Inflation/Deflation

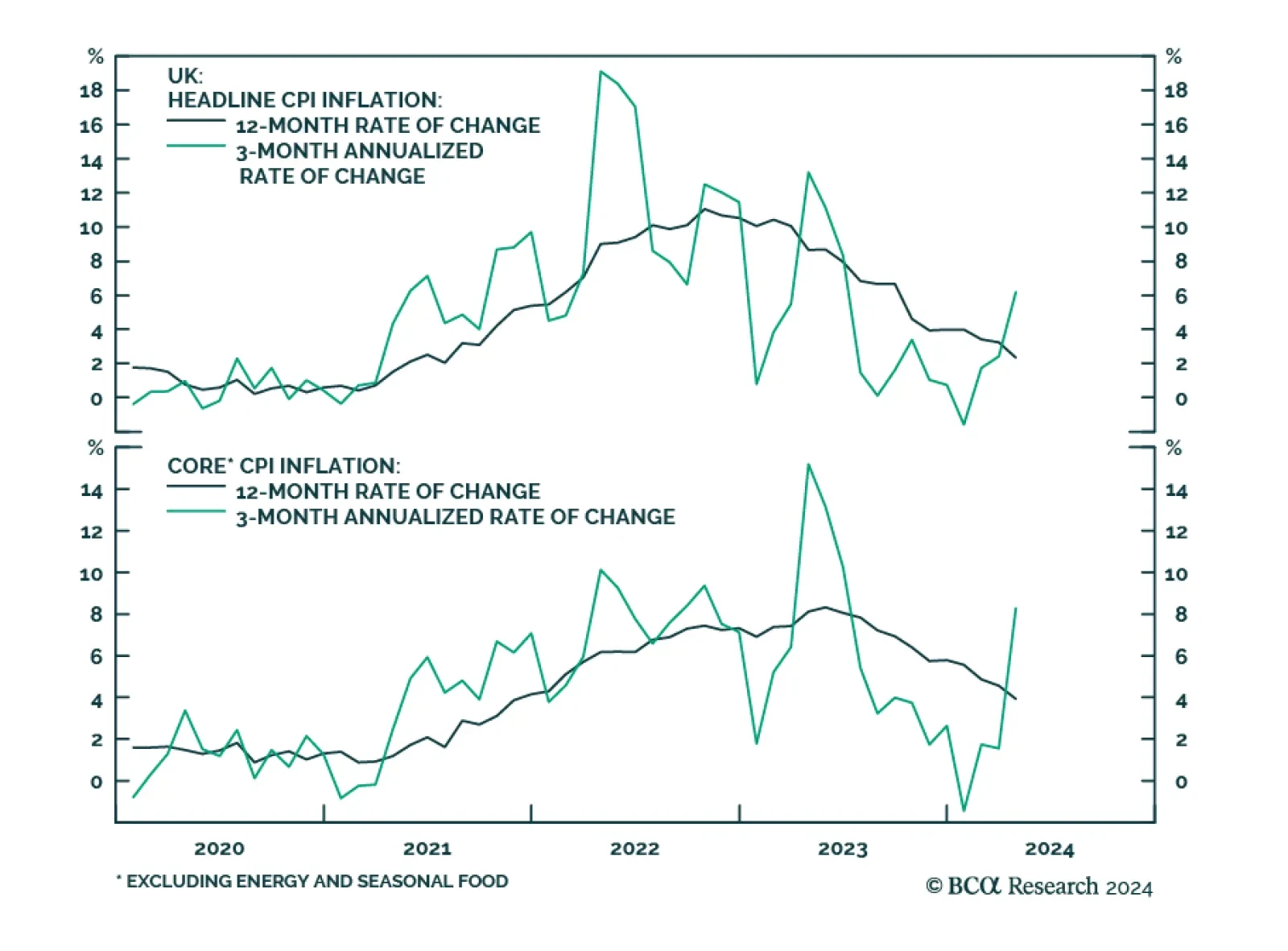

The UK CPI release surprised markets to the upside across the board on Wednesday. Headline CPI increased 2.3% year-on-year, above expectations of 2.1%. Core surprised to the upside as well, moderating from 4.2% to 3.9%y/y, less than the moderation embedded in…

