Inflation/Deflation

According to BCA Research’s Counterpoint service, the ECB is the central bank that poses the lowest risk of repeating the mistakes of the 1970s and letting inflation expectations unanchor. One reason is the ECB’s inherited Germanic anti-inflation DNA. Even…

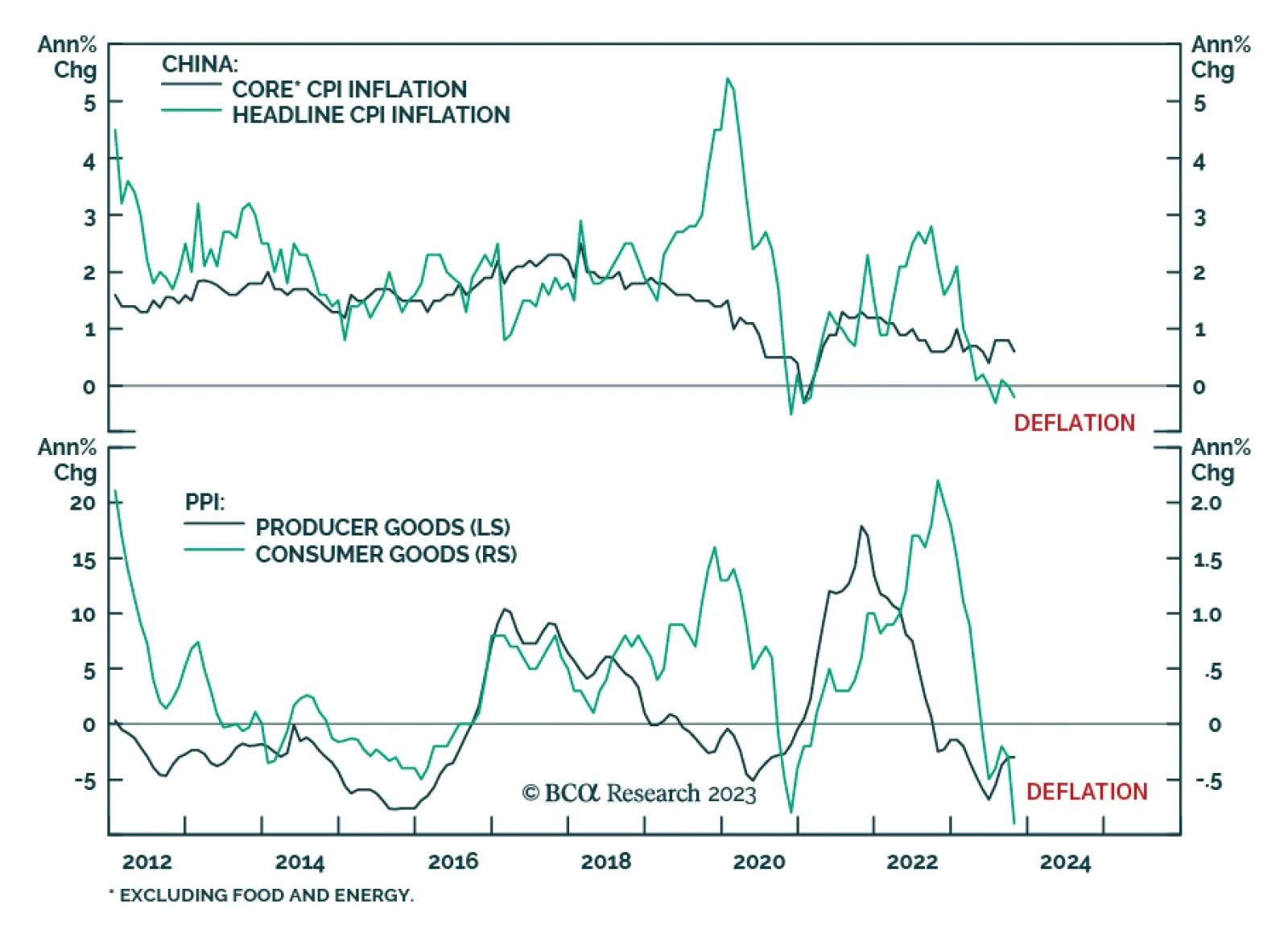

China's CPI and PPI inflation release for October indicates that deflationary pressures continue to dominate the domestic economy. After remaining unchanged in September, consumer prices declined by 0.2% y/y last month, falling below consensus estimates of a…

