Inflation/Deflation

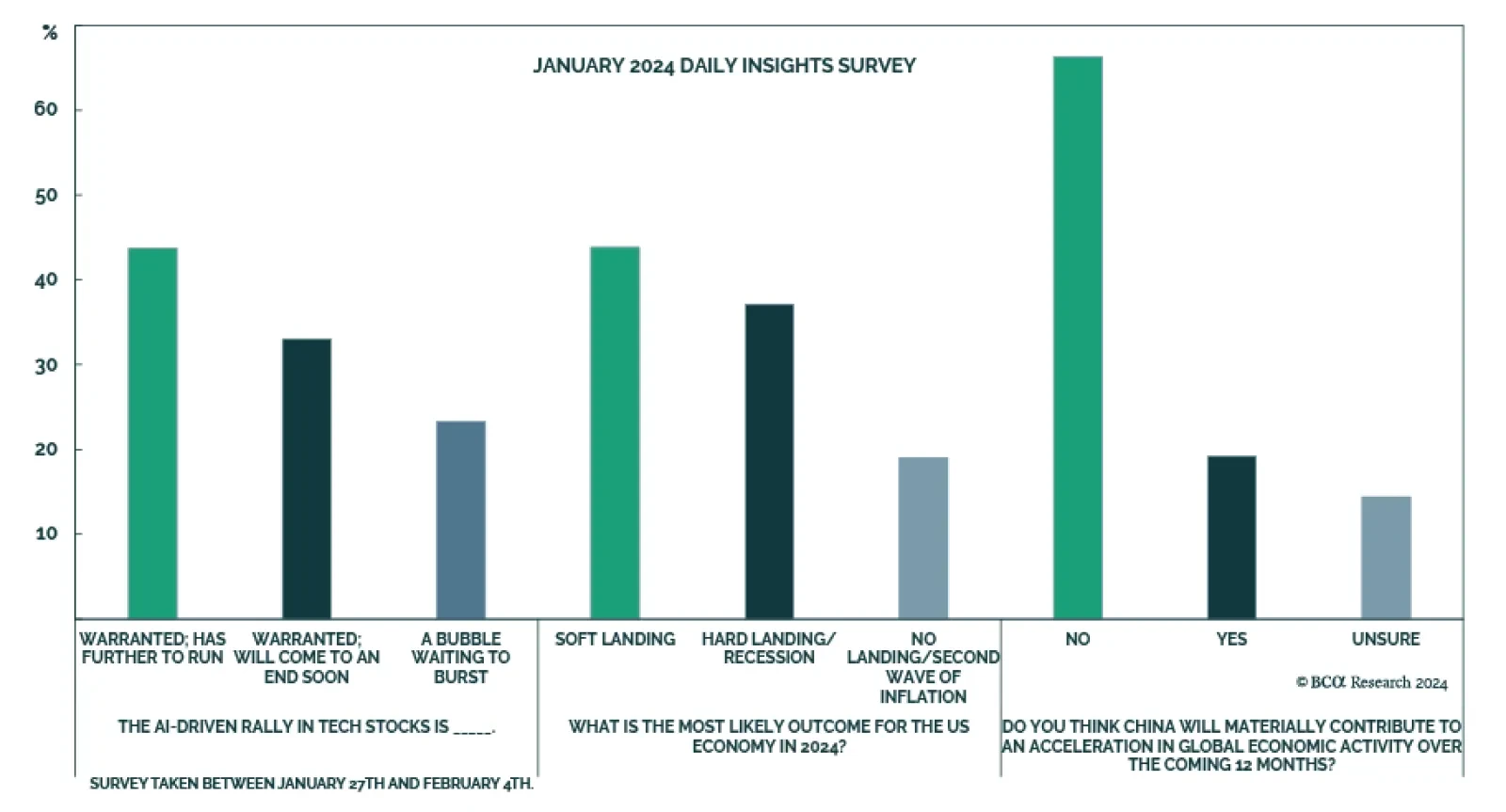

In the monthly Daily Insights Survey we conducted over the past week, we asked about our readers’ views on tech stocks, the US economy in 2024, and China’s contribution to global growth. Regarding tech stocks, 44% of respondents believe the rally as…

