Inflation/Deflation

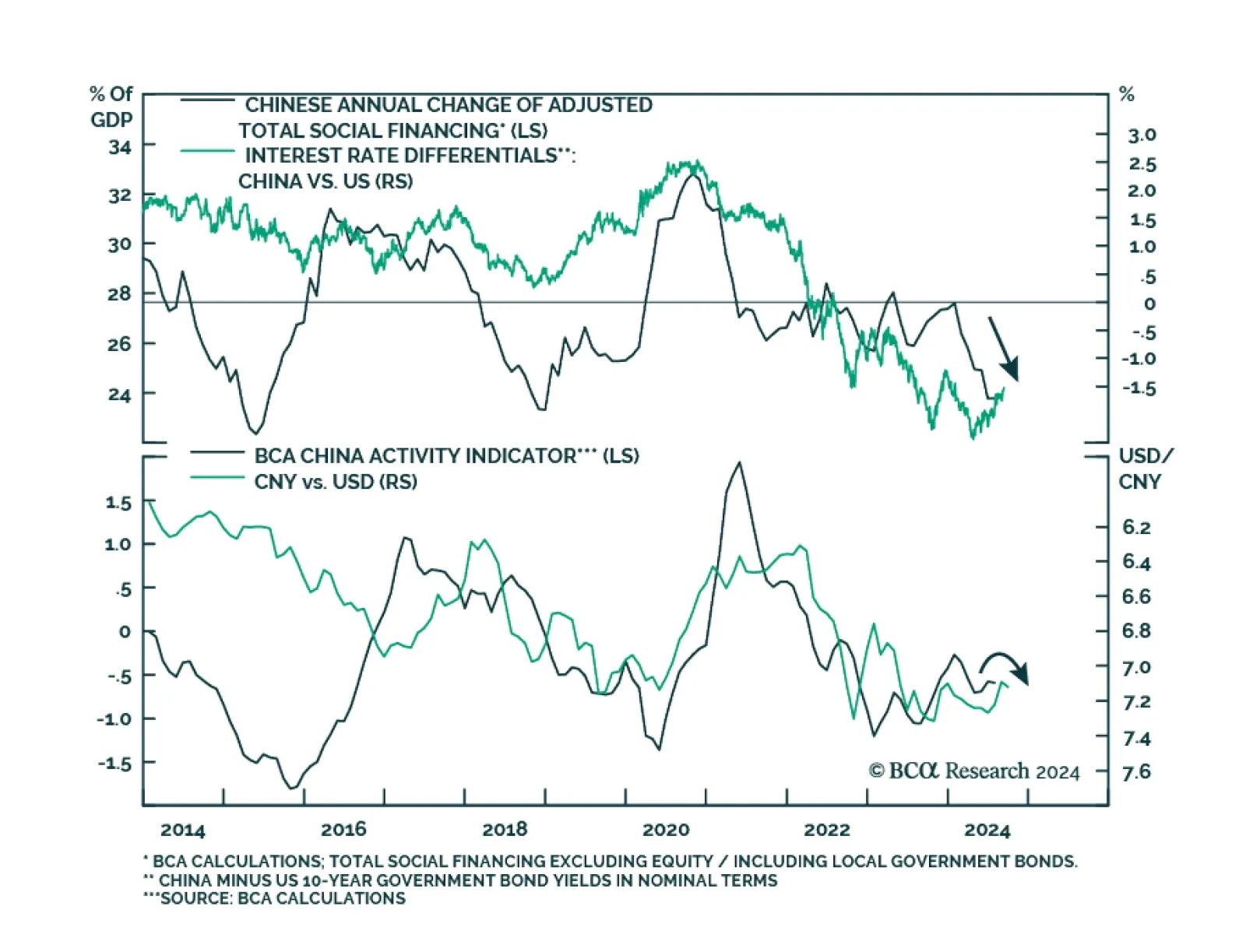

According to BCA Research’s China Investment Strategy service, the Fed’s upcoming rate cut will temporarily alleviate some of the downward pressure on the RMB, but beyond the short term the USD will likely rebound in anticipation of a global slowdown. The…