Canada’s headline CPI inflation decelerated in April from 2.9% y/y to 2.7% y/y. Notably, core median CPI eased from 2.9% y/y to a softer-than-anticipated 2.6% y/y and core trimmed-mean CPI ticked lower from 3.2% to 2.9%. Food and durable goods led the…

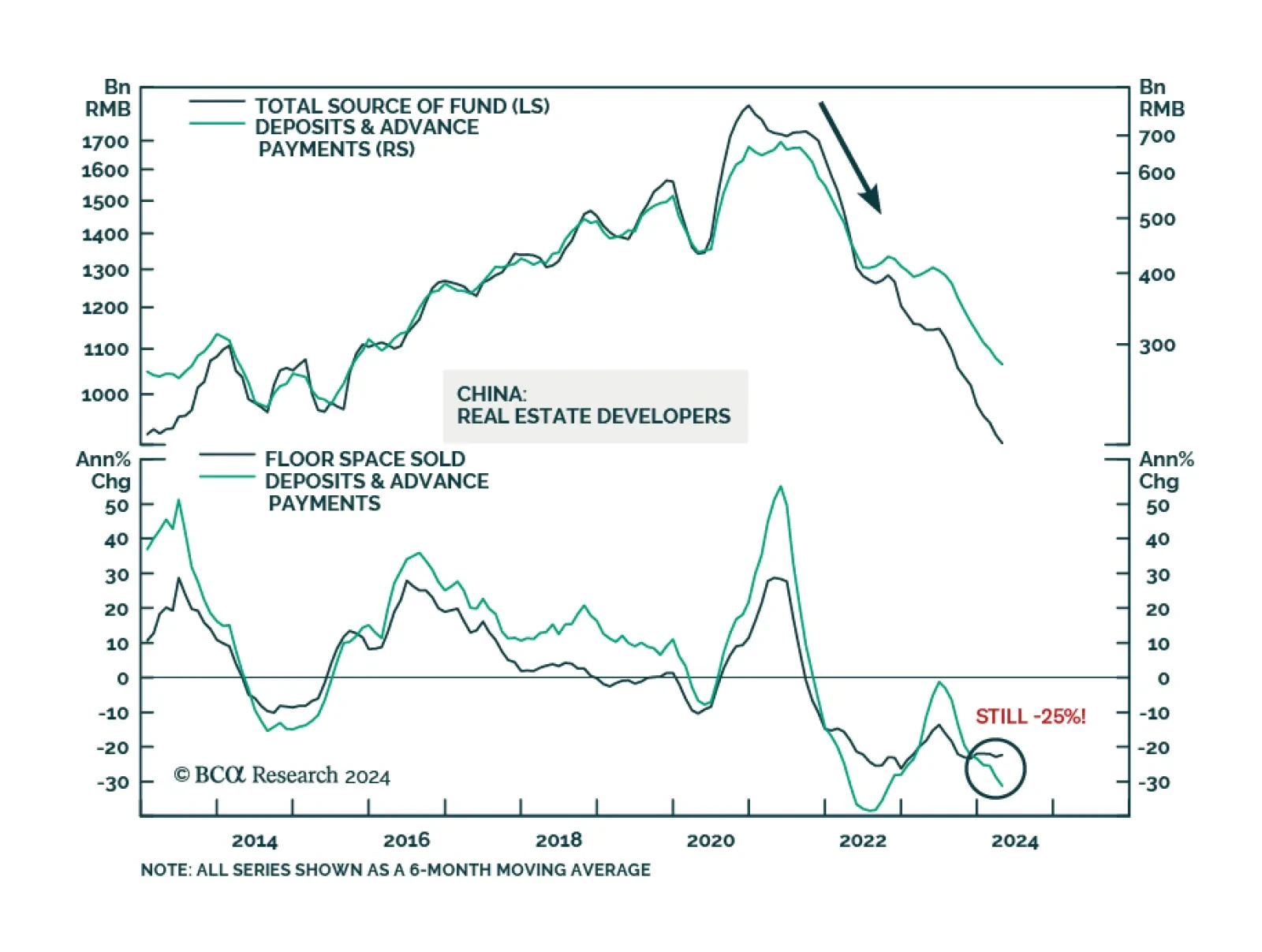

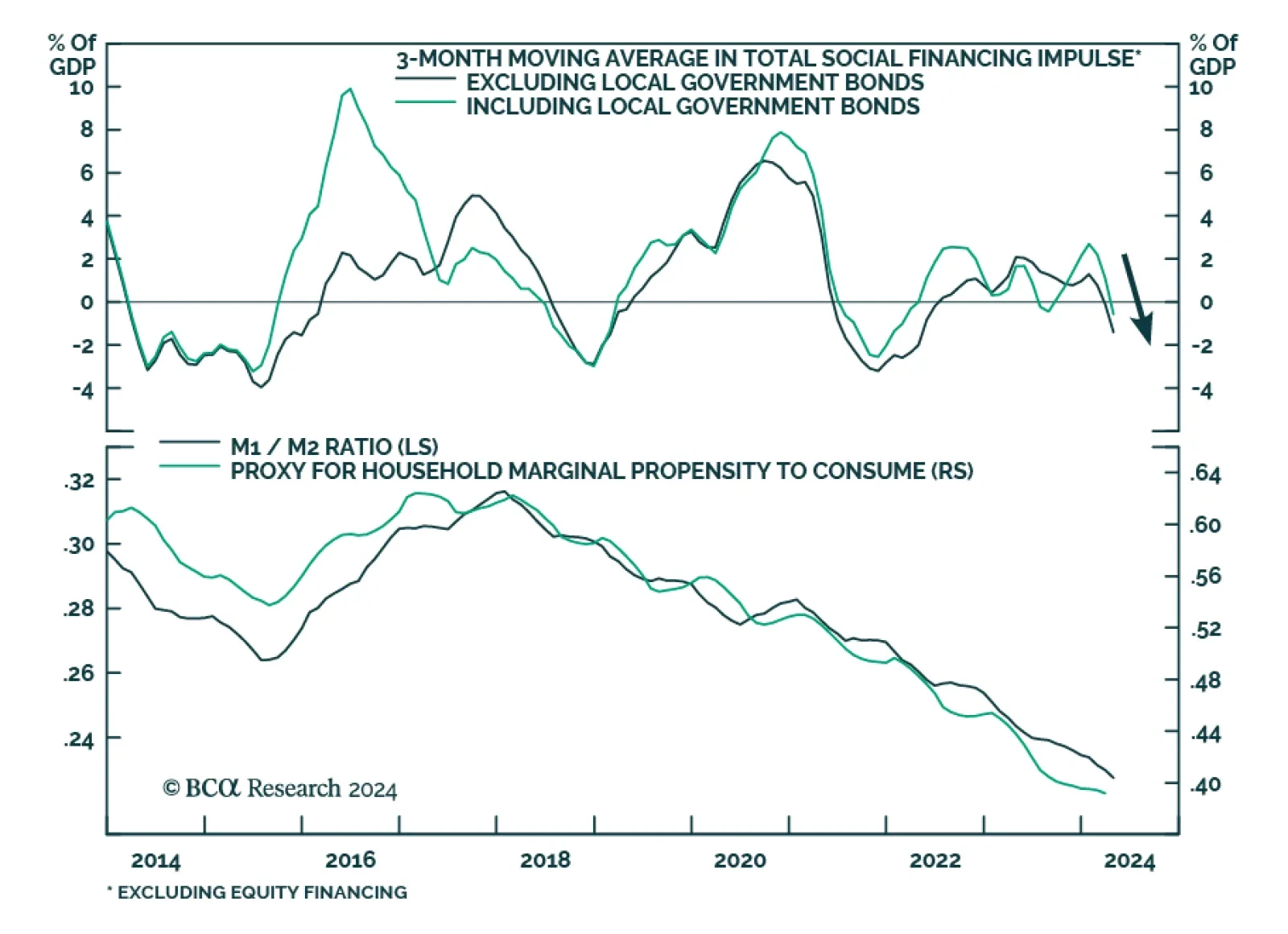

Several economic releases out of China disappointed in April. Retail sales decelerated from 3.1% y/y to 2.3% y/y and fixed asset investment growth slowed from 4.5% YTD y/y to 4.2% YTD y/y. Both were expected to accelerate. Although industrial production…

According to BCA Research’s Global Investment Strategy service, the BoC should have sufficient evidence of Canadian disinflation to cut rates this summer. The market is pricing in a similar amount of rate cuts for the BoC and the Fed over the next 12 months.…