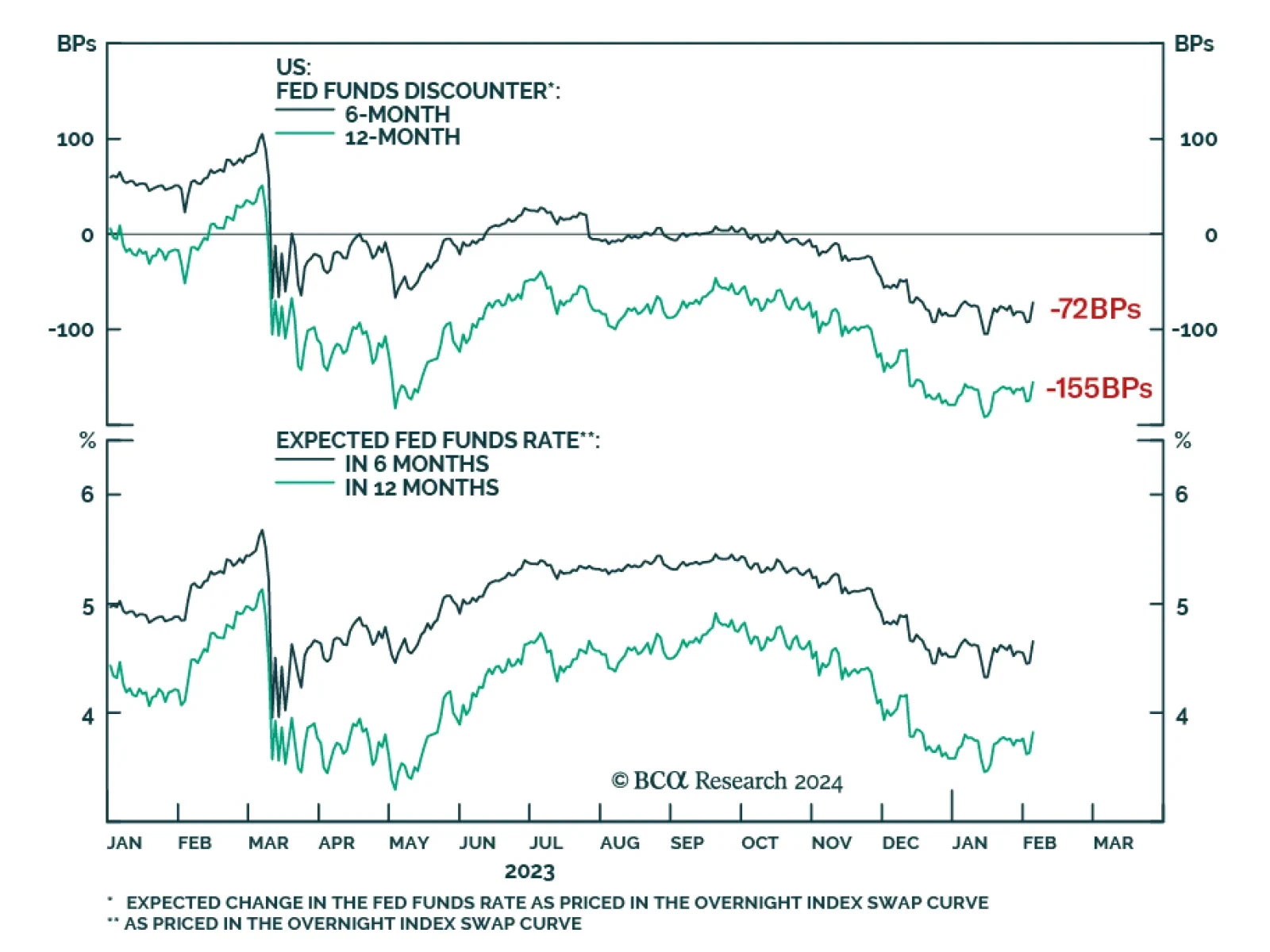

Treasury yields continued to push higher on Monday, bringing the total increase over the past two trading days to 29bps. The move comes on the back of strong economic data releases indicating that conditions in the US are resilient. Notably, Friday’s…

