Inflation

The Fed held rates steady this afternoon, and the timing of its next move will be dictated by whether the tariff shock to inflation is transitory or more long lasting.

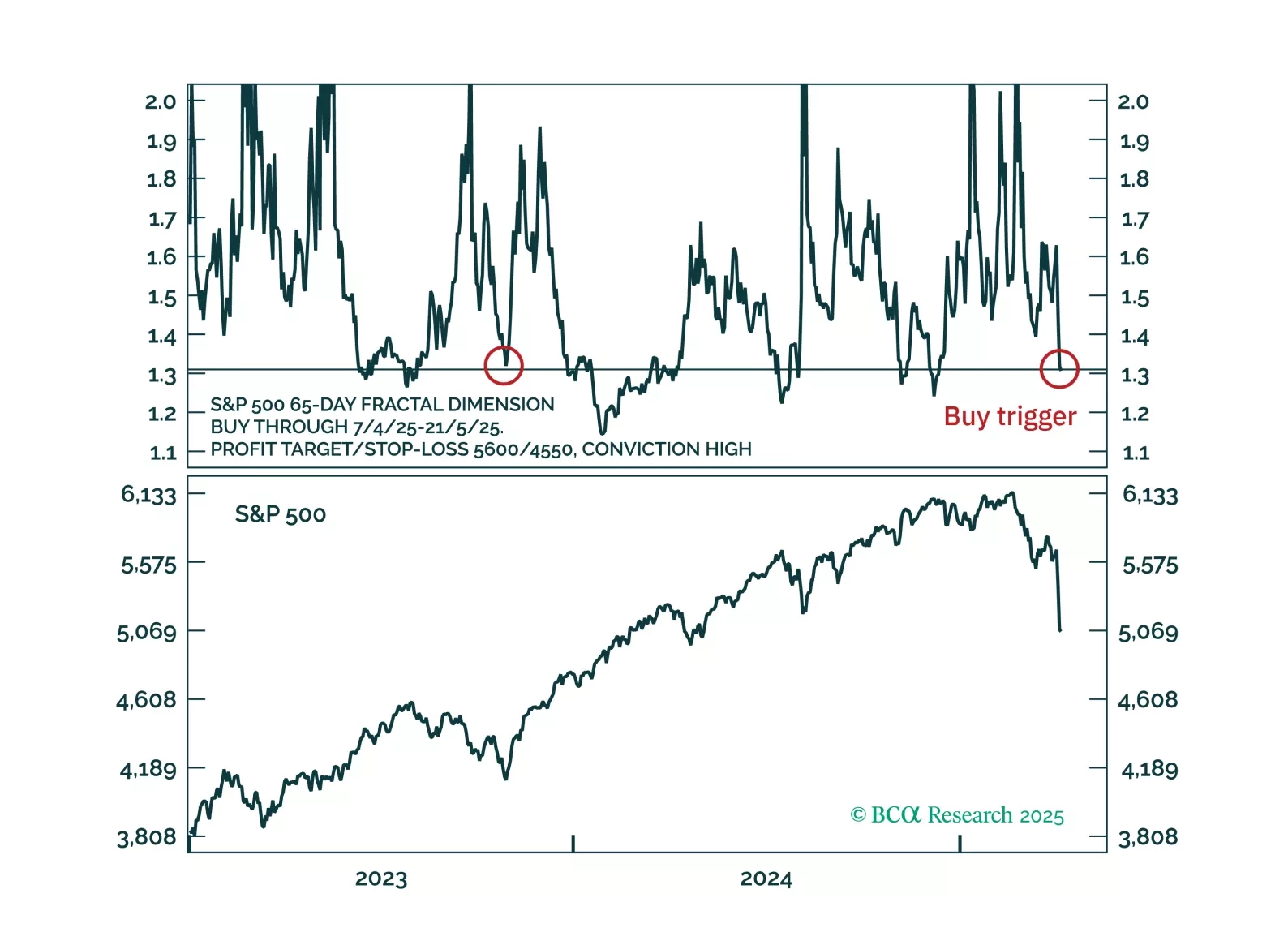

Countertrend buy triggers have been activated for the S&P 500, Nasdaq and Nasdaq versus 30-year T-bond.

