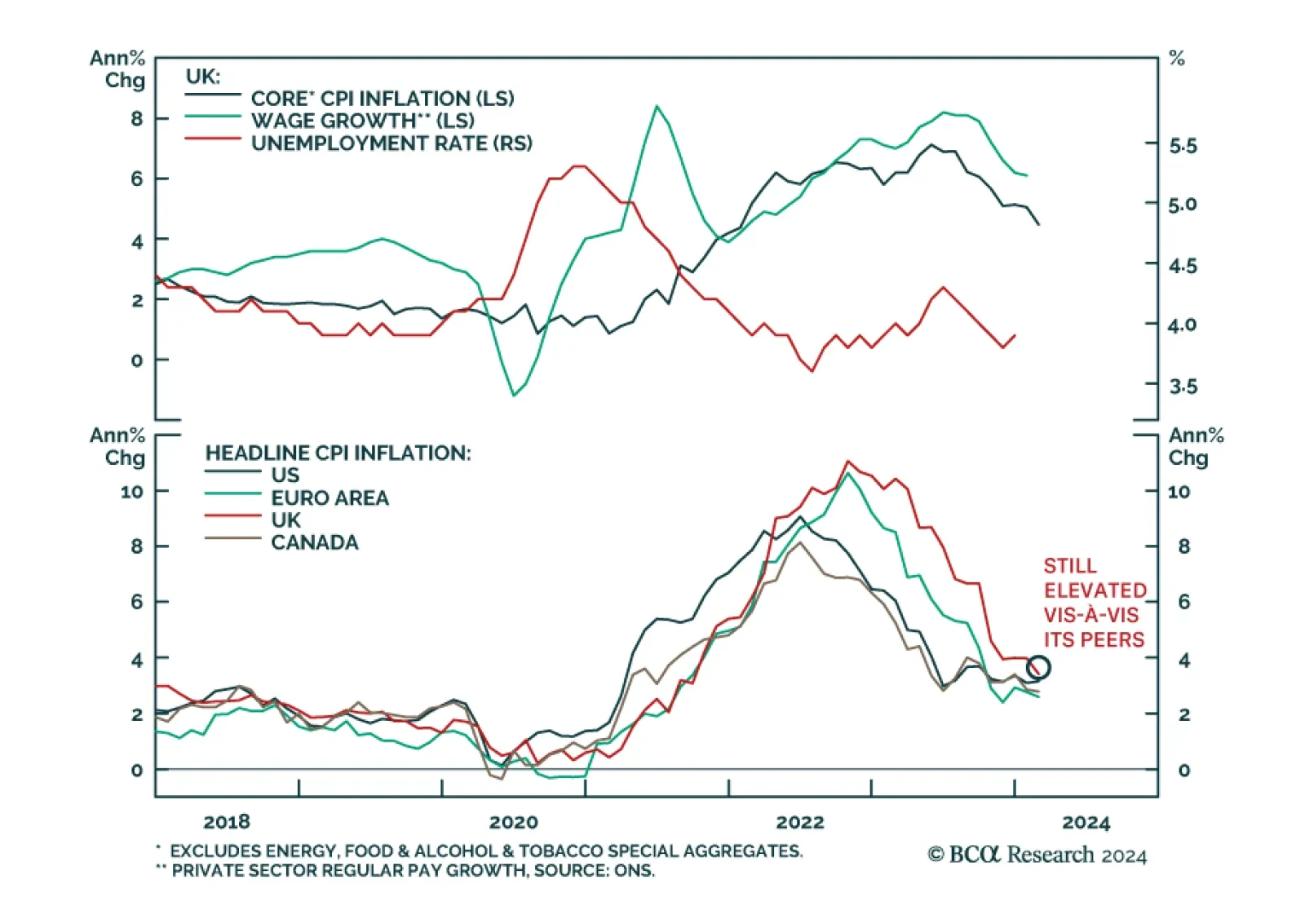

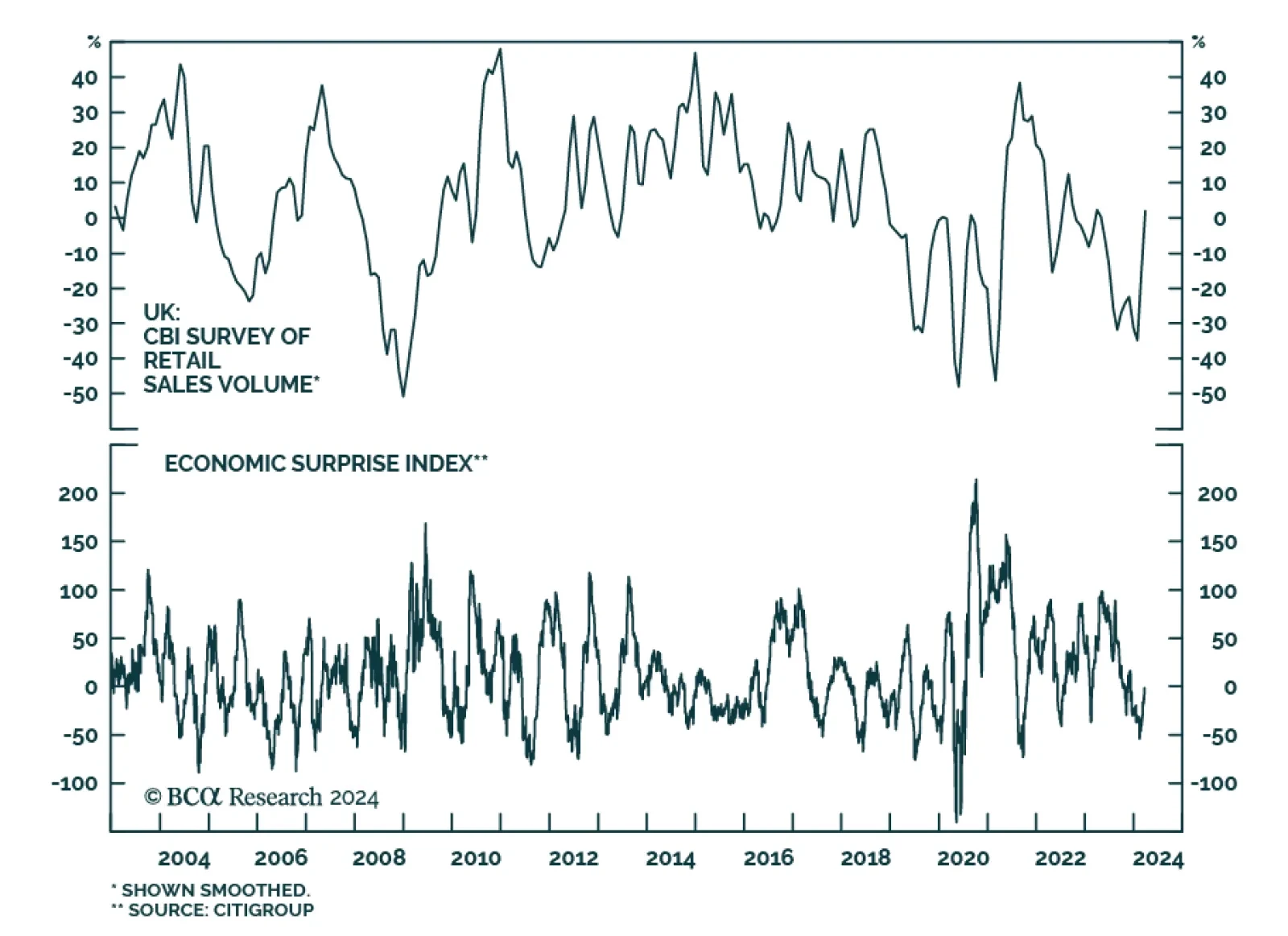

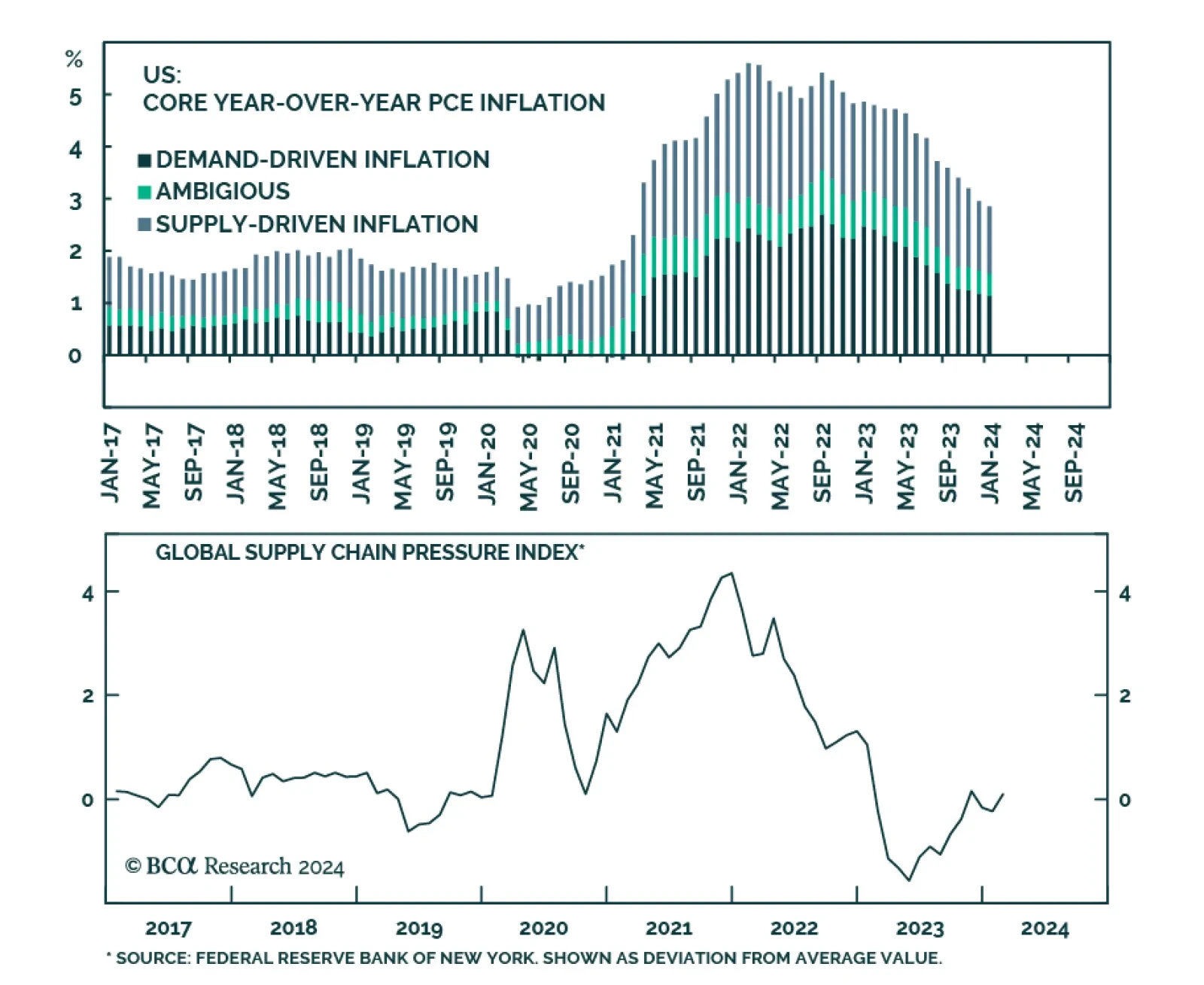

