Inflation/Deflation

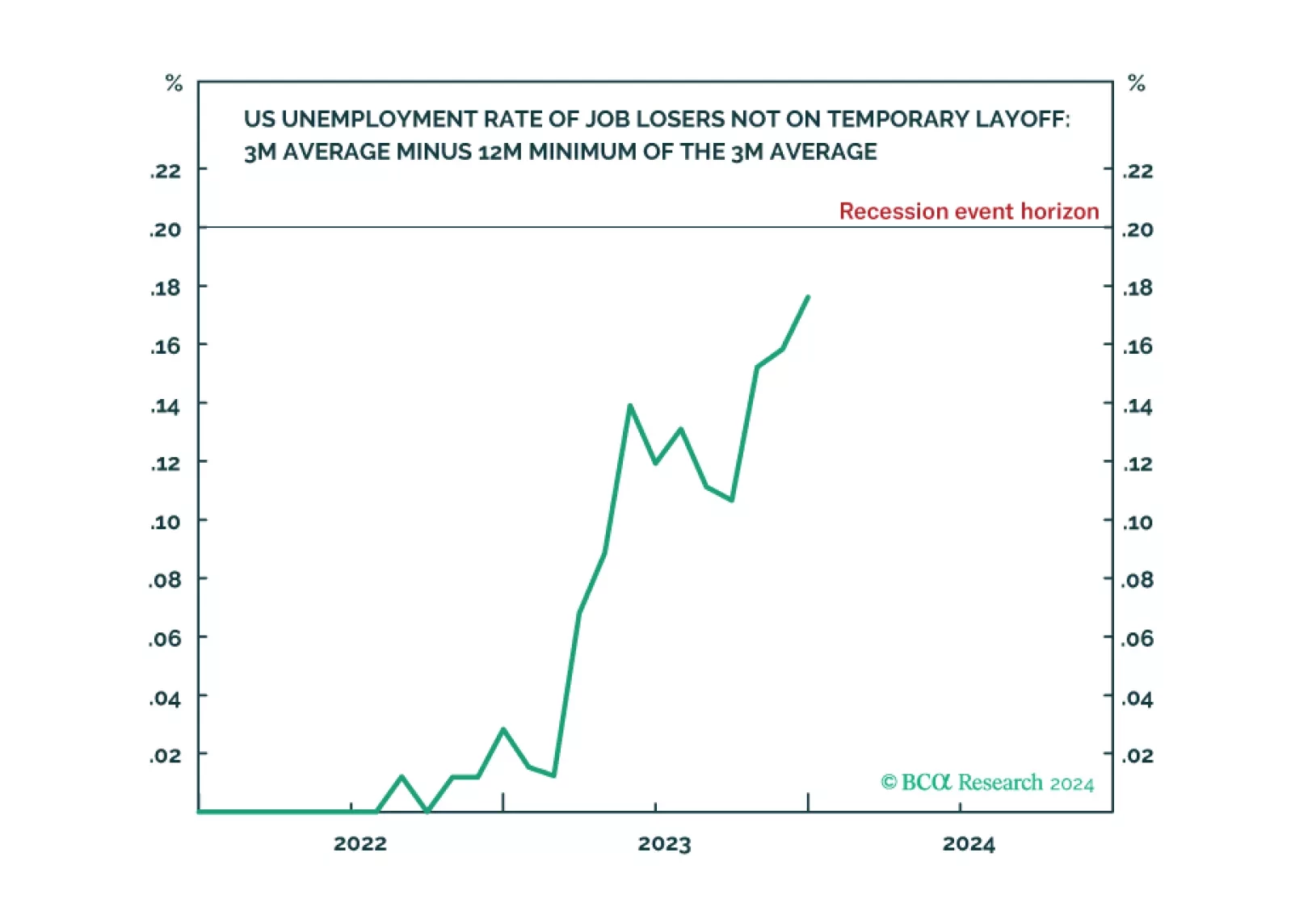

