Inflation/Deflation

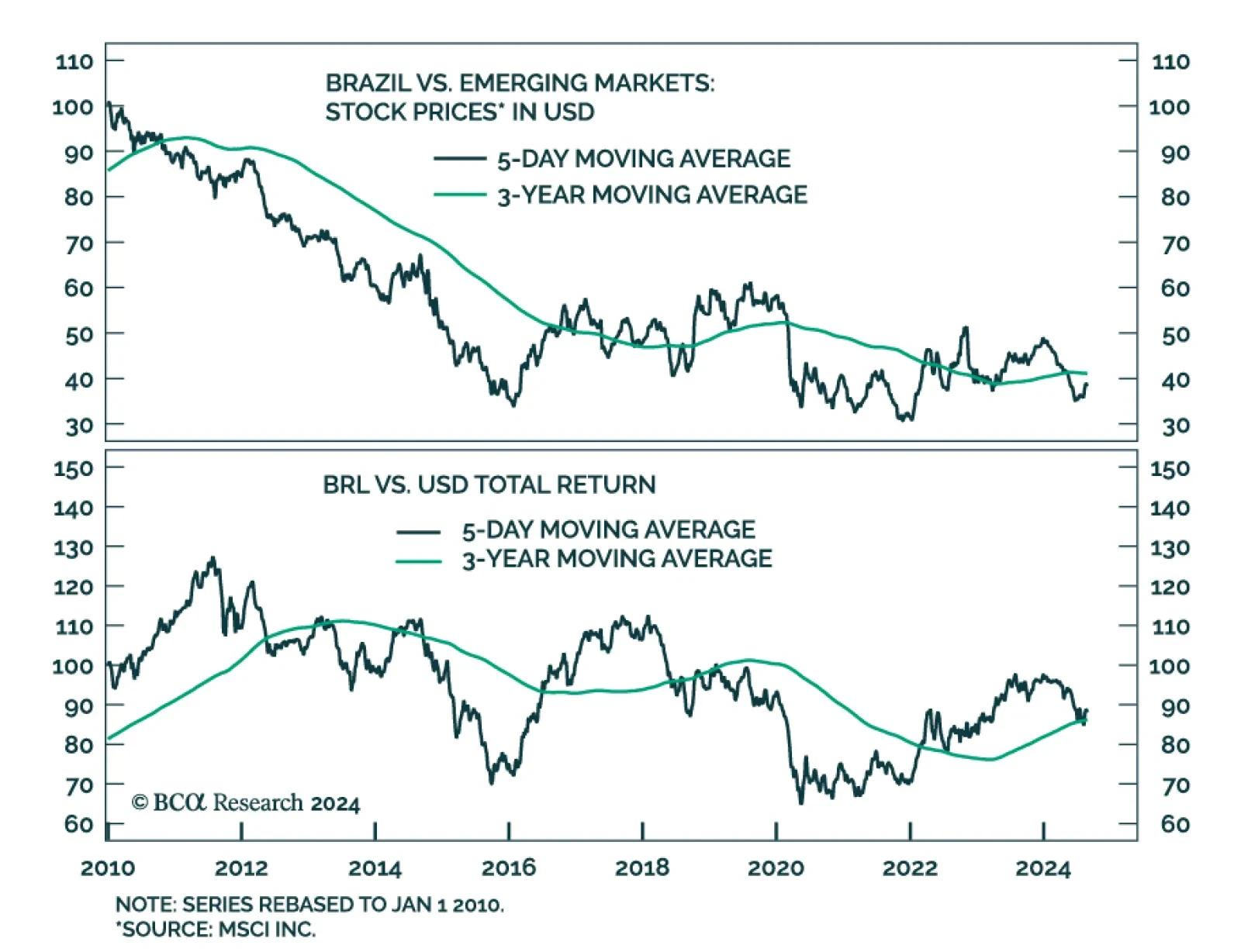

Brazilian equities have largely underperformed their EM peers in USD terms since the beginning of the year. Rising public debt and inflation are the two main forces weighing on the Brazilian bourse. Our Emerging Market strategists expect public debt-to-GDP…