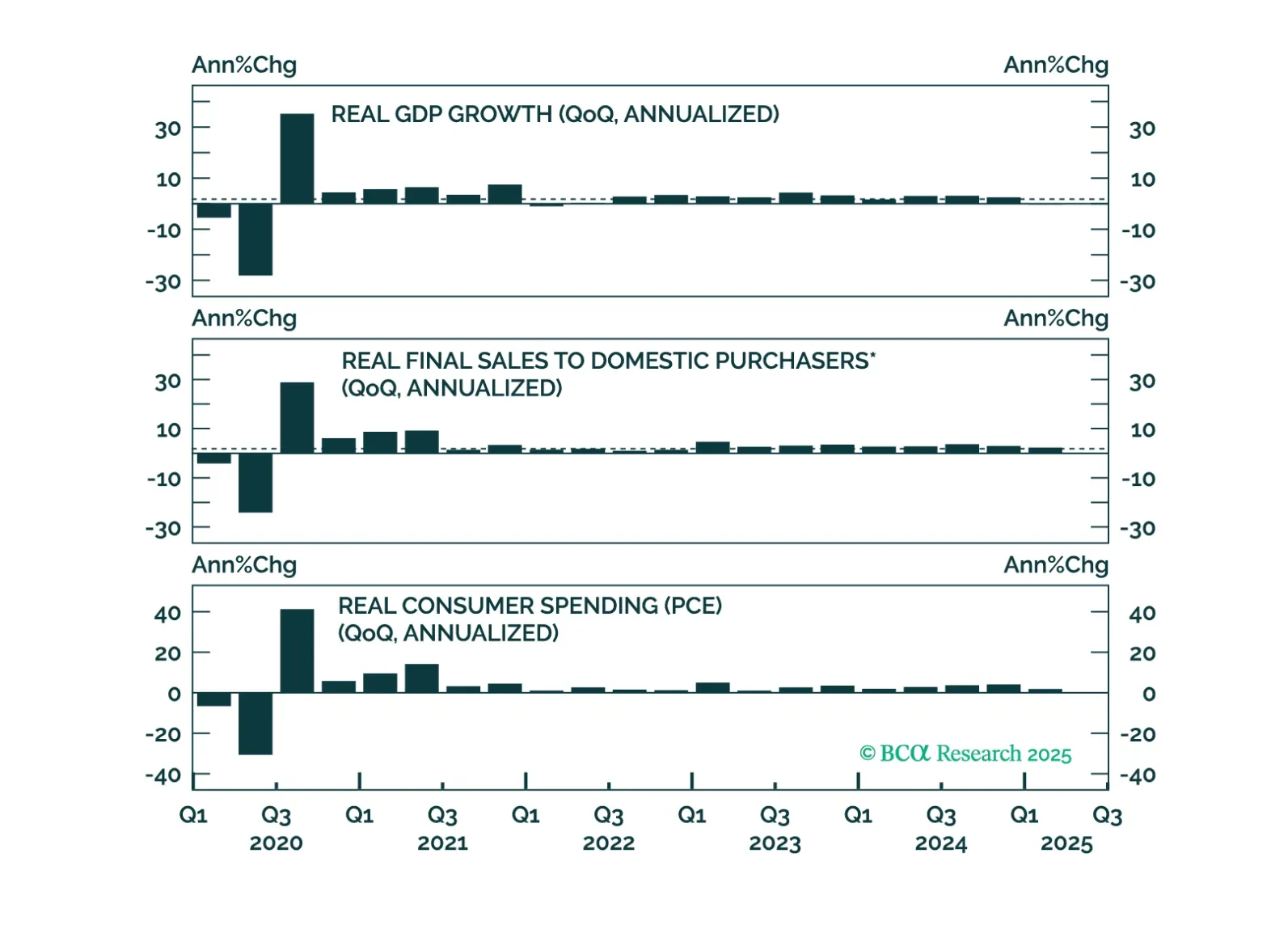

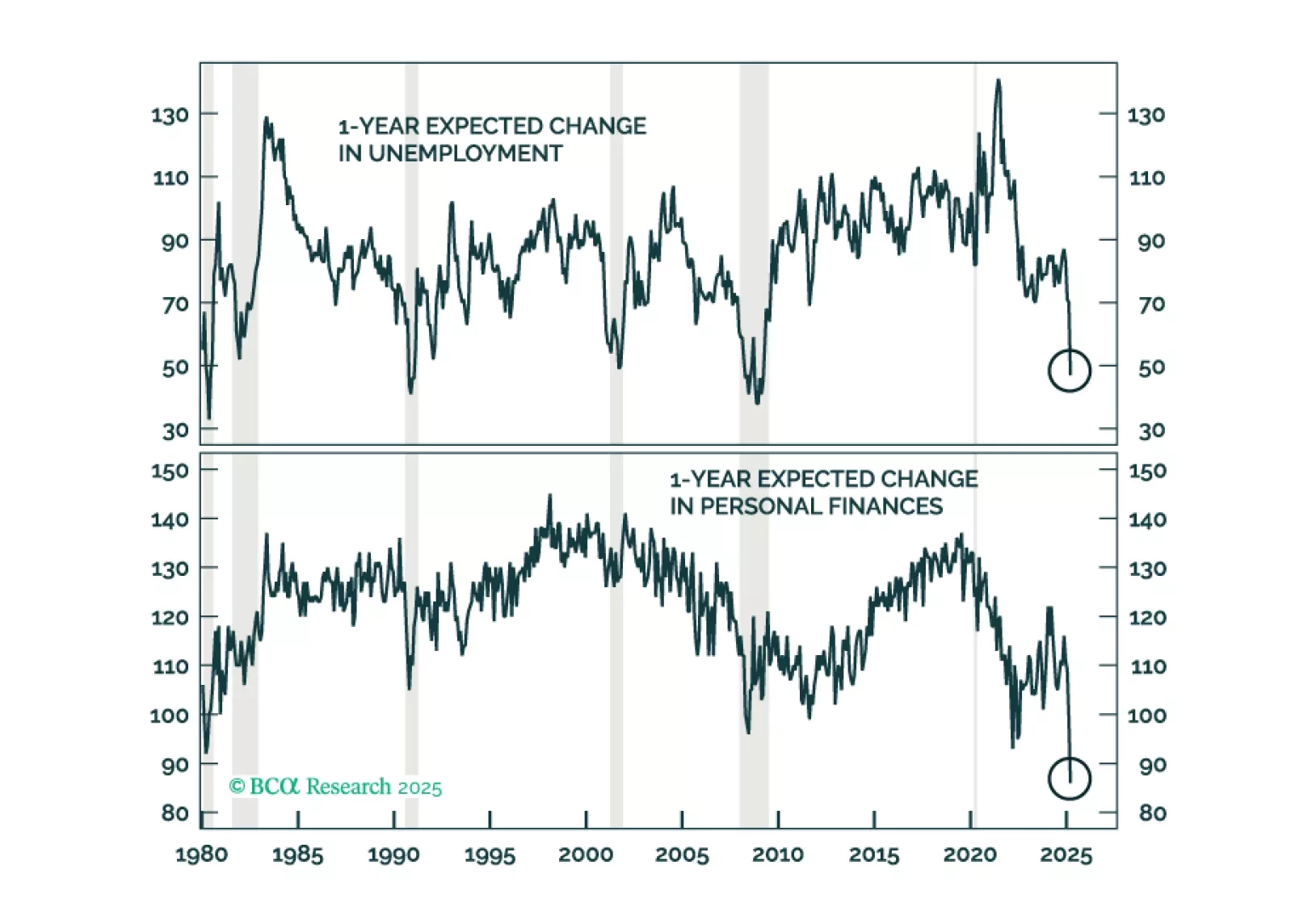

The stimulus measures driving the post-COVID expansion were beginning to wane after five years and pointing the economy in the direction of an organically occurring recession. Now that DOGE and the multi-front trade war have sped up the timetable, we reiterate our risk-off recommendations.