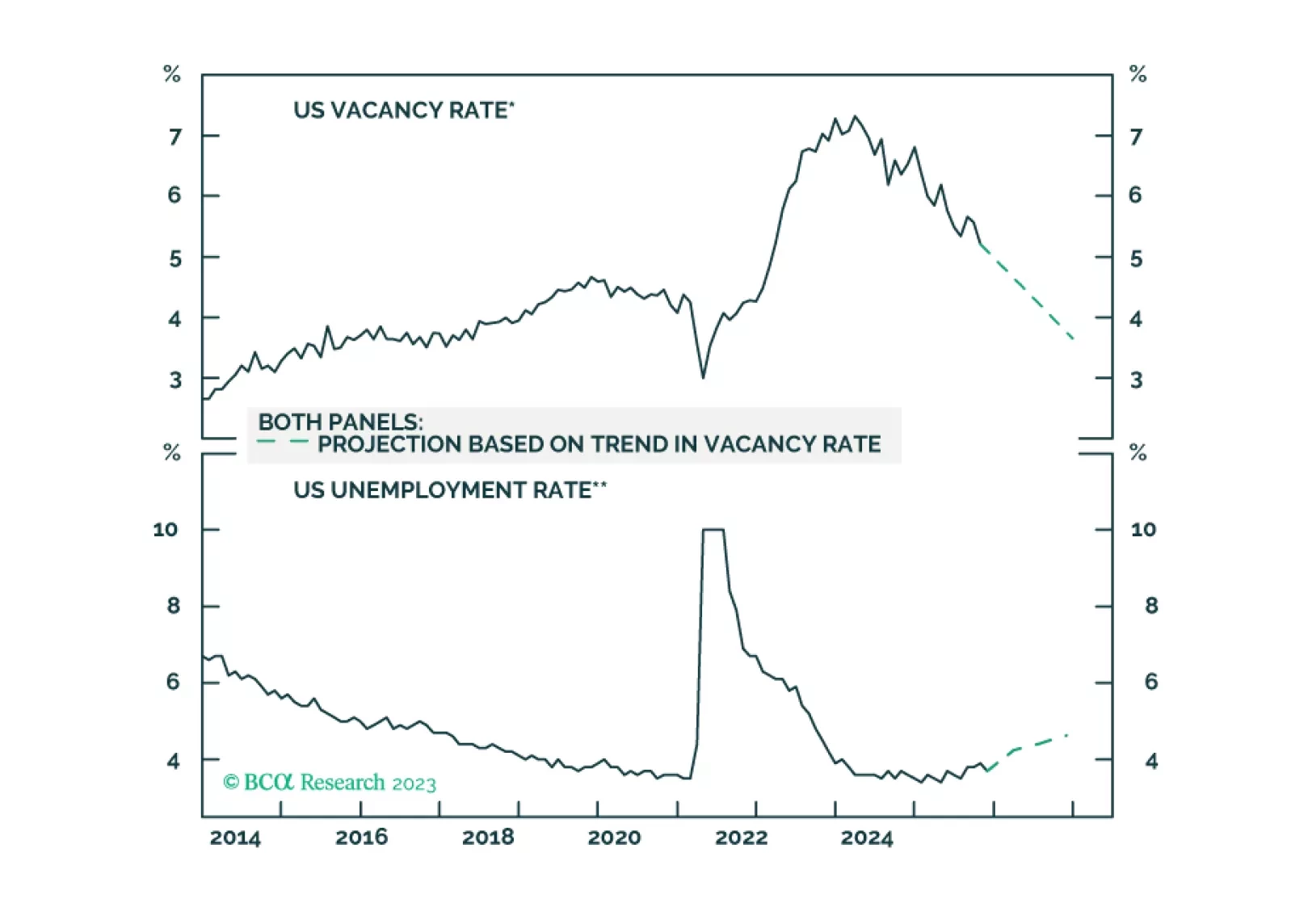

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.