Inflation/Deflation

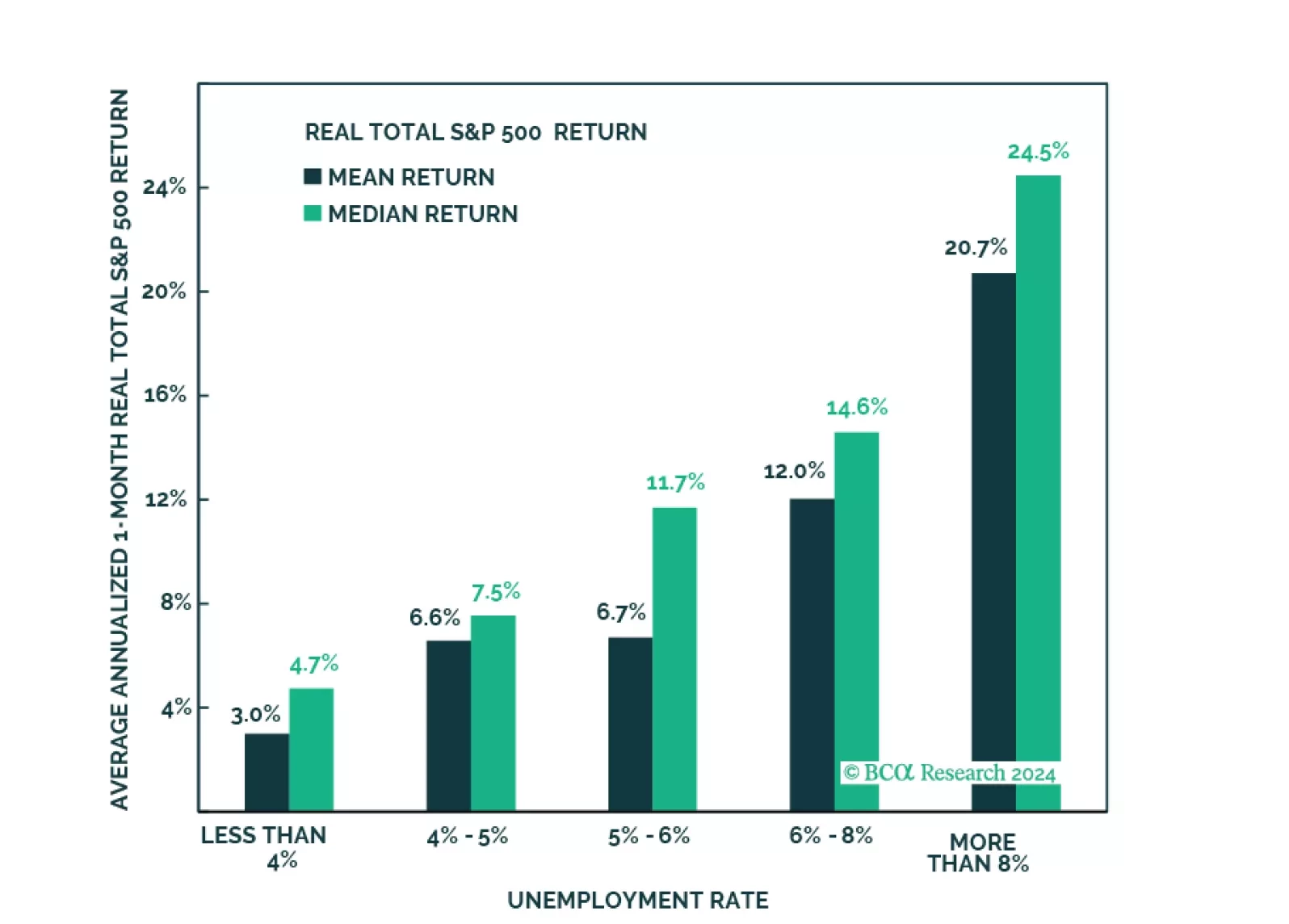

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