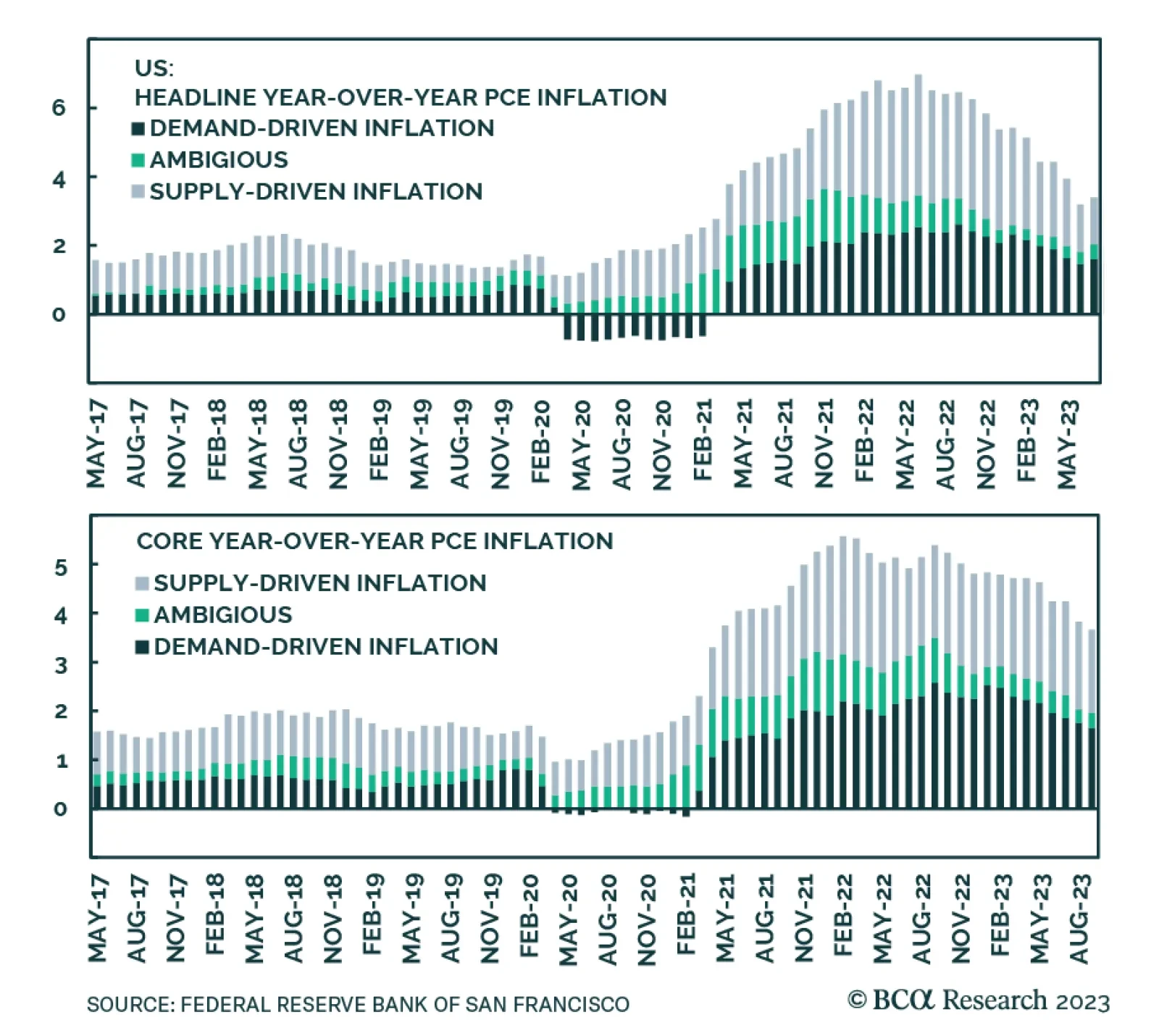

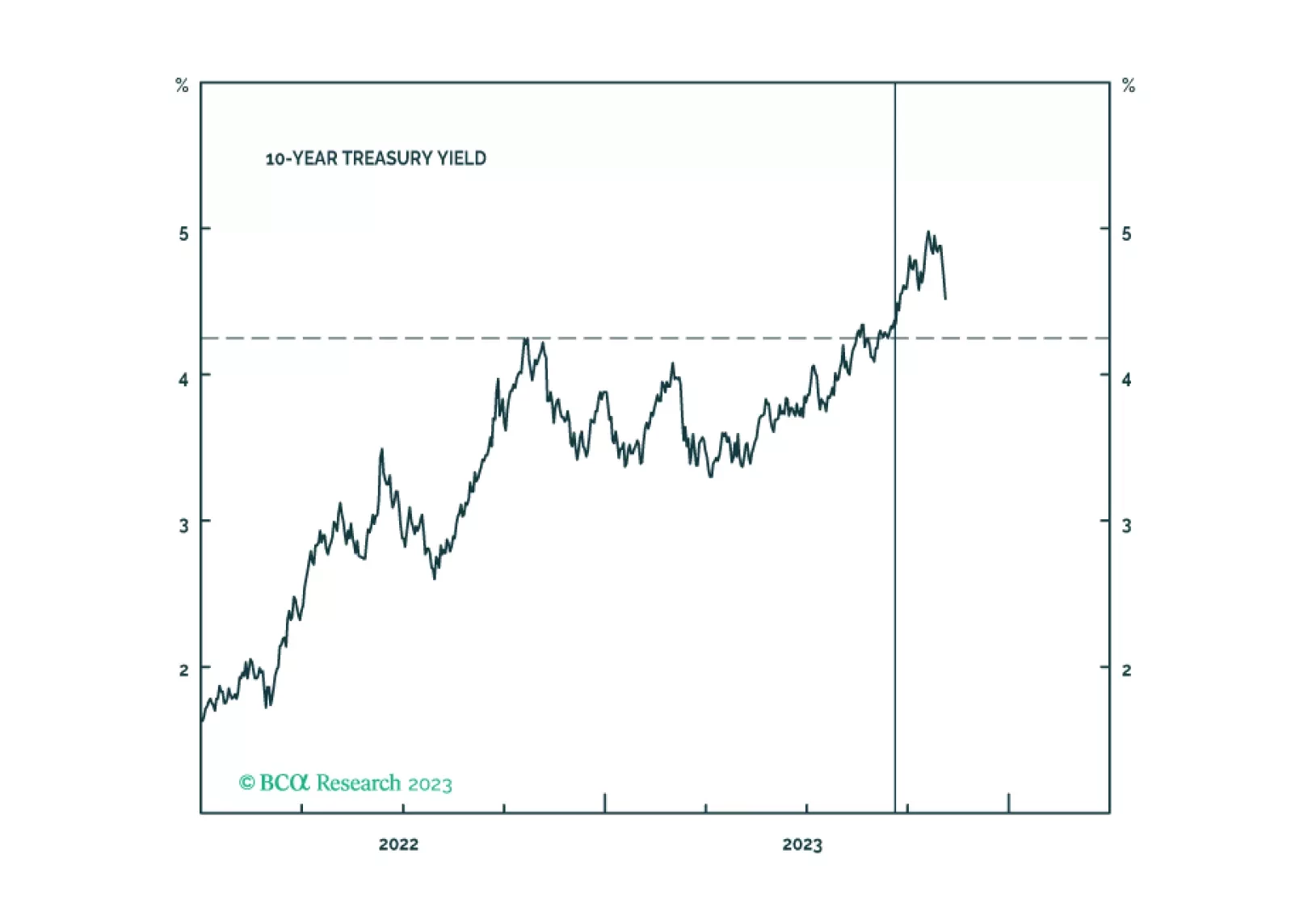

The US disinflationary trend remains intact. The core PCE deflator continued its downtrend in September, falling to 3.7% y/y from a peak of 5.6% in February 2022. Alternative measures of underlying price pressures such as the trimmed mean and median PCE…