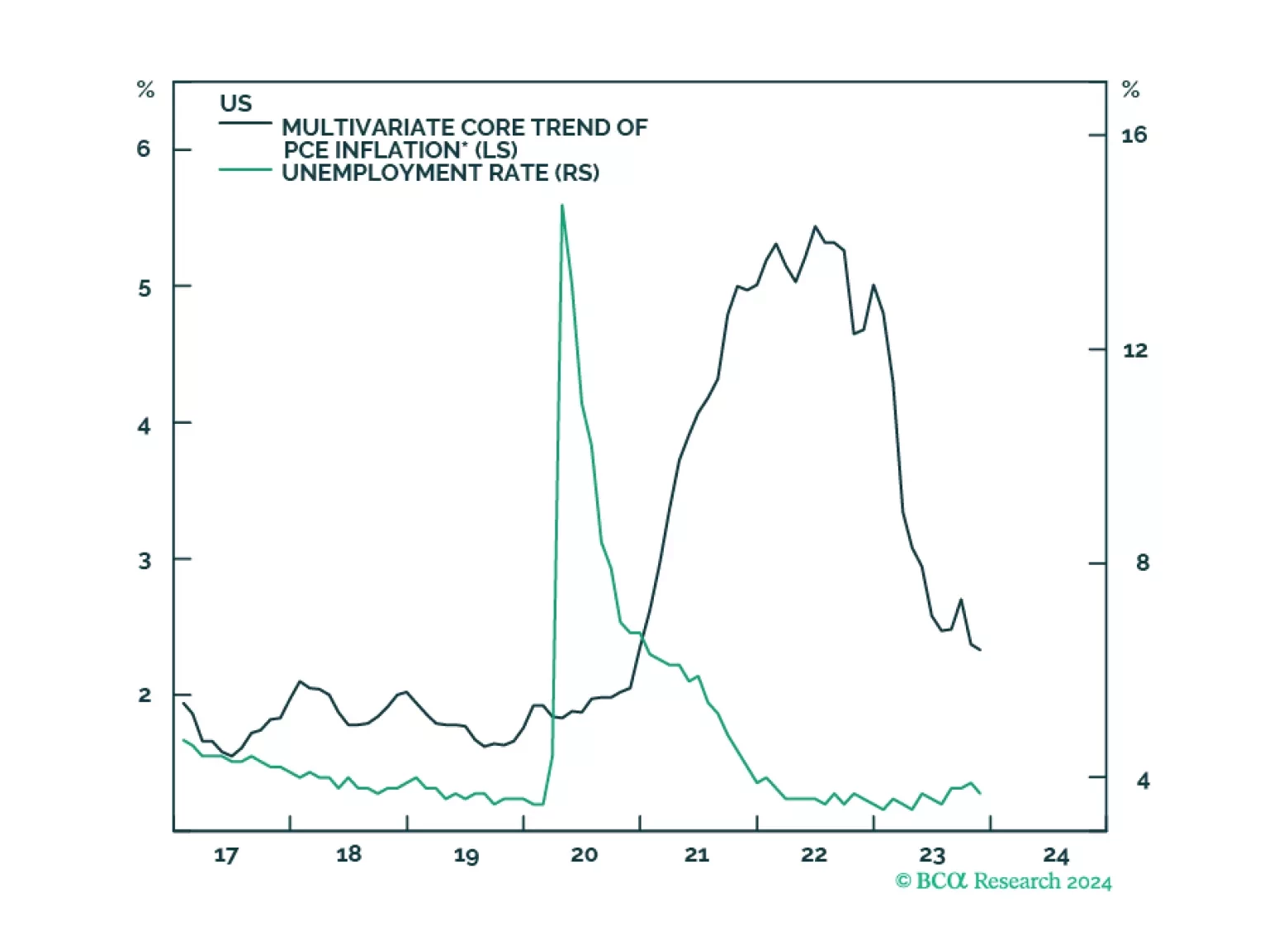

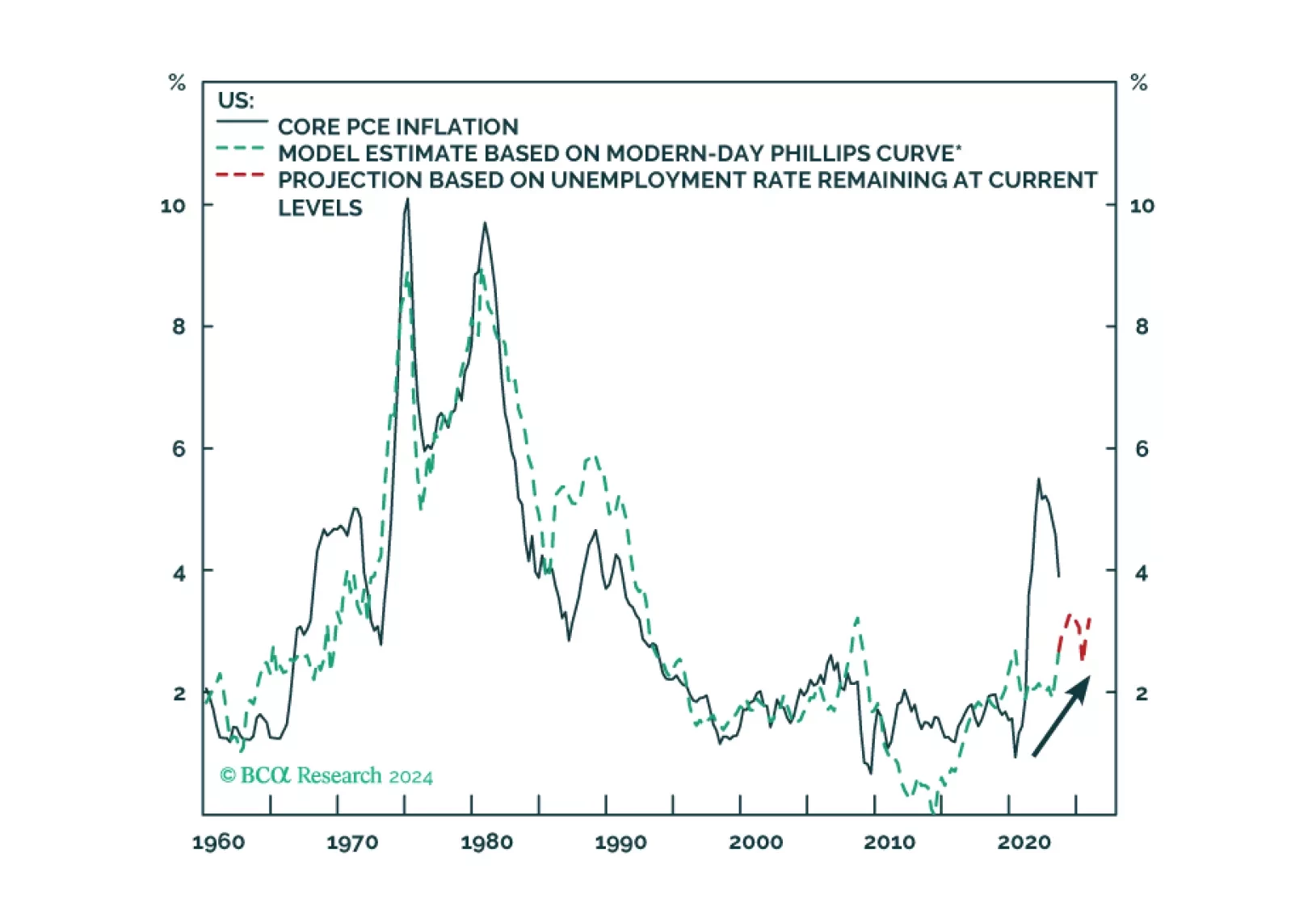