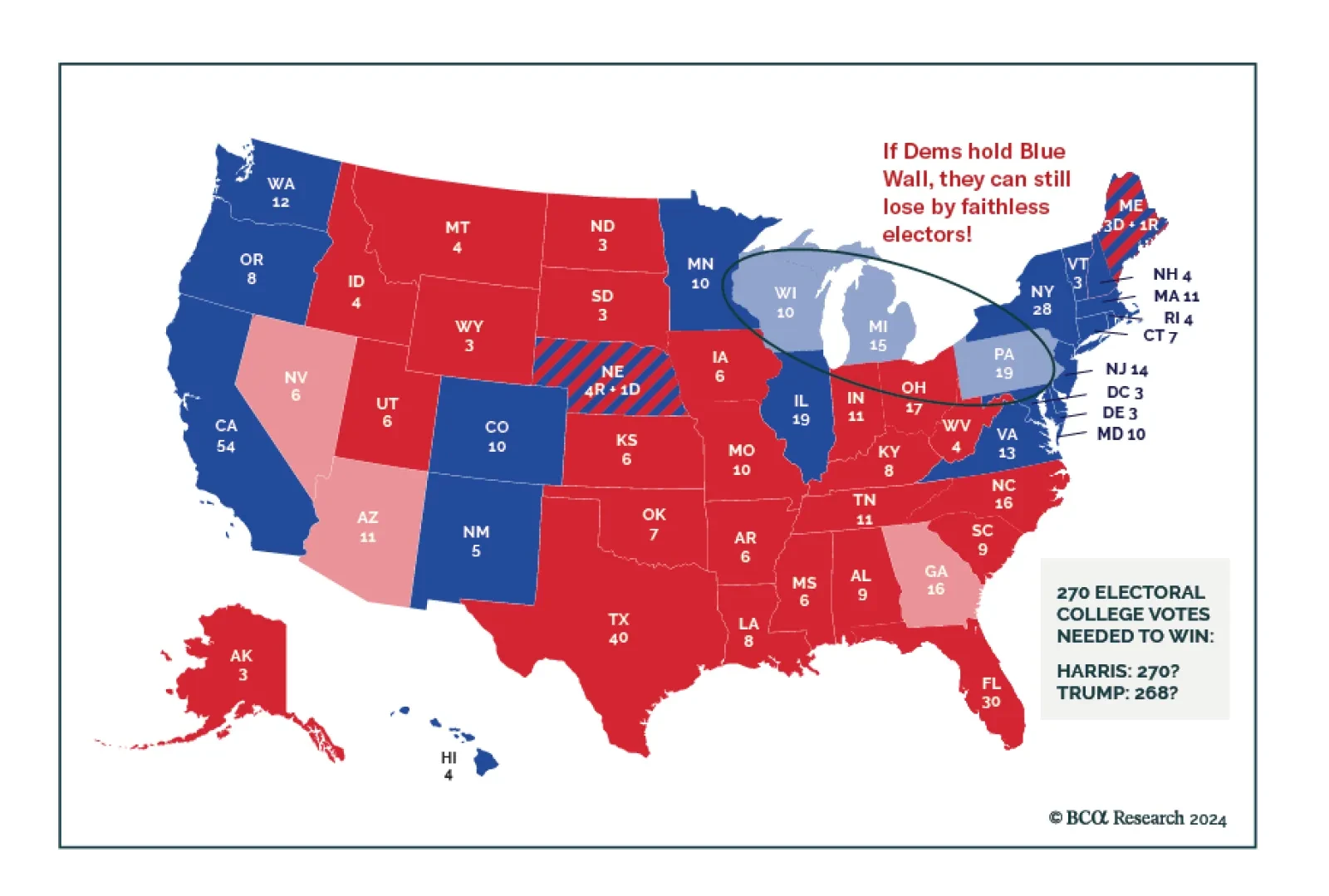

According to BCA Research’s US Political Strategy service, former President Trump still has a path to come back to power, despite his disastrous performance in the debate with Vice President Kamala Harris on September 10. A cascade of shifting opinion…