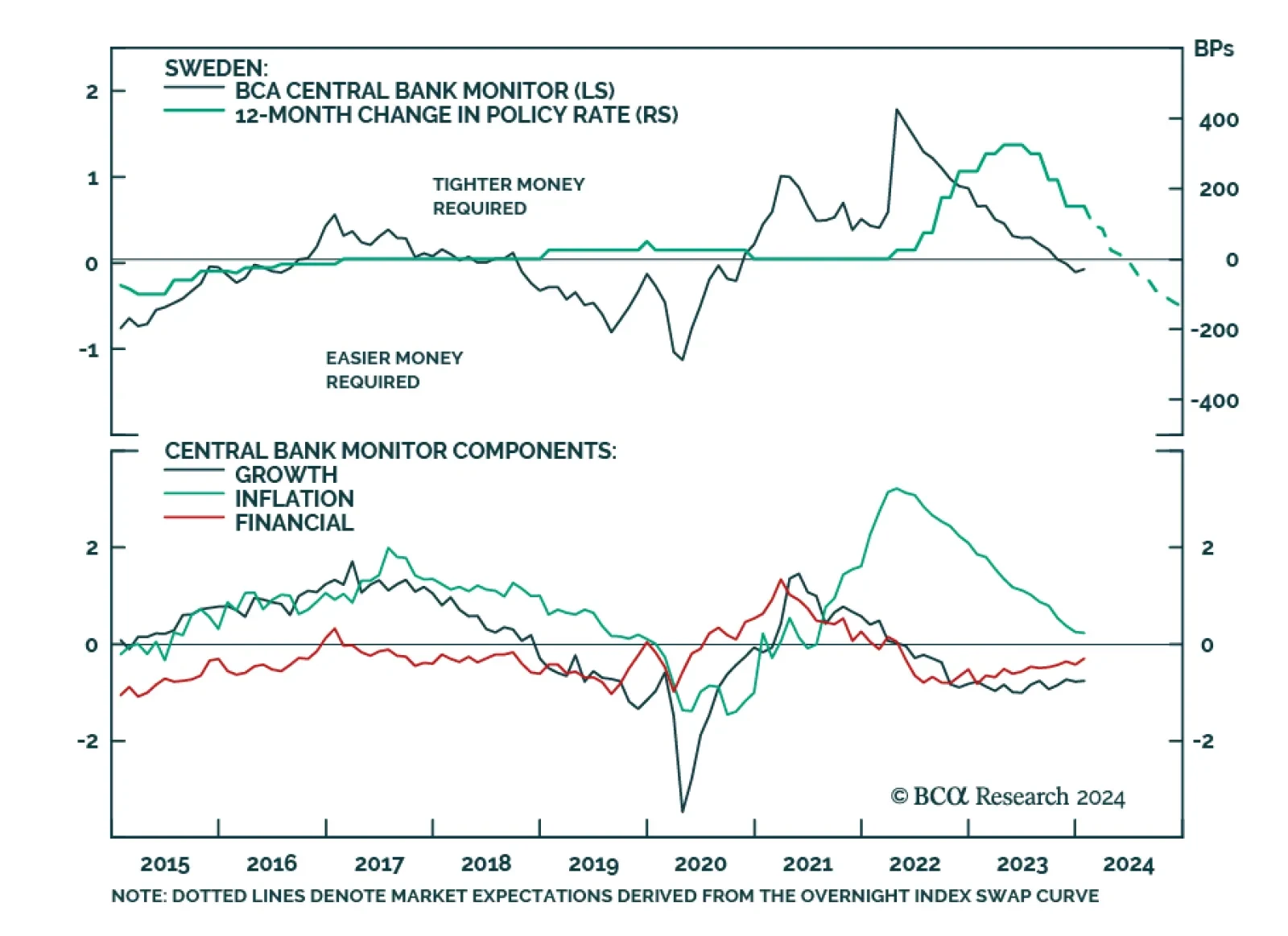

BCA Research’s European Investment Strategy service upgrades Swedish government bonds to neutral from underweight within European fixed-income portfolios. The Riksbank kept its policy rate steady at 4% last week. Governor Erik Thedéen and the Riksbank…