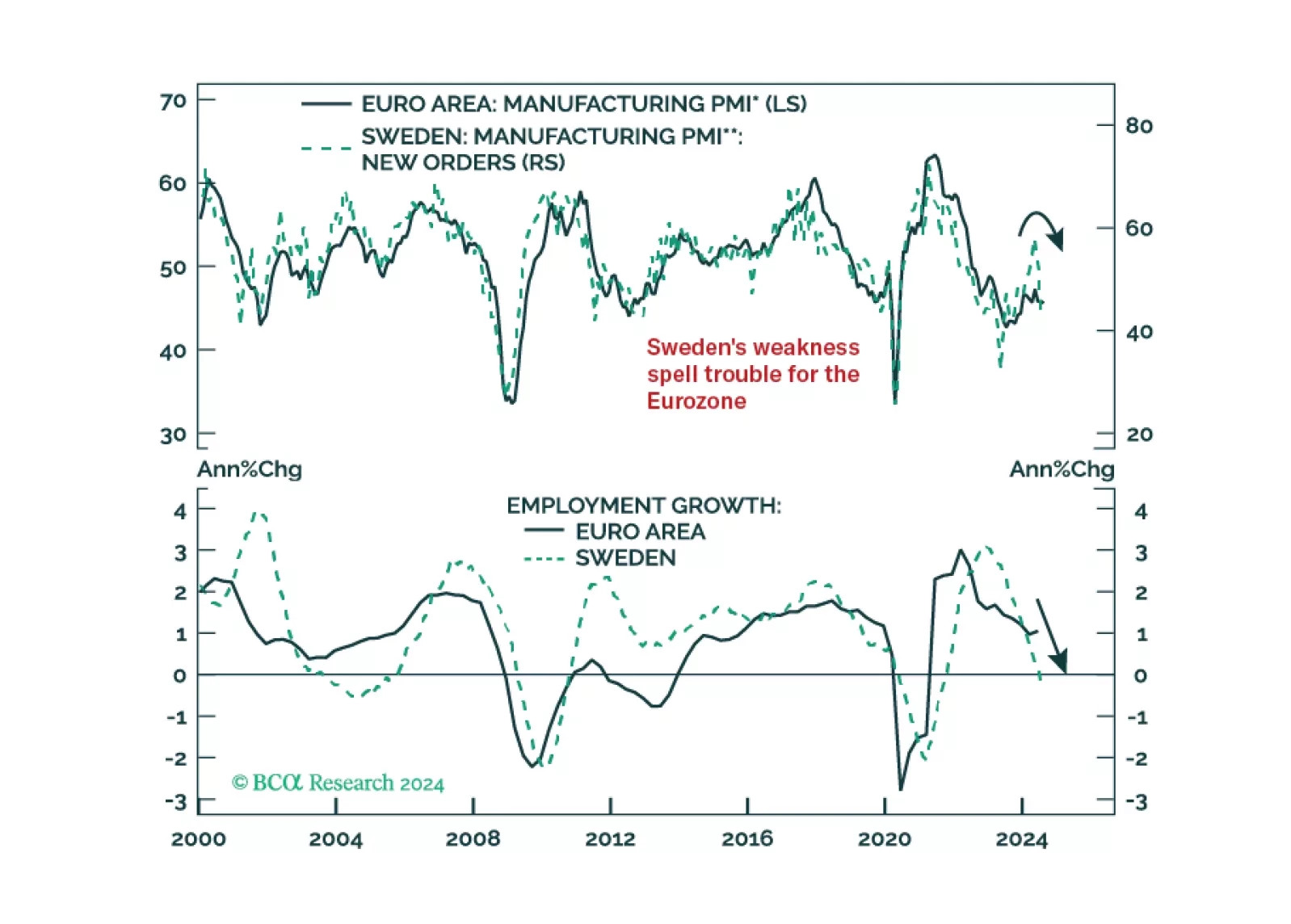

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

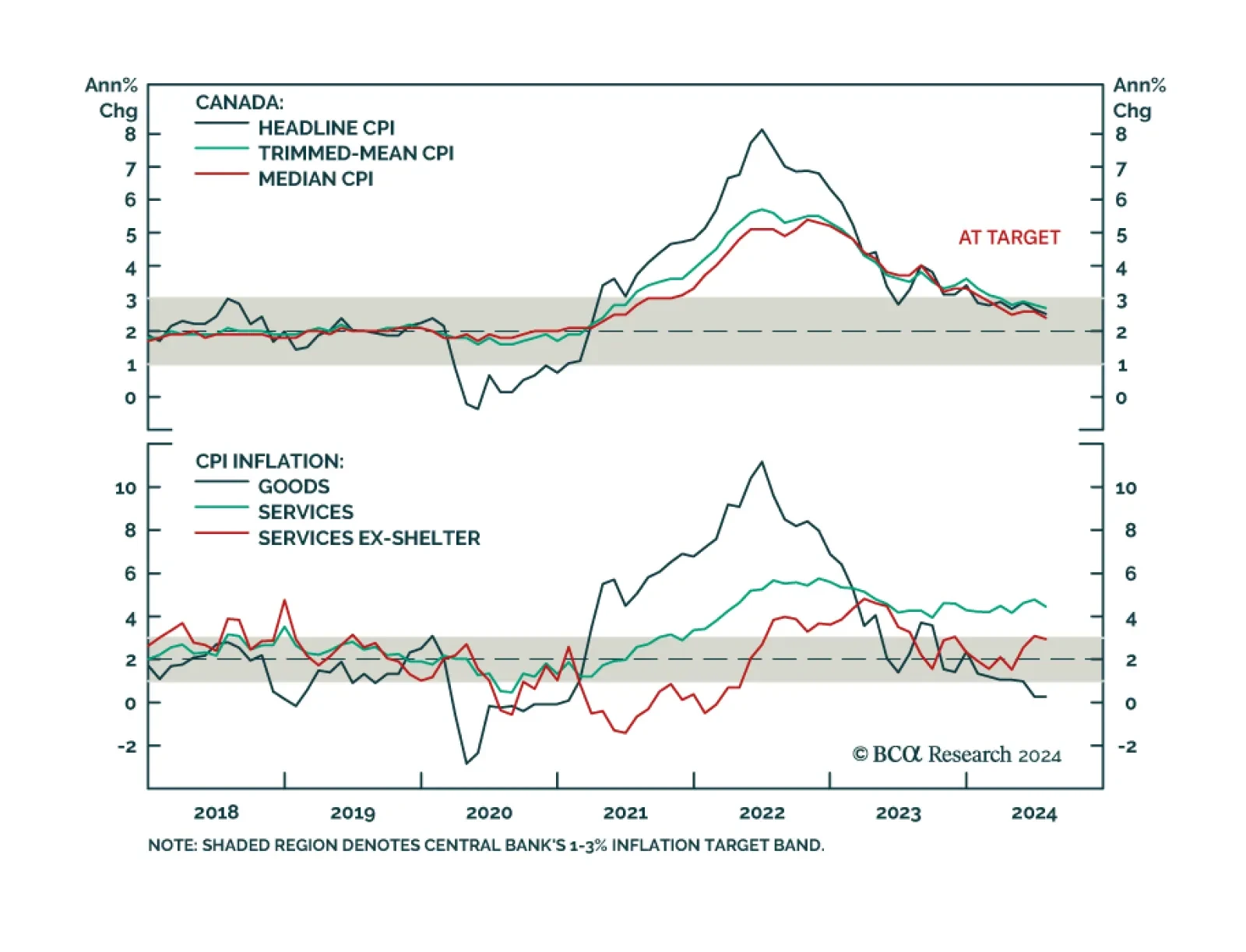

Canadian headline CPI decelerated from 2.7% y/y to 2.5% in July, the slowest pace in over 3 years. Notably, core median and trimmed-mean CPI eased further than expected, to 2.4% and 2.7% y/y respectively, 0.1 ppt below anticipations. Lower prices for…