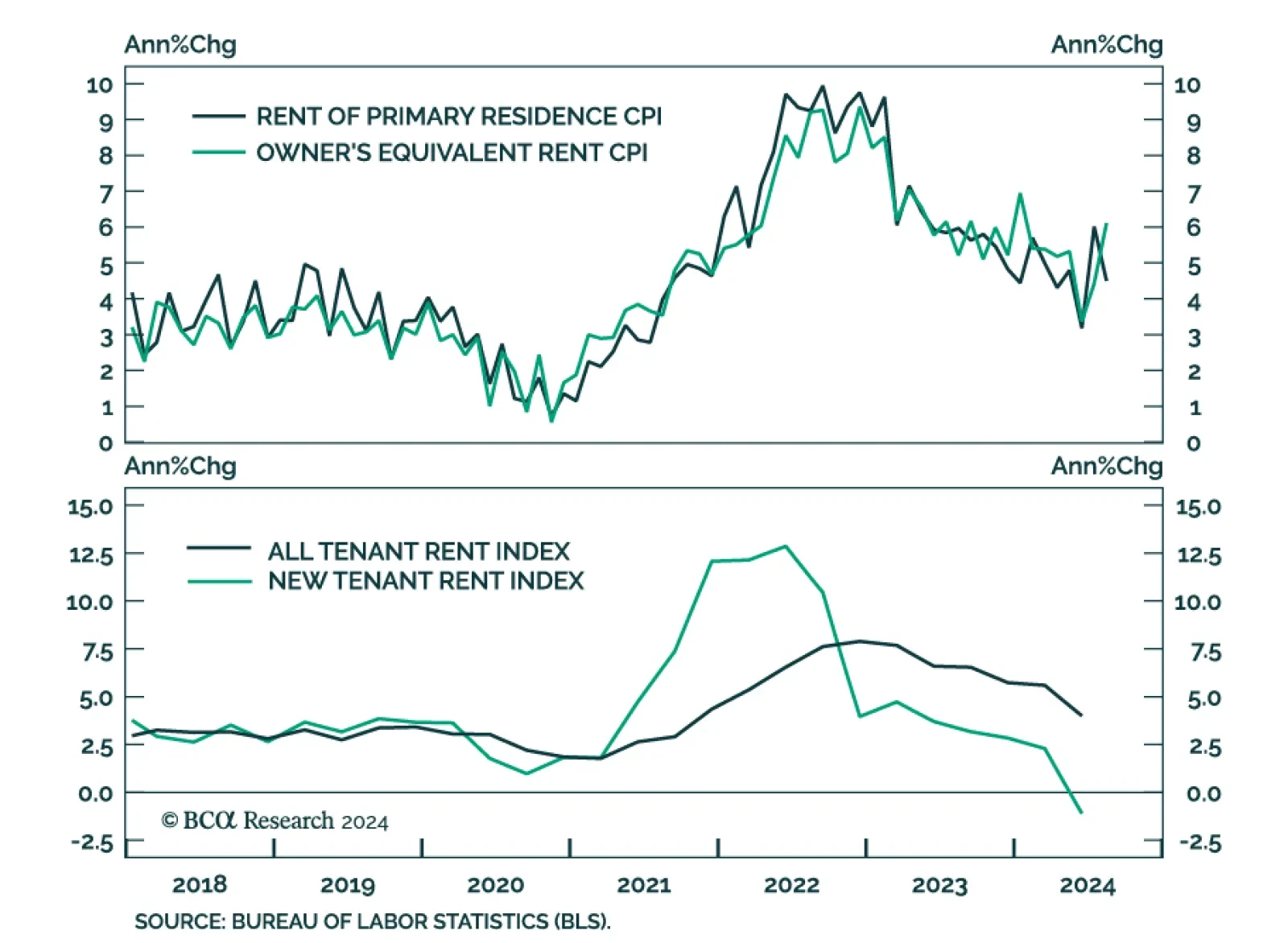

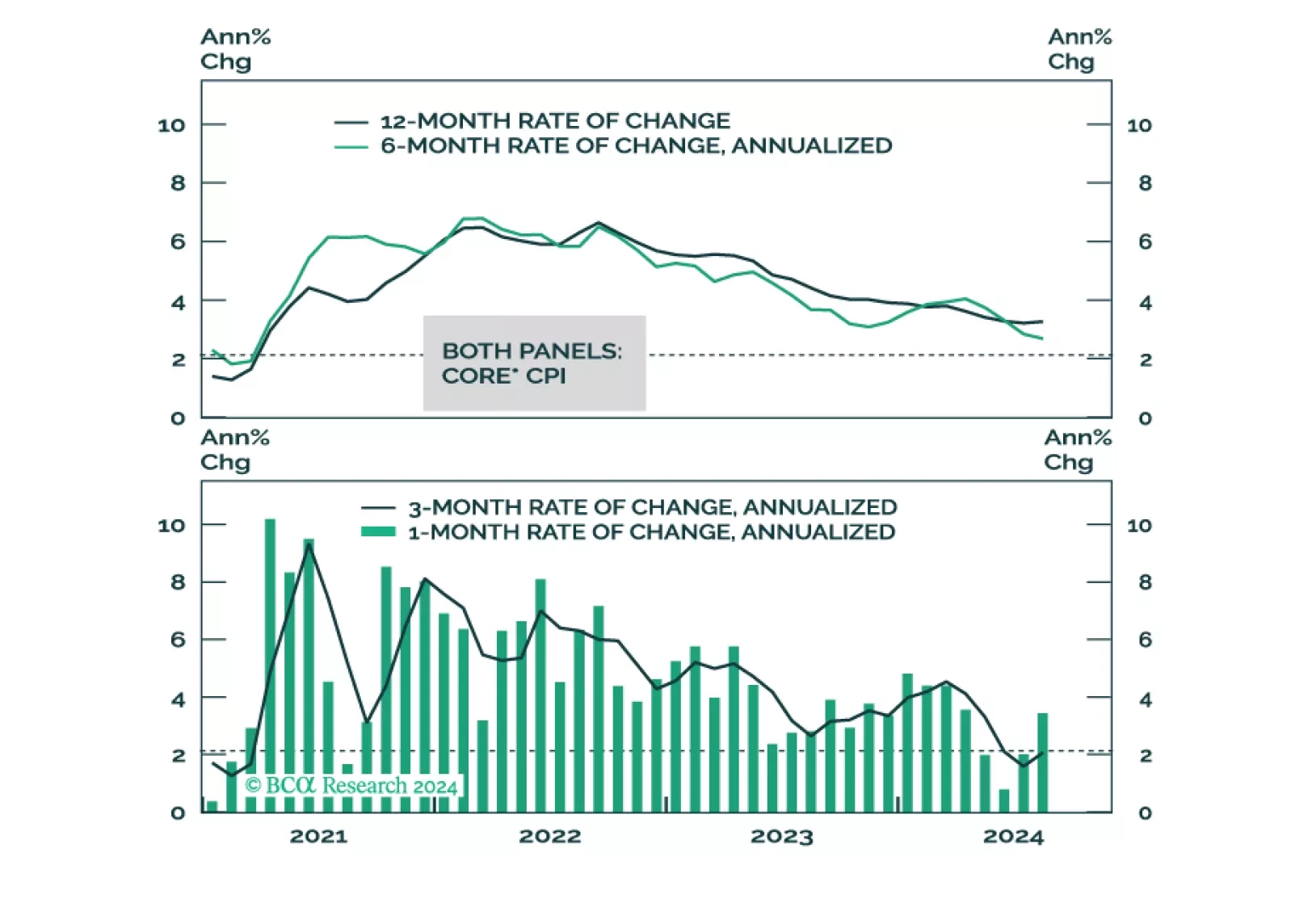

US headline CPI eased from 2.9% y/y to 2.5% in August in line with consensus predictions. However, core CPI unexpectedly accelerated from 0.2% m/m to 0.3%. Aside from airfares -- a highly volatile series which is likely to reverse in coming months given…

