Inflation/Deflation

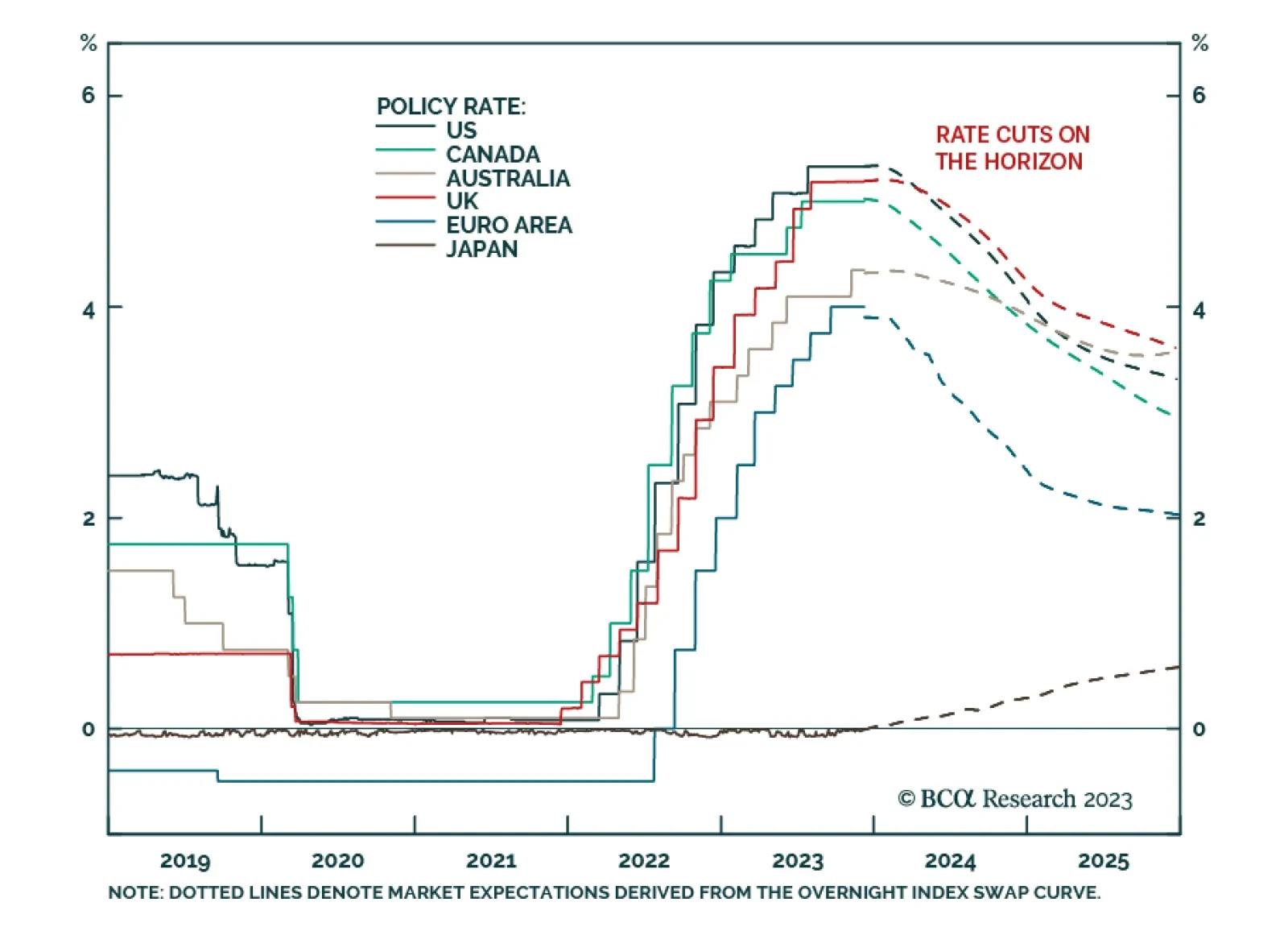

Multiple major DM central banks are scheduled to decide on monetary policy this week. The US Fed will meet on Wednesday, followed by the ECB, BoE, and Norges Bank on Thursday. It comes after the BoC and RBA both opted to keep rates unchanged last week. …

Our US fixed income team’s key investment views for 2024.