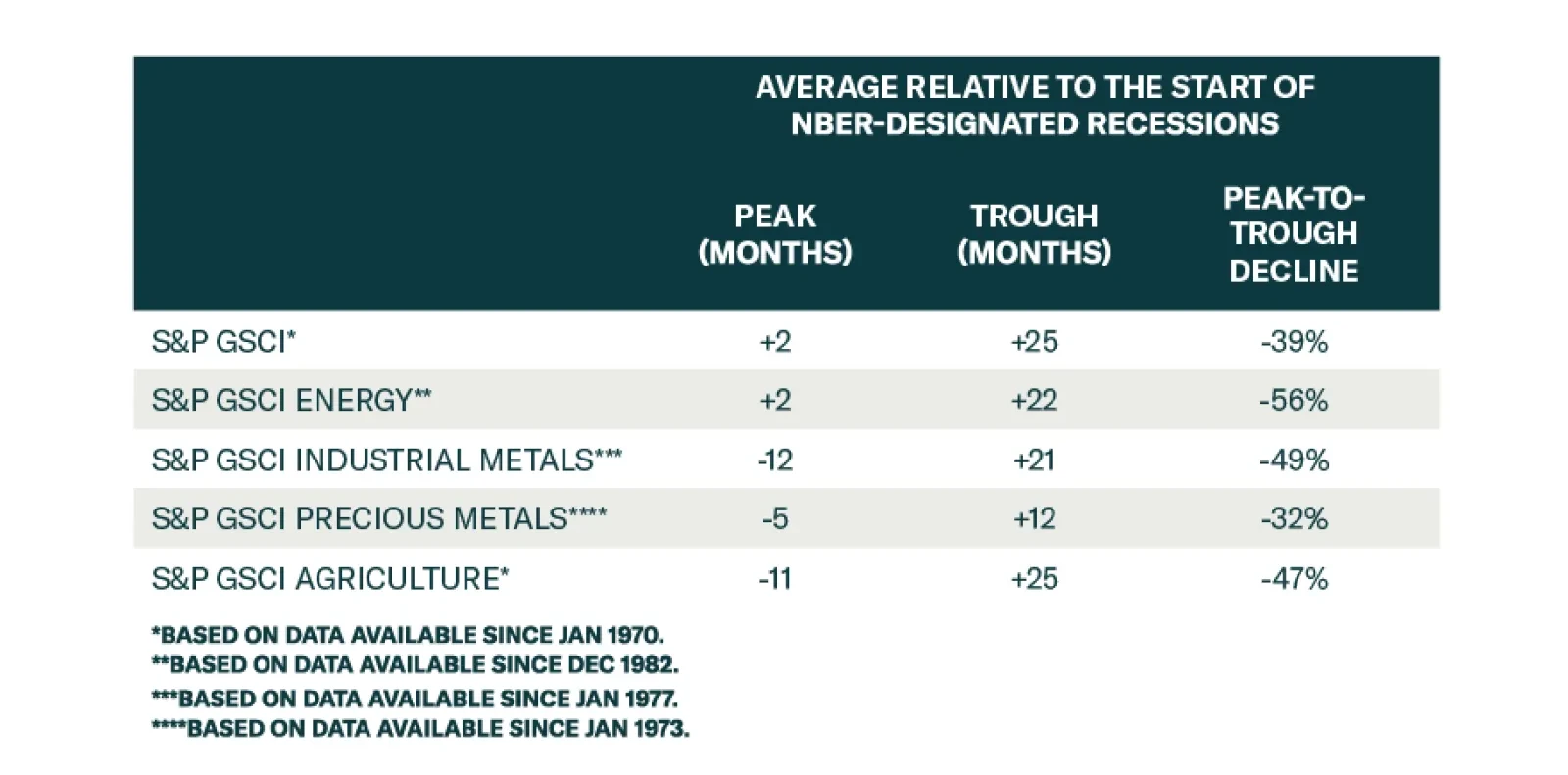

According to BCA Research’s Commodity & Energy Strategy service, among the commodity groups, industrial metals provide the most reliable leading signal that the US economy is heading toward recession. Industrial metals’ greater exposure to the very…

US headline CPI inflation decelerated to a softer-than-expected 0.3% m/m (3.4% y/y) in April, from 0.4% m/m (3.5% y/y). Core CPI eased from 0.4% m/m (3.5% y/y) to 0.3% m/m (3.4% y/y). Declines in new (-0.4% m/m) and used vehicles (-1.4% m/m) prices largely…

Our updated views on Treasury yields and Fed policy following this morning’s CPI report.