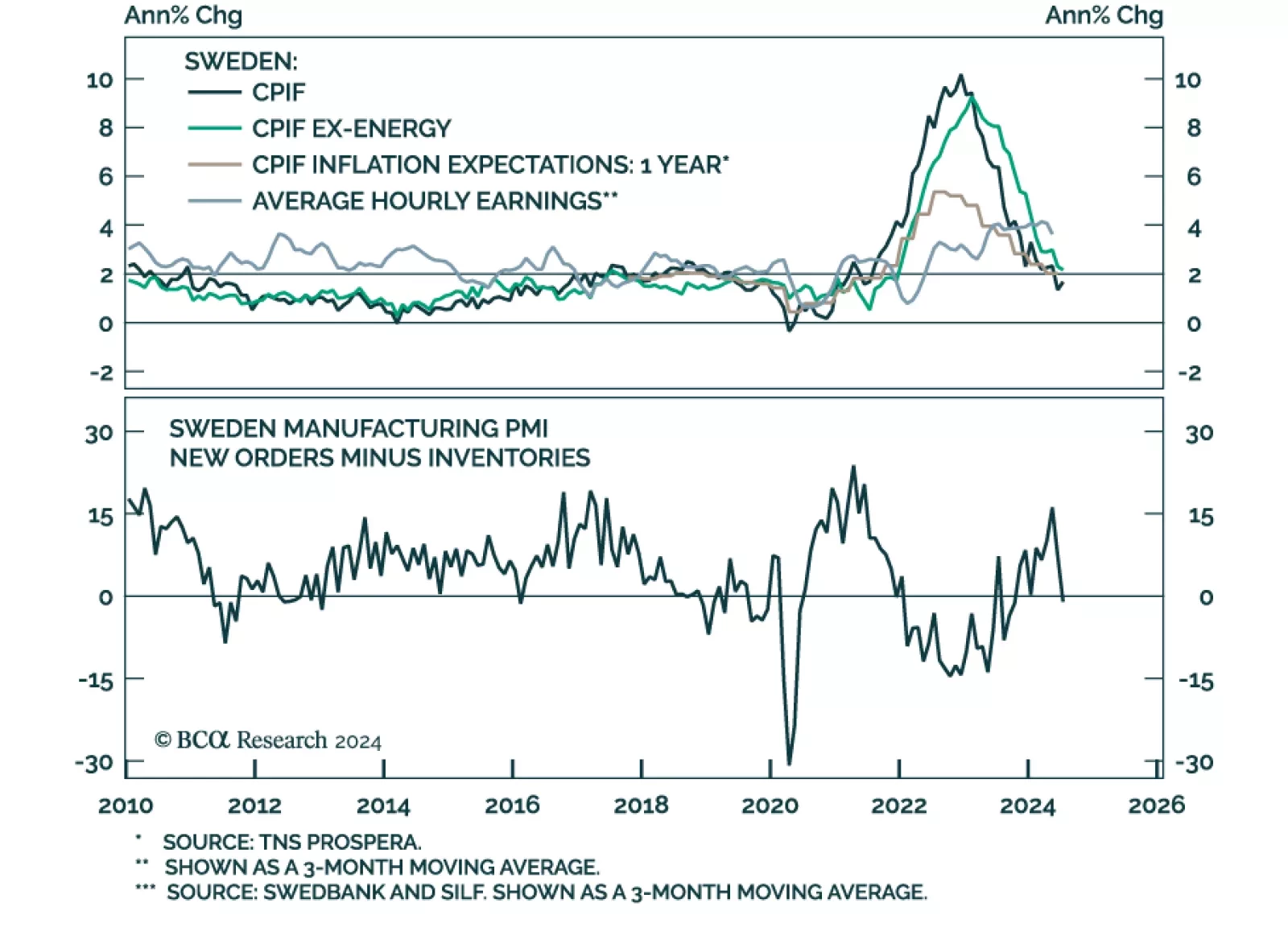

In a widely expected move, the Riksbank lowered its policy rate from 3.75% to 3.5% in August. It had kept rates on hold in June, after having led many other major DM central banks in easing policy in May. The Riksbank also signaled it could cut as many as…