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

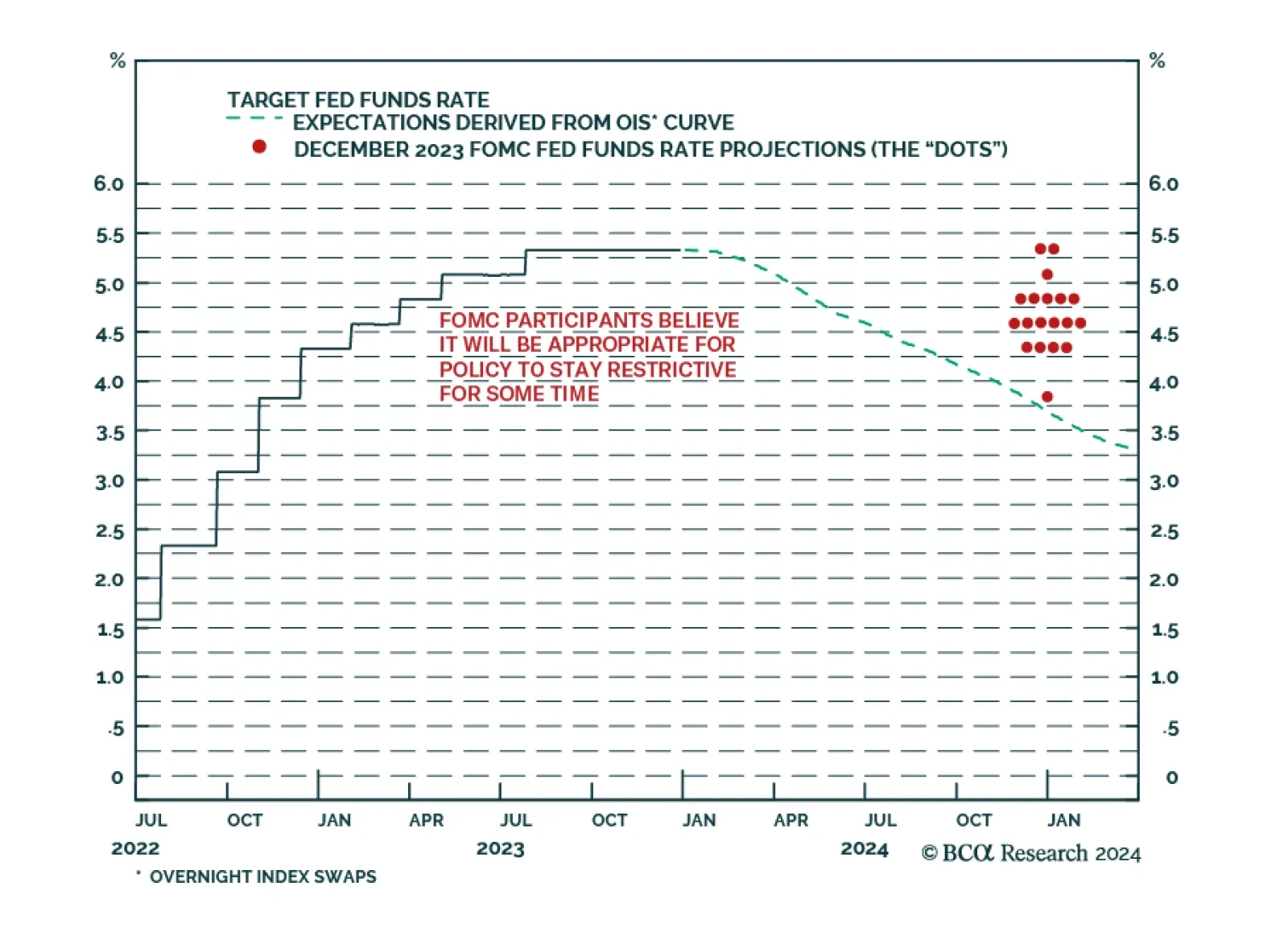

