Inflation/Deflation

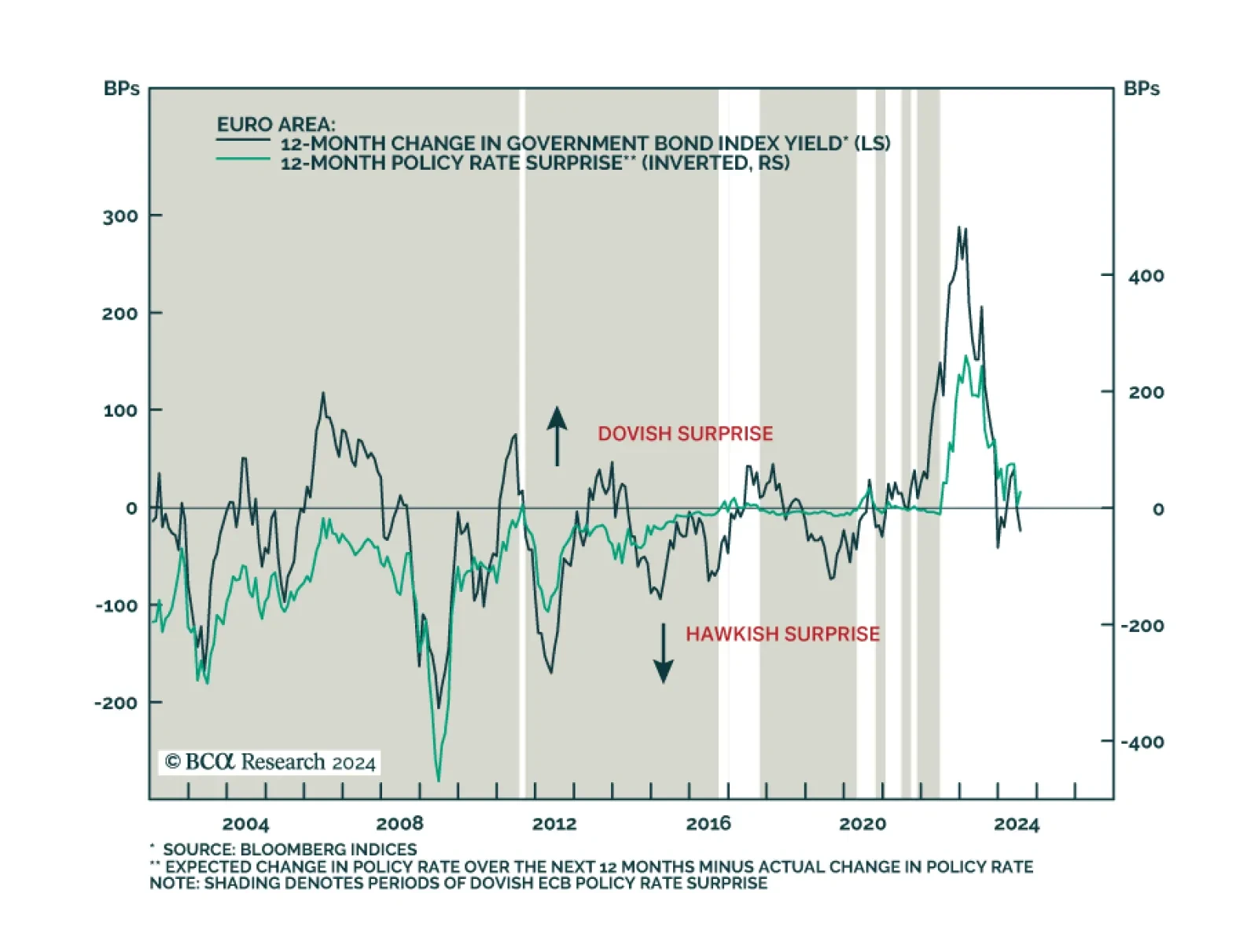

Eurozone headline CPI inflation unexpectedly accelerated in July, from 2.5% y/y to 2.6%. Core CPI remained stable at 2.9% despite expectations it would ease. EU Harmonized CPI accelerated in the regions’ three largest economies, surprising by a large margin…

China’s NBS manufacturing PMI declined further in July, from 49.5 to 49.4, marking a third consecutive month of contraction. New orders and new export orders underscored continued weakness in both domestic and foreign demand conditions. Meanwhile, the NBS…