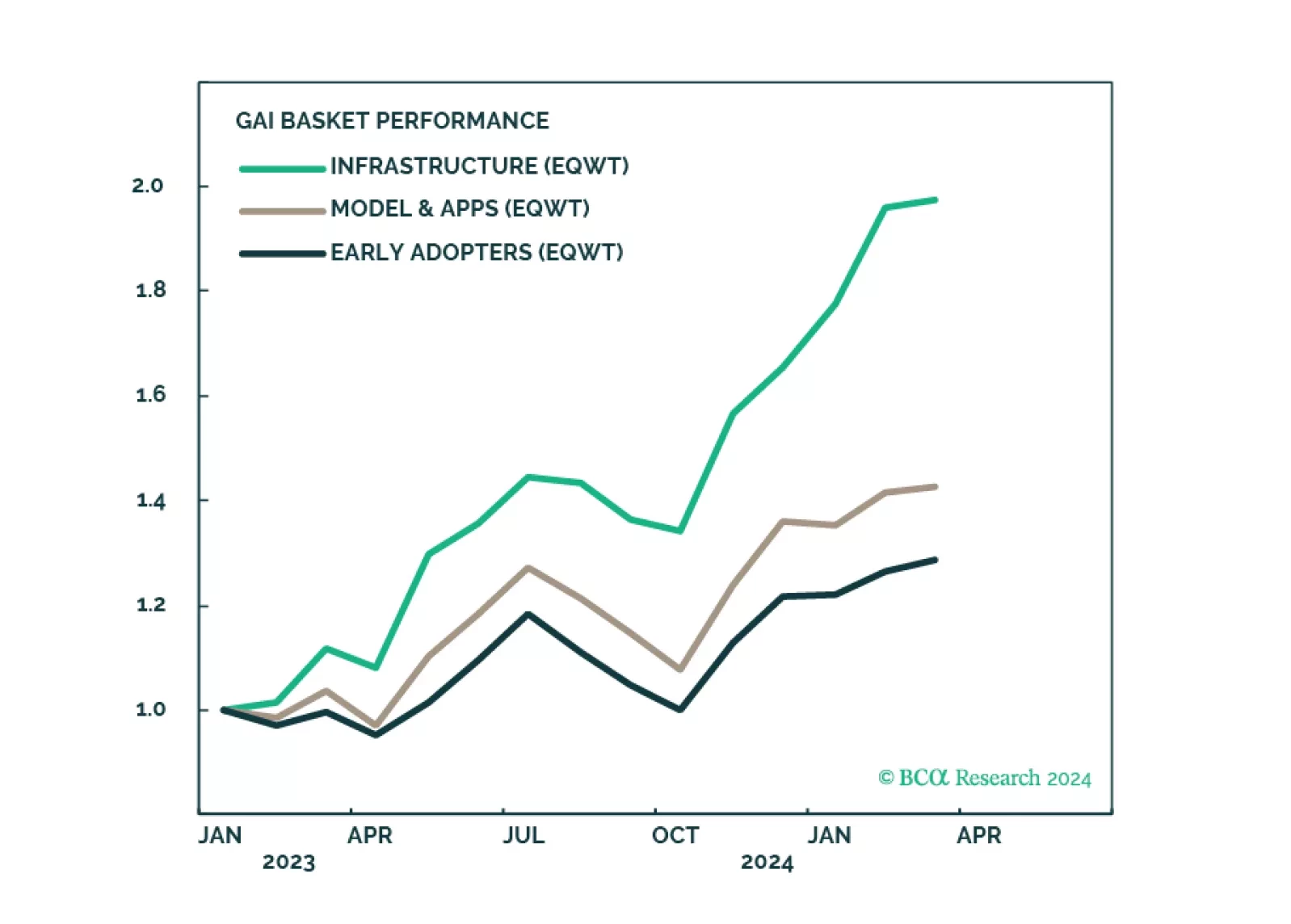

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