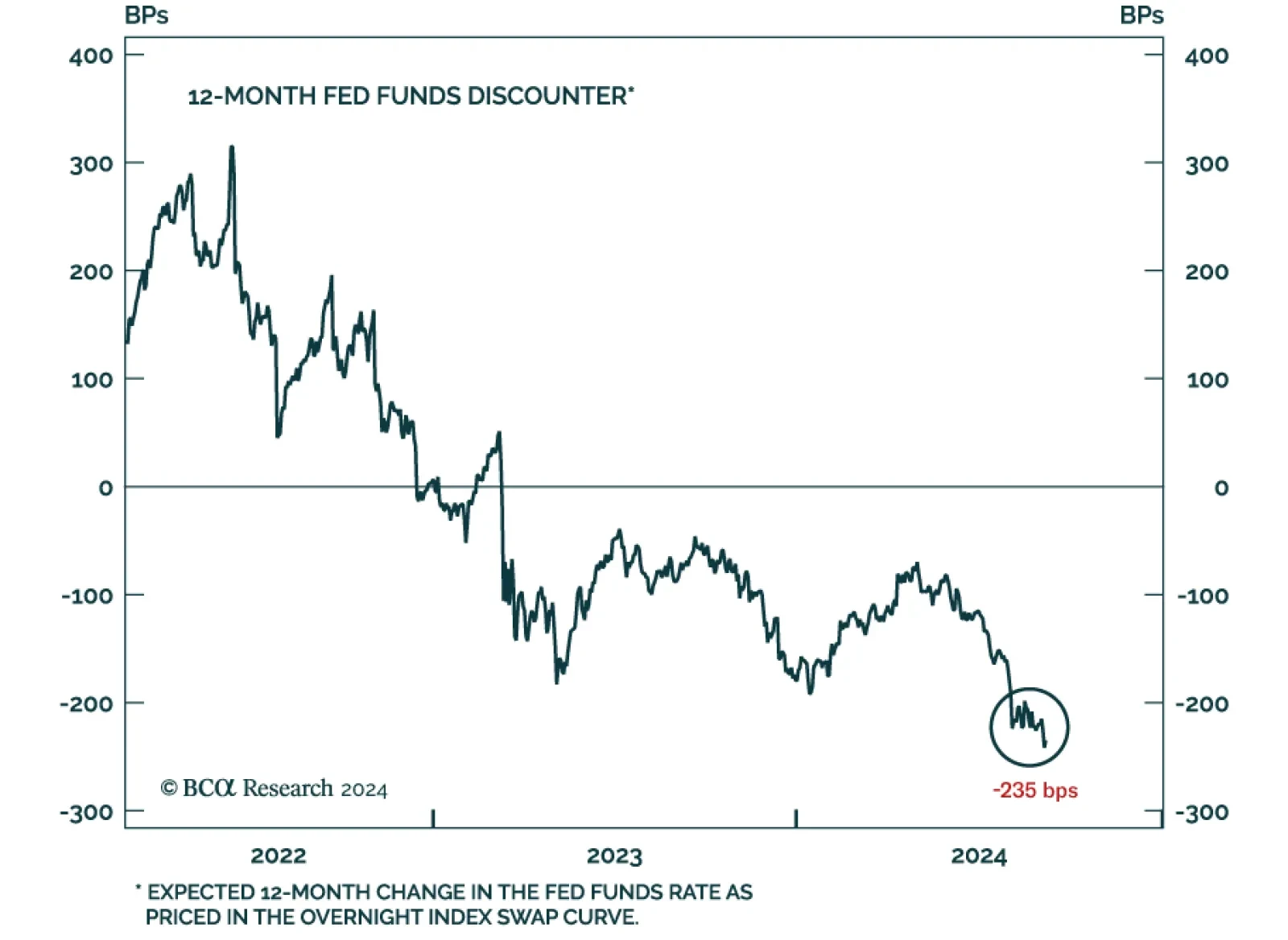

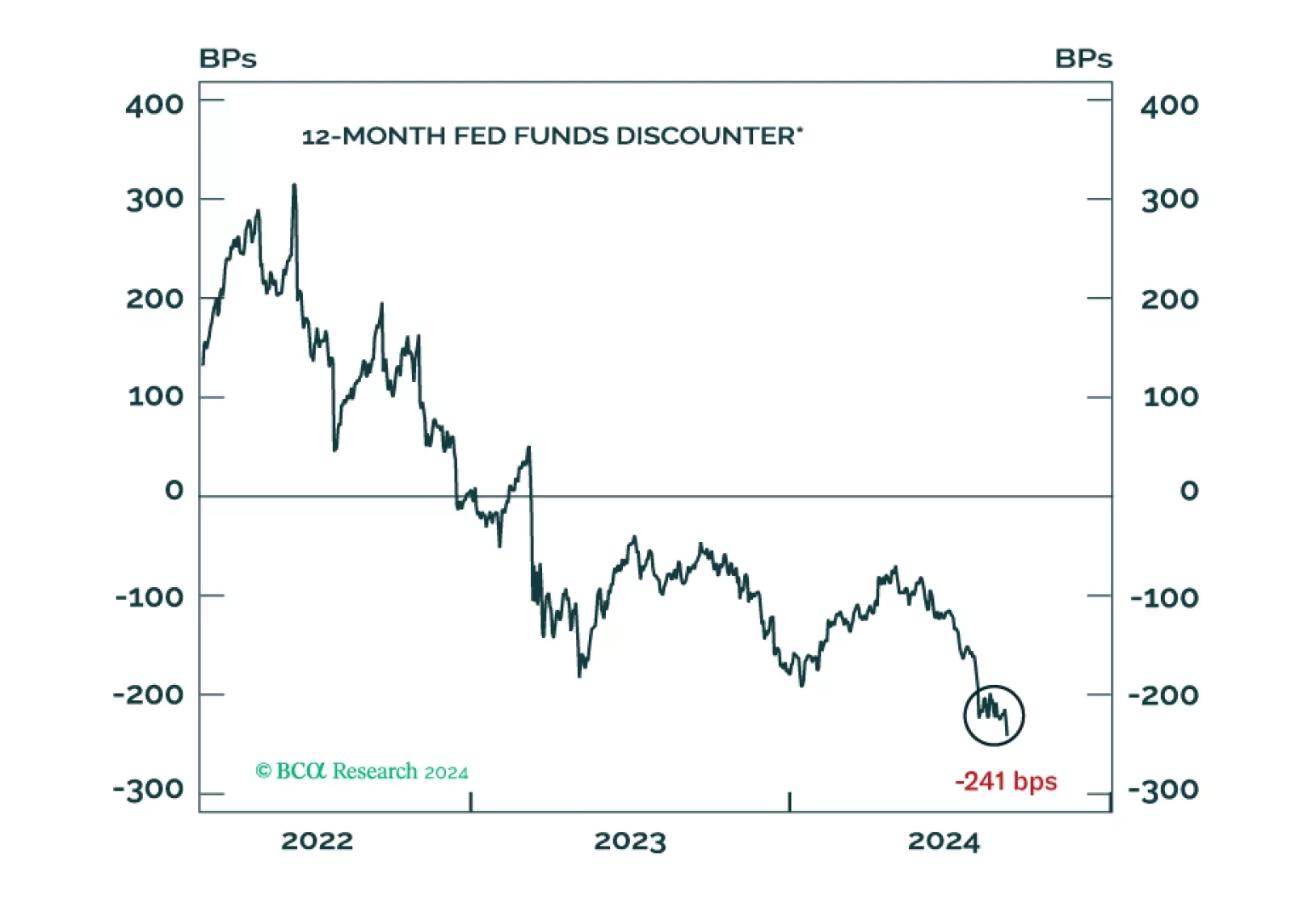

Our reaction to this morning’s CPI report and what it means for Fed policy.

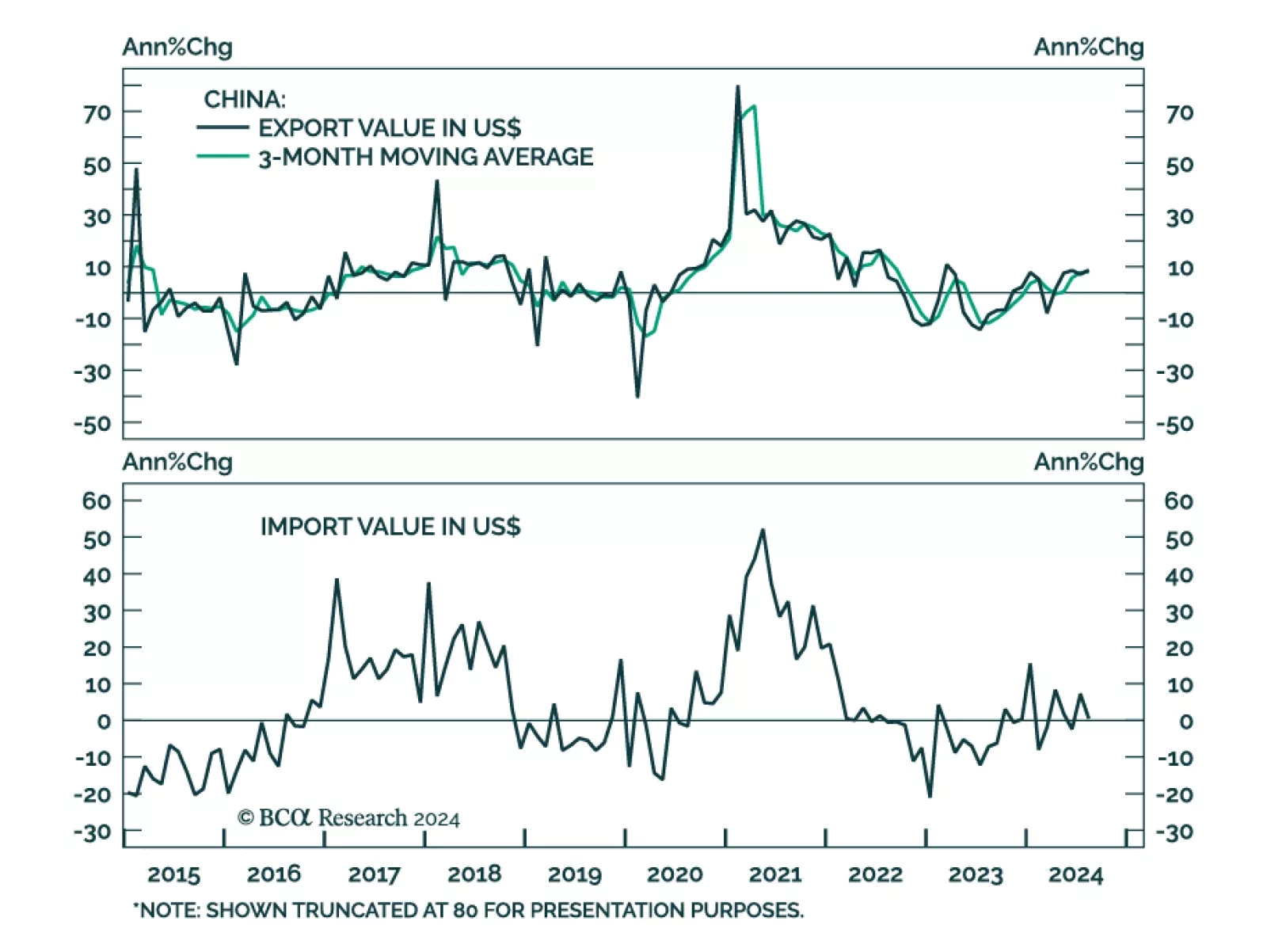

Chinese export growth in USD terms accelerated from 7.0% y/y to a larger-than-expected 8.7% in August. China’s exports to its major trading partners (US, EU and ASEAN) were all growing in August on a year-on-year basis, though at a decelerating pace in the US…