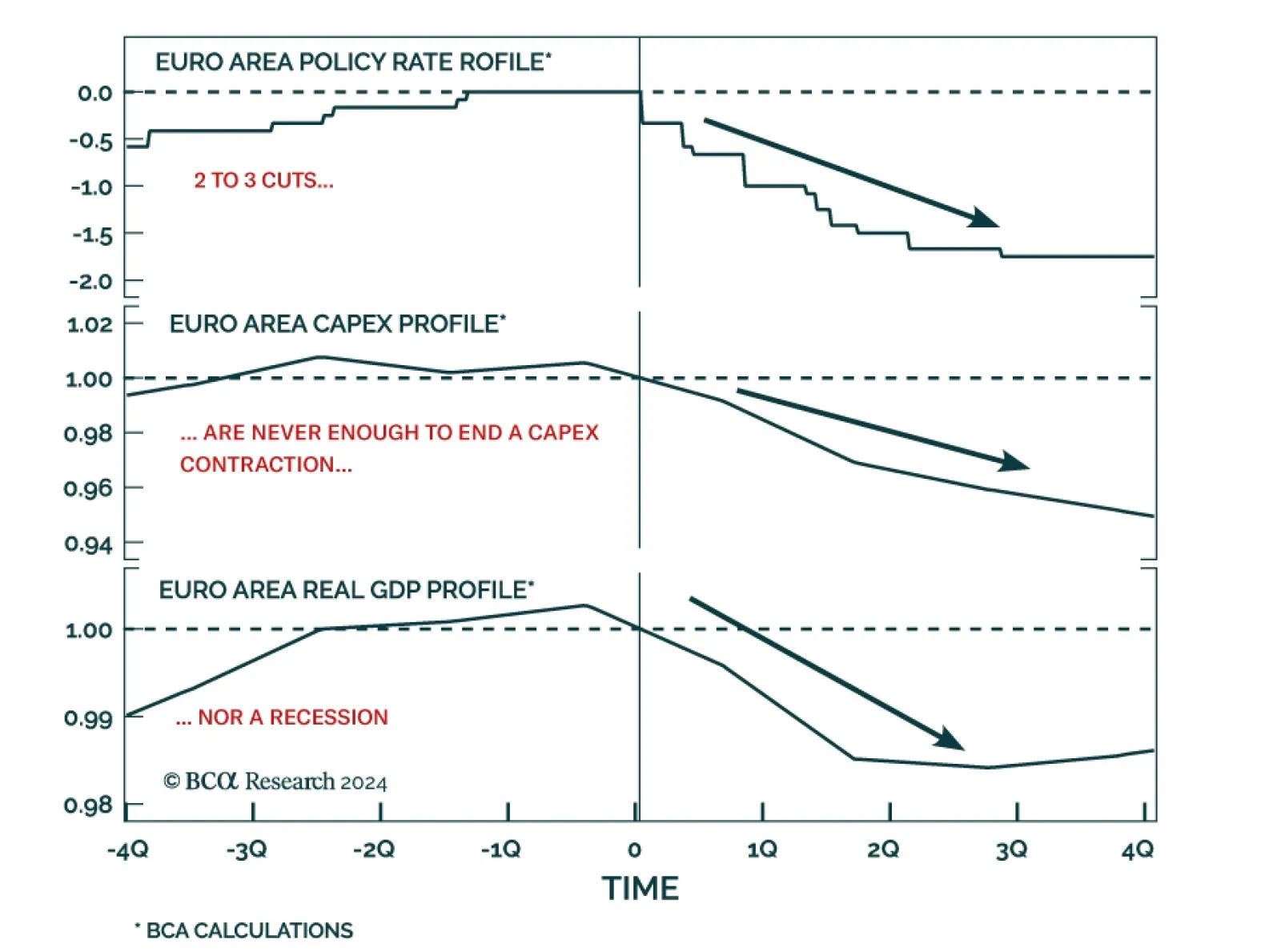

The Fed kept rates steady today, but teed up an initial rate cut in September while putting more emphasis on the employment side of its dual mandate.