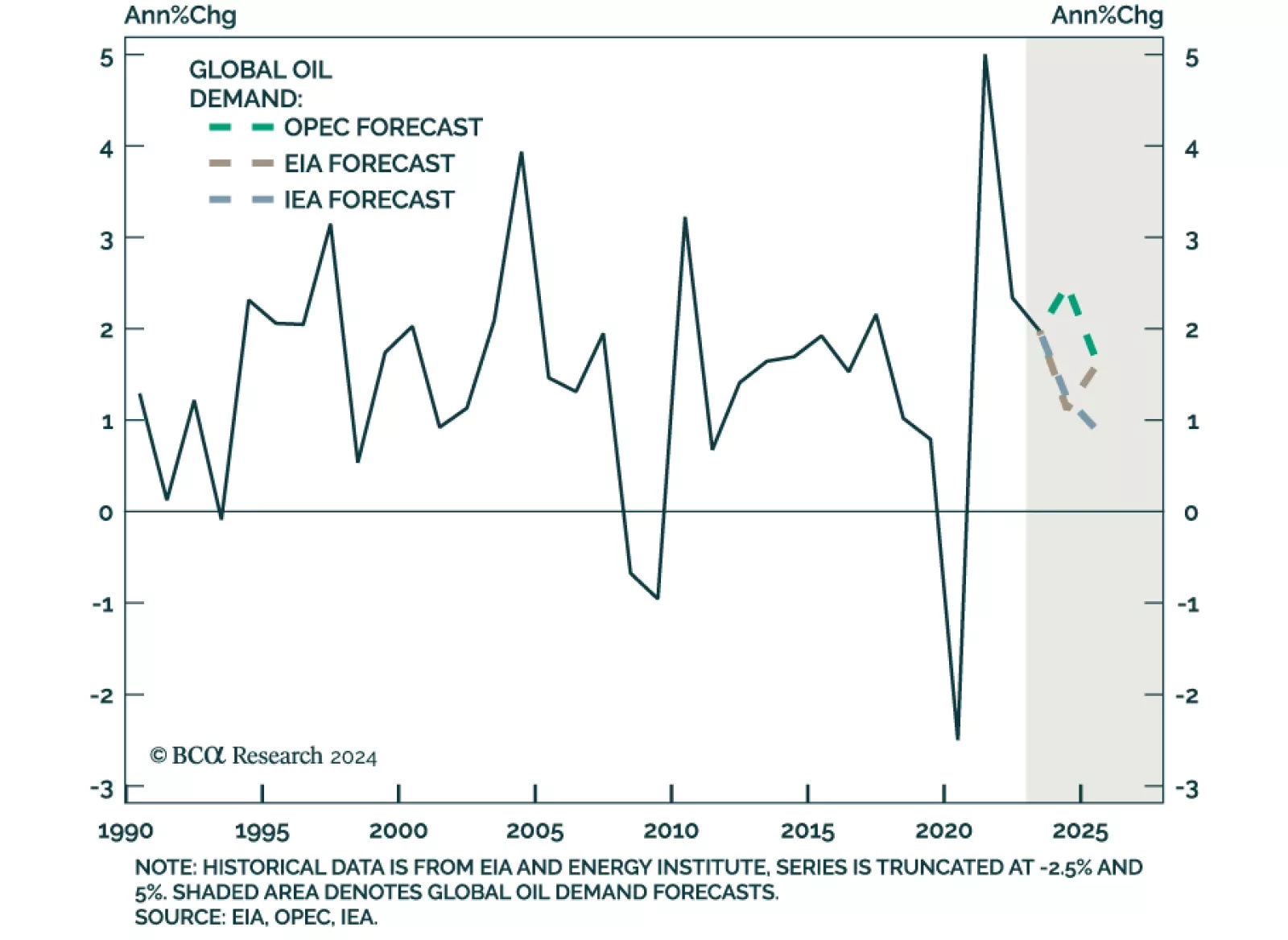

Back in May, our Commodity and Energy strategists argued that OPEC, EIA, and IEA oil demand forecasts were likely too optimistic. Indeed, while all three major oil price forecasters projected a moderation in demand this year, none of them anticipated weak…