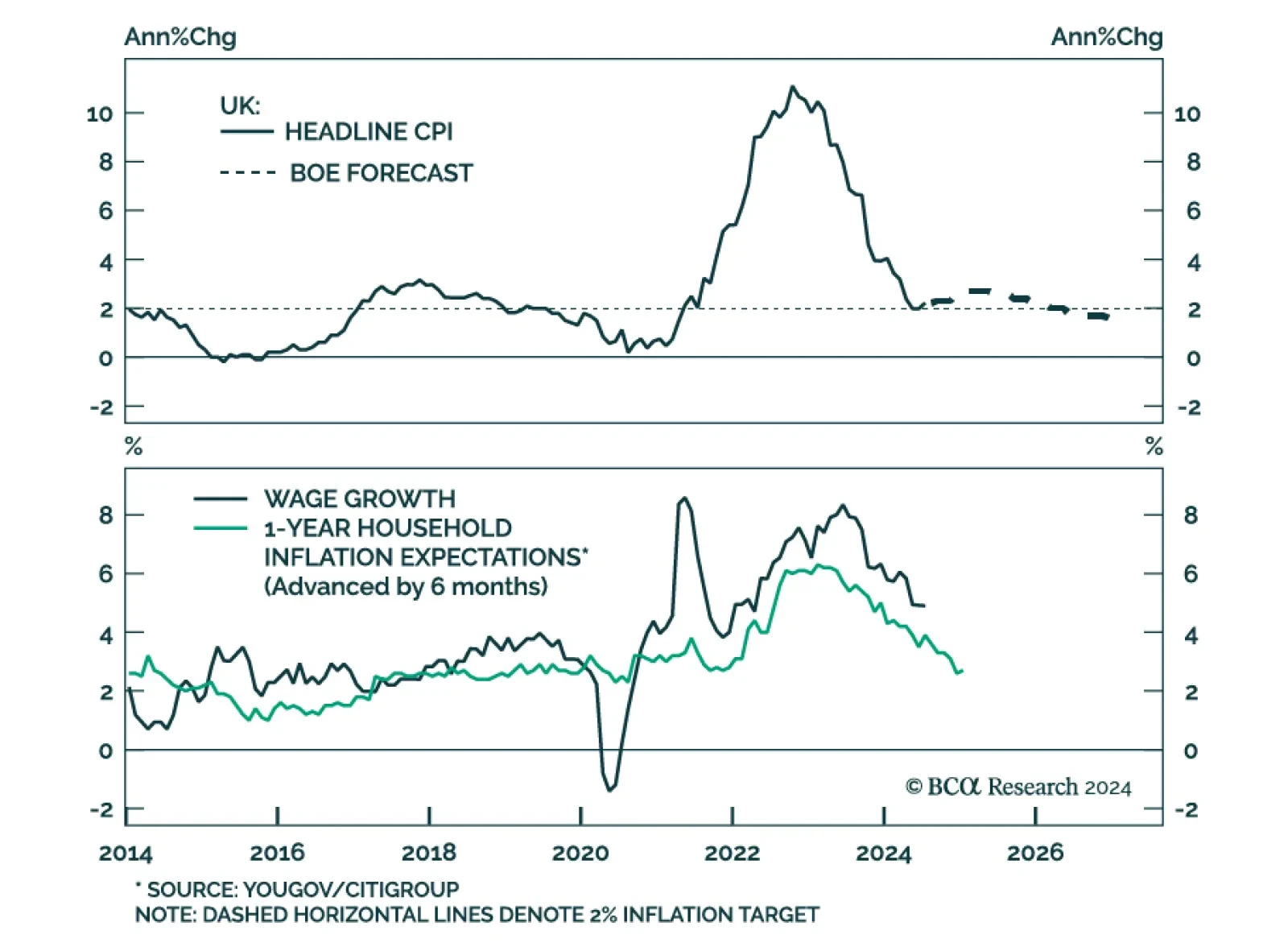

The BoE embarked on its easing cycle in August, delivering its first 25 bps rate cut. The decision was nowhere near unanimous, with 5 MPCs out of 9 voting in favor of lowering policy rates. Indeed, while headline inflation is sitting right on the central…