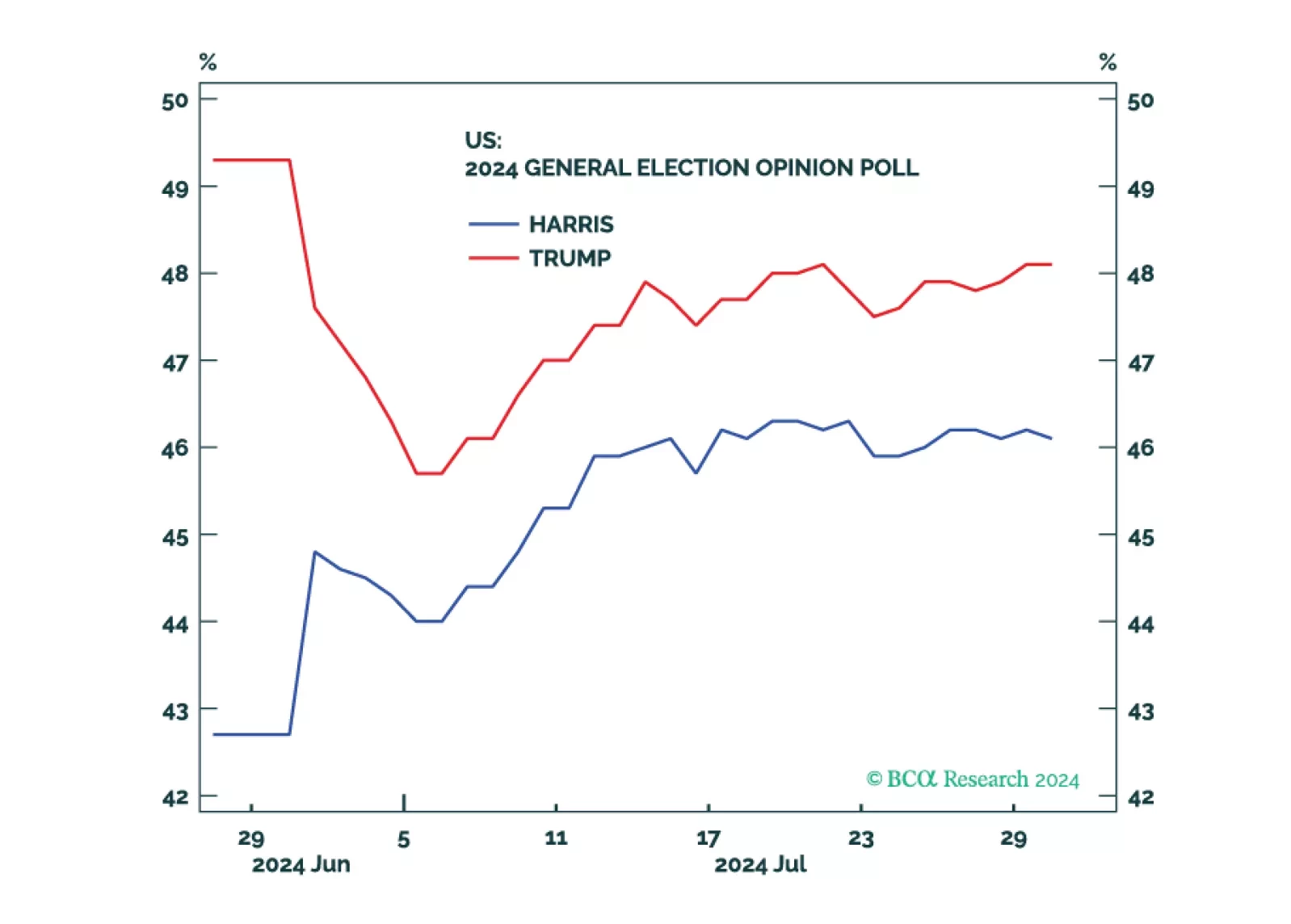

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

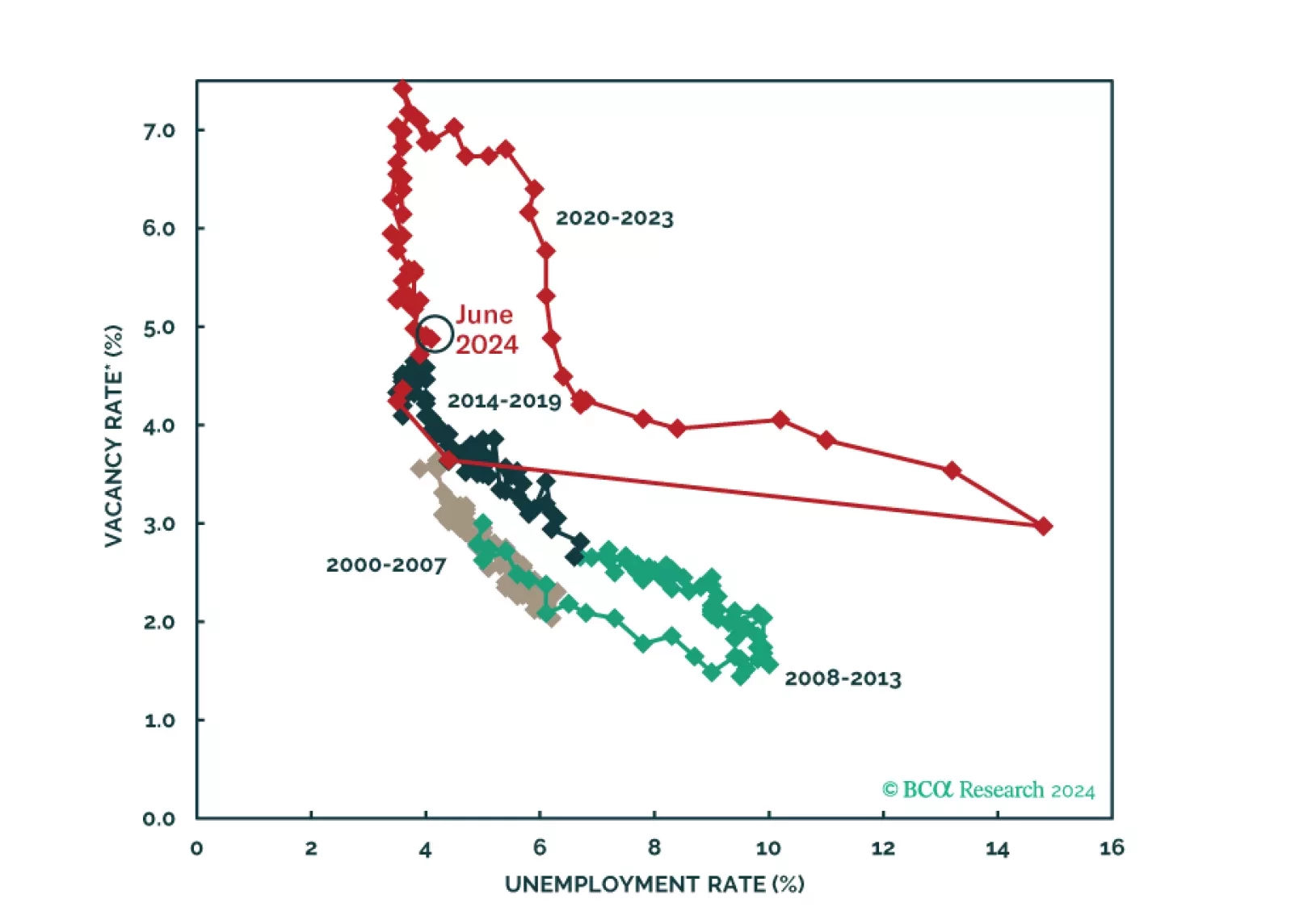

Eurozone GDP surprised to the upside in Q2, growing by 0.3% q/q annualized against expectations of 0.2%. Stronger-than-expected expansions in France (0.3% q/q vs 0.2%) and Spain (0.8% q/q vs 0.5%), as well as steady growth in Italy (0.2% q/q), offset a…

