Inflation/Deflation

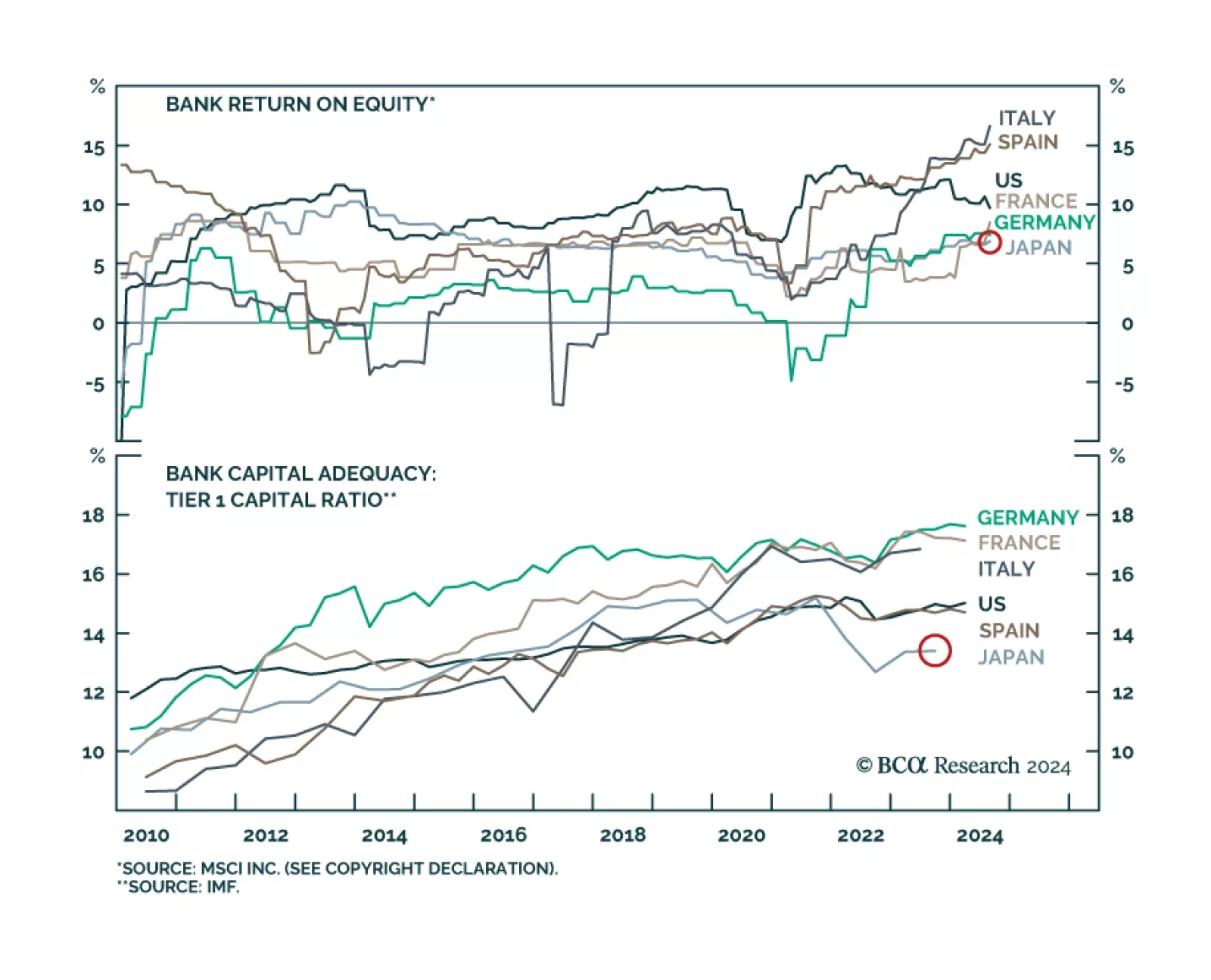

The Bank of Japan’s policy normalization has been accompanied by exceptional outperformance by Japanese banks. Japanese banks have outperformed both the country’s broader market as well as the MSCI ACW Banks index by 10.3% and 2.6%, respectively, so far this…