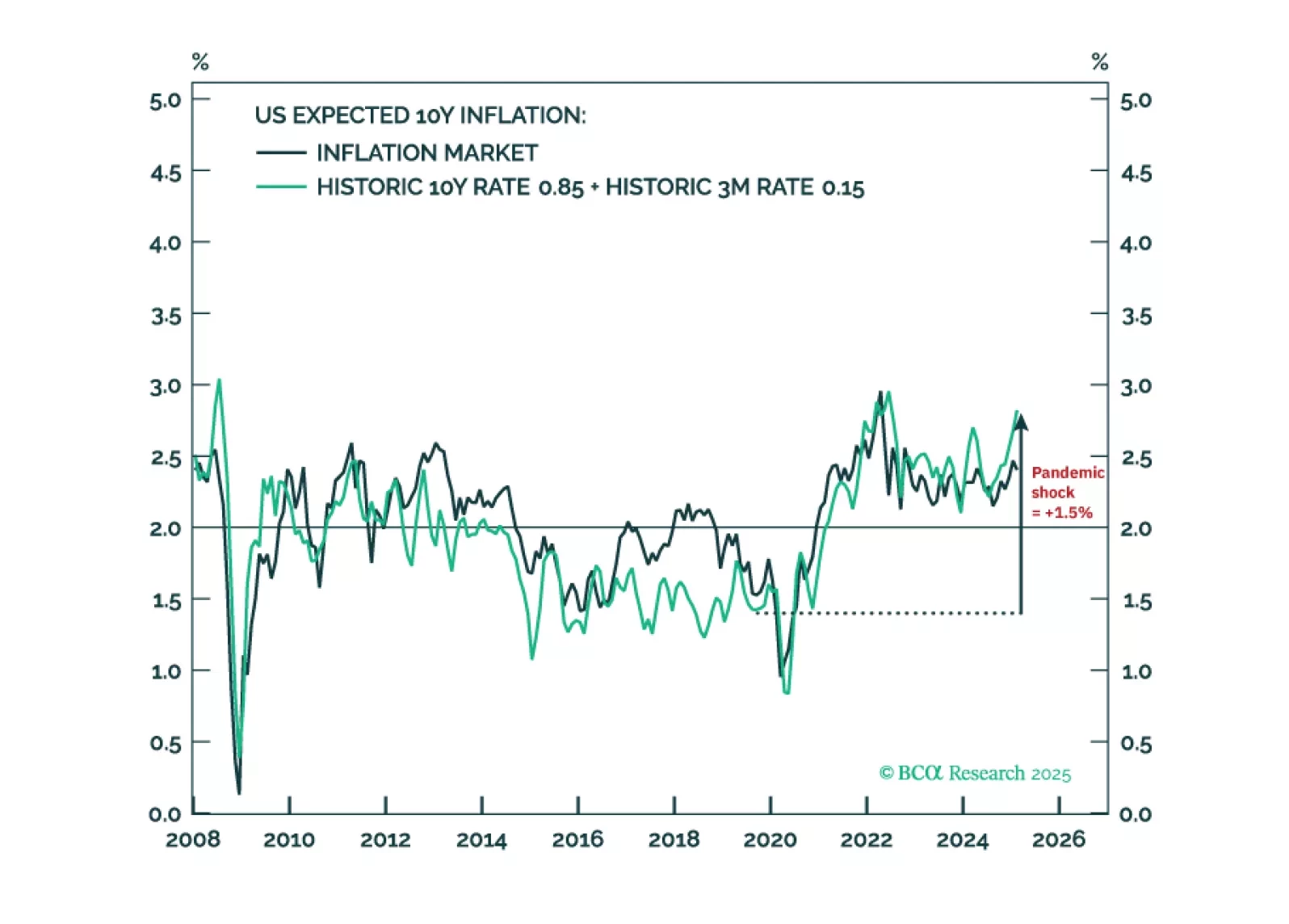

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