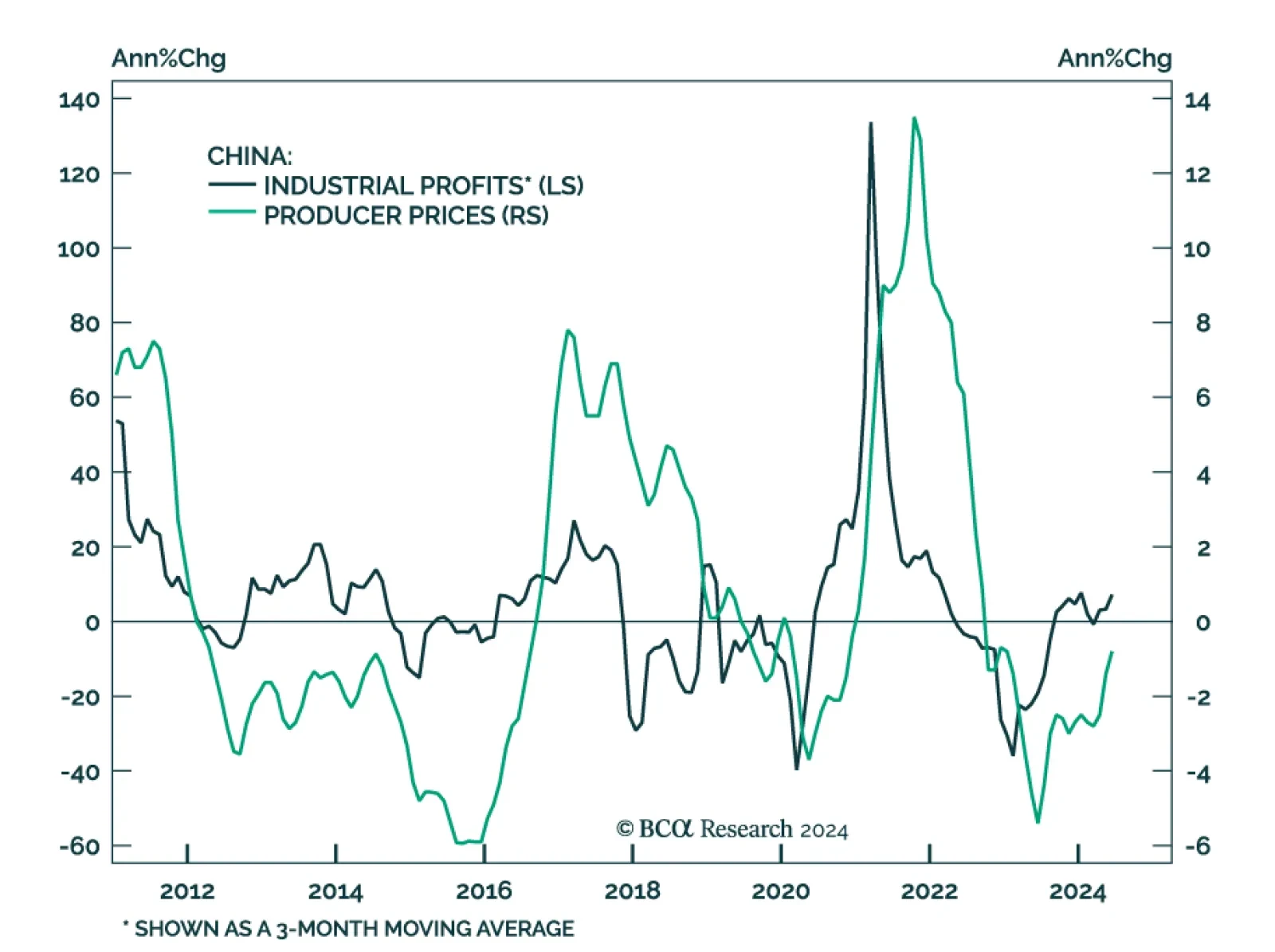

Chinese industrial profits growth accelerated in June, rising from 0.7% y/y to 3.6%. Profits expanded at 3.5% in the first half of 2024, compared to 3.4% in the first half of 2023, and suggest that China’s manufacturing sector remains resilient. A slower…