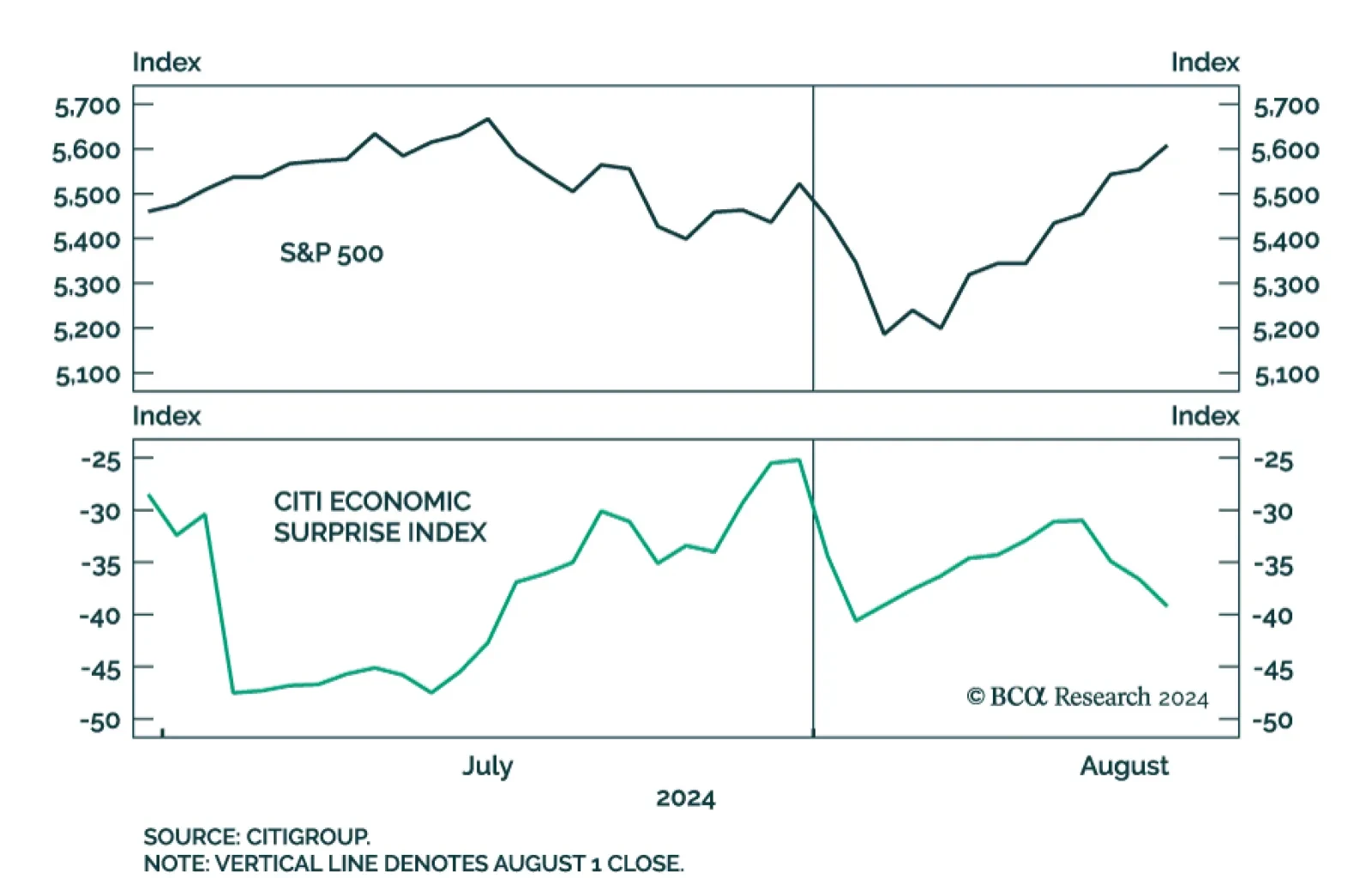

It didn't take long for markets to utterly shrug off the surprise rise in July's unemployment rate. On Tuesday, the S&P 500 closed higher than it was the day before the July Employment Situation report was released. The Russell 2000 gained 5.2% since…