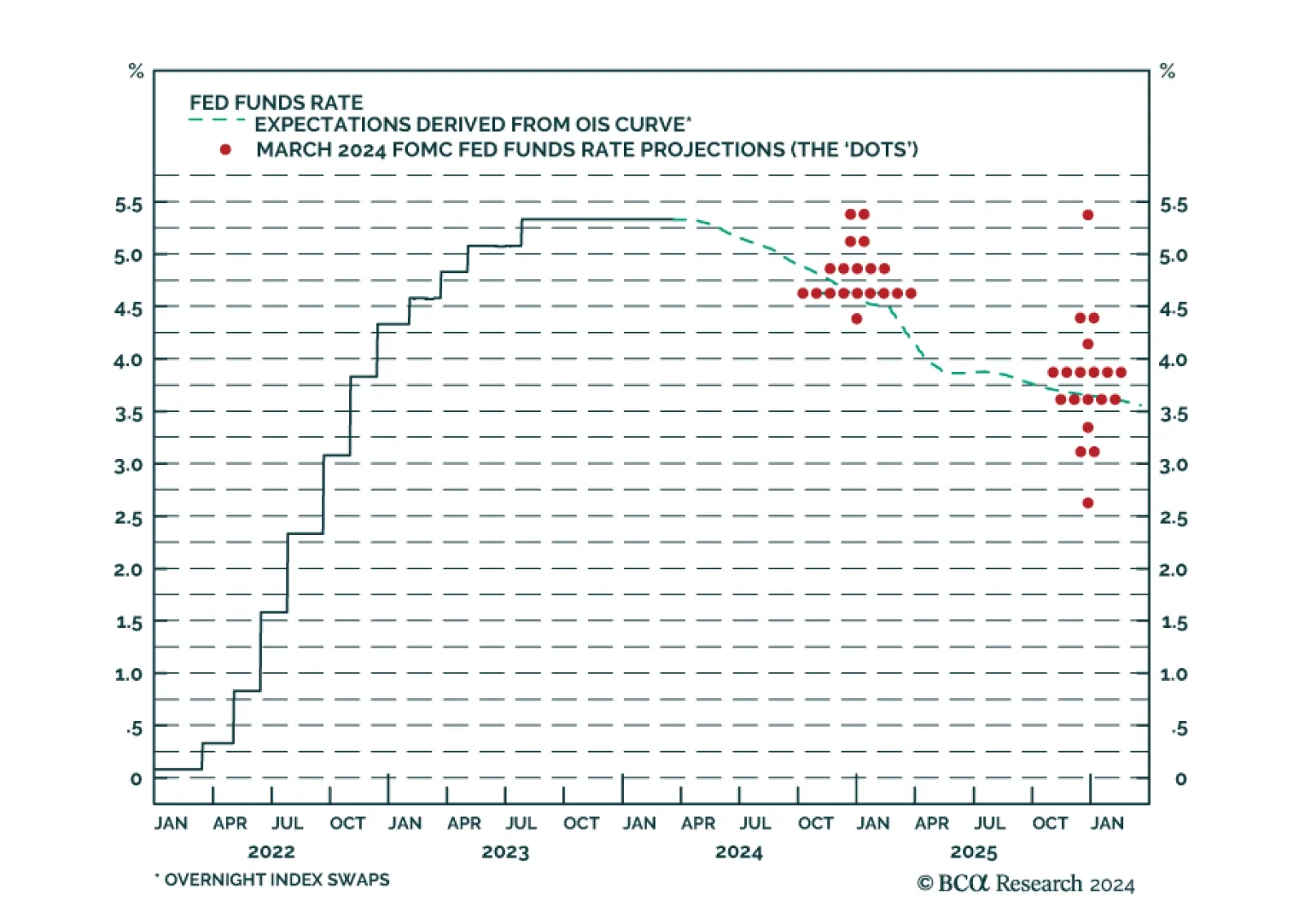

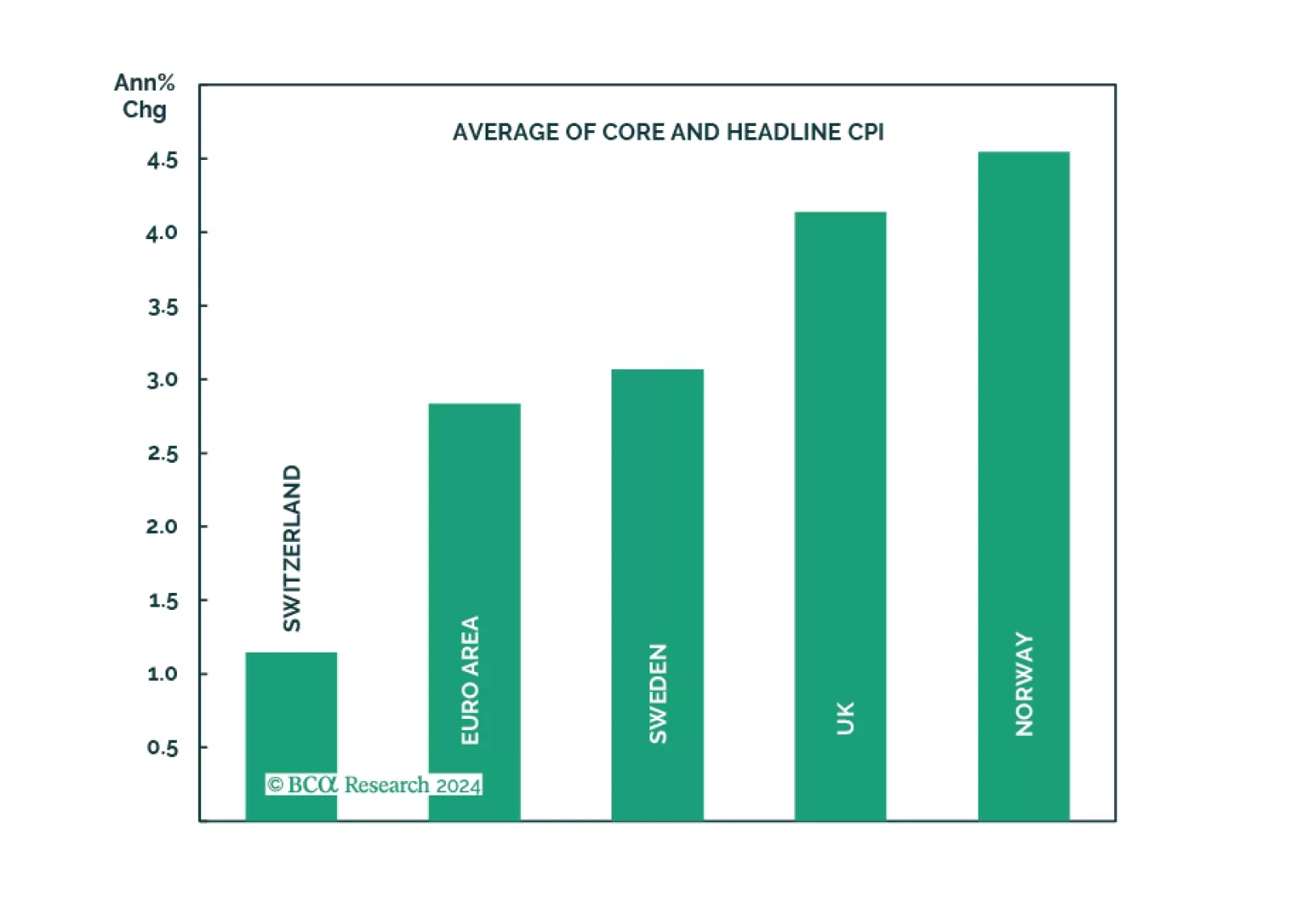