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

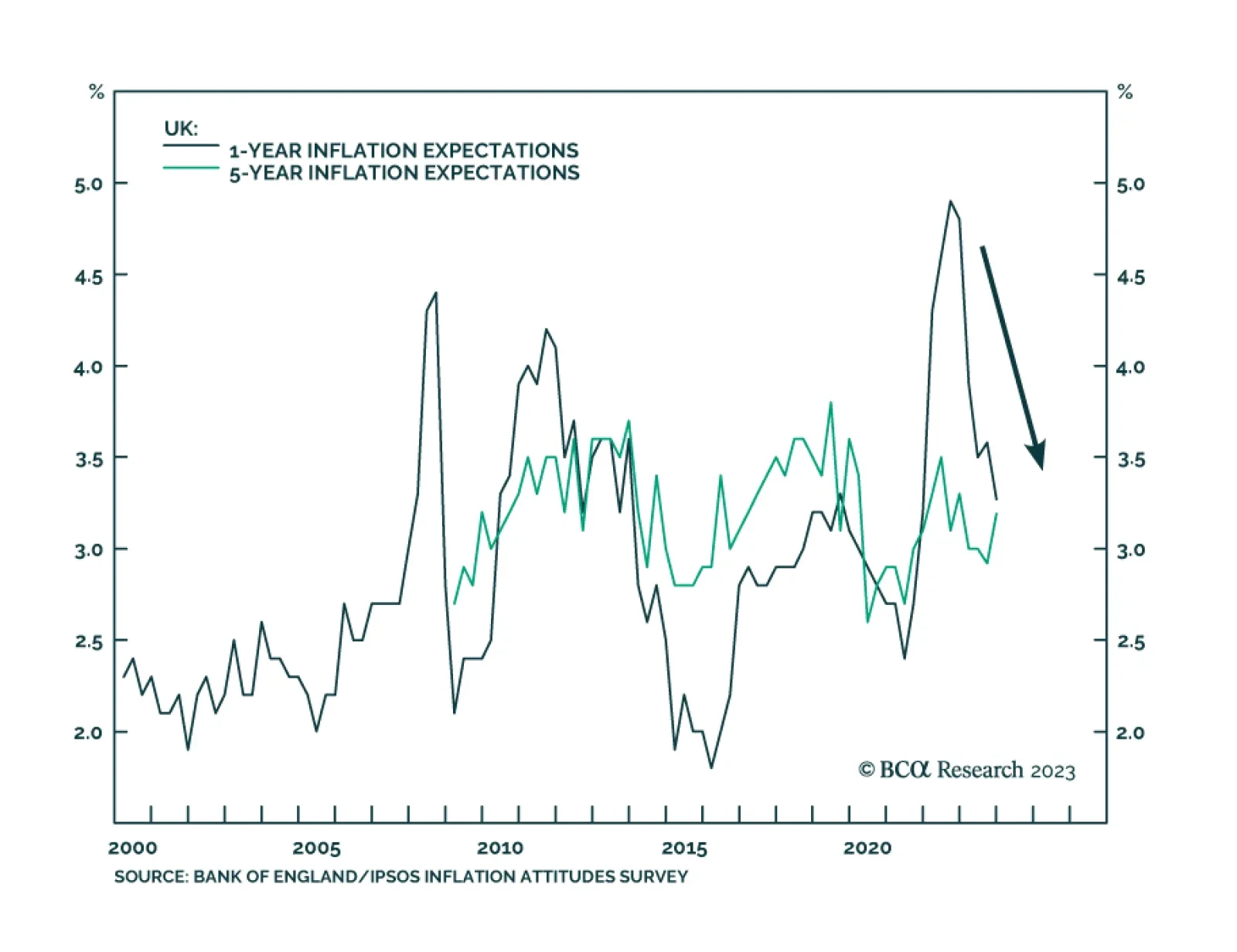

The latest Bank of England/Ipsos quarterly Inflation Attitudes Survey shows the public revised down its near-term inflation outlook. Respondents now believe inflation will fall to 3.3% in the year ahead – down from 3.6% in the August survey and the lowest…