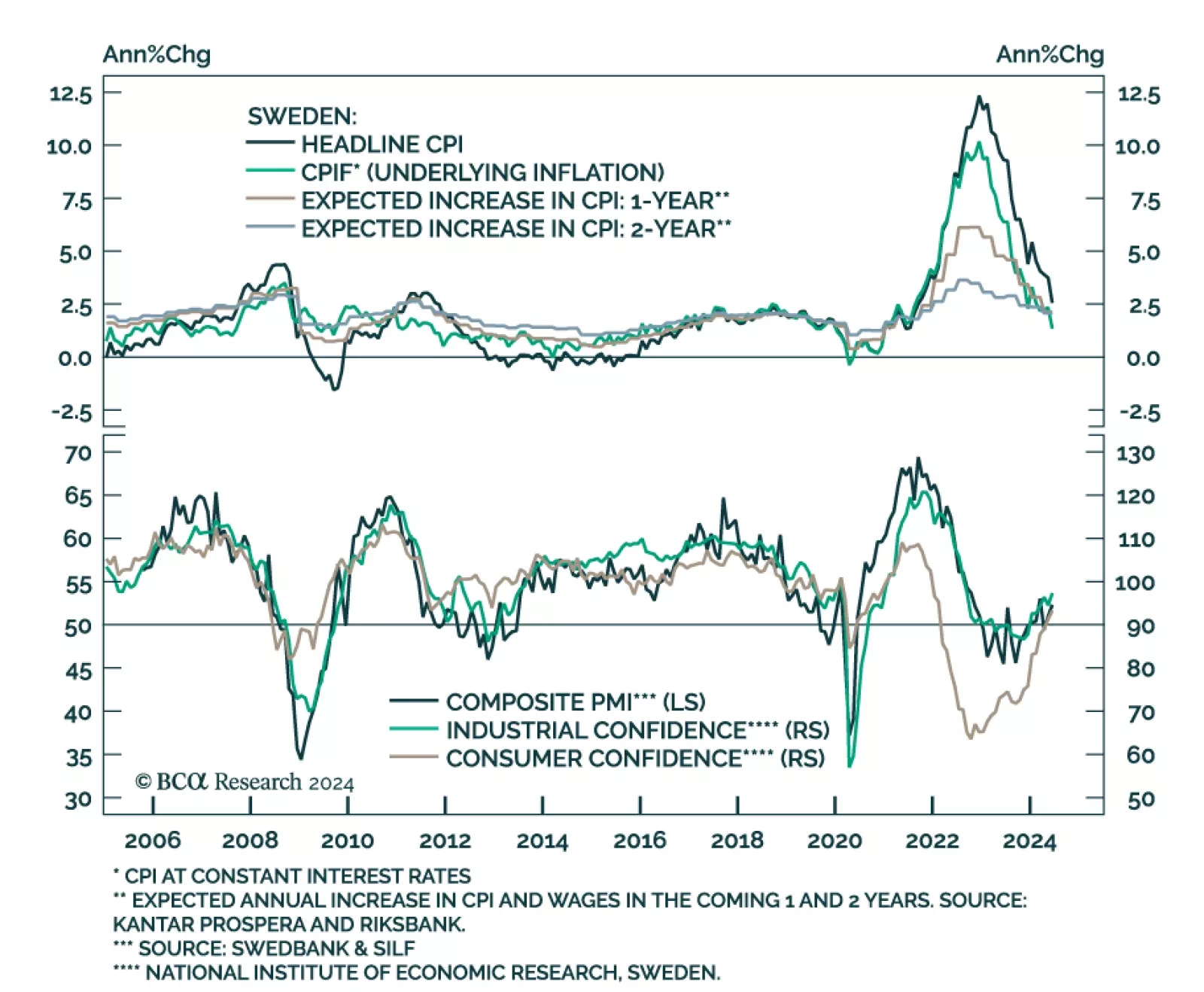

Preliminary estimates suggests that the Swedish economy unexpectedly contracted in Q2. The seasonally adjusted GDP Indicator declined by 0.8% q/q, following a 0.7% Q1 rise in actual GDP growth. Flash estimates lack details and are prone to revisions.…

