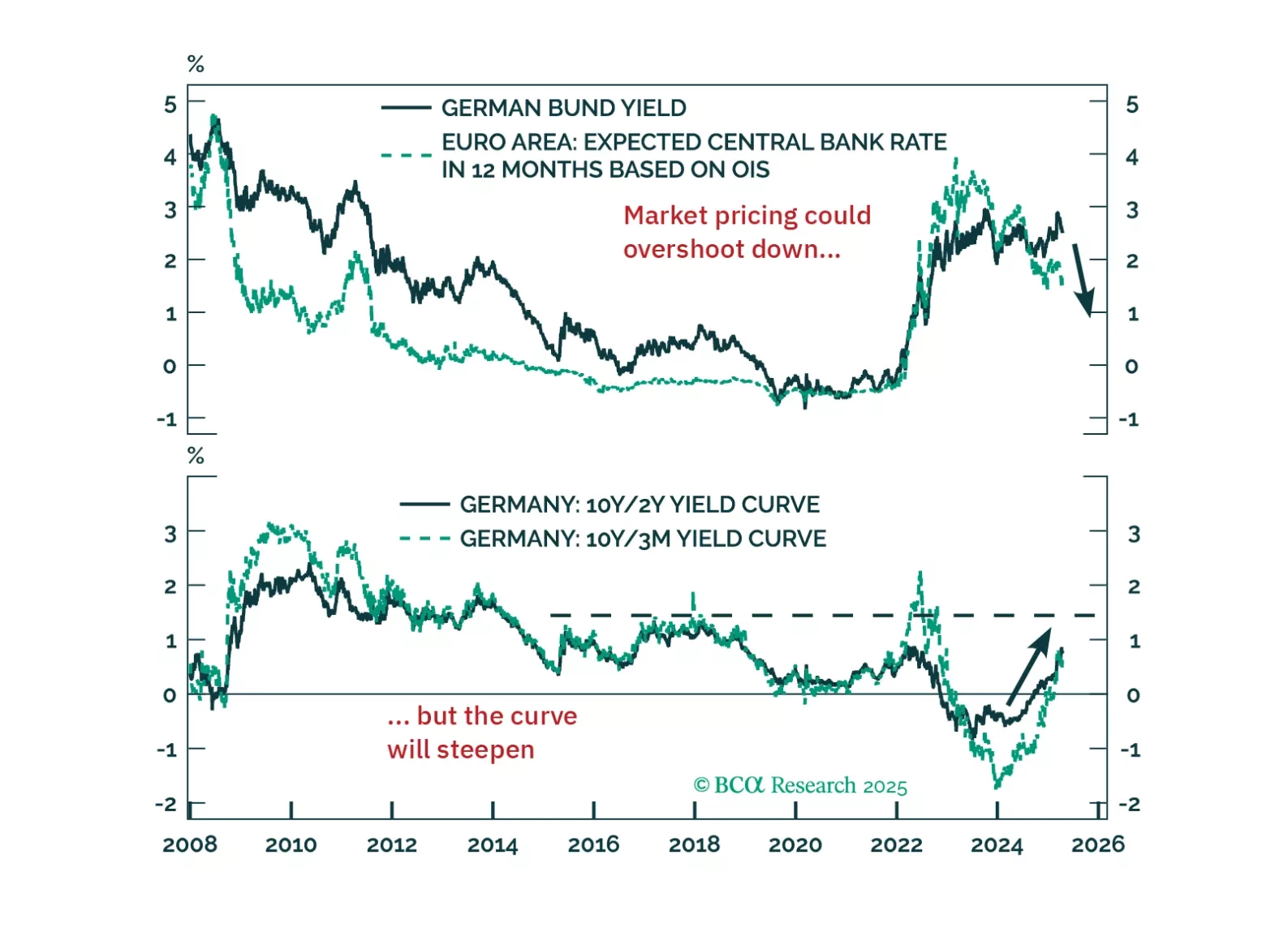

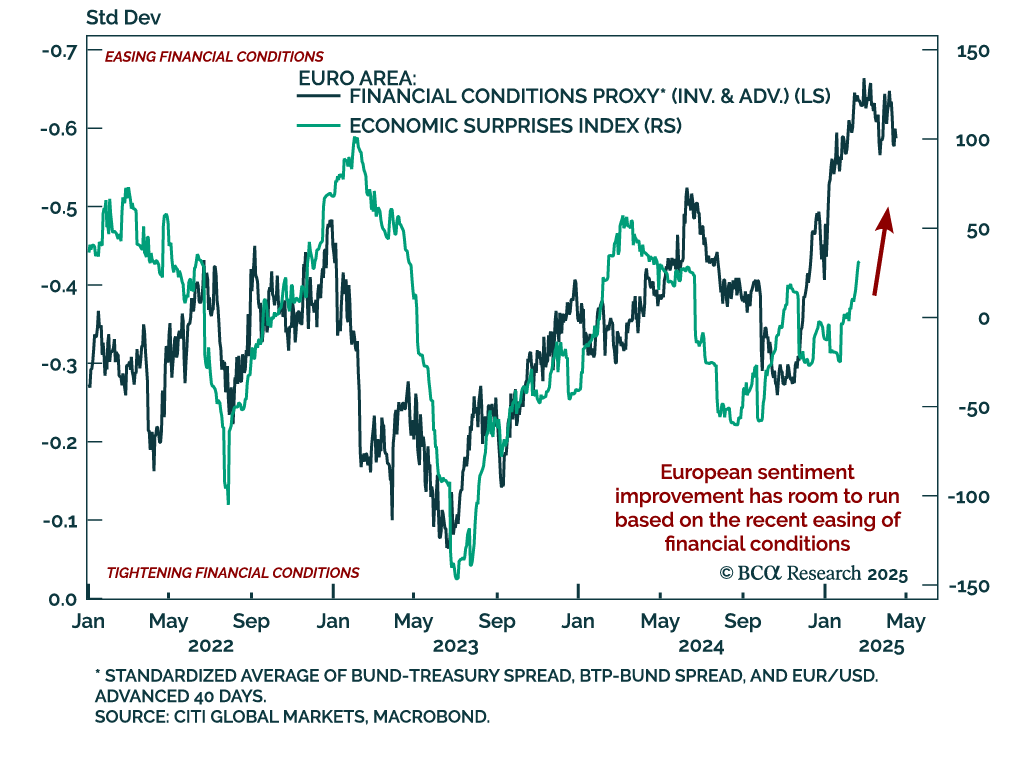

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.