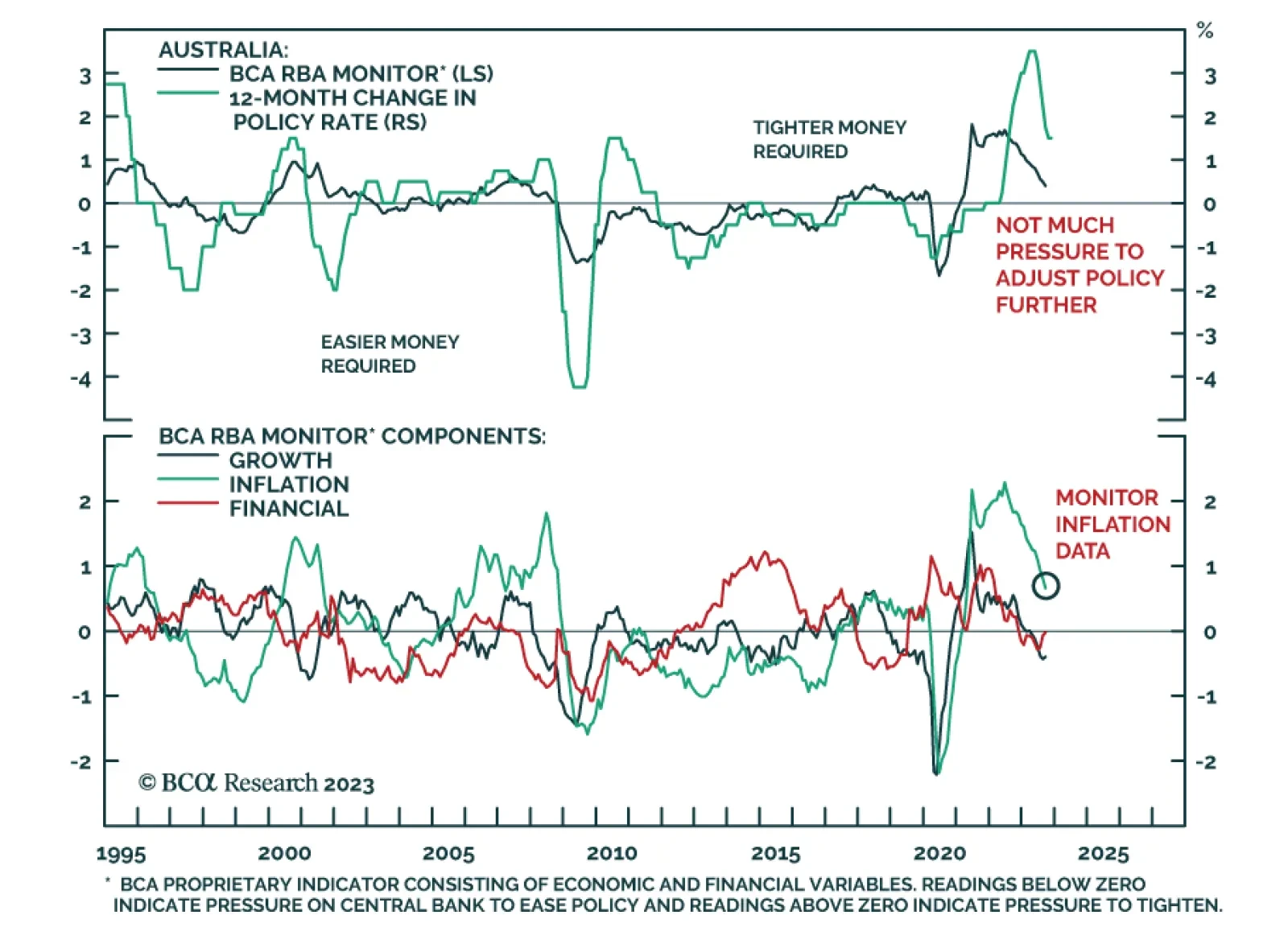

The Reserve Bank of Australia lifted the cash rate by 25 bps to a 12-year high of 4.35% on Tuesday, in line with consensus expectations. Governor Michele Bullock's post meeting statement underscored that although inflation is moderating, it remains too high…

