Inflation/Deflation

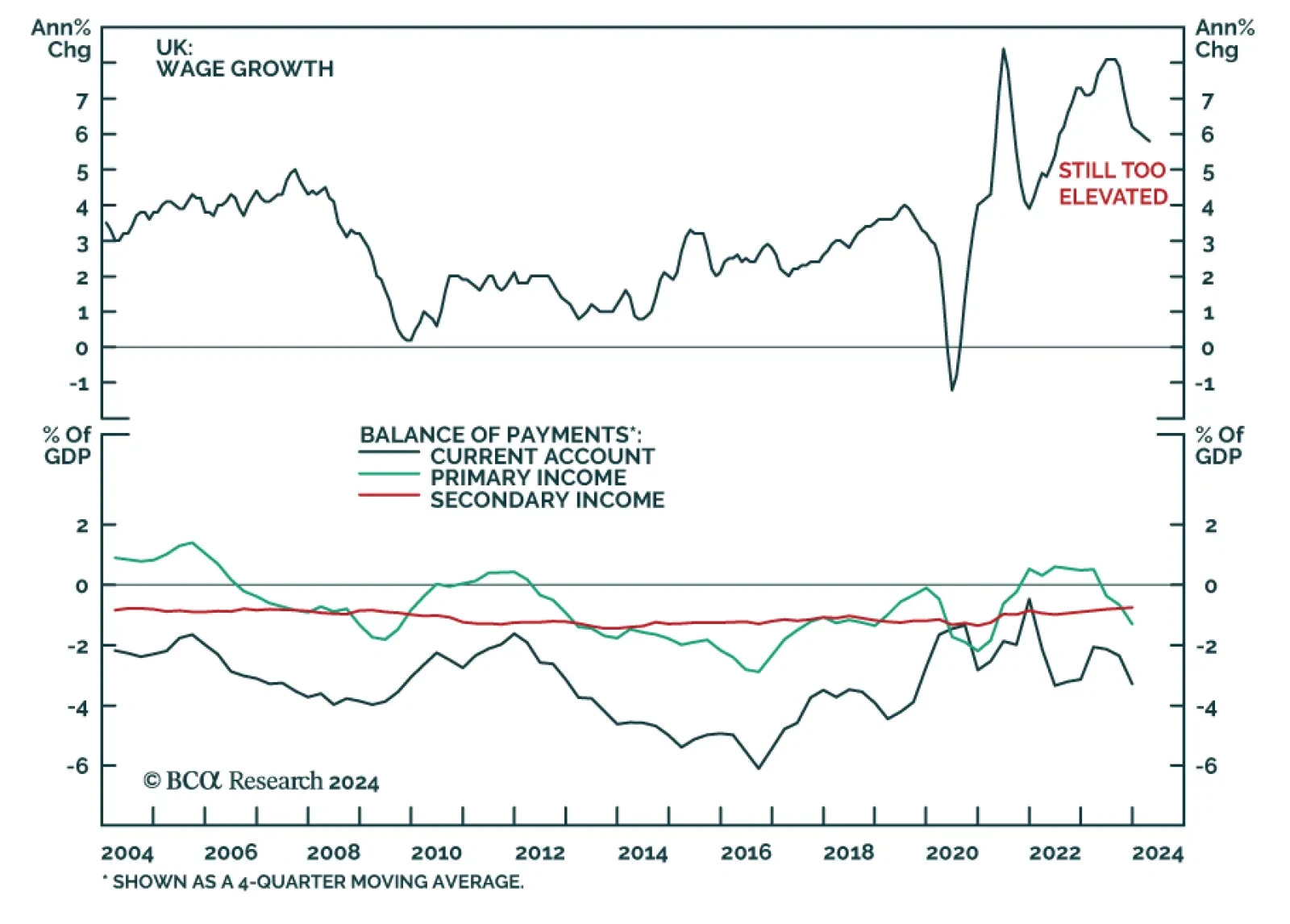

The UK unemployment rate surprised to the upside in the 3-month period ending in April, ticking up to 4.4% against expectations it would remain stable at March’s originally reported 4.3%. Concurrently, wage growth remains elevated. The 3-month measure of…