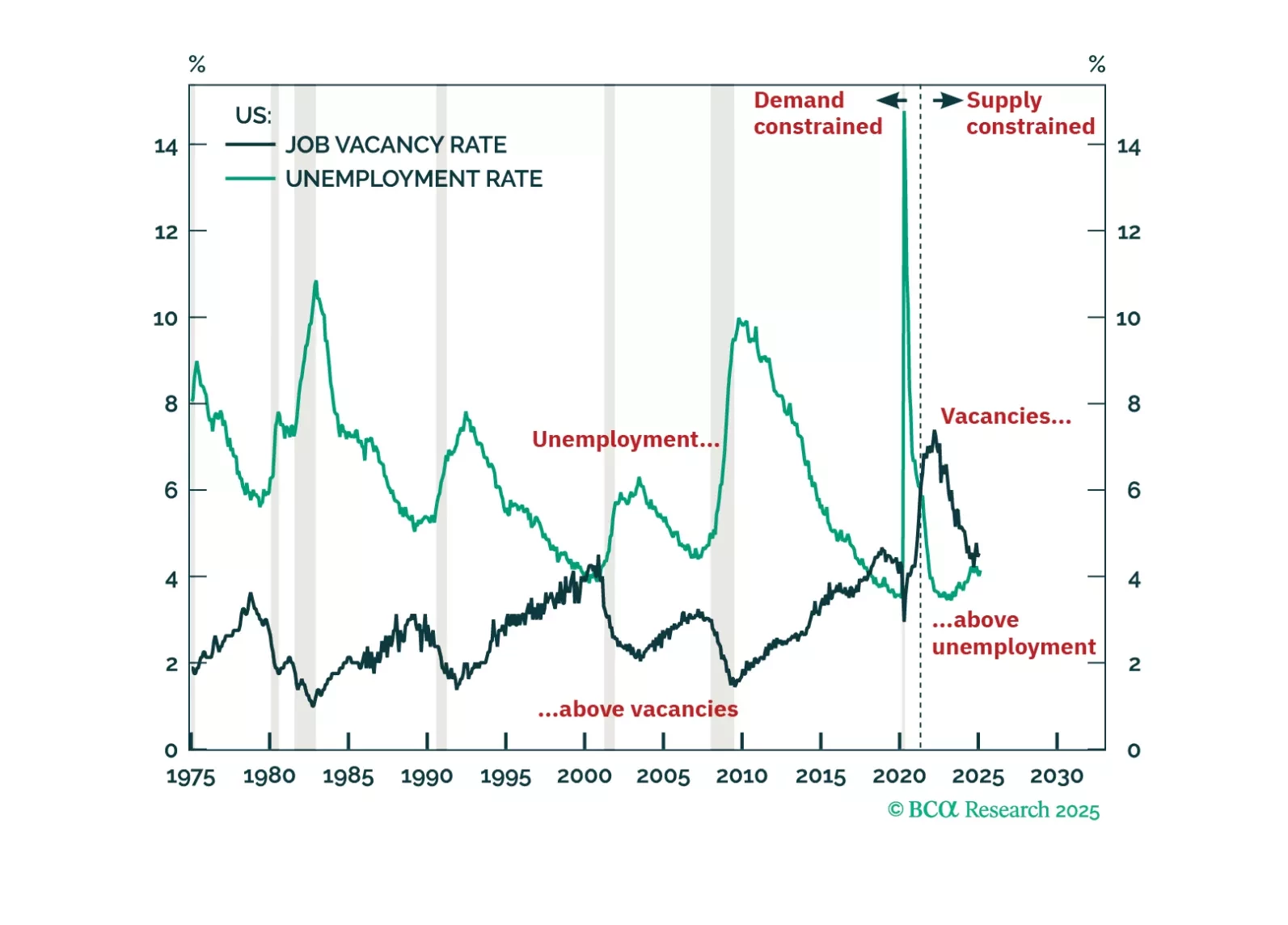

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.