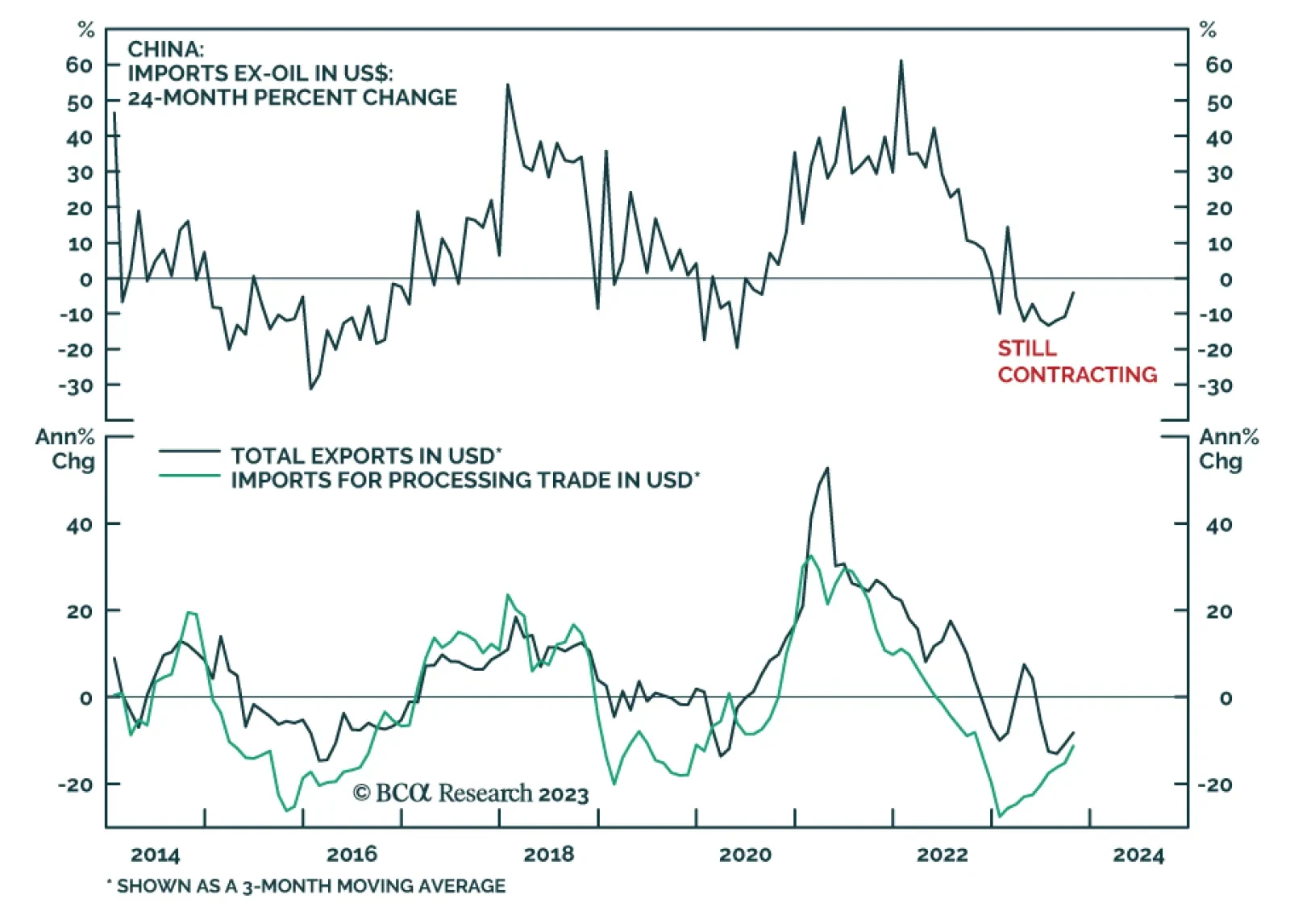

Chinese trade data for October delivered a mixed message on Tuesday. On the one hand, the export contraction deepened to -6.4% y/y following -6.2% y/y in September and surprised expectations that it would moderate to -3.5% y/y. Yet on the other hand, import…