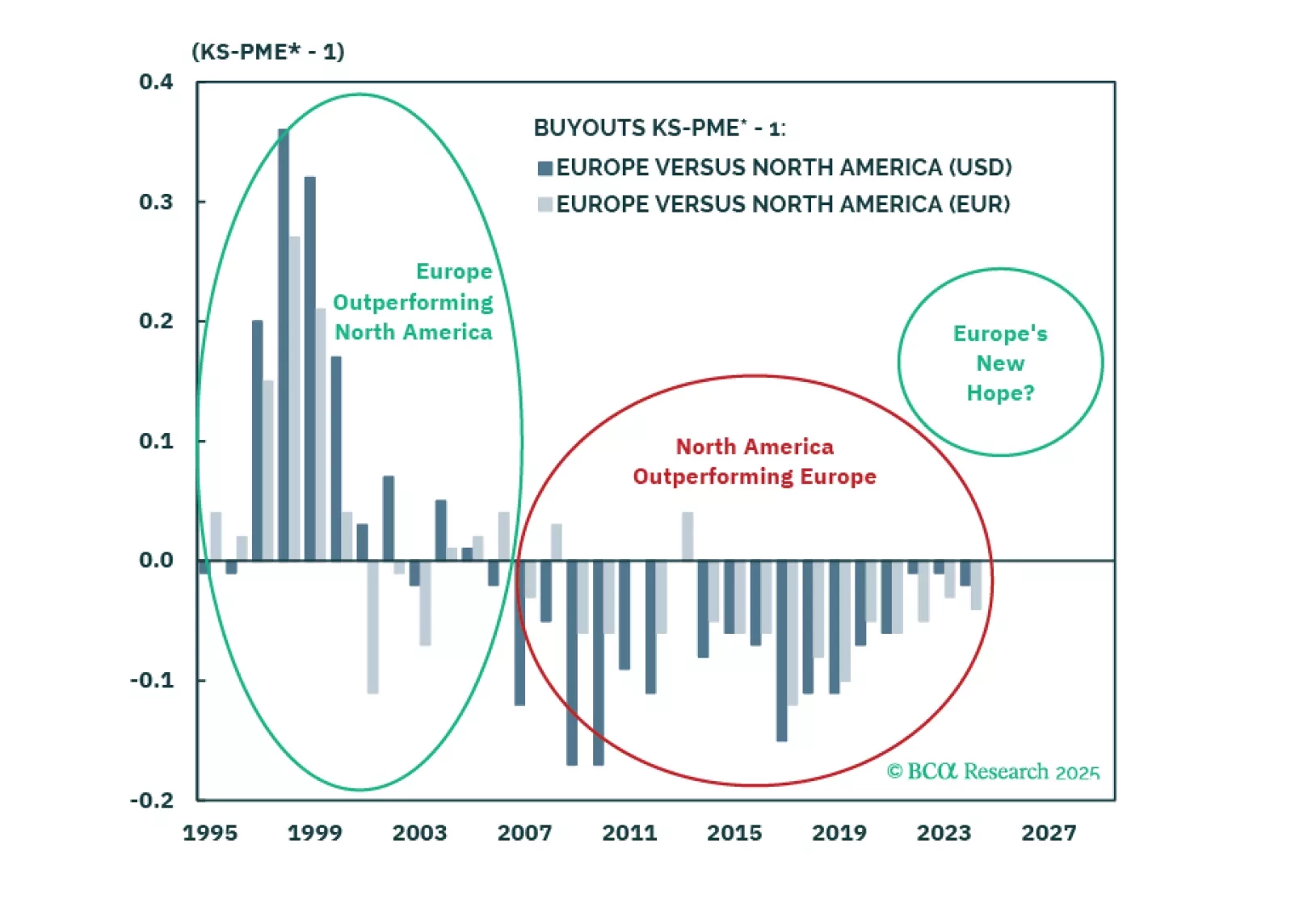

We are at a pivotal moment for Europe, supported by structural reforms and macro catalysts. While expanding credit markets and lower rates favor Private Equity over Private Credit, opportunities vary by segment. Large+ Buyouts are attractive as markets have priced in structural challenges. We downgrade Europe Private Credit, remain neutral on Europe Private Equity broadly but overweight Europe vs. North America in PE portfolios.