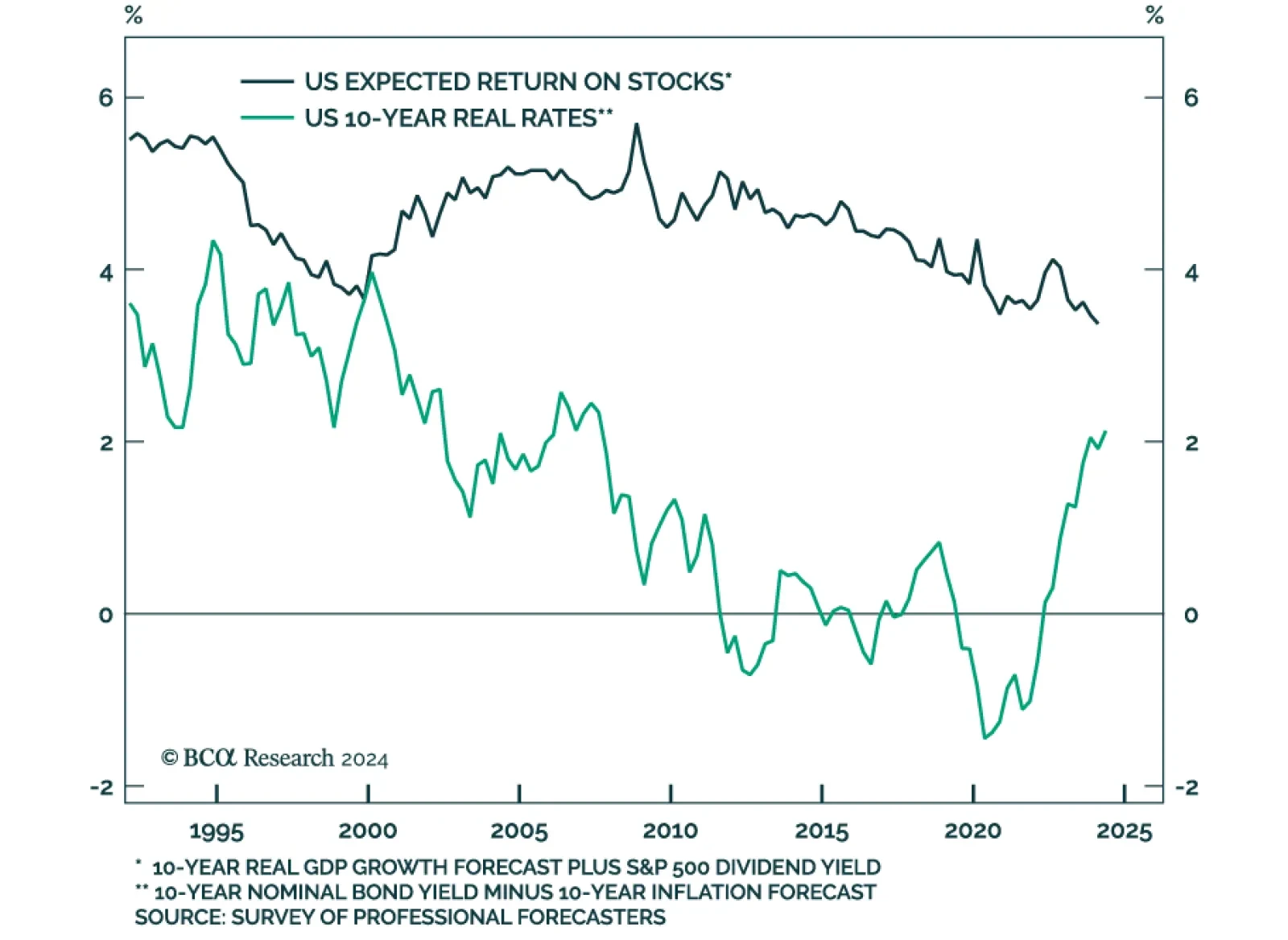

According to BCA Research’s US Investment Strategy and US Bond Strategy services, the drivers of the structural downtrend in real interest rates include: demographic trends (declining fertility rates, longer life expectancy and a rising dependency…