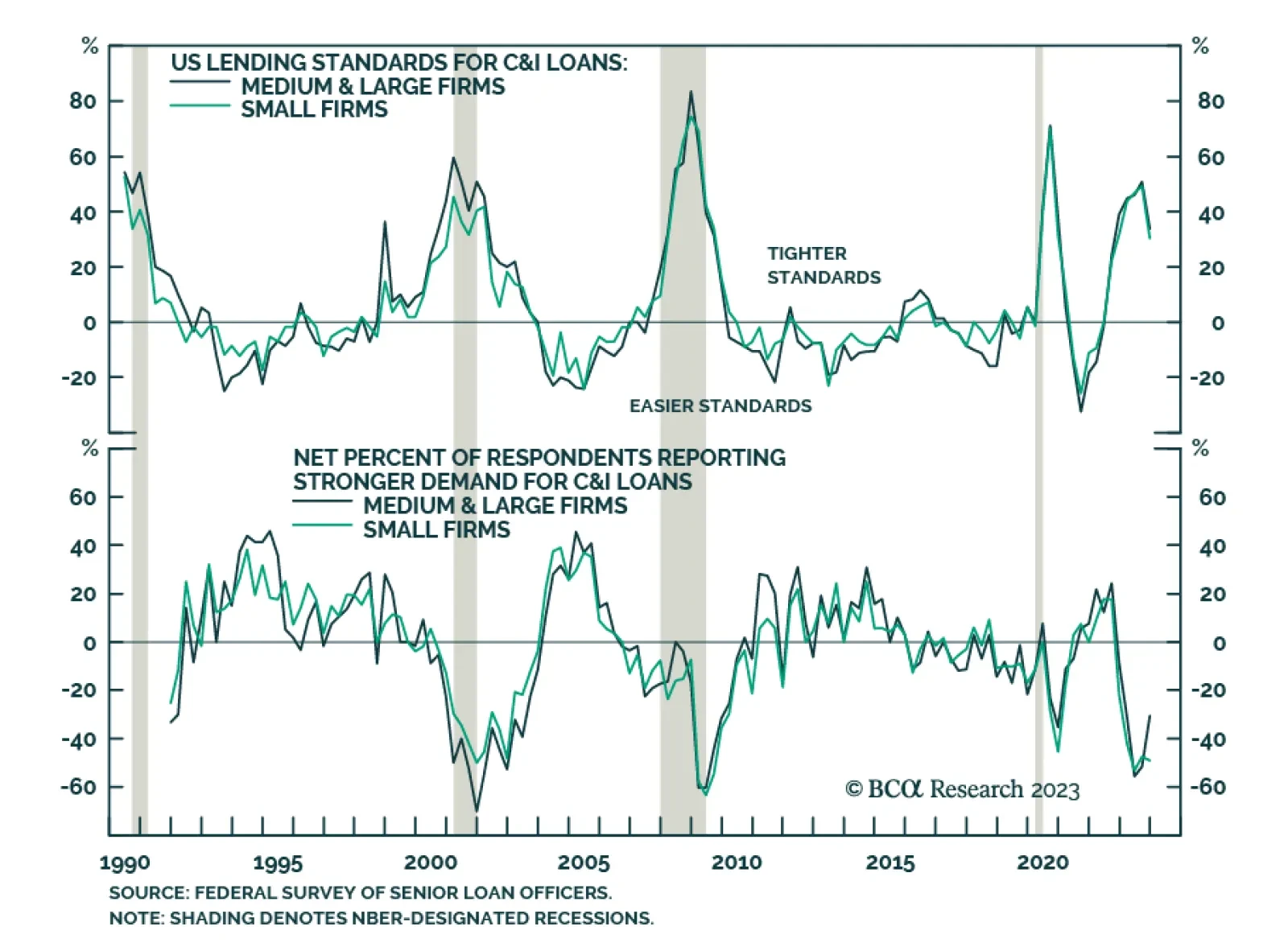

The US Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) reveals that US banks continued to tighten lending standards for commercial and industrial (C&I), commercial real estate (CRE), residential real estate (RRE) except government residential…

