Inflation Protected

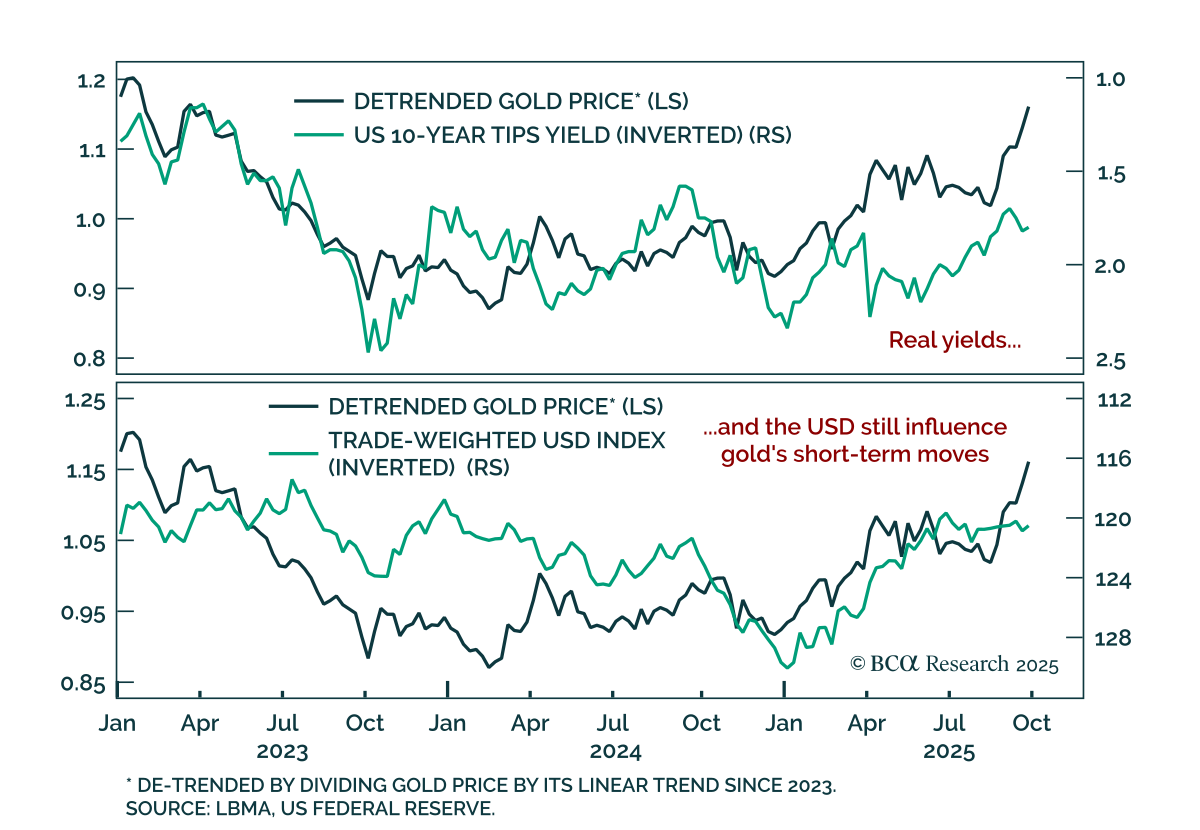

Gold’s decisive break above $4,000/oz, extending gains to over 55% year-to-date, reinforces