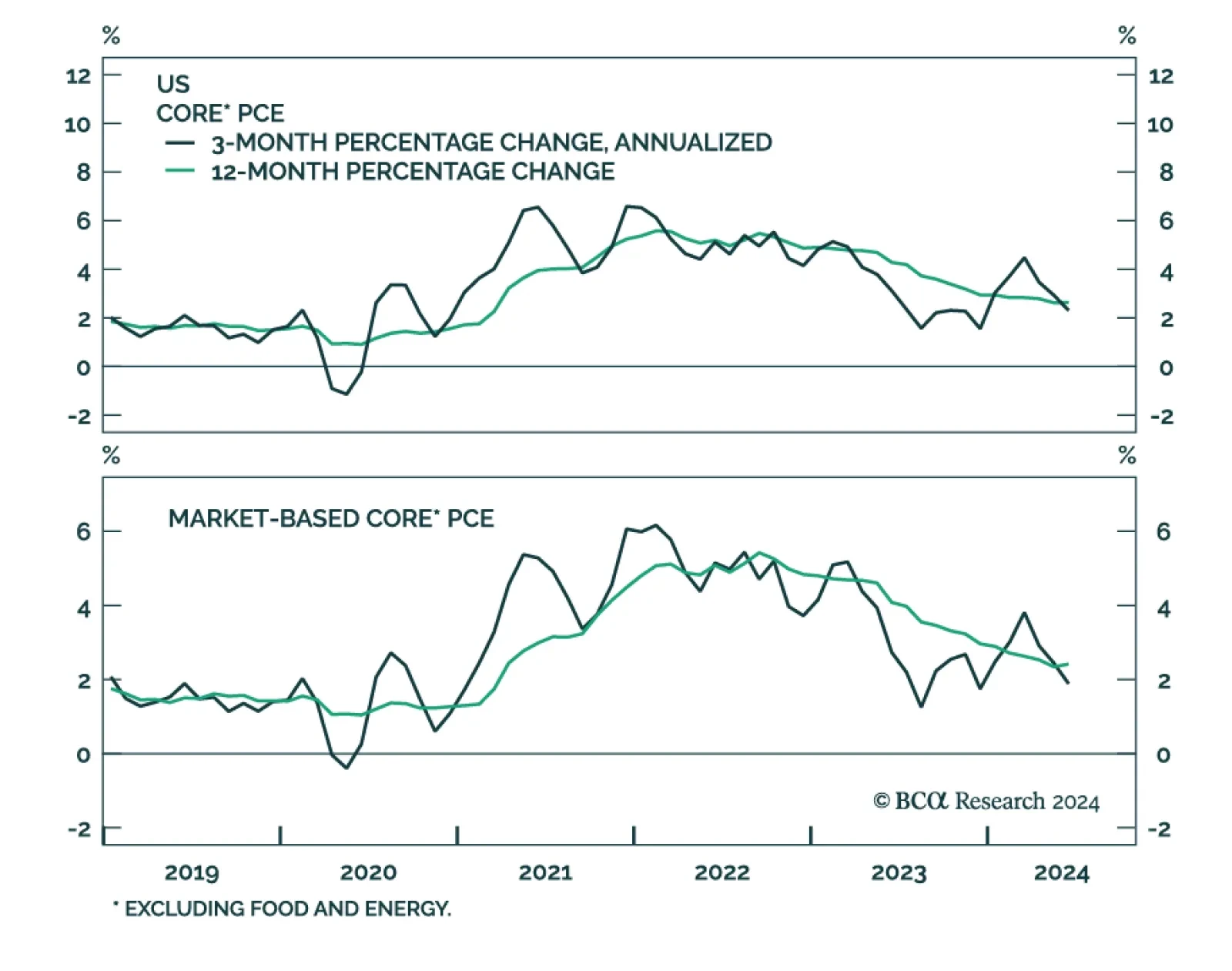

US nominal personal income growth and real personal spending decelerated at a faster-than-expected pace in June, both moderating to 0.2% m/m from 0.4% in May. Core PCE – the Fed’s favored inflation gauge – remained unchanged, growing at 2.6% y/y. Notably,…