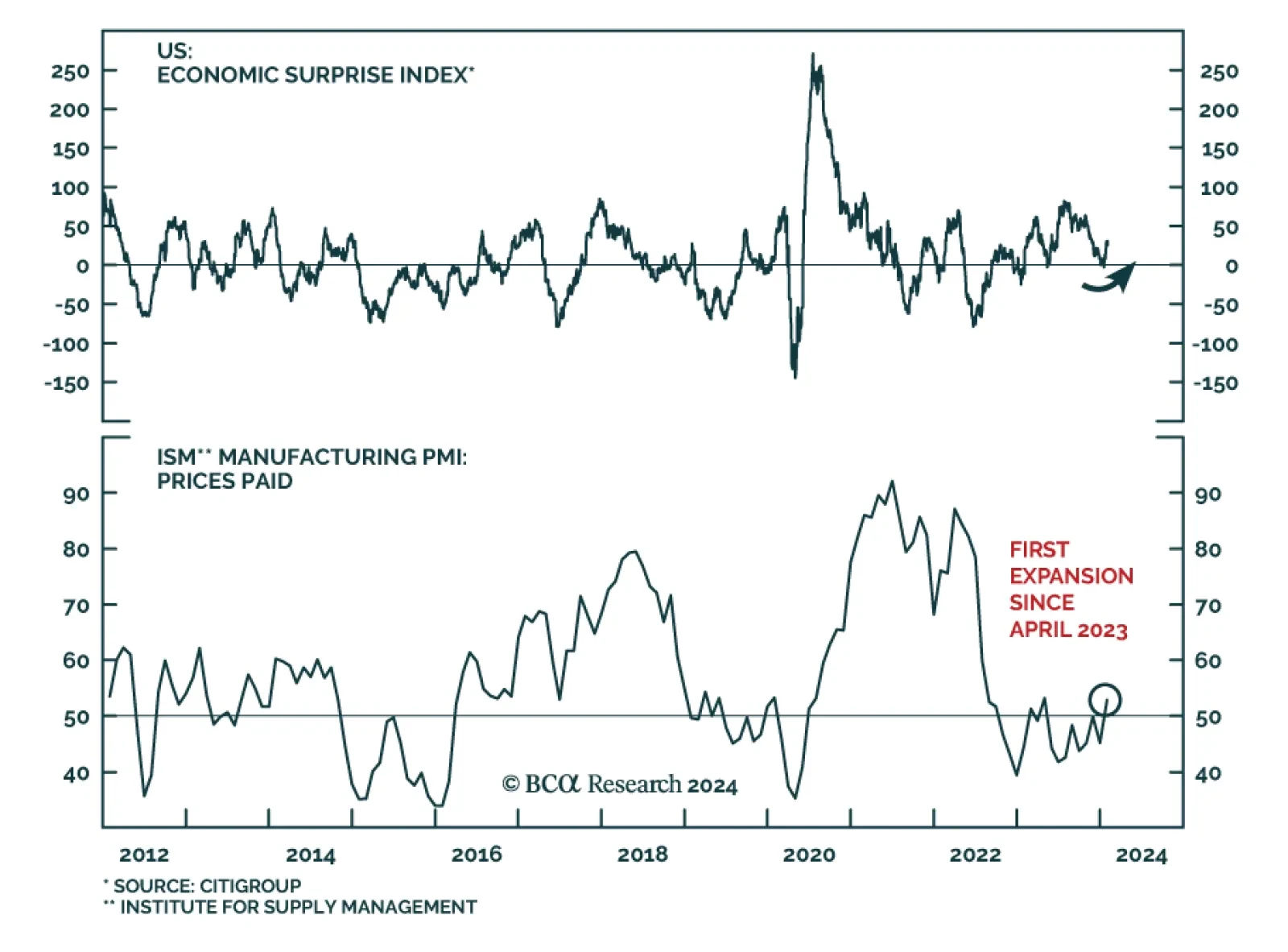

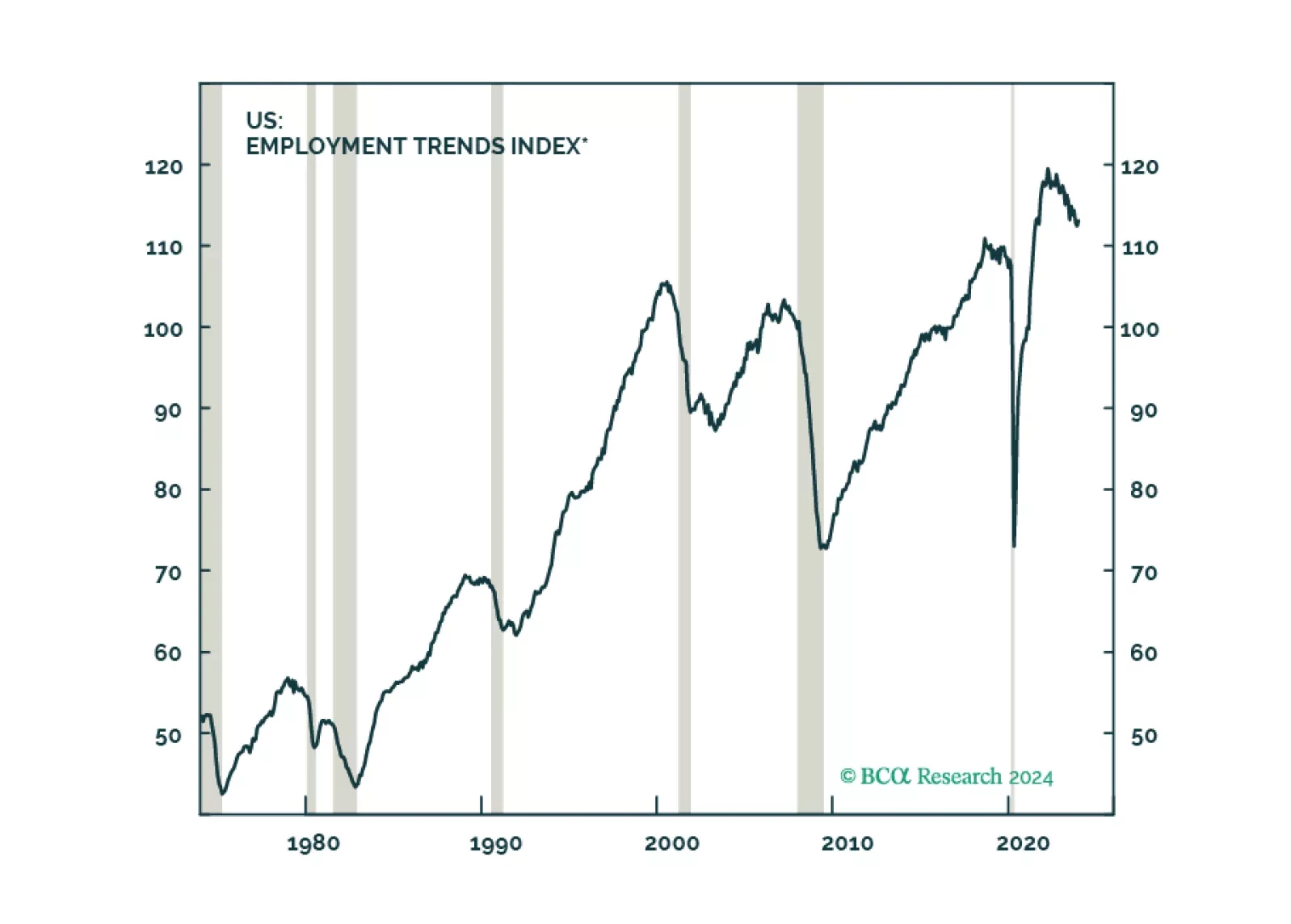

After falling throughout most of the second half of 2023, the US economic surprise index has surged over the past few weeks, indicating that economic conditions are firm at the start of the year. Indeed, Manufacturing PMIs delivered a positive signal last…