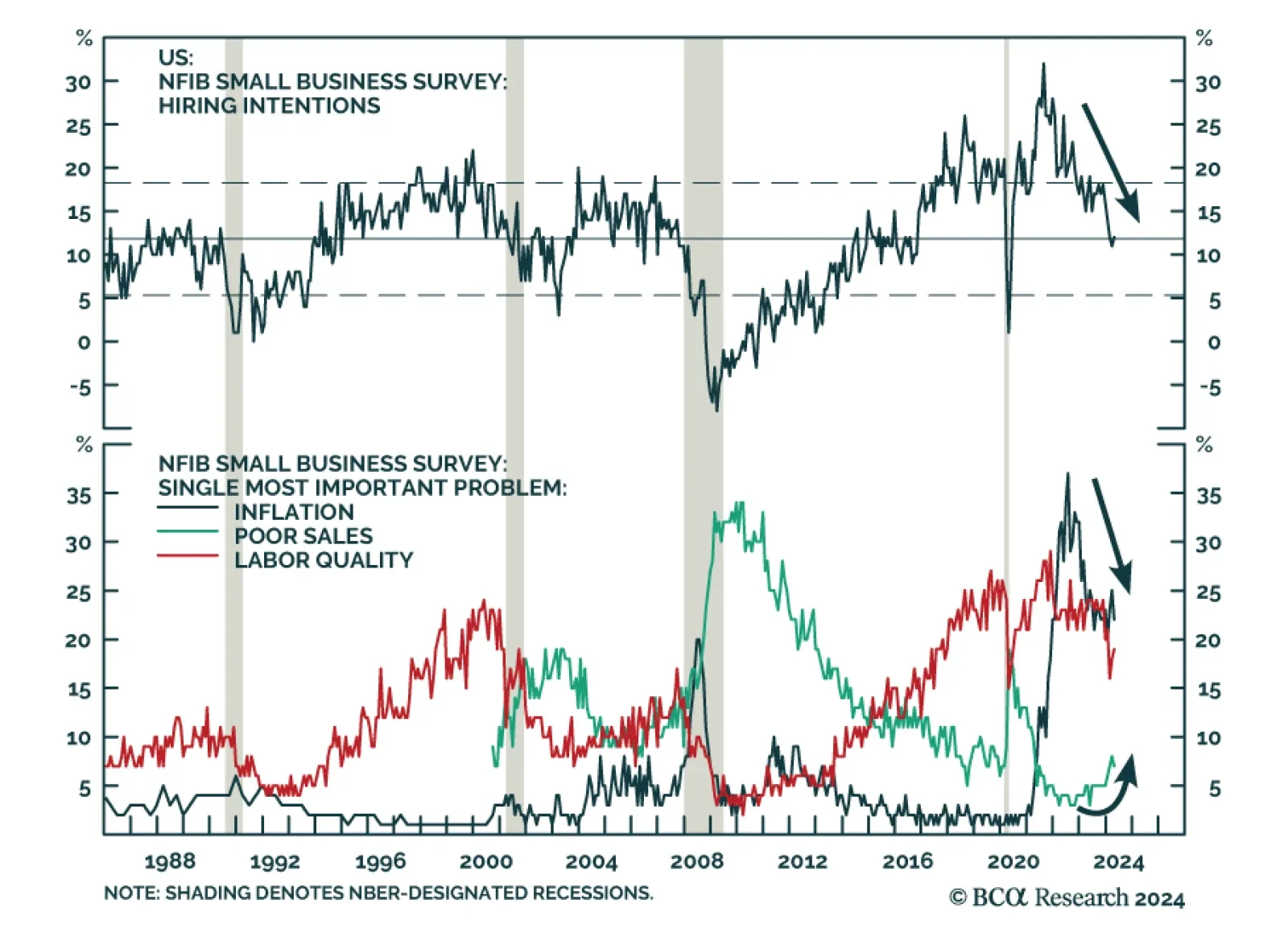

On the surface, the Tuesday release of the NFIB Small Business Survey indicated resilience among small businesses. The headline index appreciated to 89.7 from 88.5, upending expectations of a moderation to 88.2. However, the marginal improvement has not…