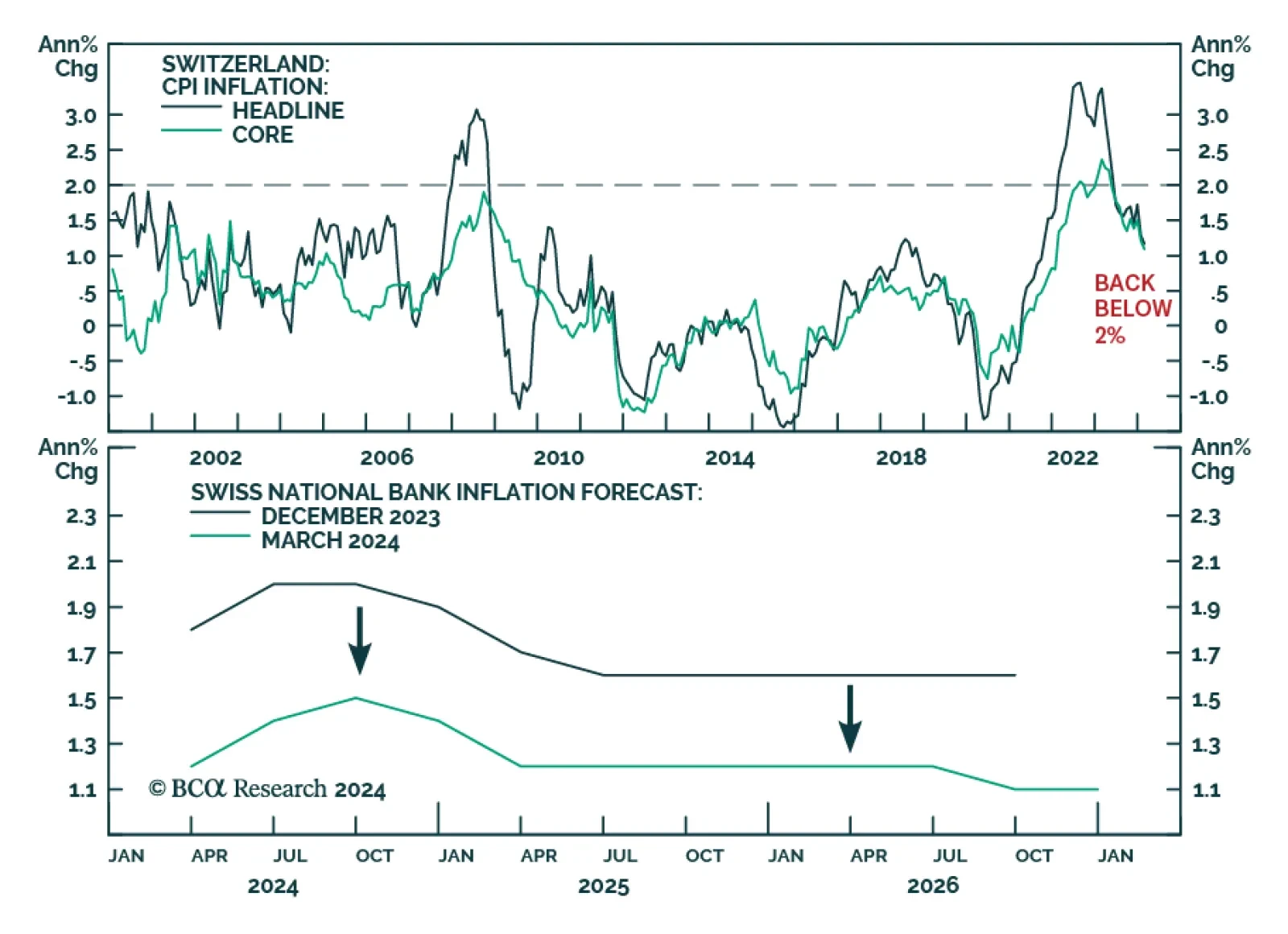

Does the recent surprise rate cut by the Swiss National Bank augur other dovish surprises among major central banks in Europe?

The US Presidential election is eight months away. In this report, we will be looking at what is left of President Biden’s political capital and his room for actions in the next few months which may include market-negative actions such as the recently announced investigation into Apple.