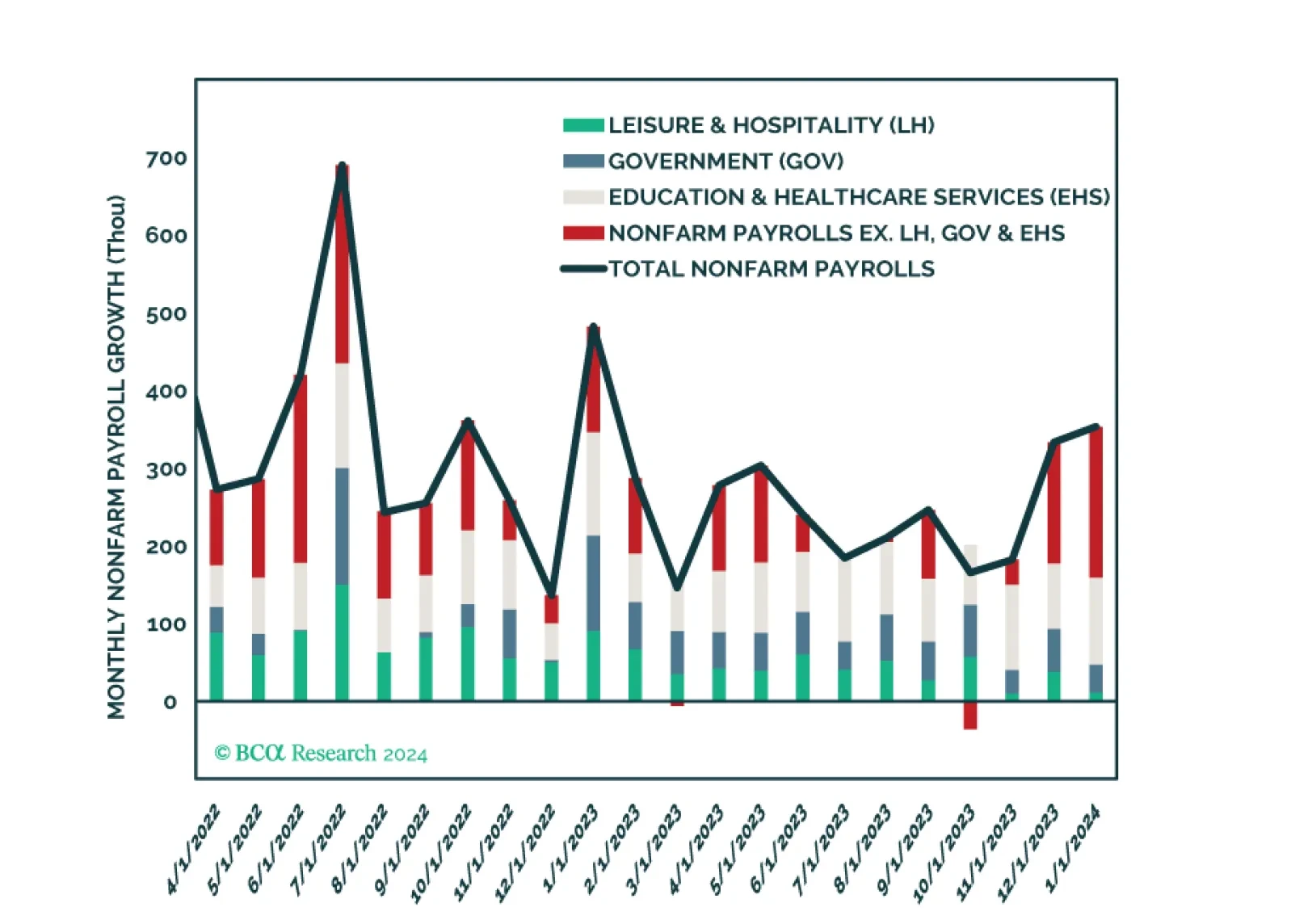

Our thoughts on bond positioning following this morning’s employment data.