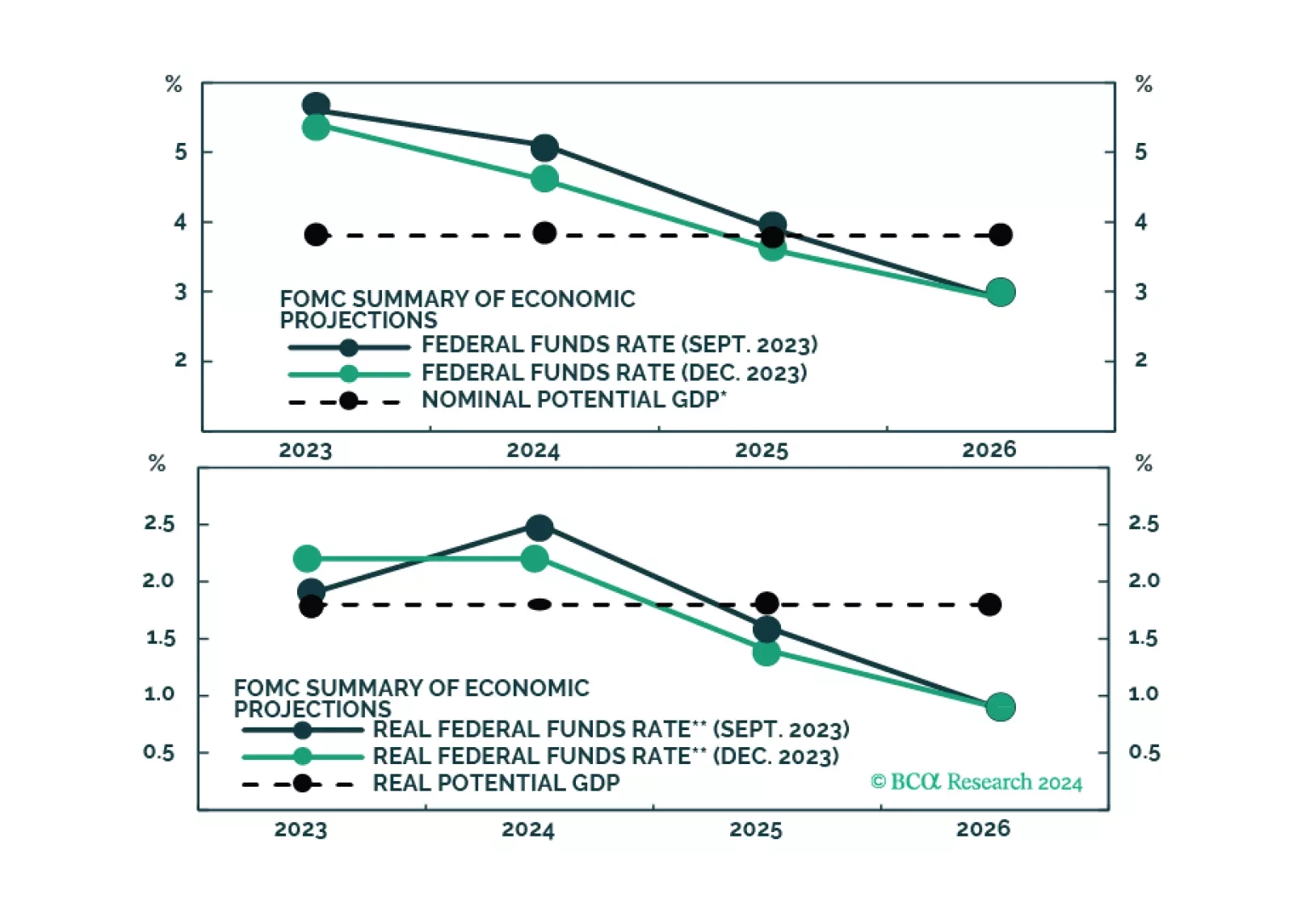

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.