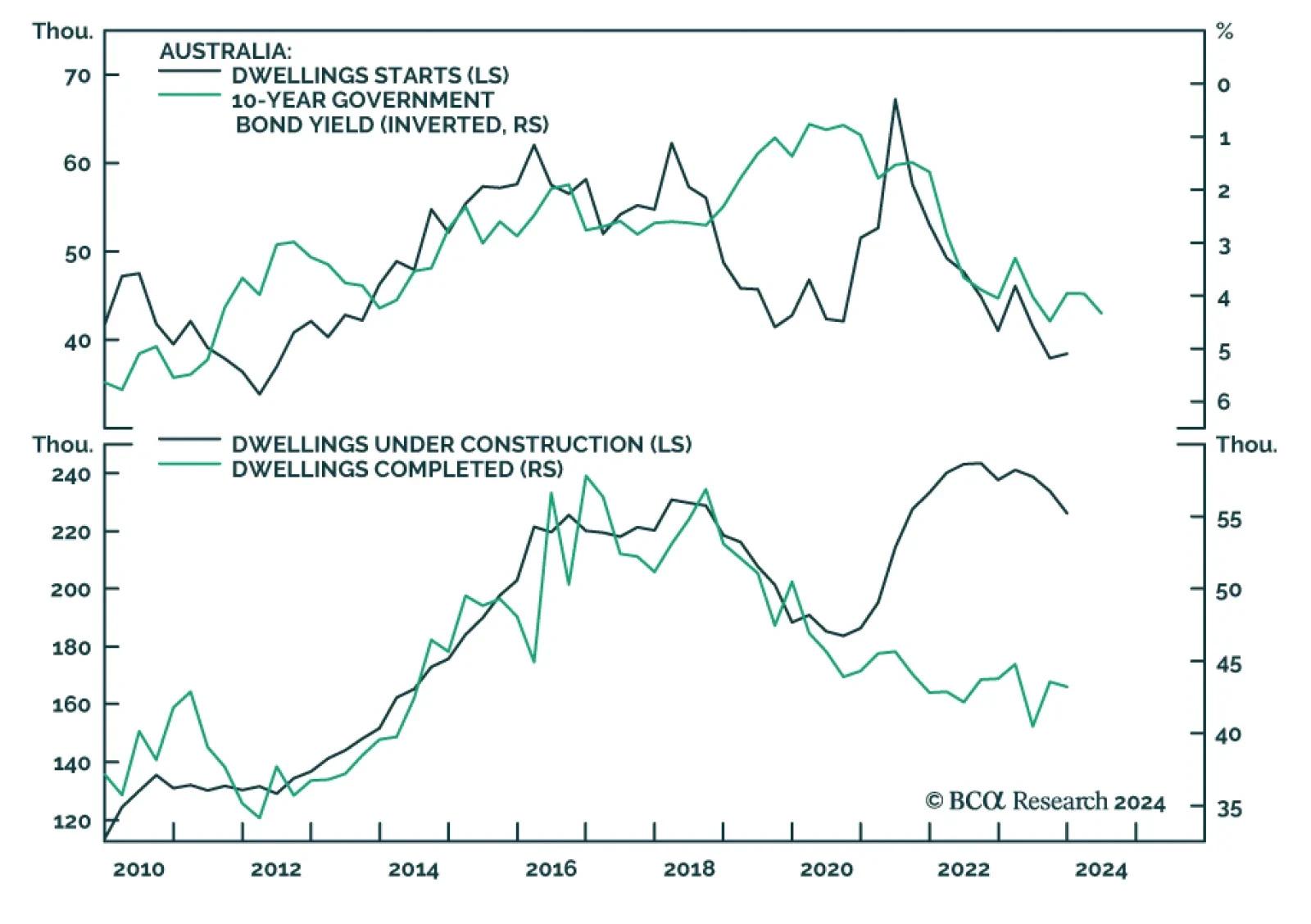

Despite historically high interest rates and the fact that variable-rate mortgage issuances dominate the mortgage market landscape, Australian home prices continue to climb at a close to double-digit annual rate. The Core Logic House Price index is now…

Chinese aggregate financing, a broad measure of credit, declined on a YTD basis, from CNY 12.9tr to CNY 12.7tr in April, disappointing expectations that it would grow to CNY 13.9tr. Moreover, new loan growth missed expectations (from CNY 9.5tr to CNY 10.2tr)…