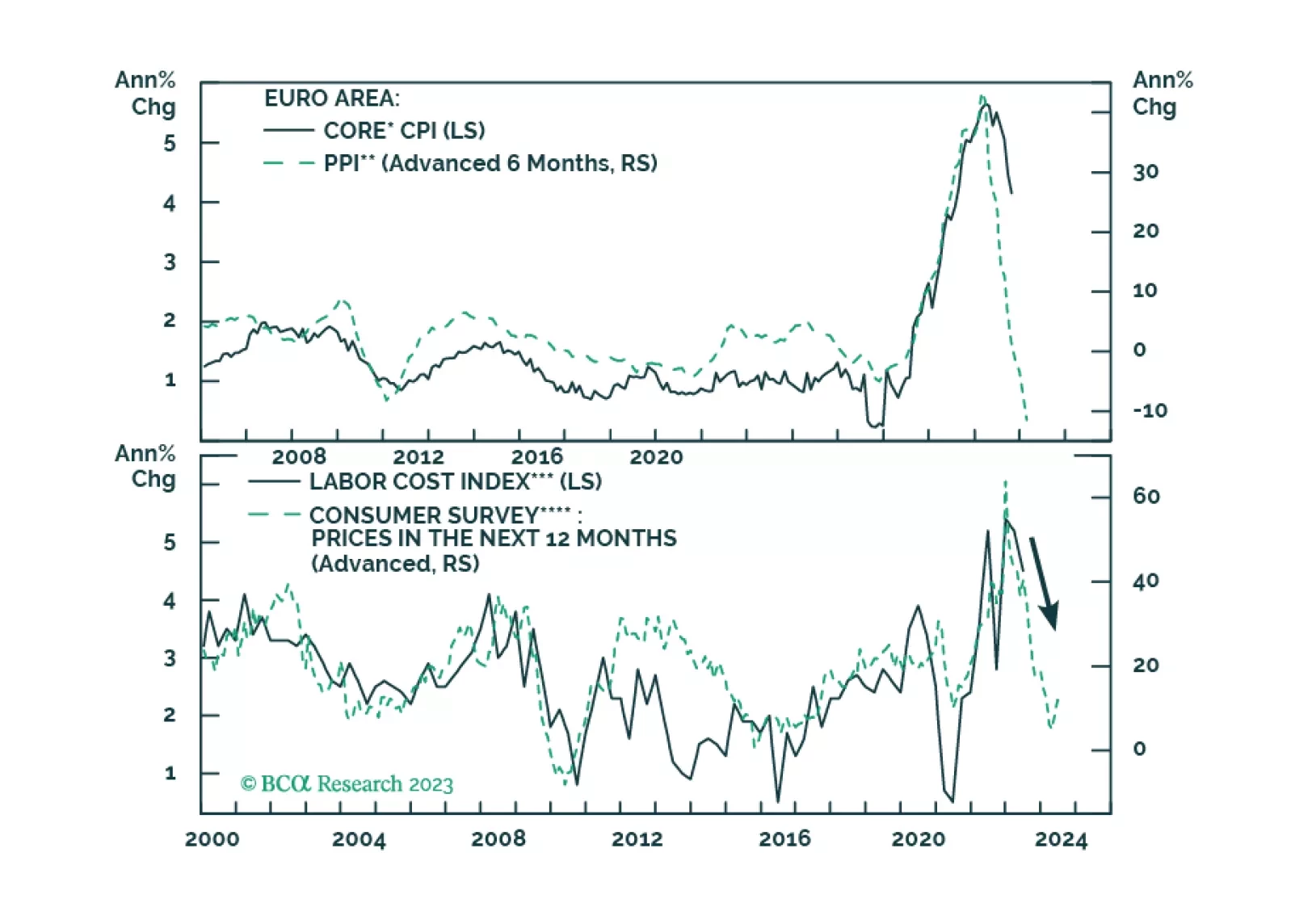

According to BCA Research’s European Investment Strategy service, German yields will fall toward 2% as market-based inflation expectations dip. For now, the deceleration in Eurozone core CPI can be attributed to the effect of the pass-through of energy…

The Eurozone’s inflation will continue to slow over the coming months. While this trend will help Bund prices, will it boost the appeal of European equities?

We consider several uncertainties in this week’s report, from the interest rate outlook to the source of the mountain of cash households have amassed since the pandemic began. We have not adjusted our tactical asset-allocation recommendations but will do so soon to align with the defensive cast of our cyclical recommendations.