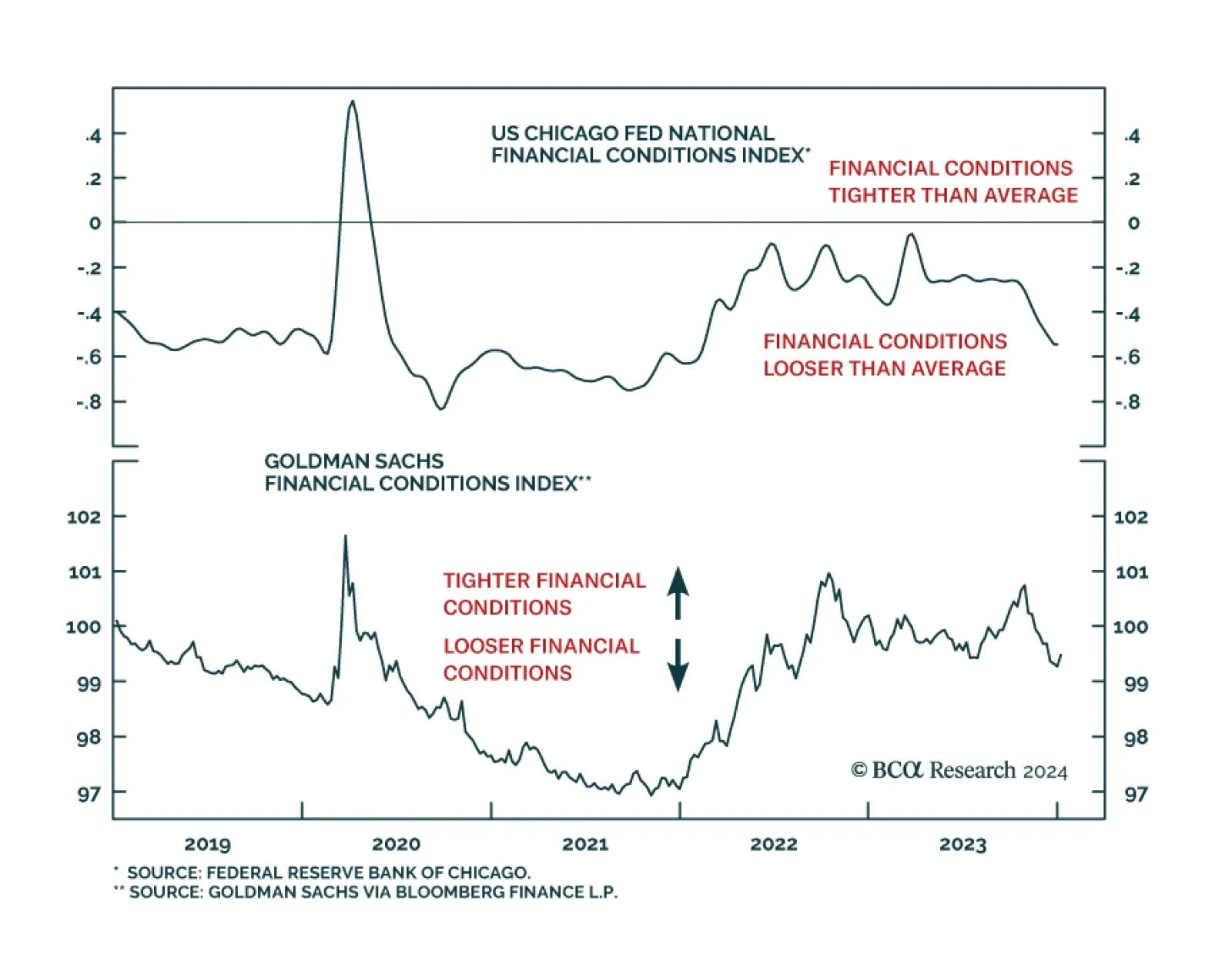

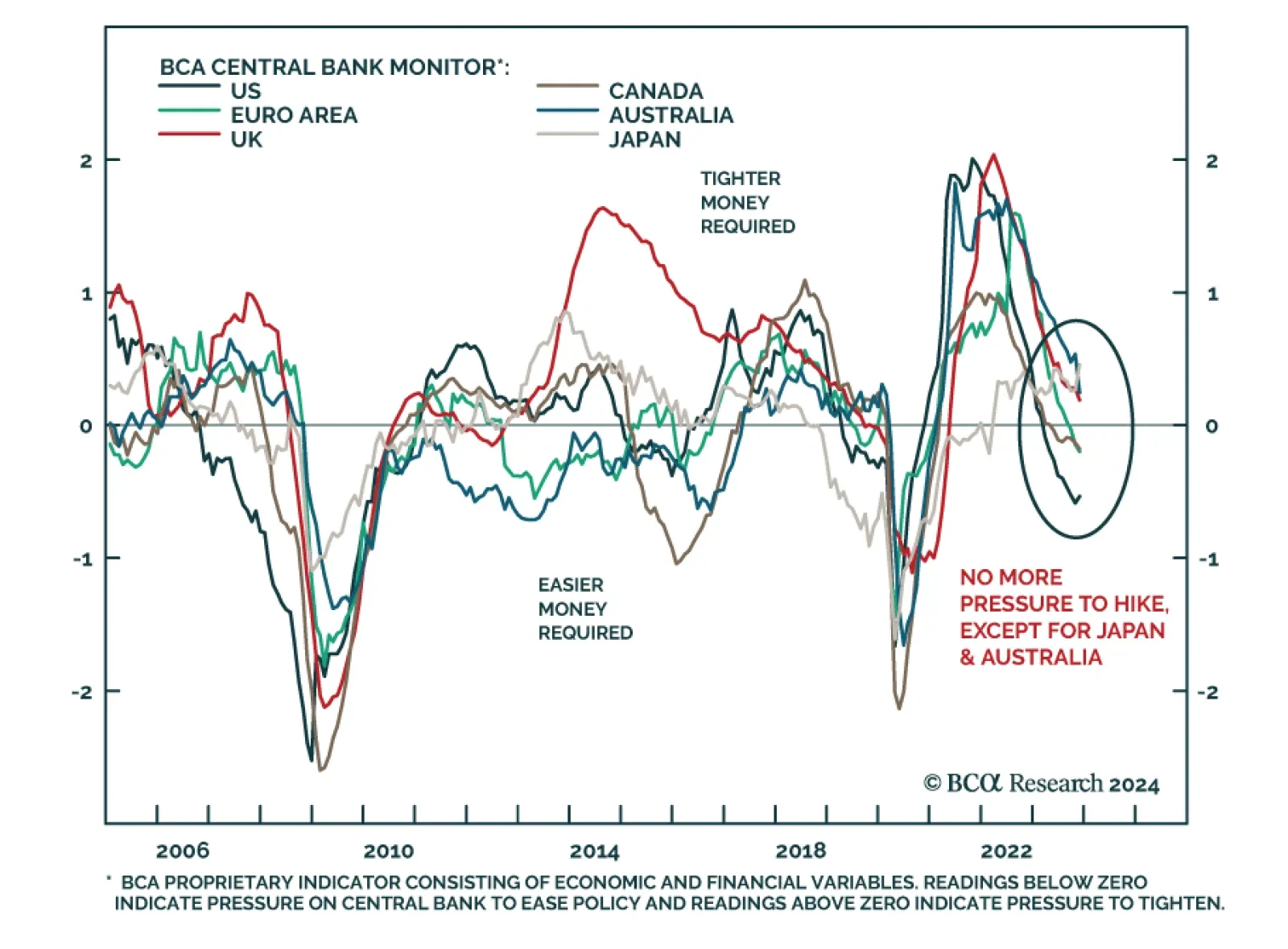

In Section I, we discuss the implications and potential risks of the Fed’s recent pivot. The near-term implications of the Fed's dovish pivot are likely to continue to be bullish for risky asset prices, and a new high in global stock prices cannot be ruled out. The Fed has not effectively countered market expectations that monetary policy will cease to be tight in a year’s time, which has eased financial conditions and will work counter to the Fed’s economic forecasts. However, we would expect this, at most, to delay rather than to prevent a recession. Developed economies remain on a recessionary path so long as monetary policy in the US and euro area remains actually tight. As such, we do not see the December meeting as a truly bullish catalyst for risky assets on a 12-month time horizon. In Section II, my colleague Ryan Swift of BCA’s US Bond Strategy service reviews the outlook for the Fed’s interest rate and balance sheet policies for next year.