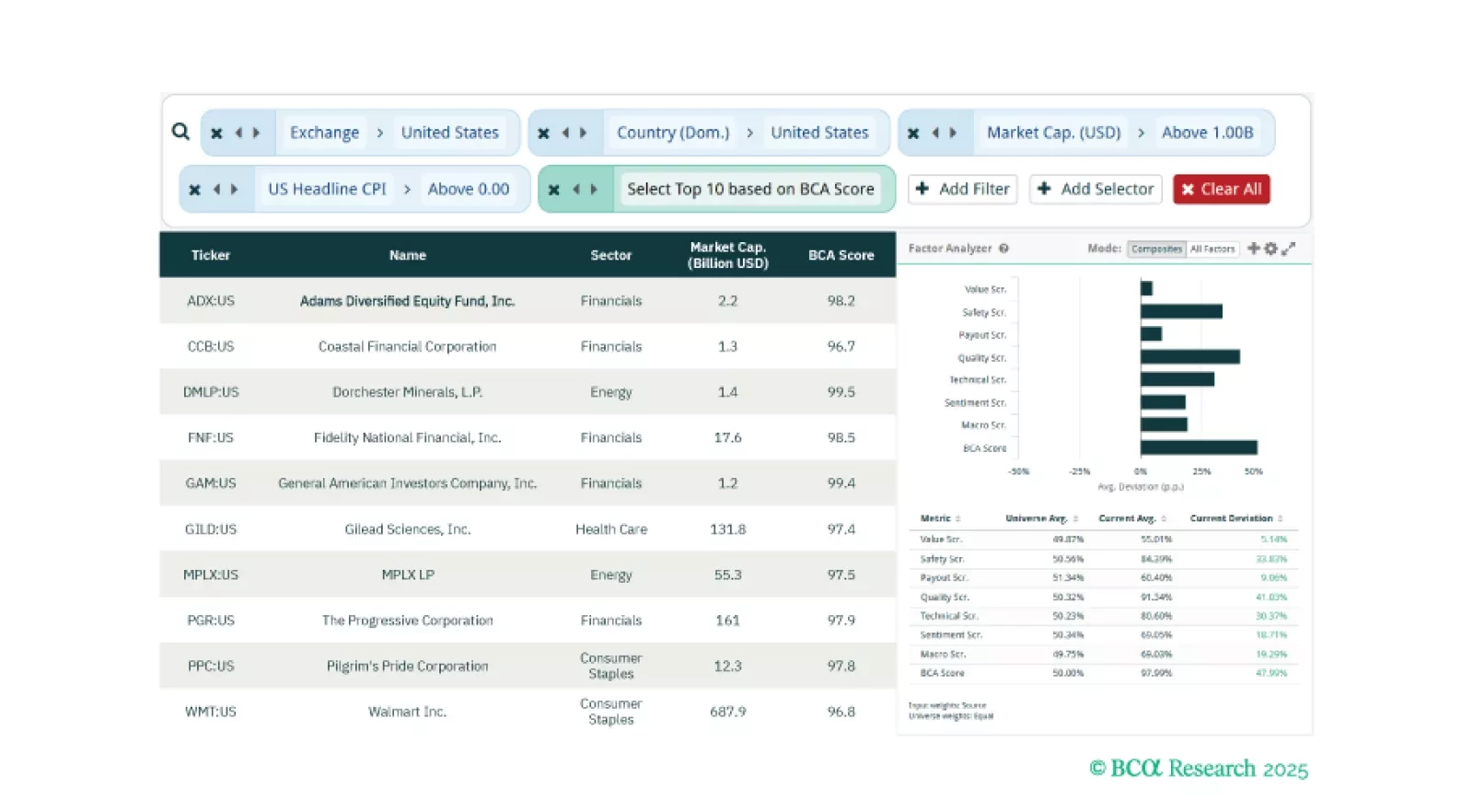

This week, our three screeners cover equity plays for “transitory” inflation impacts from US tariffs, a correction in sentiment within the European Aerospace and Defense industry, and Value Investor, Warren Buffett’s Philosophy.