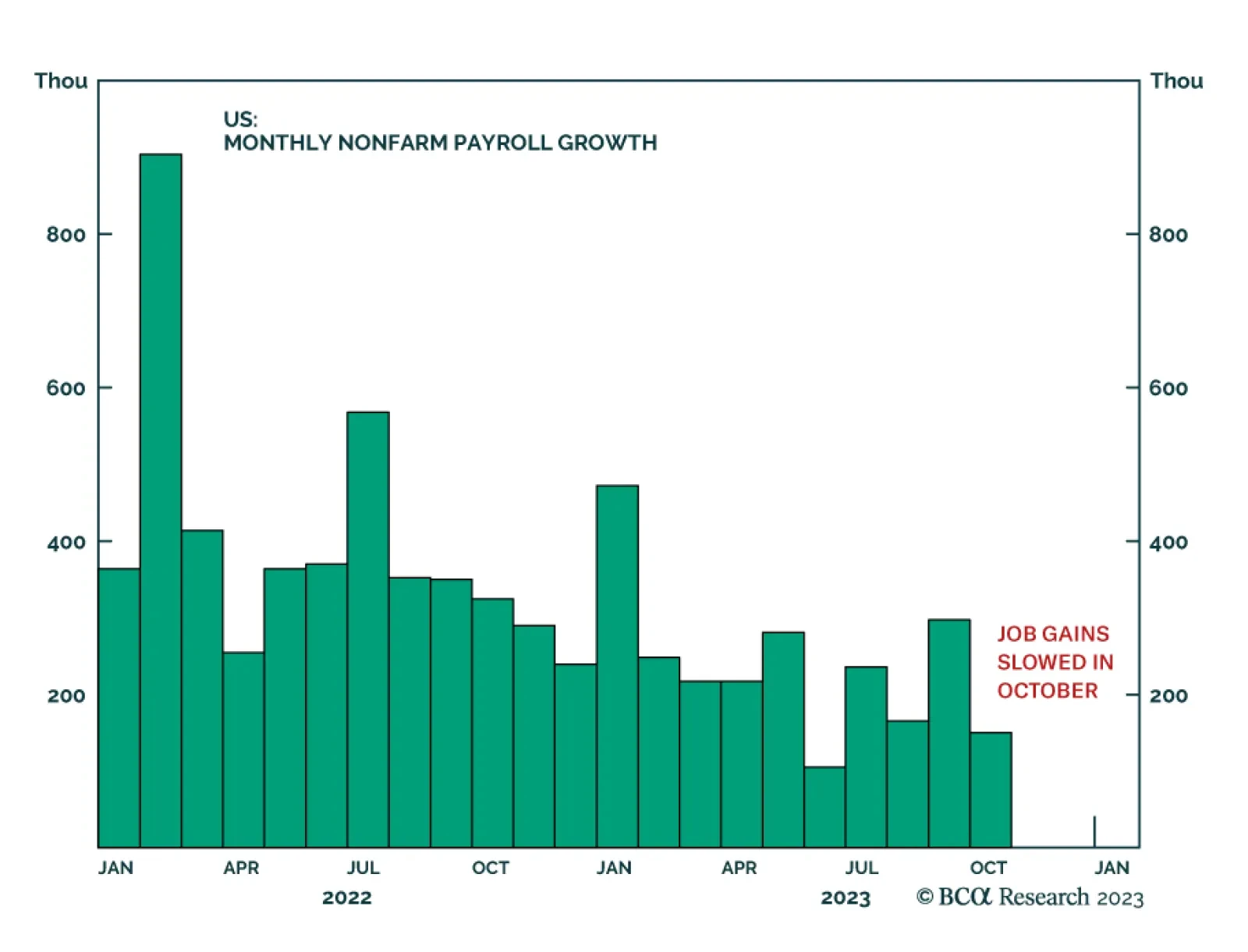

The US Nonfarm Payroll report indicates that labor market conditions cooled in October. The 150 thousand increase in payroll employment fell below expectations of 180 thousand and marks a slowdown from the 297 thousand increase in September. Moreover, the…