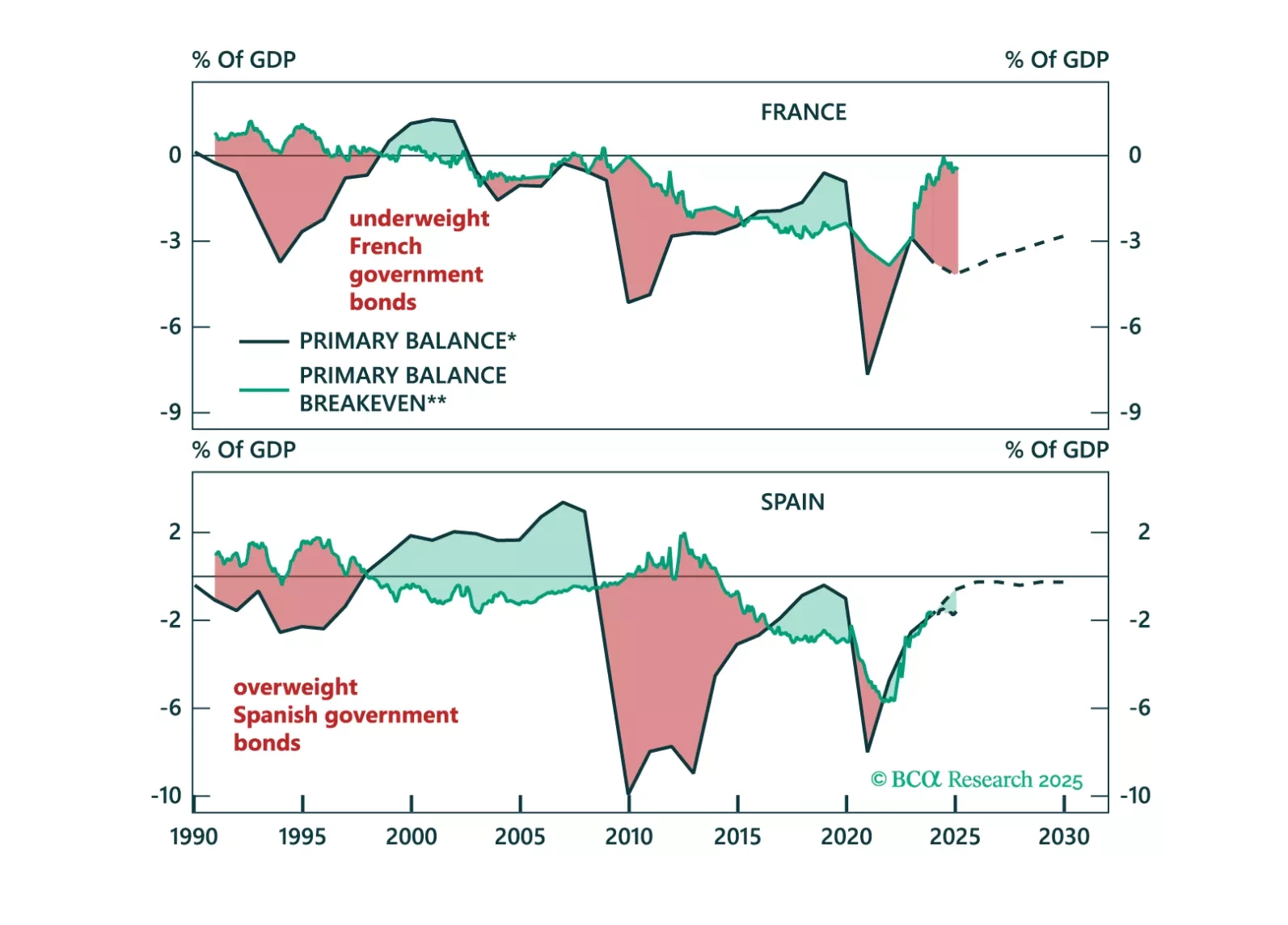

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.

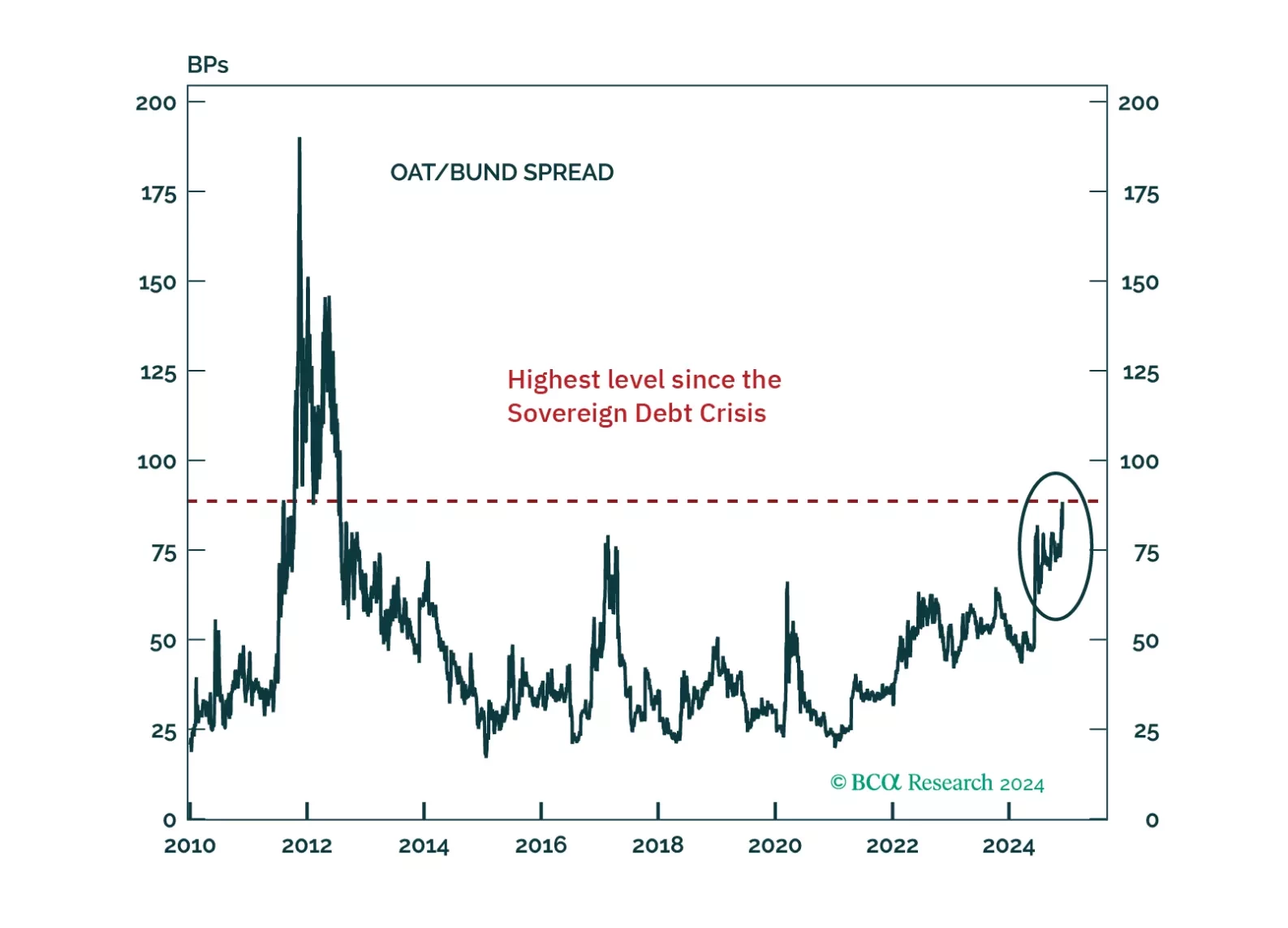

France finds itself in a unique, thorny situation. Can it heave itself out of it? And what does it mean for investors?