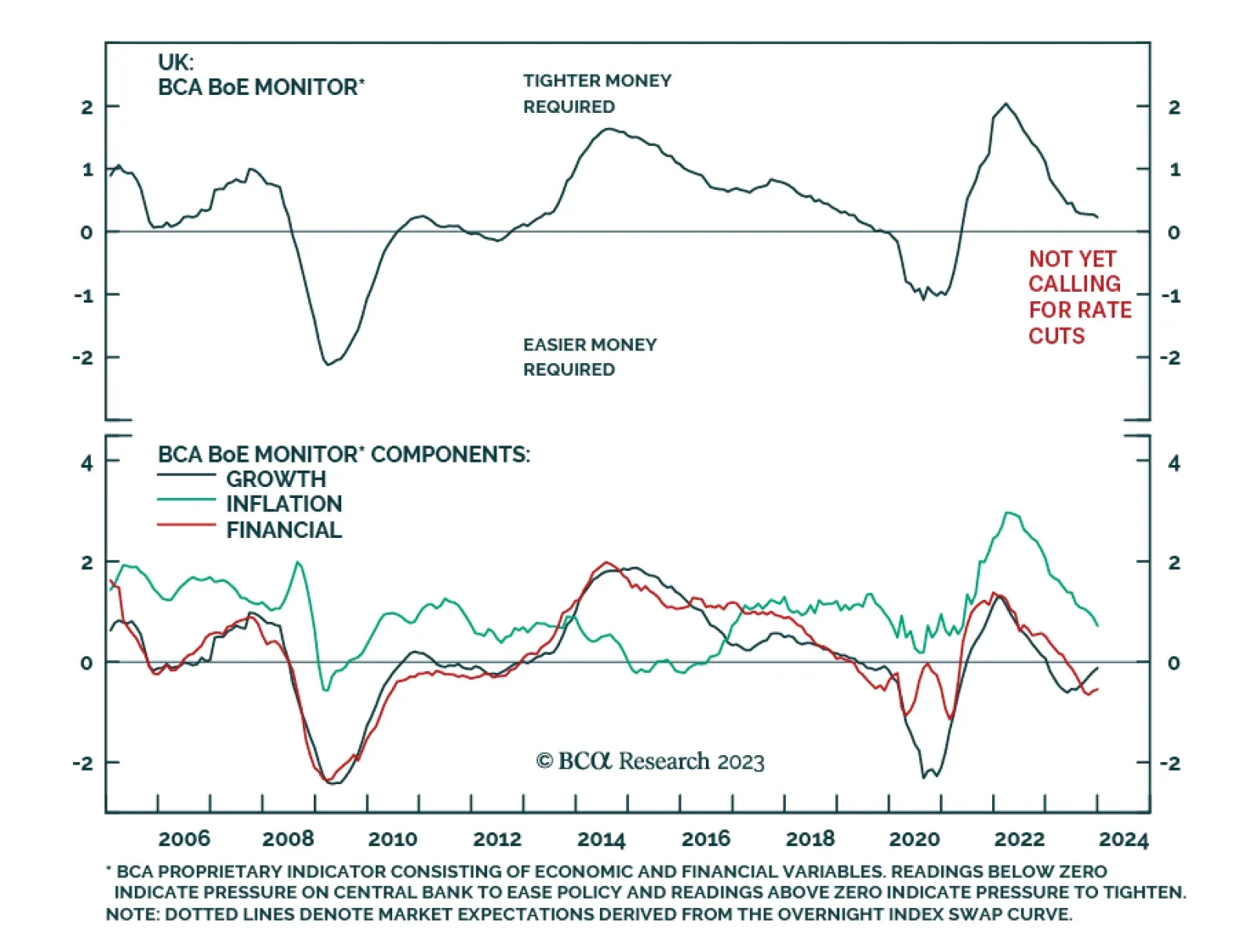

As expected, the Bank of England voted to keep its bank rate unchanged at 5.25% on Thursday – maintaining policy on hold for the fourth consecutive meeting. Two of the nine MPC members voted in favor of a 25bps rise (one less than in December) while one…