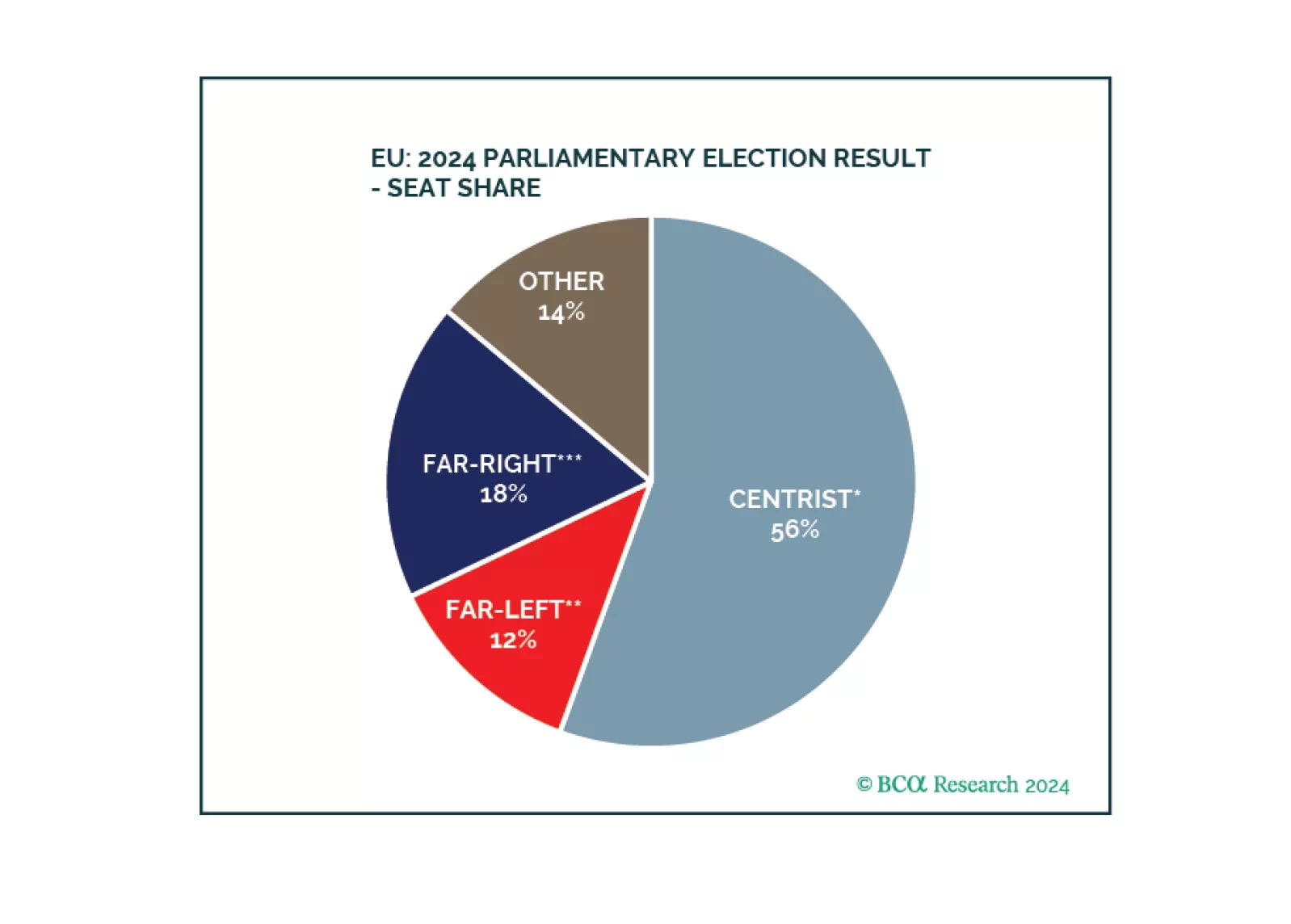

Europe did not witness a major policy reversal. Inflationary pressures are coming down, enabling the ECB to cut rates and European states to maintain soft budgets. Geopolitical challenges ensure that European parties continue to cooperate on national defense, economic security, and energy security.