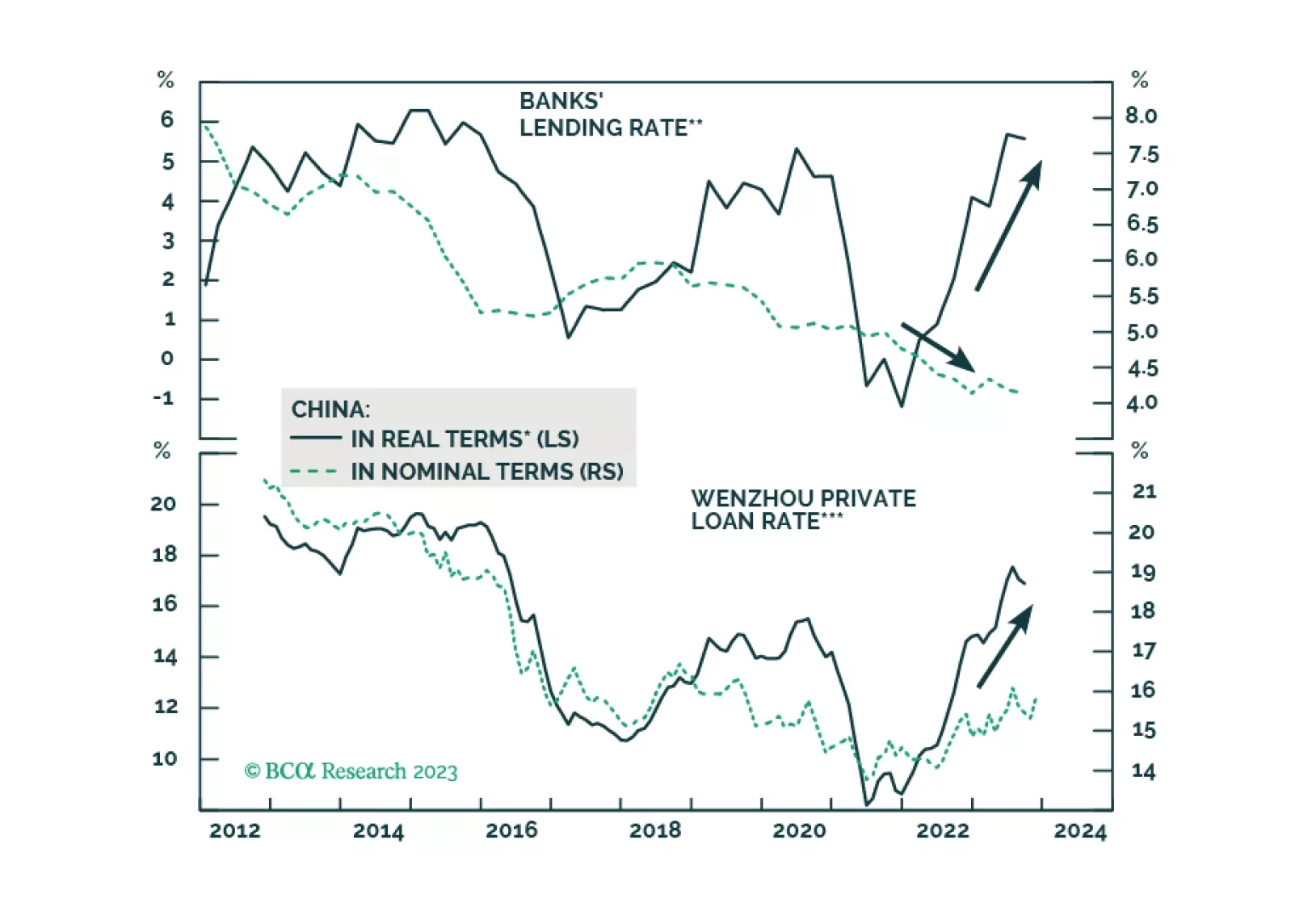

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.