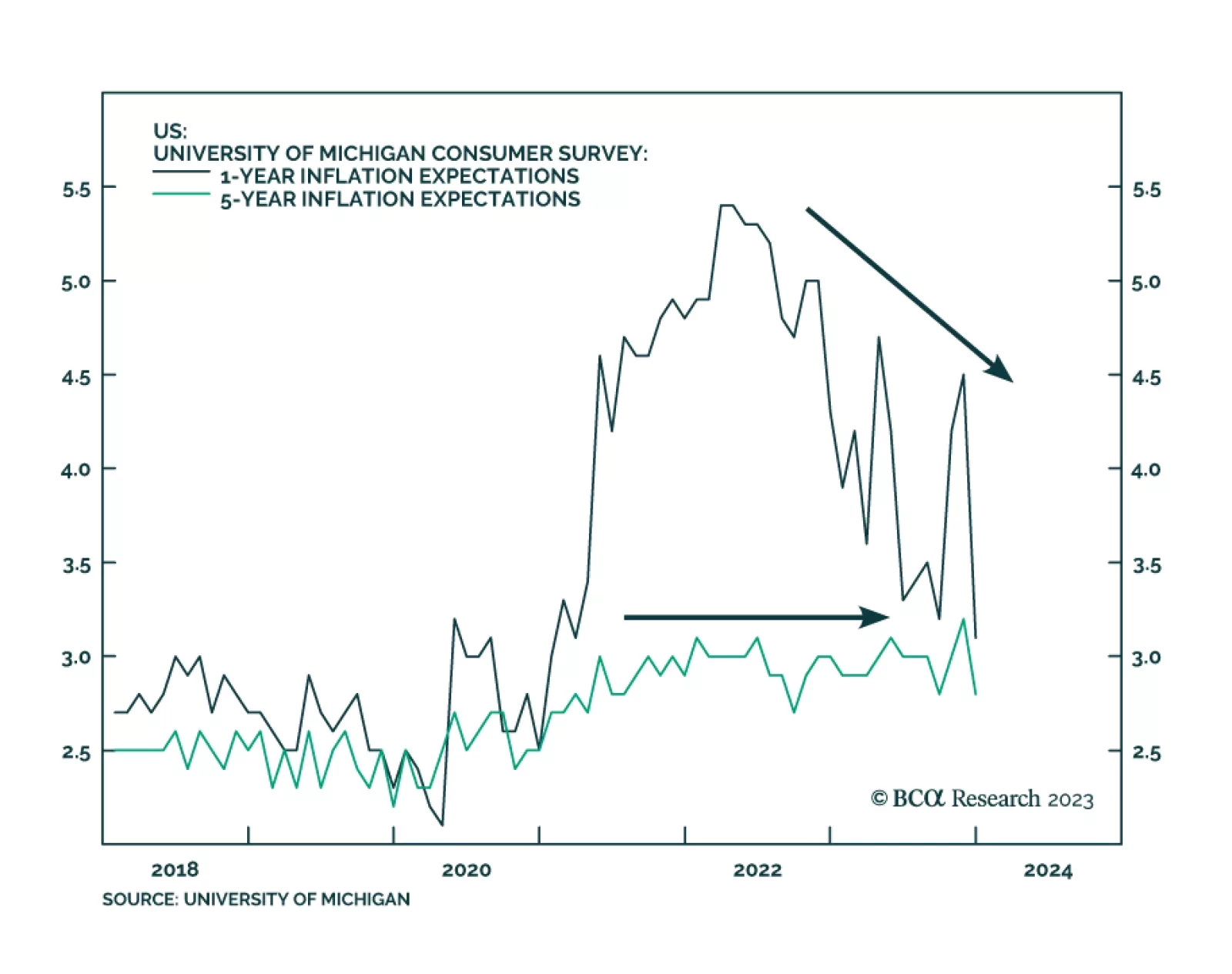

The University of Michigan’s Consumer Survey sent an optimistic signal about the attitude of the US consumer on Friday, handily beating consensus estimates across the board. The preliminary headline index came in at 69.4, up from 62.0 in November, surprising…