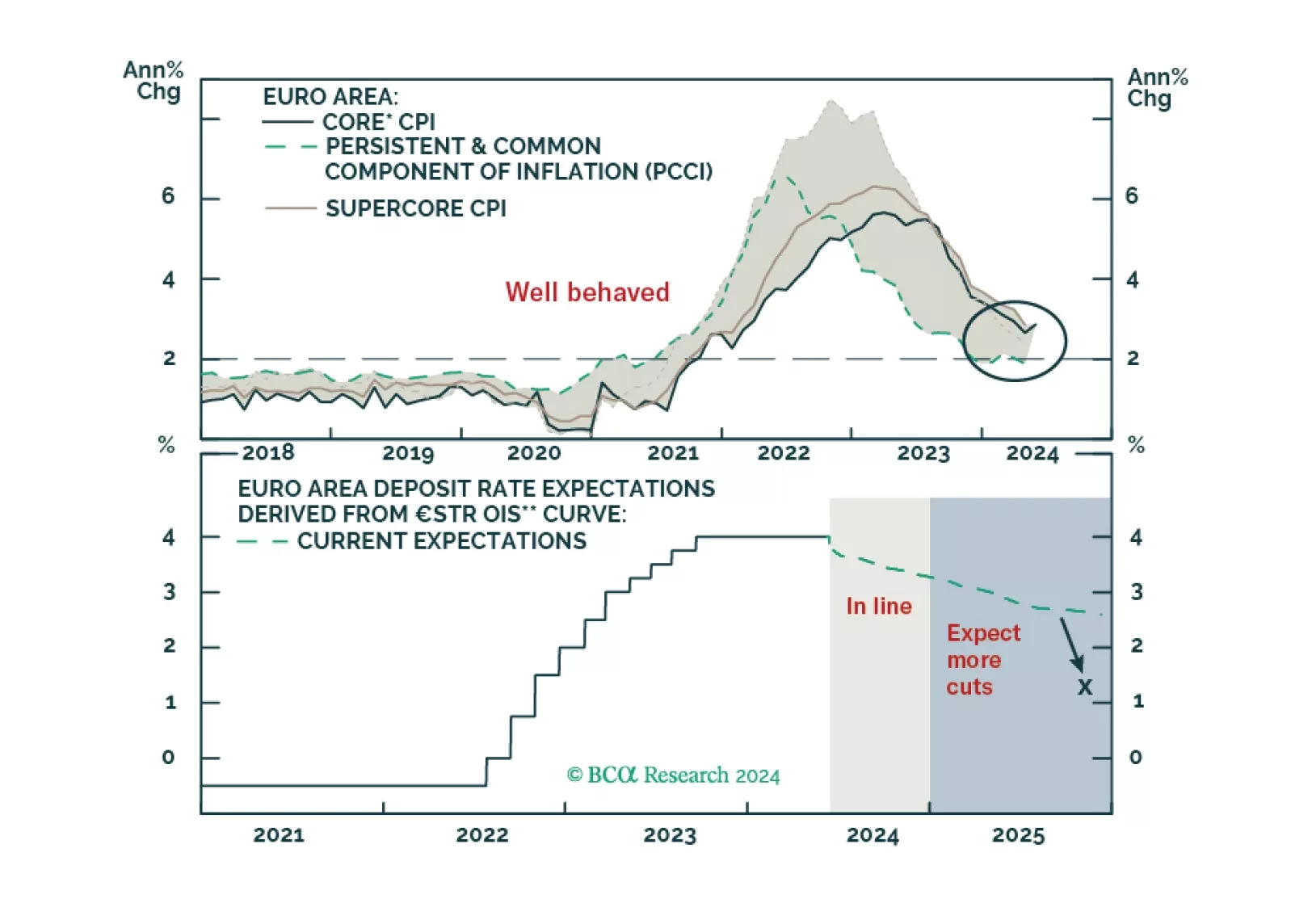

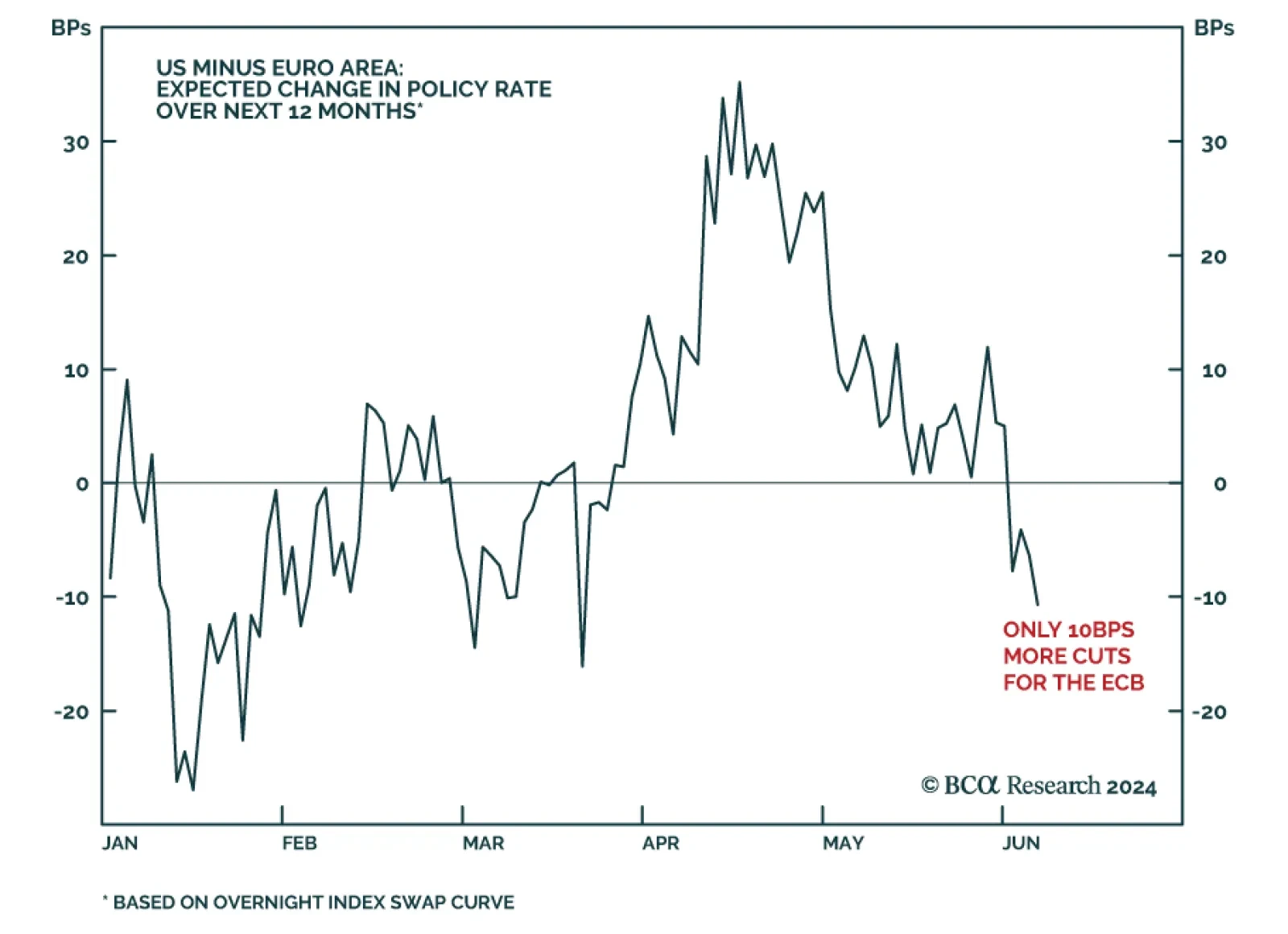

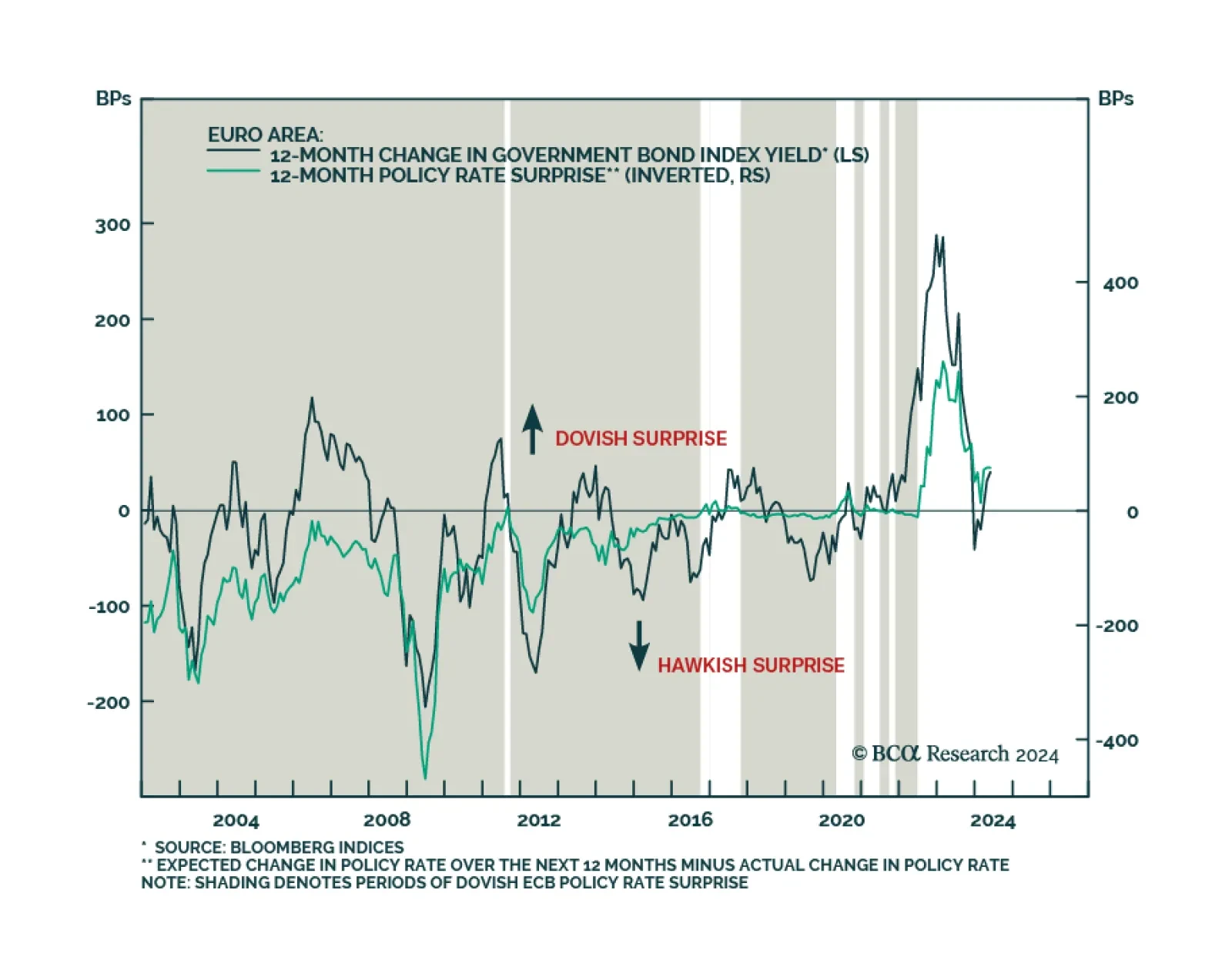

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

After holding rates steady over the past nine months, the ECB delivered on its widely expected rate cut on Thursday. The Governing Council lowered all three key ECB interest rates by 25 bps, bringing the refinancing, marginal lending facility and deposit…