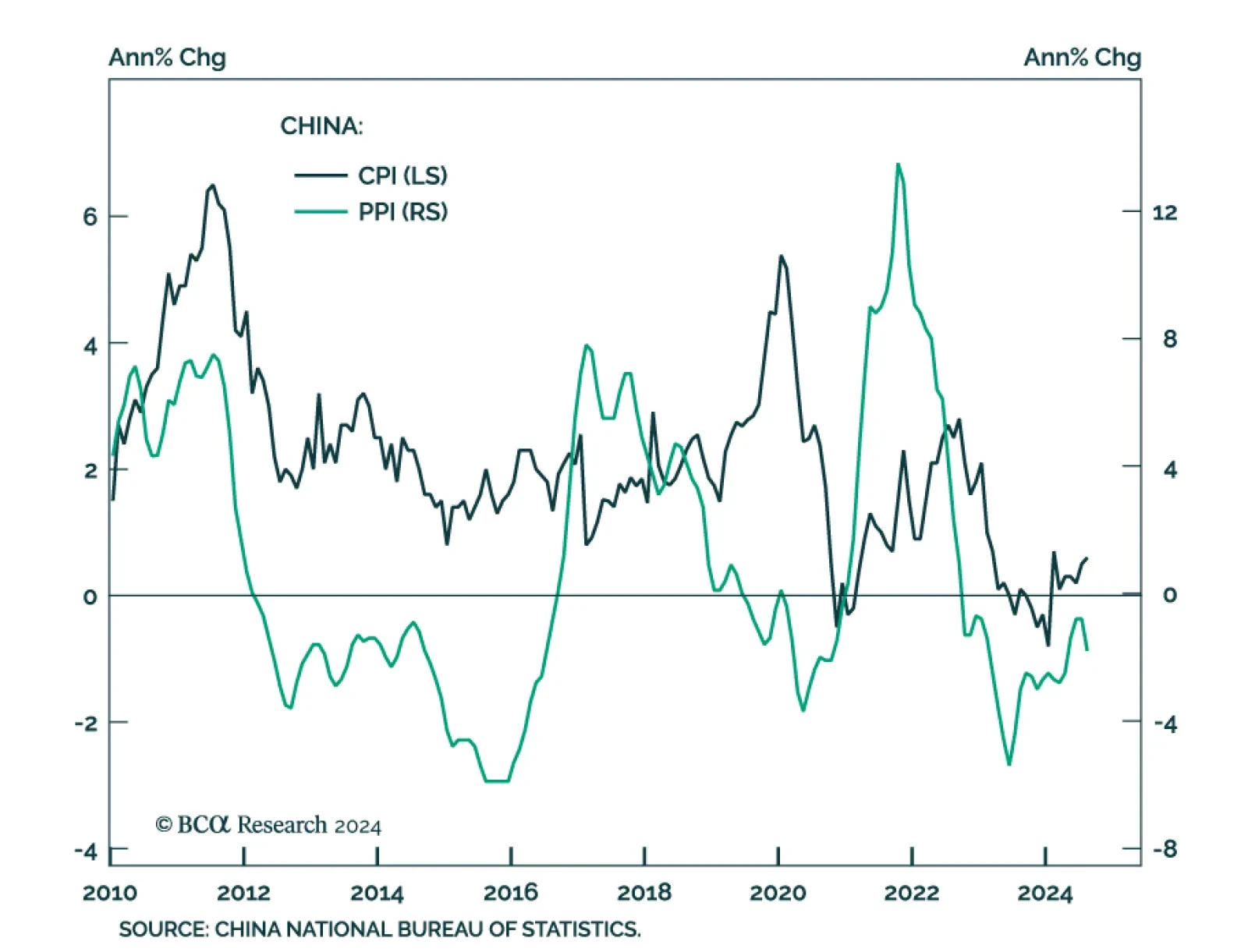

China’s CPI and PPI both surprised to the downside in August. Consumer prices grew from 0.5% y/y to 0.6%, below the 0.7% anticipated. However, a 2.8% y/y surge in food prices (the fastest pace so far this year) overstates this headline figure. Core CPI…

Eurozone GDP’s final estimate indicates that growth was slower than expected in Q2. Output grew 0.2% q/q in Q2, compared to 0.3% previously reported. A significant downward revision to capex (2.2% contraction against 1.8% previously estimated) drove the…

The July Employment Situation report had already cemented the case for a September rate cut and Chairman Powell’s Jackson Hole comments dispelled any remaining doubt about an imminent monetary easing cycle. All the labor market data released since then…

Our Portfolio Allocation Summary for September 2024.