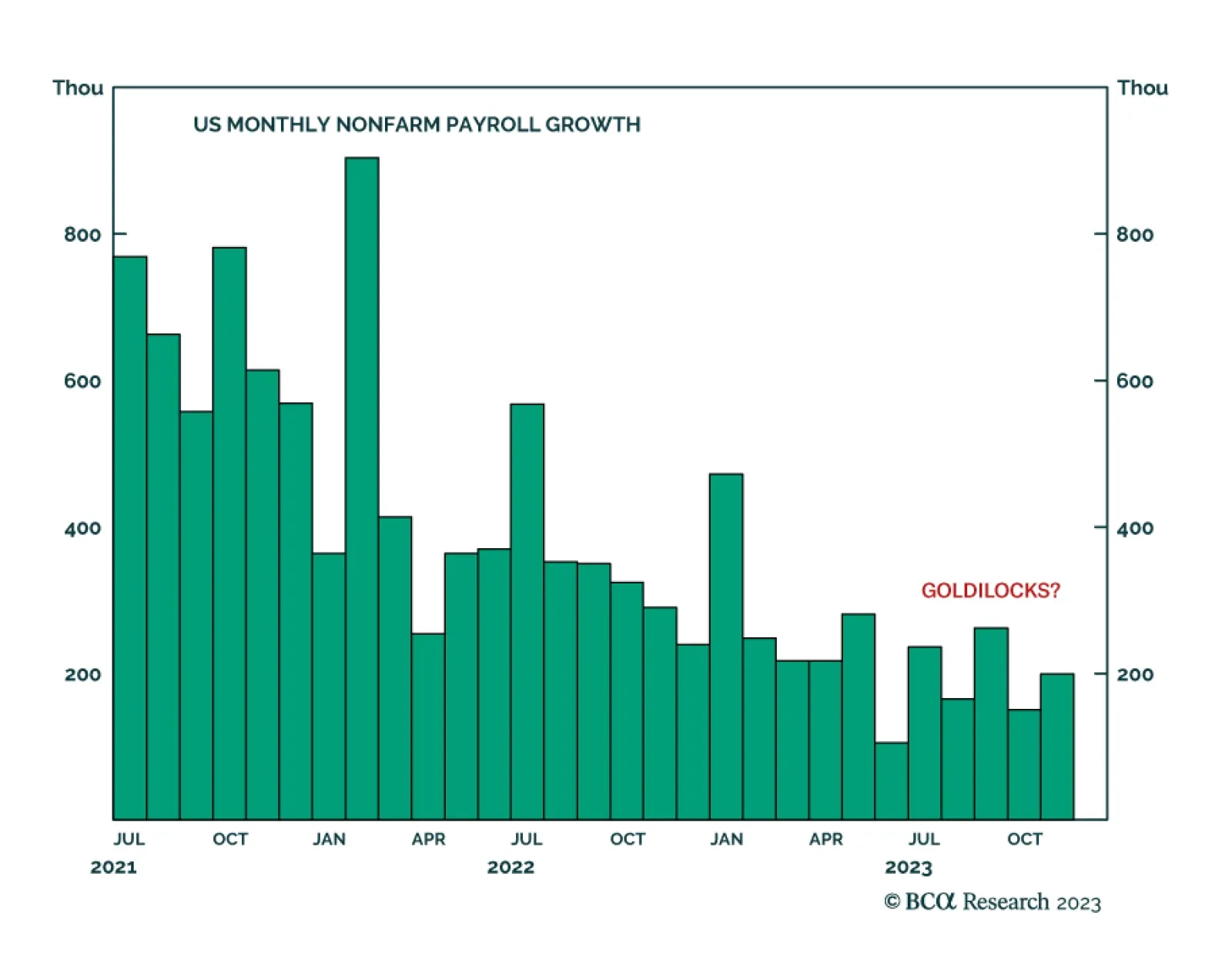

The US employment report delivered a positive surprise on Friday. Nonfarm payroll growth accelerated from 150 thousand to 199 thousand in November, beating expectations of 185 thousand. Importantly, the favorable result was corroborated by the unemployment…