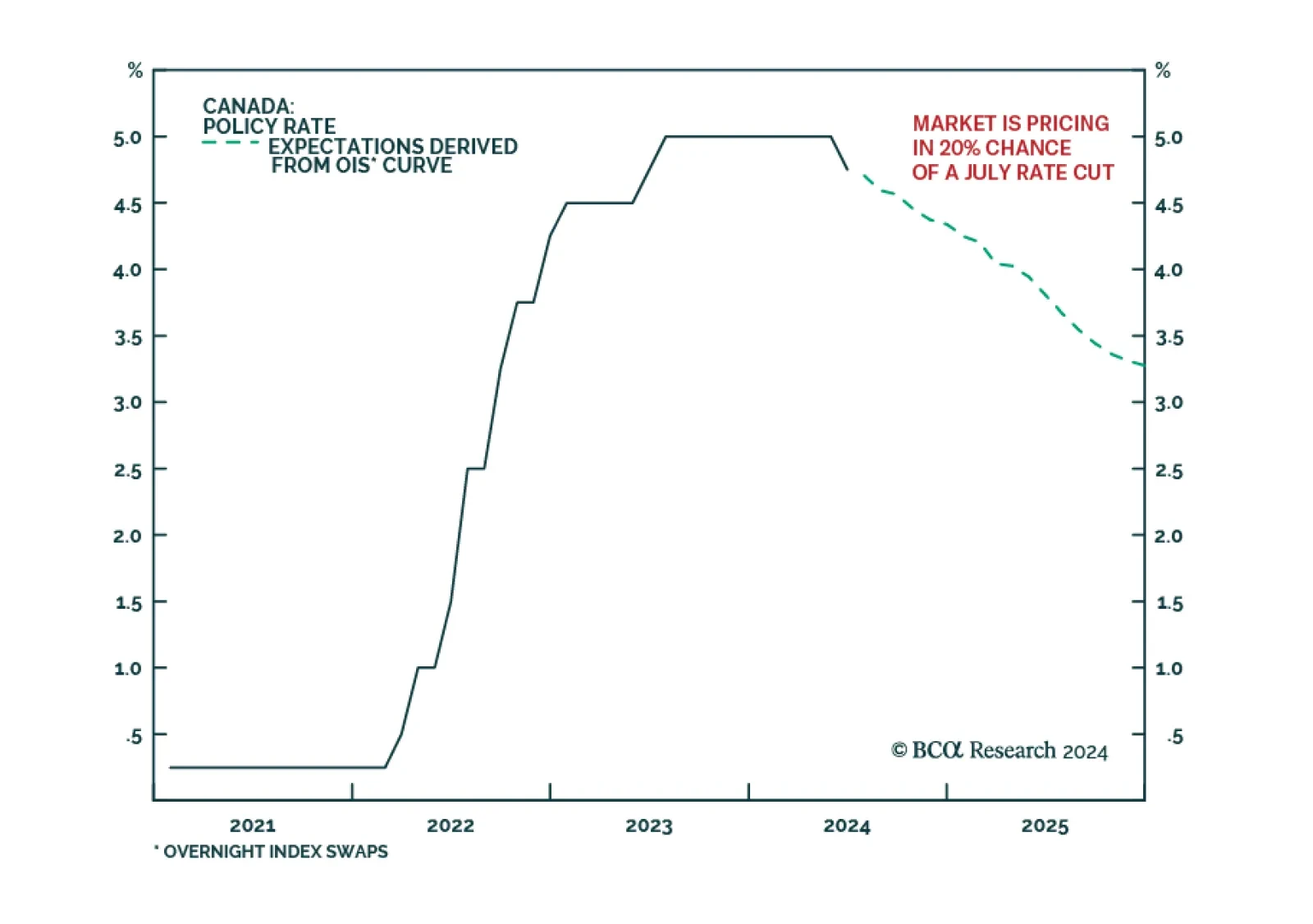

The Bank of Canada reduced its policy rate by 25 basis points from 5% to 4.75% on Wednesday, in line with the market consensus. Headline inflation and the BoC’s preferred measures of core inflation are within the BoC’s target range of 1-3%, and shorter-term…