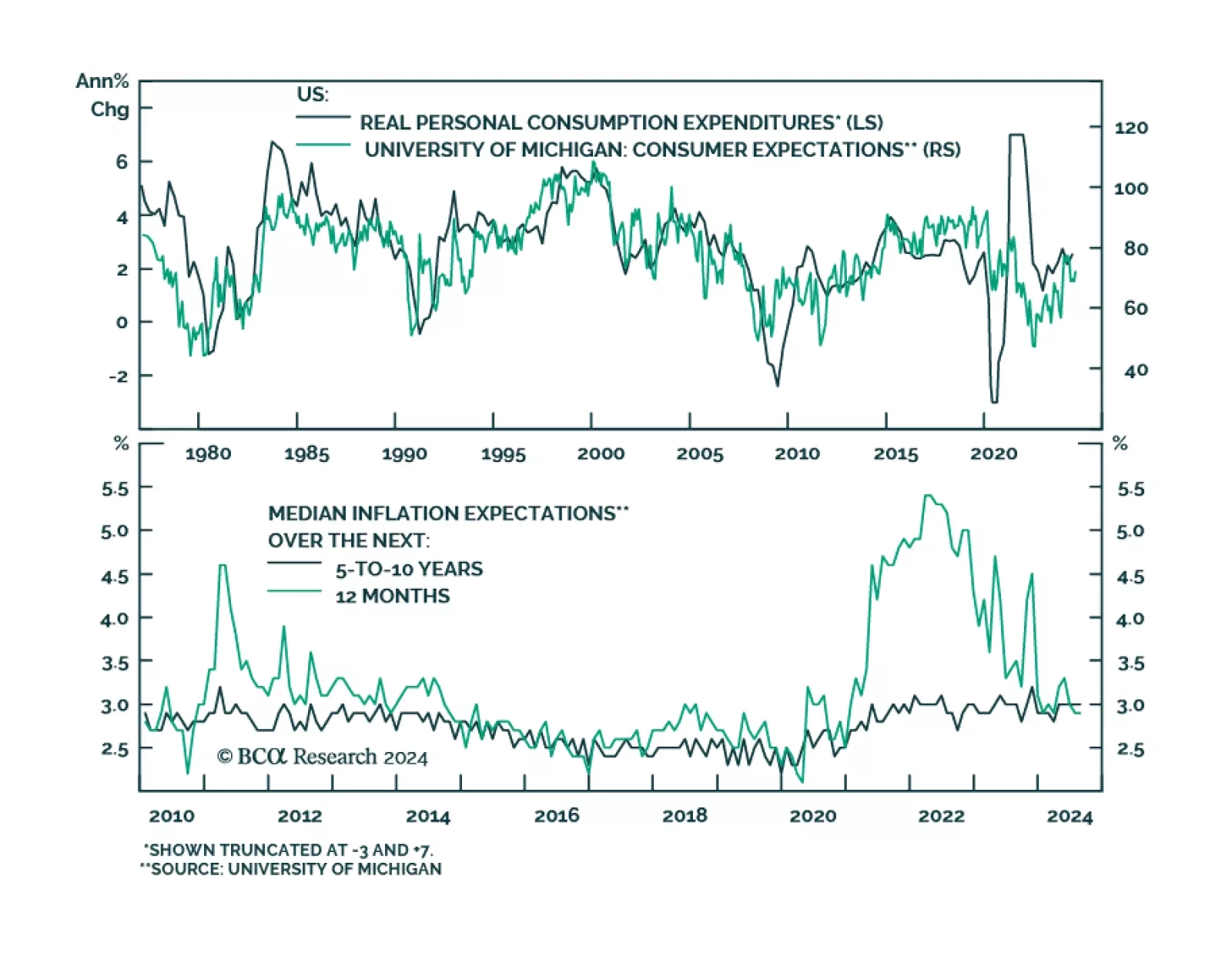

Preliminary estimates suggest that although consumers’ perceptions of current economic conditions unexpectedly deteriorated in August, they are becoming increasingly optimistic about the future. The University of Michigan current conditions gauge dropped…