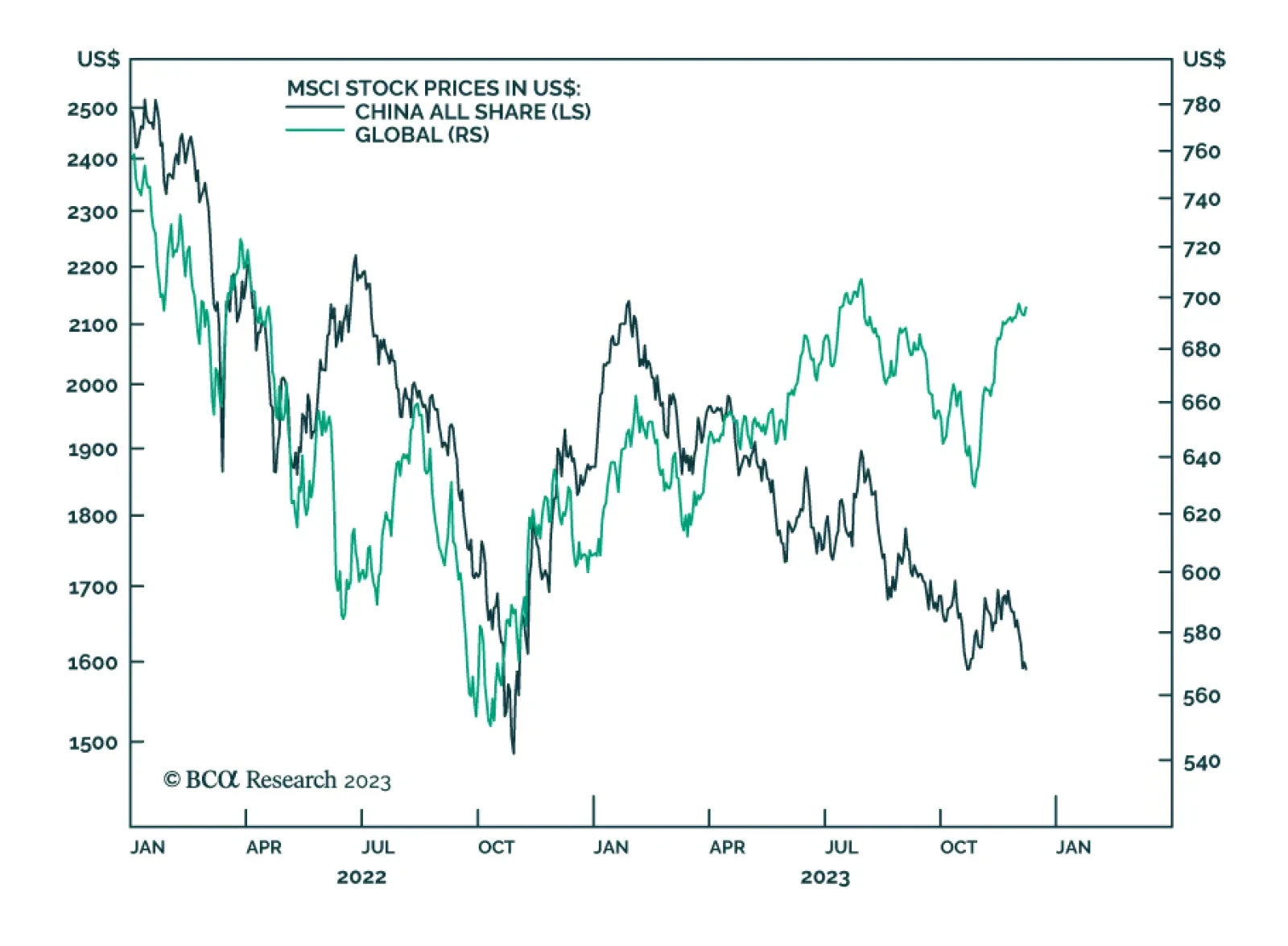

The global investment community has become well aware of many problems facing the Chinese economy including real estate excesses, policymakers’ reluctance to stimulate, as well as elevated debt levels among local governments, enterprises, and consumers. …