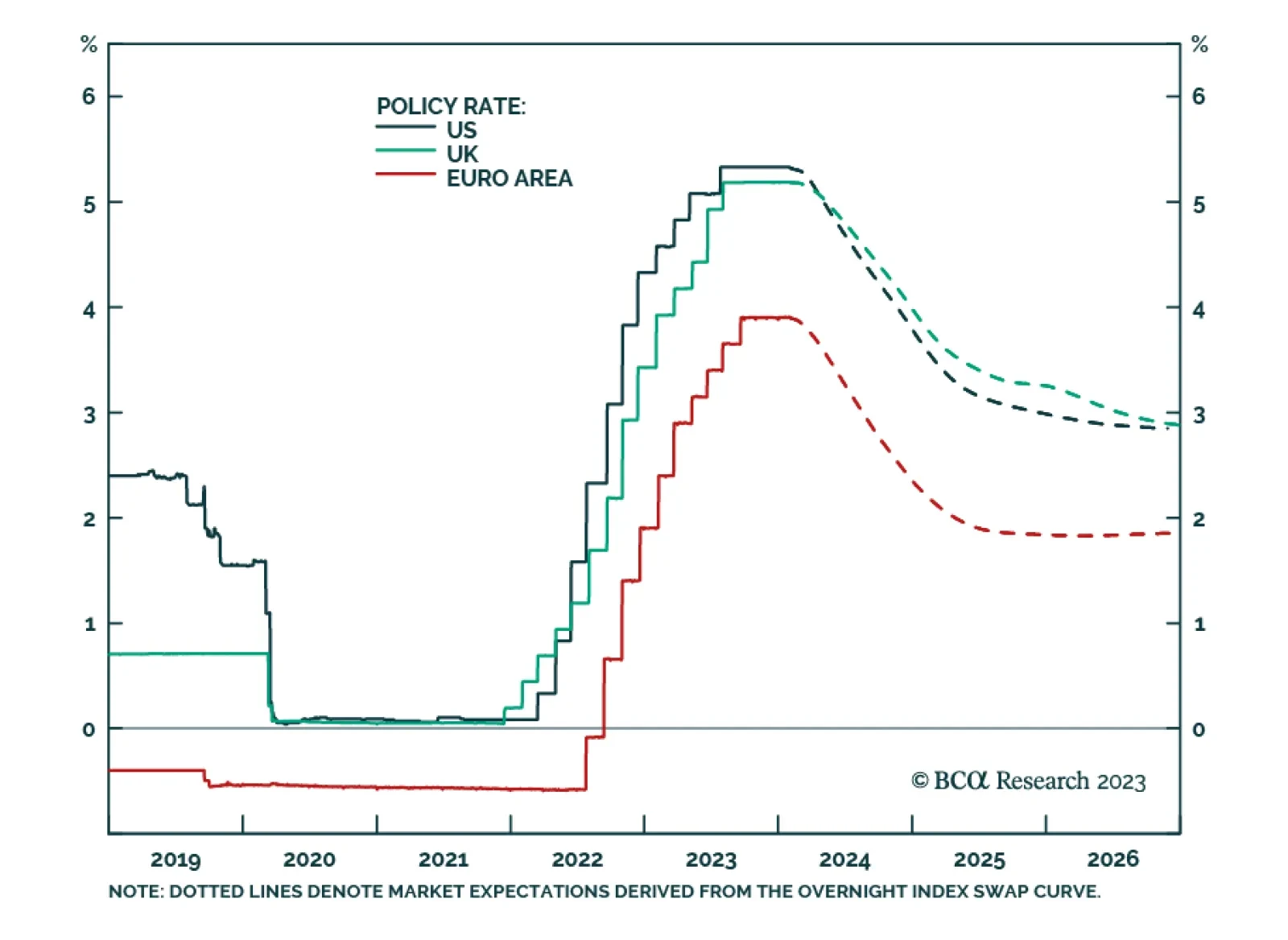

Given the huge disparities in wage inflation between the US, euro area and UK, it is remarkable that the markets are pricing near-identical rate cuts from the Fed, ECB, and BoE of around 150 bps through 2024. Assuming central banks don’t behave recklessly –…