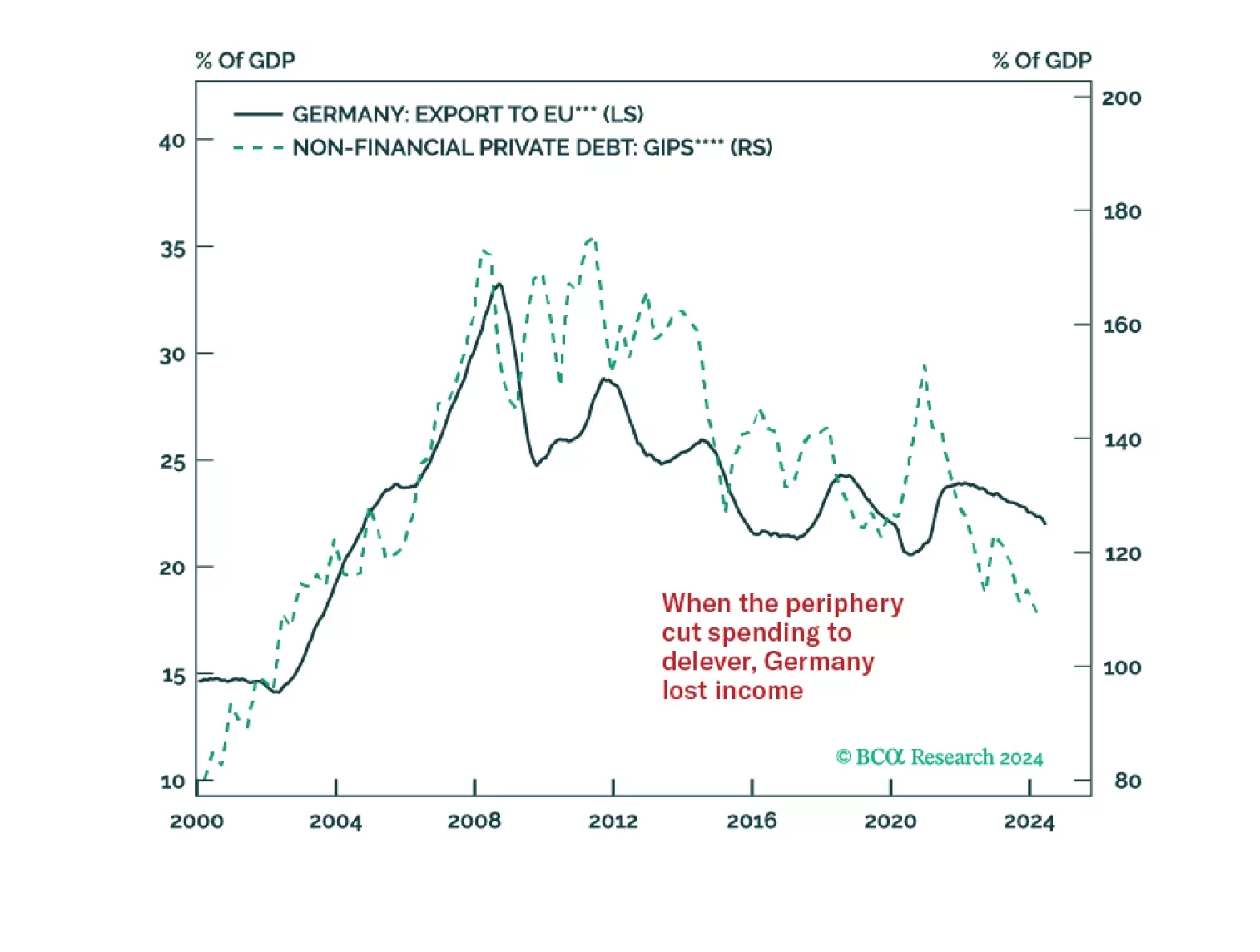

Germany’s economy has lagged that of the rest of Europe for nearly 10 years. So have German stocks. Investors are extrapolating these trends to bet on the country’s deindustrialization. Could Germany manage to beat dismal expectations?