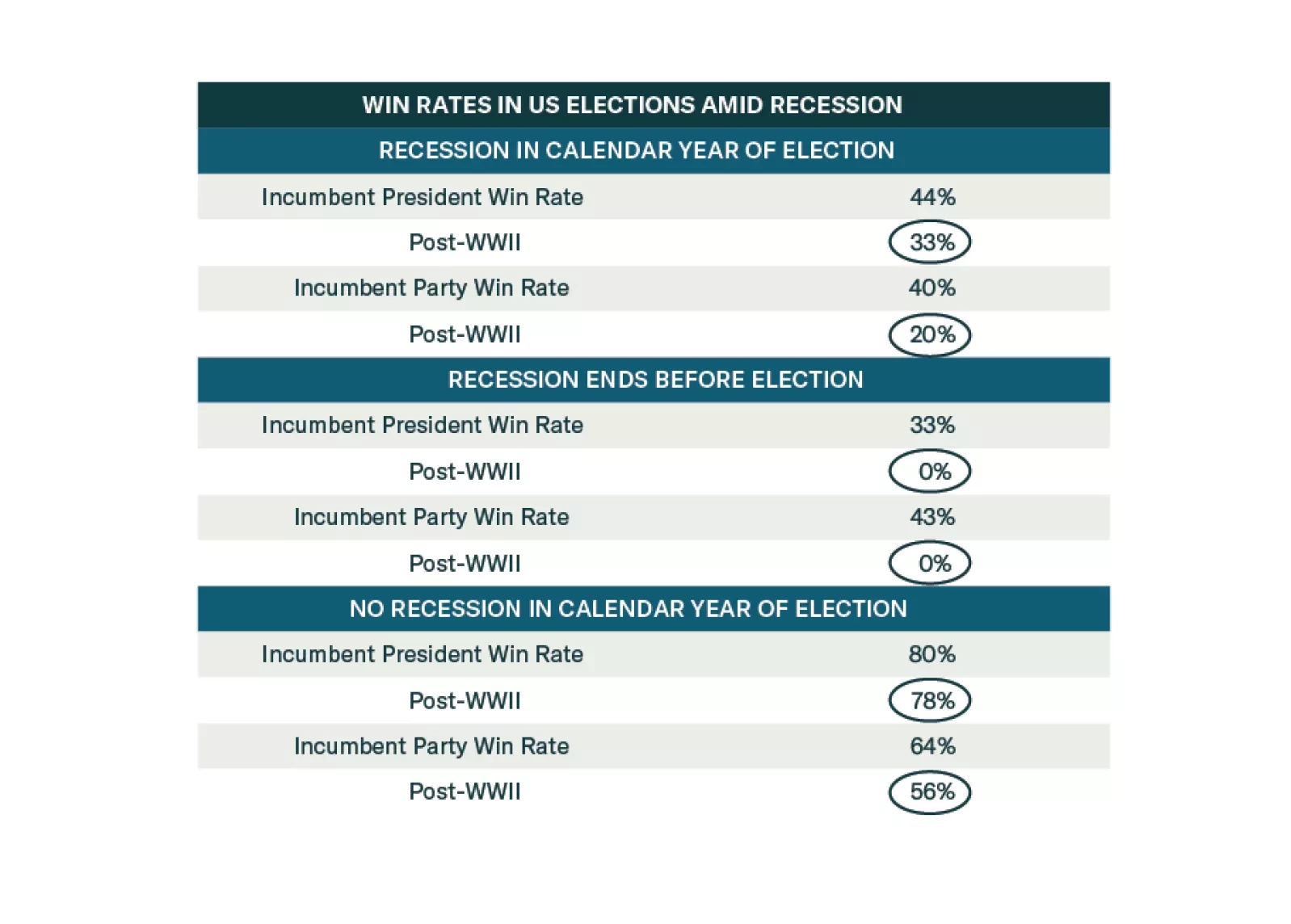

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

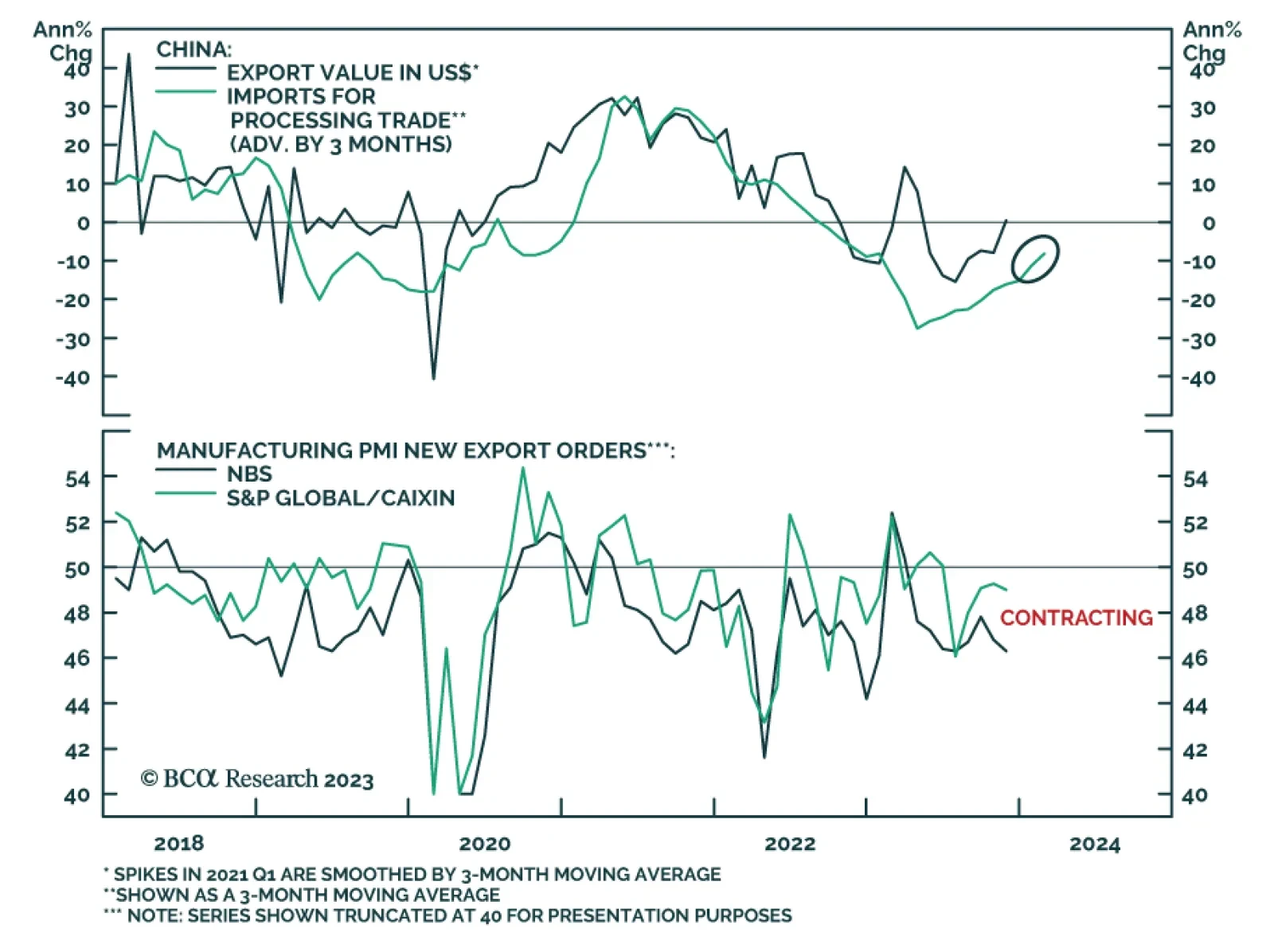

On the surface, Chinese export data delivered a positive surprise on Thursday, painting a favorable picture of the global manufacturing cycle. Exports unexpectedly grew on a year-over-year basis in November for the first time since April. The 0.5% y/y…