the structural bull case driven by persistent central bank demand and mounting fiscal concerns globally, supporting an overweight stance in bullion relative to other…

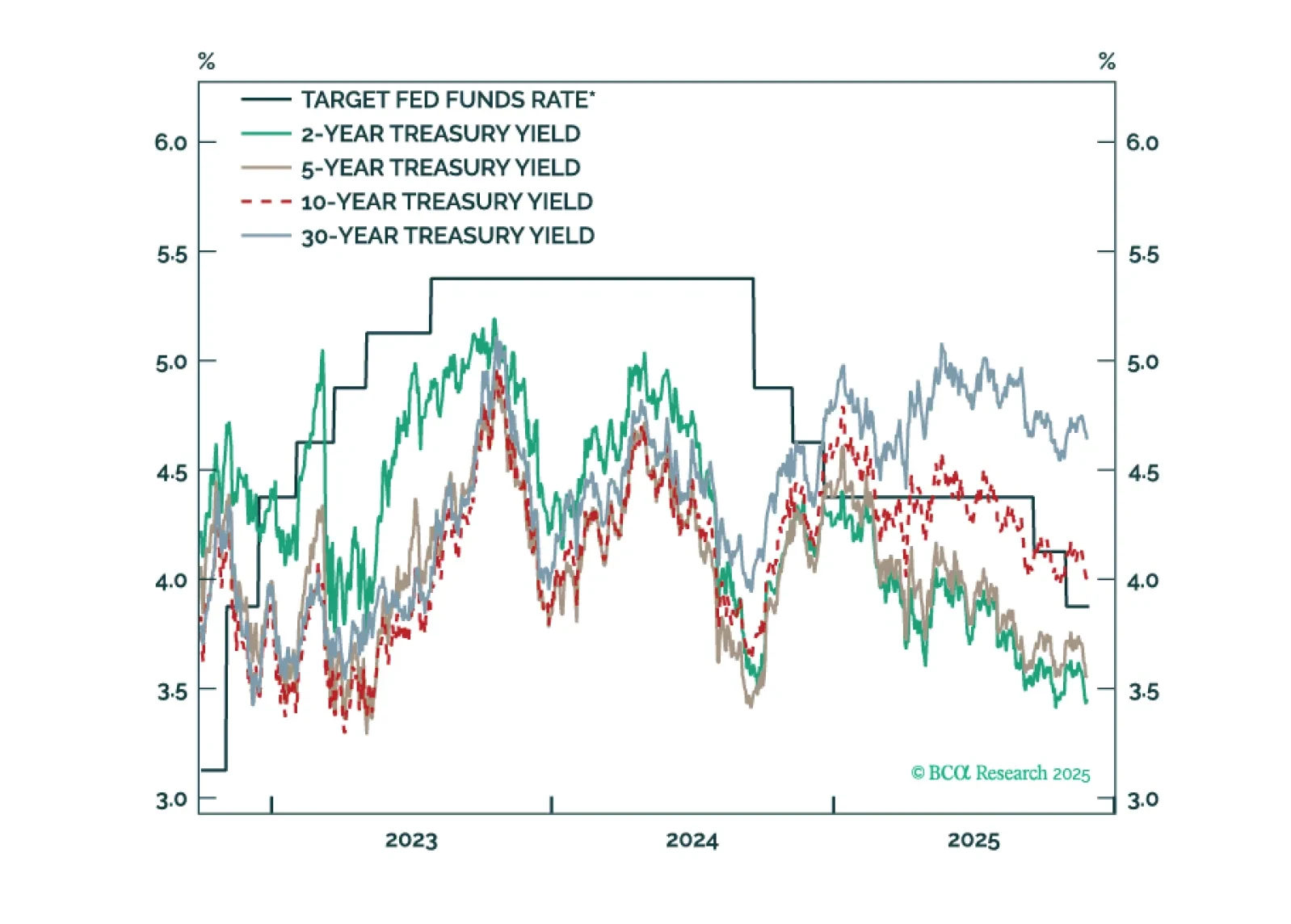

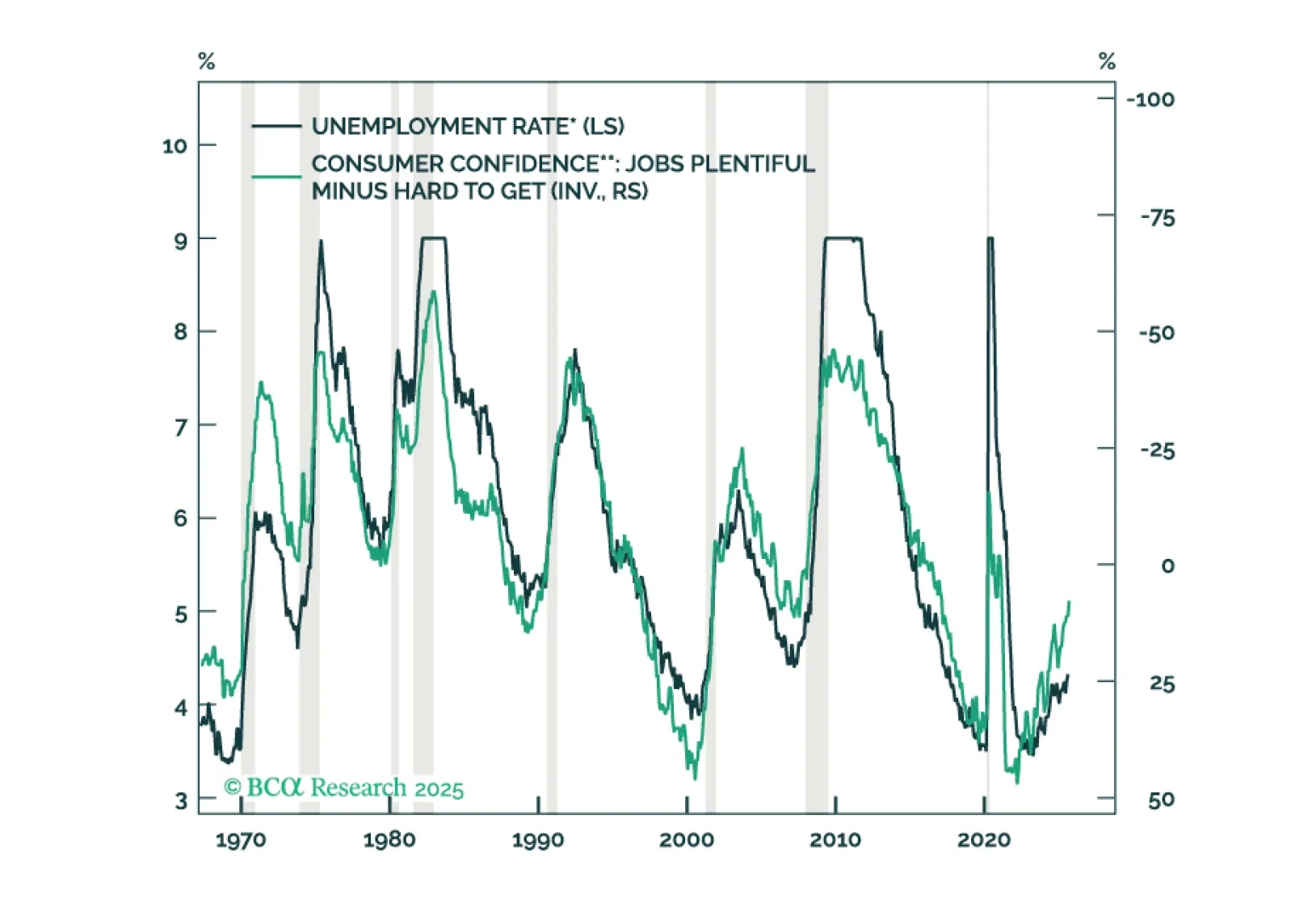

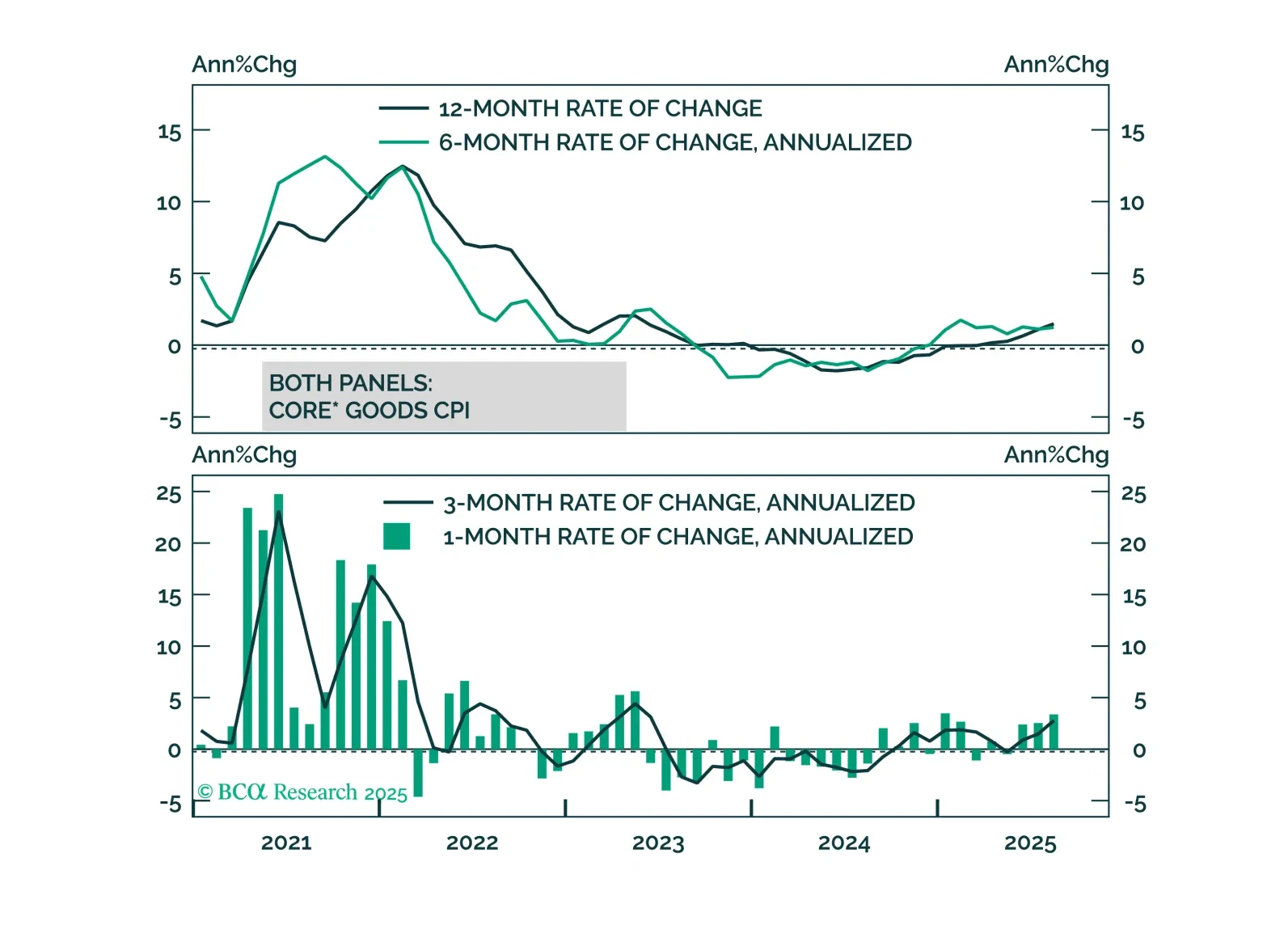