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

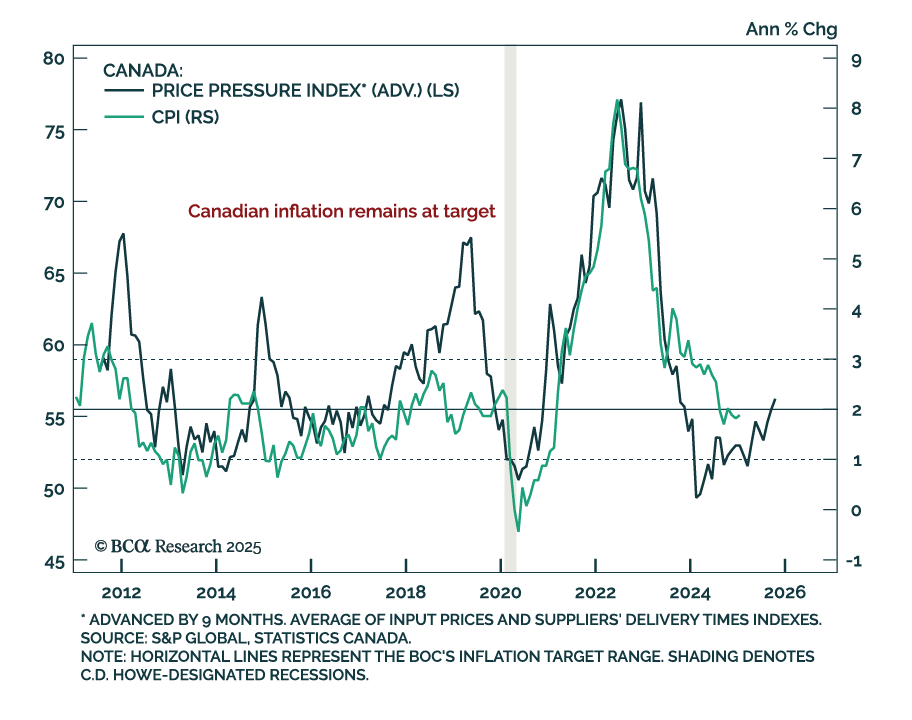

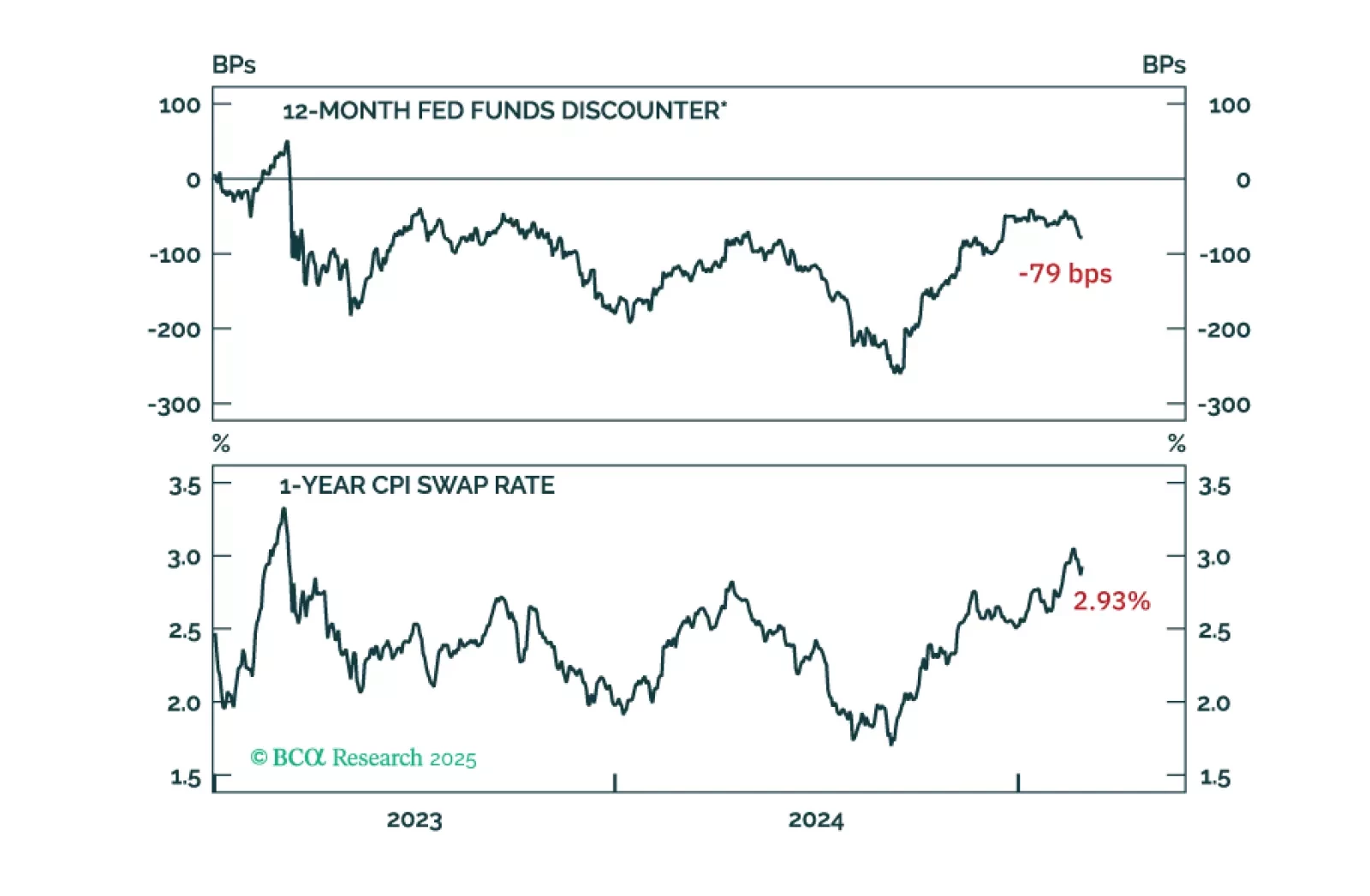

Core PCE inflation was tame this morning, but with large tariffs looming we anticipate loftier inflation readings in the months ahead.