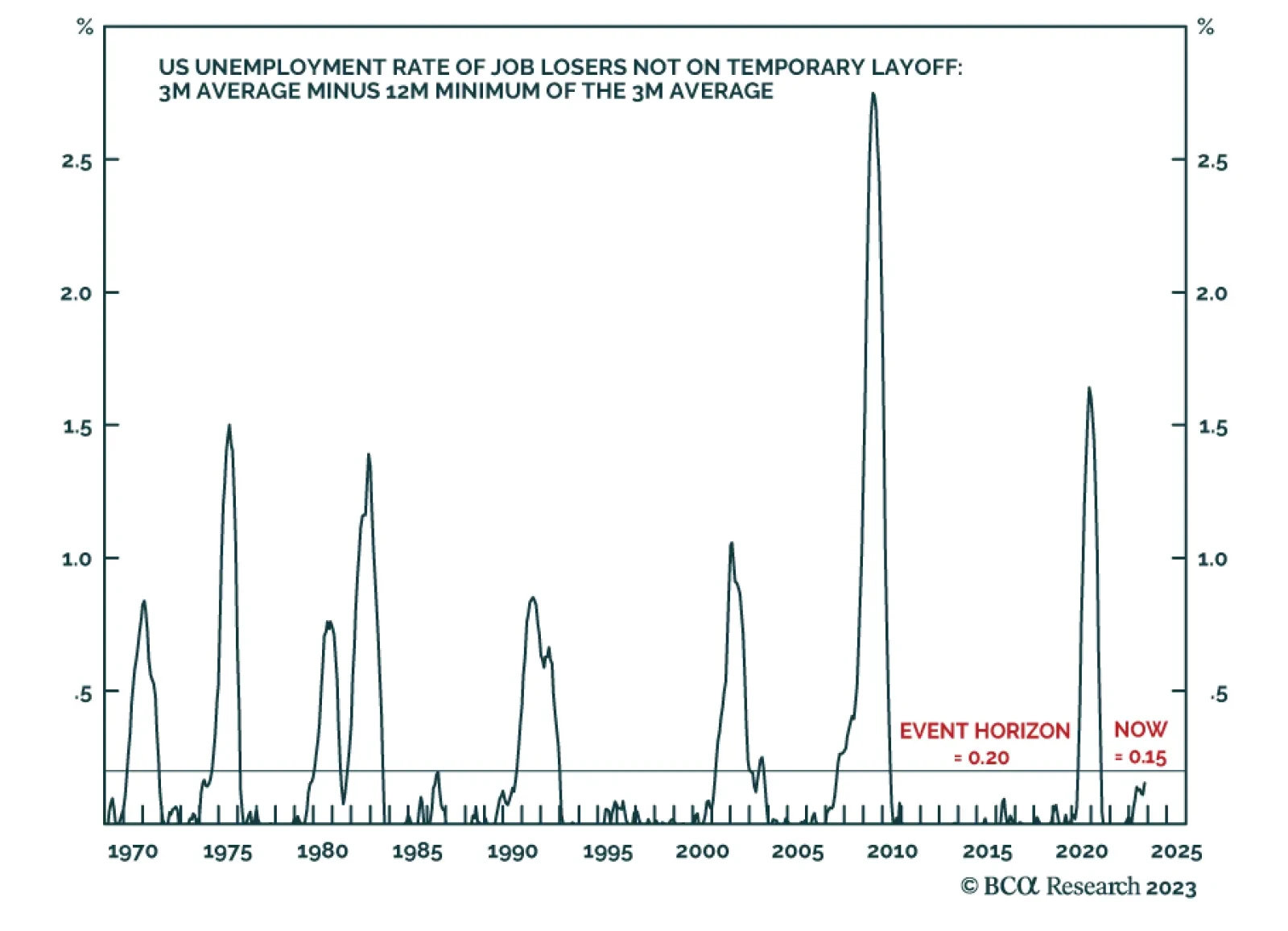

The ‘Joshi rule’ real-time recession indicator signals the start of a US recession when the three-month moving average of the unemployment rate of ‘job losers not on temporary layoff’ rises by 0.20 percent from its low during the previous 12 months. The…