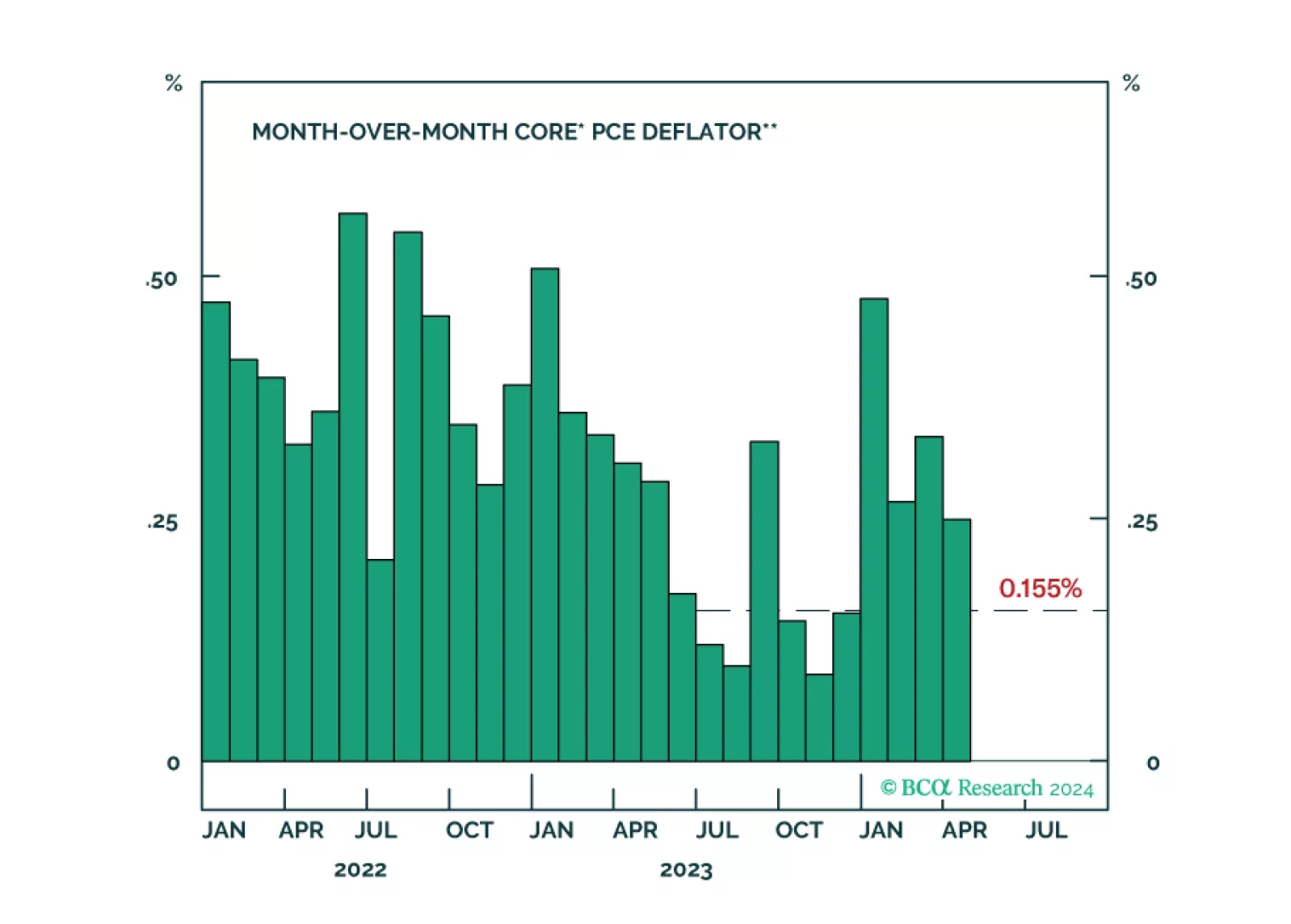

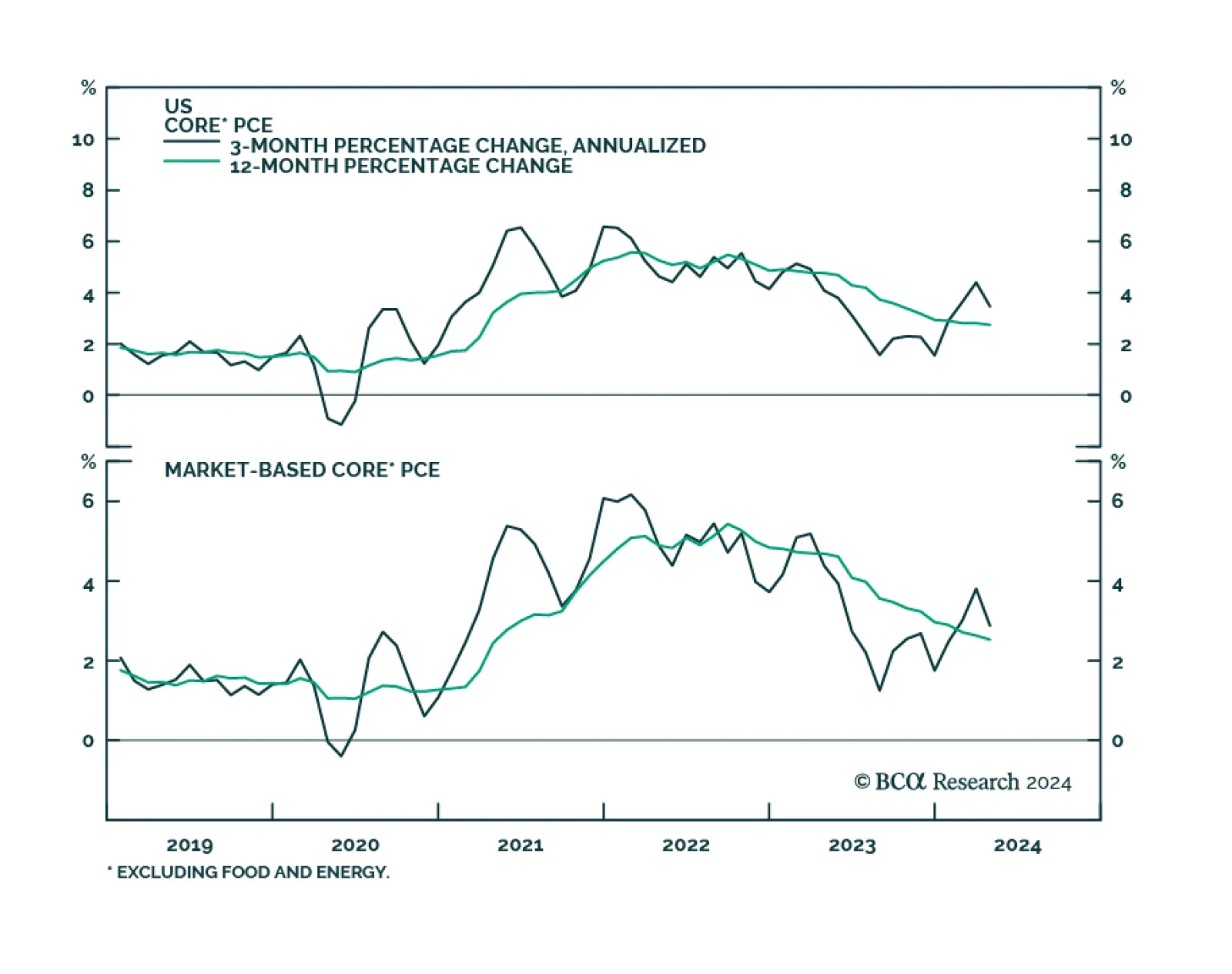

The moderation in core PCE in April was a step in the right direction towards a Fed easing. Our Global Investment Strategists also highlighted that outside of a few pandemic-related “catch-up” categories such as shelter, health care, and auto insurance, CPI…

Our Portfolio Allocation Summary for June 2024.