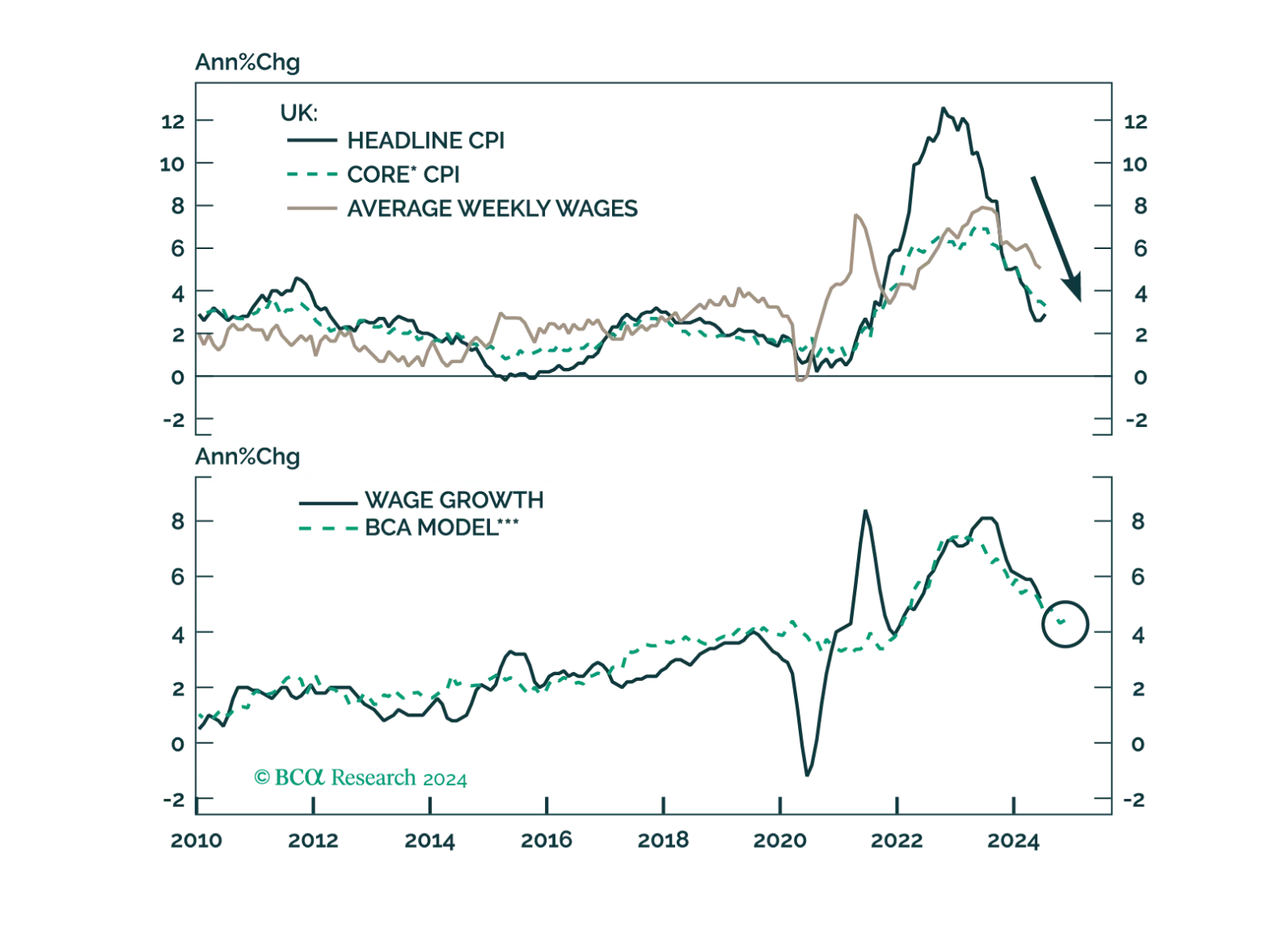

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

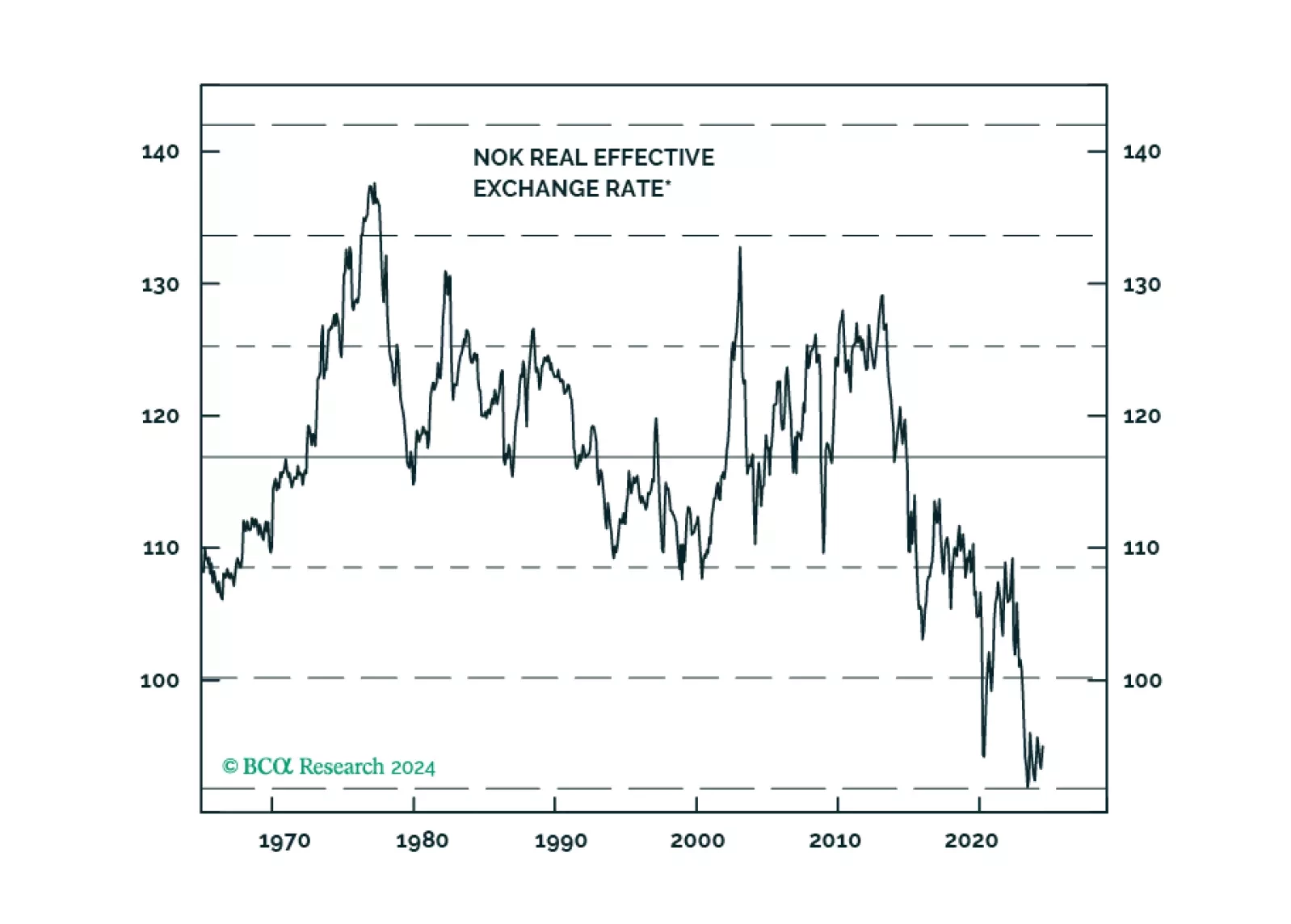

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.