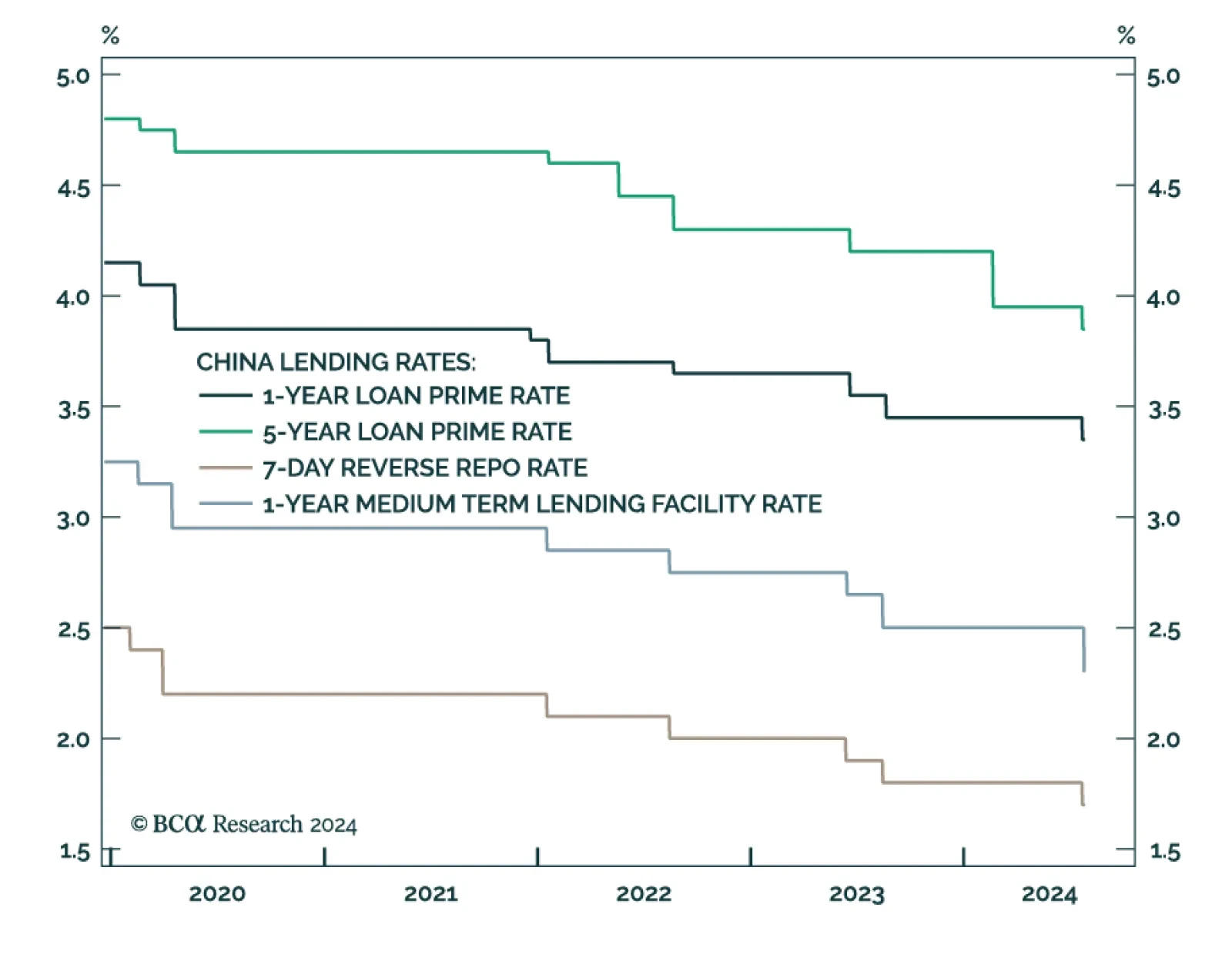

Just a few days after unexpectedly lowering three key borrowing rates by 10 basis points (bps), the PBoC cut the 1-year medium-term lending facility rate by 20 bps, from 2.50% to 2.30%. While the earlier cut lowered the interest rate charged by commercial…

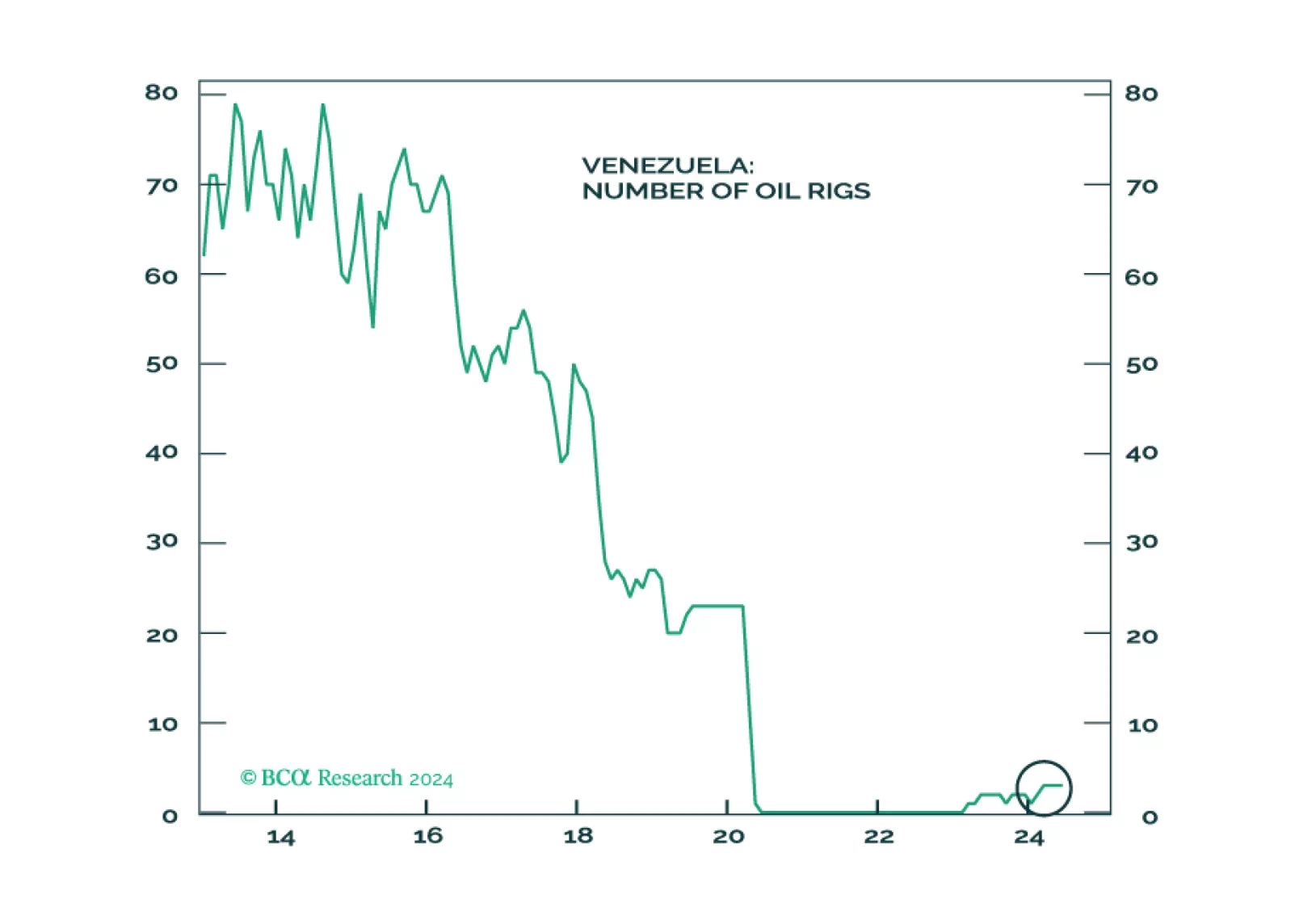

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.