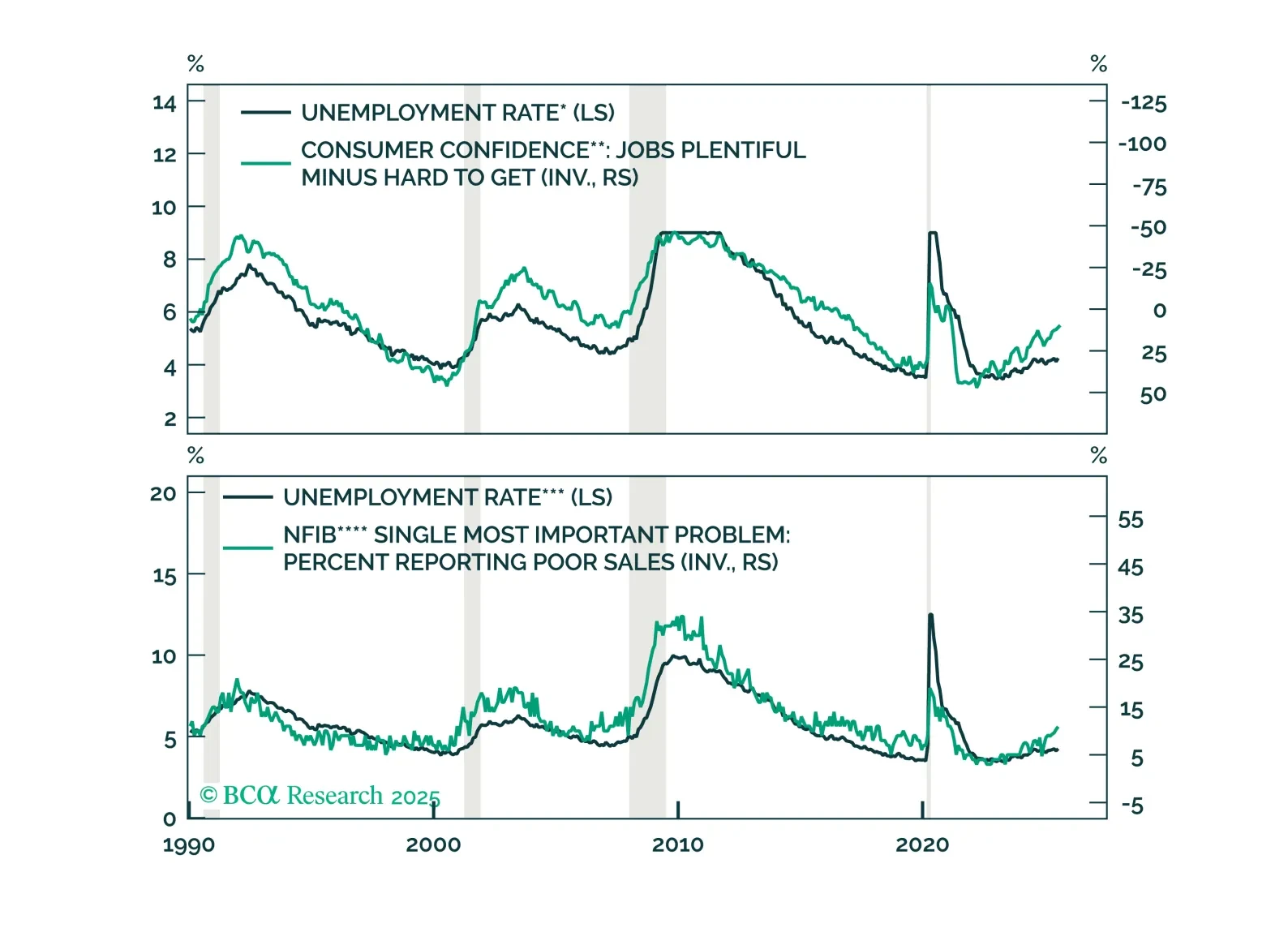

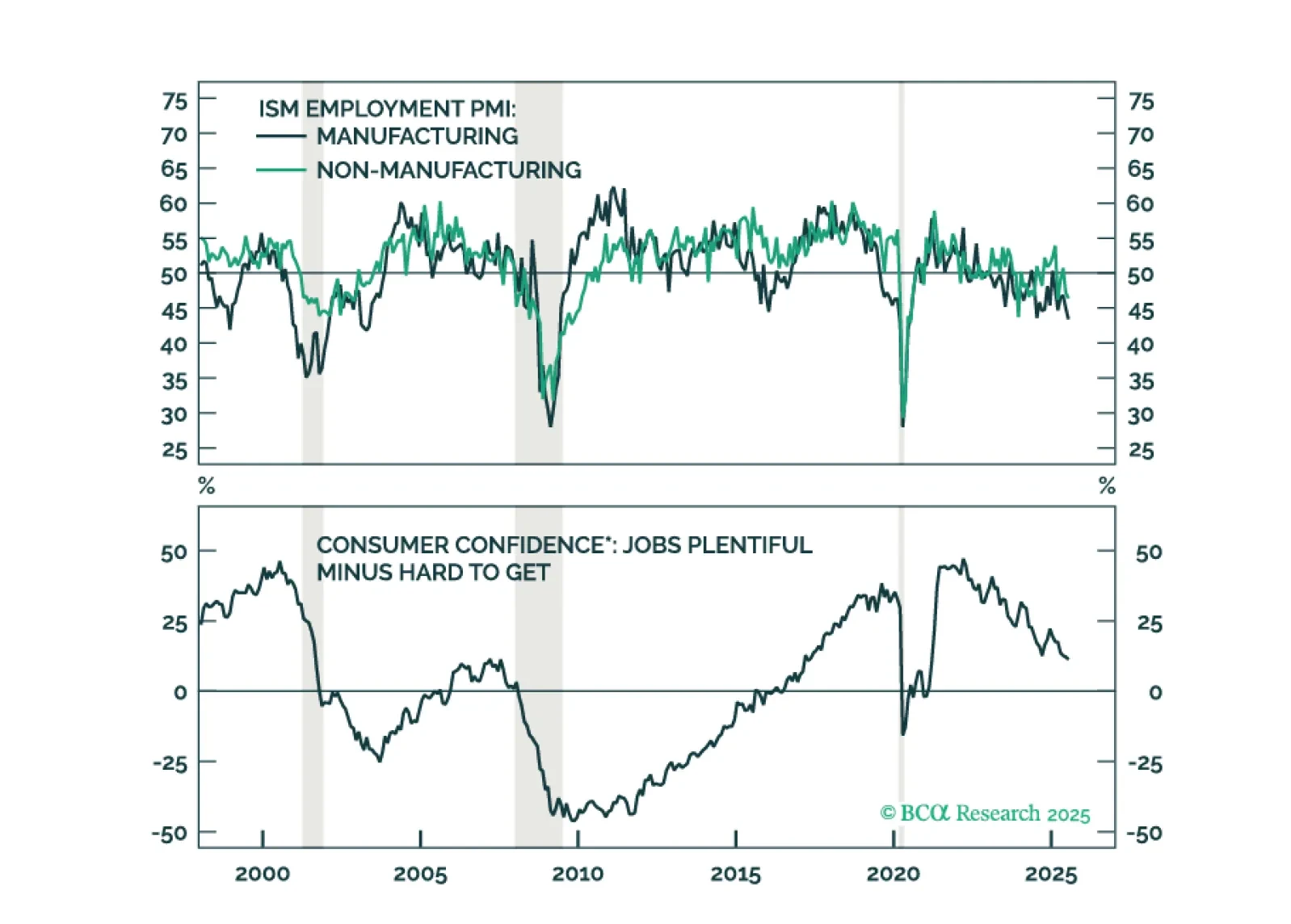

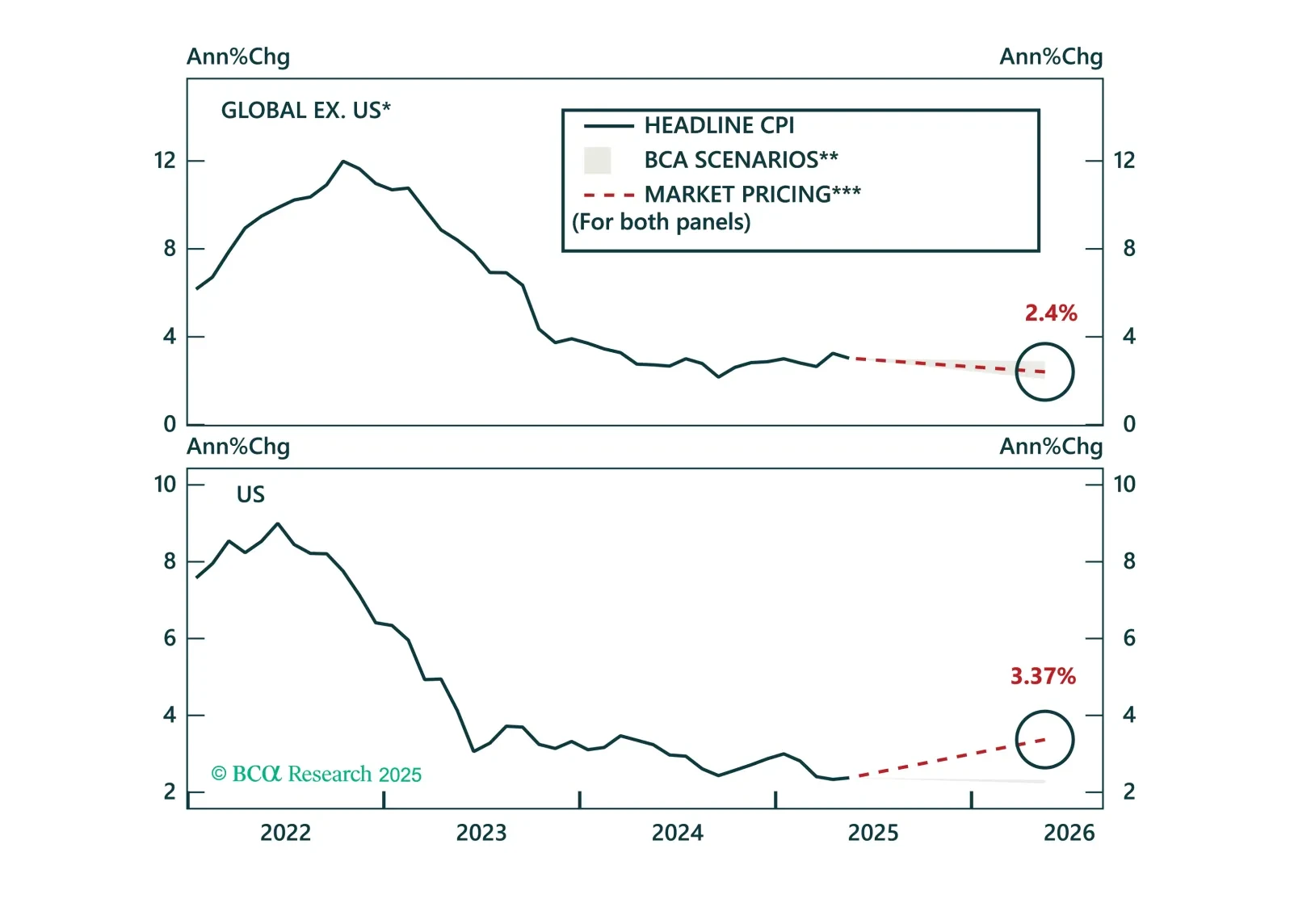

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

Disinflation continues to unfold globally, and markets are finally catching up. Inflation expectations have broadly realigned with fundamentals, prompting us to shift our global ILB allocation to neutral. While tariff risks are inflating US expectations, pricing in the UK, Japan, and Australia has adjusted sharply. Today’s Strategy Report reviews these developments and updates our country-level ILB positioning.