US nominal personal income growth decelerated from 0.5% m/m to 0.3% m/m in April, in line with expectations. However, nominal personal spending surprised to the downside, and contracted 0.1% m/m in real terms. Core PCE – the Fed’s favored inflation gauge –…

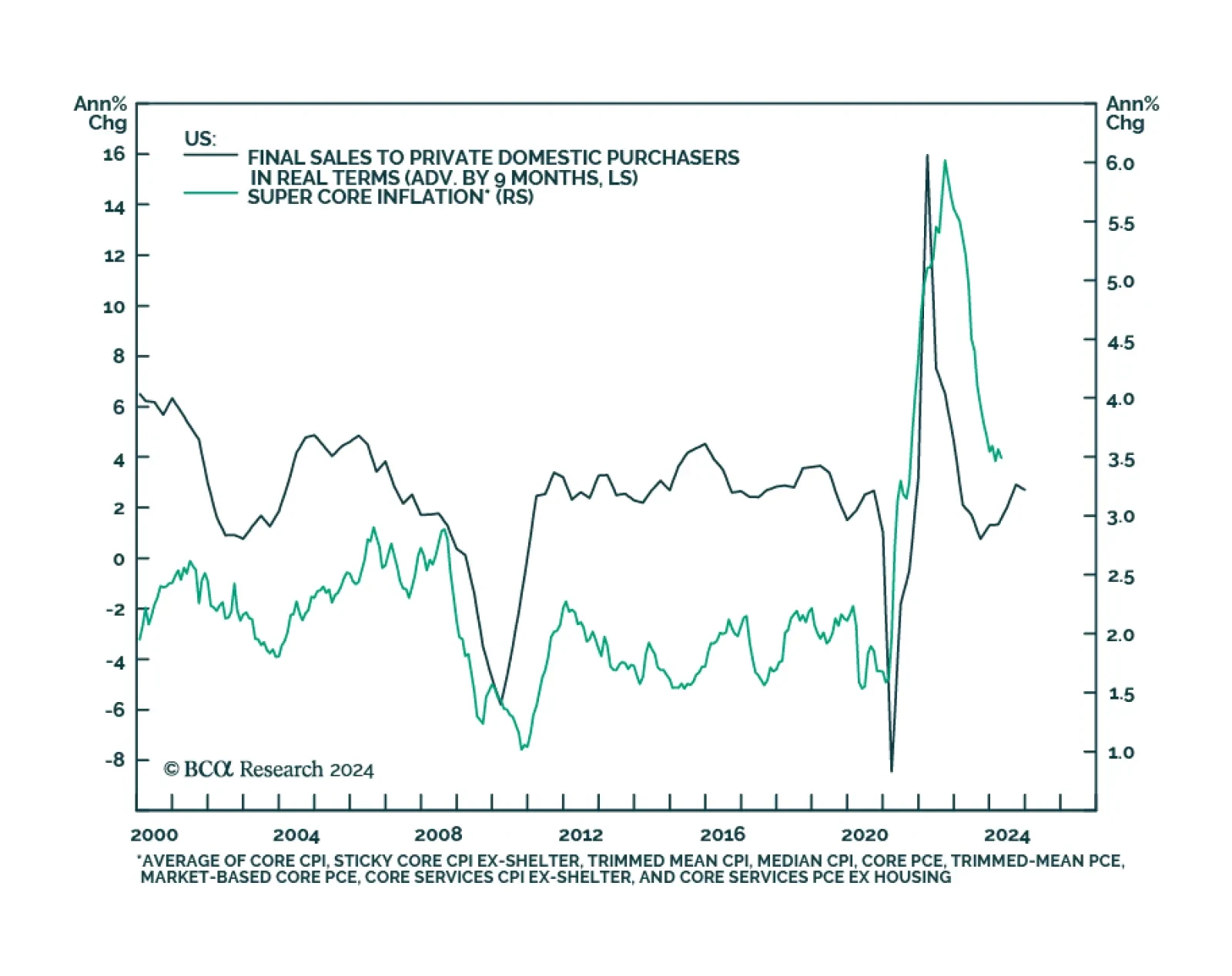

US Q1 GDP was revised lower from 1.6% q/q annualized to 1.3%. Notably, the downward revision to personal consumption was higher than expected, from 2.5% q/q annualized to 2.0%. Investment and government spending were revised higher. Real final sales to…

Euro Area CPI accelerated for the first time this year from 2.4% y/y to a faster-than-expected 2.6% y/y in May. Preliminary estimates also suggest that core CPI accelerated from 2.7% y/y to 2.9% y/y, against expectations of a constant growth rate. …