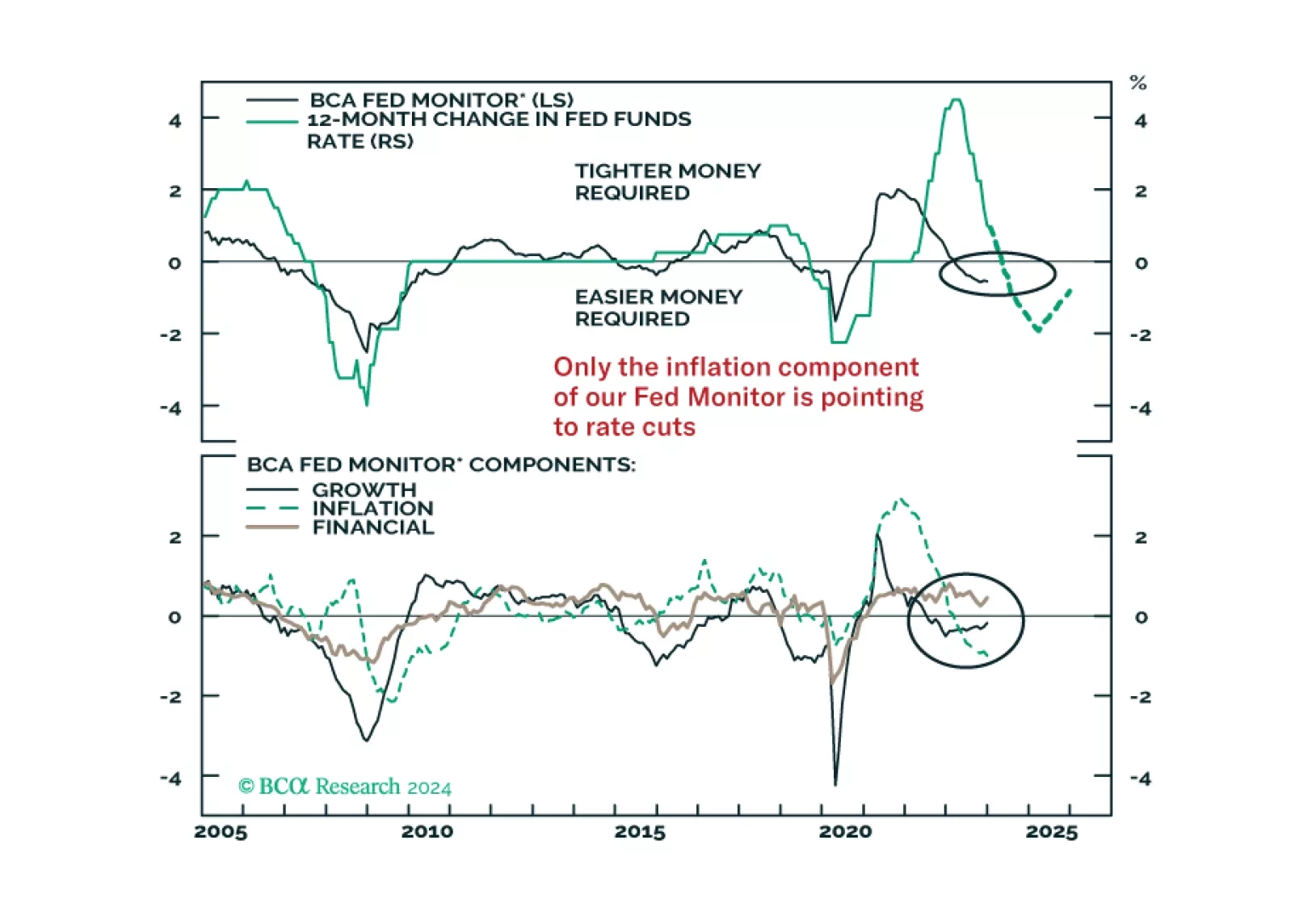

In this Insight, we share our thoughts on yesterday’s FOMC meeting and the Fed’s likely next moves, with implications for US bond strategy.

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.

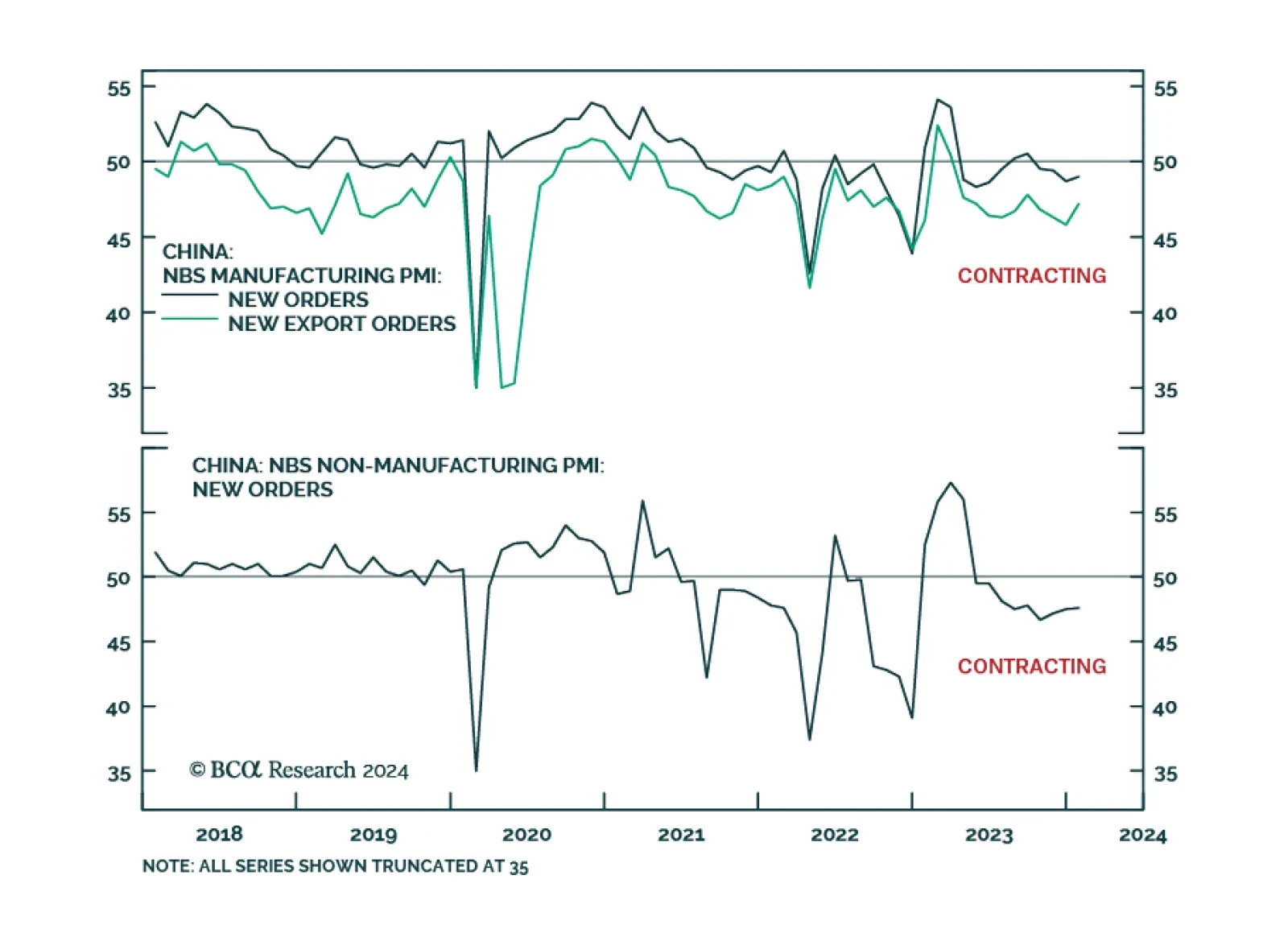

China’s official NBS PMI indicates that growth conditions remain sluggish. Although the composite index ticked up from 50.3 to 50.9, it is still barely in expansionary territory. Notably, the manufacturing PMI – which inched up by 0.2 points in January –…