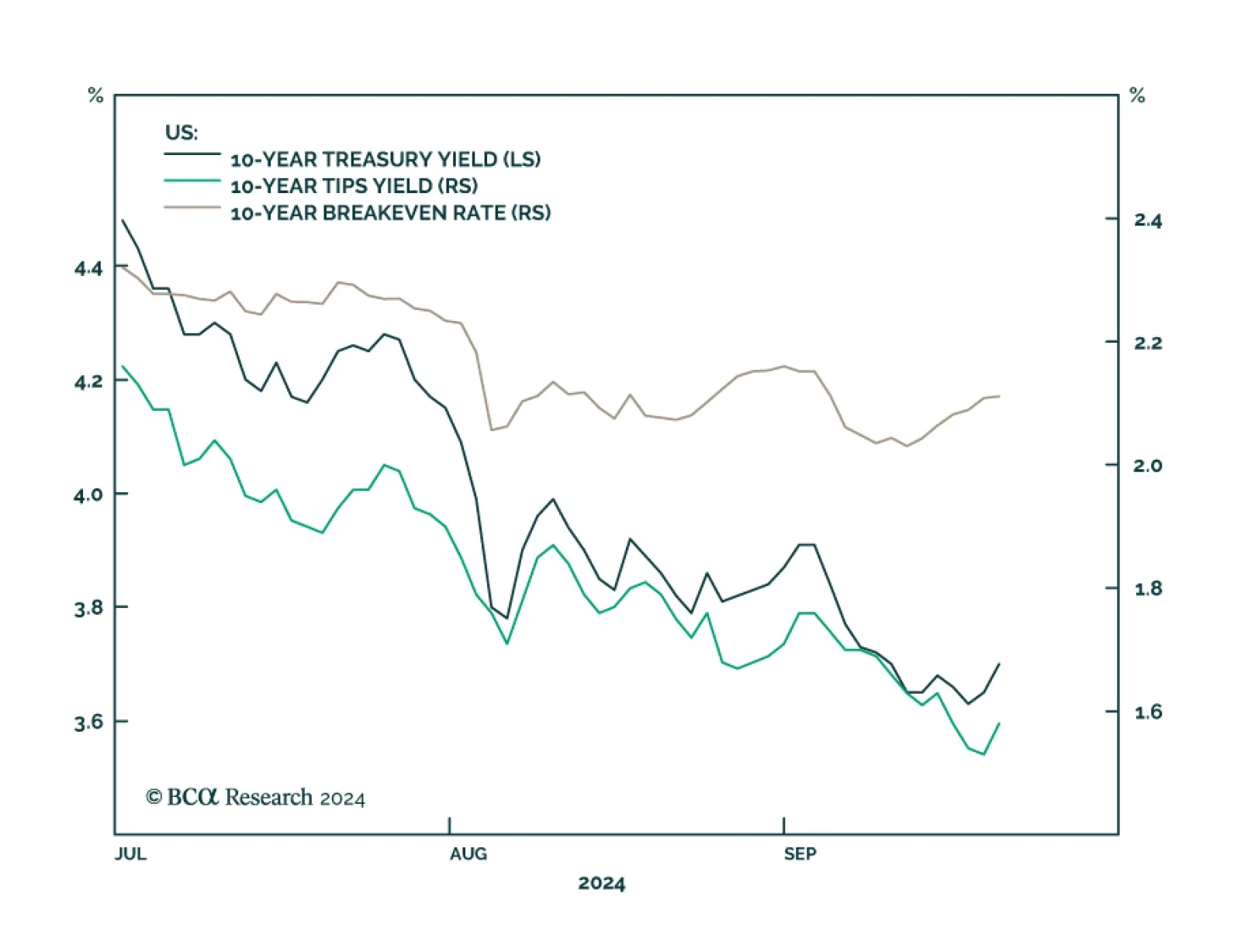

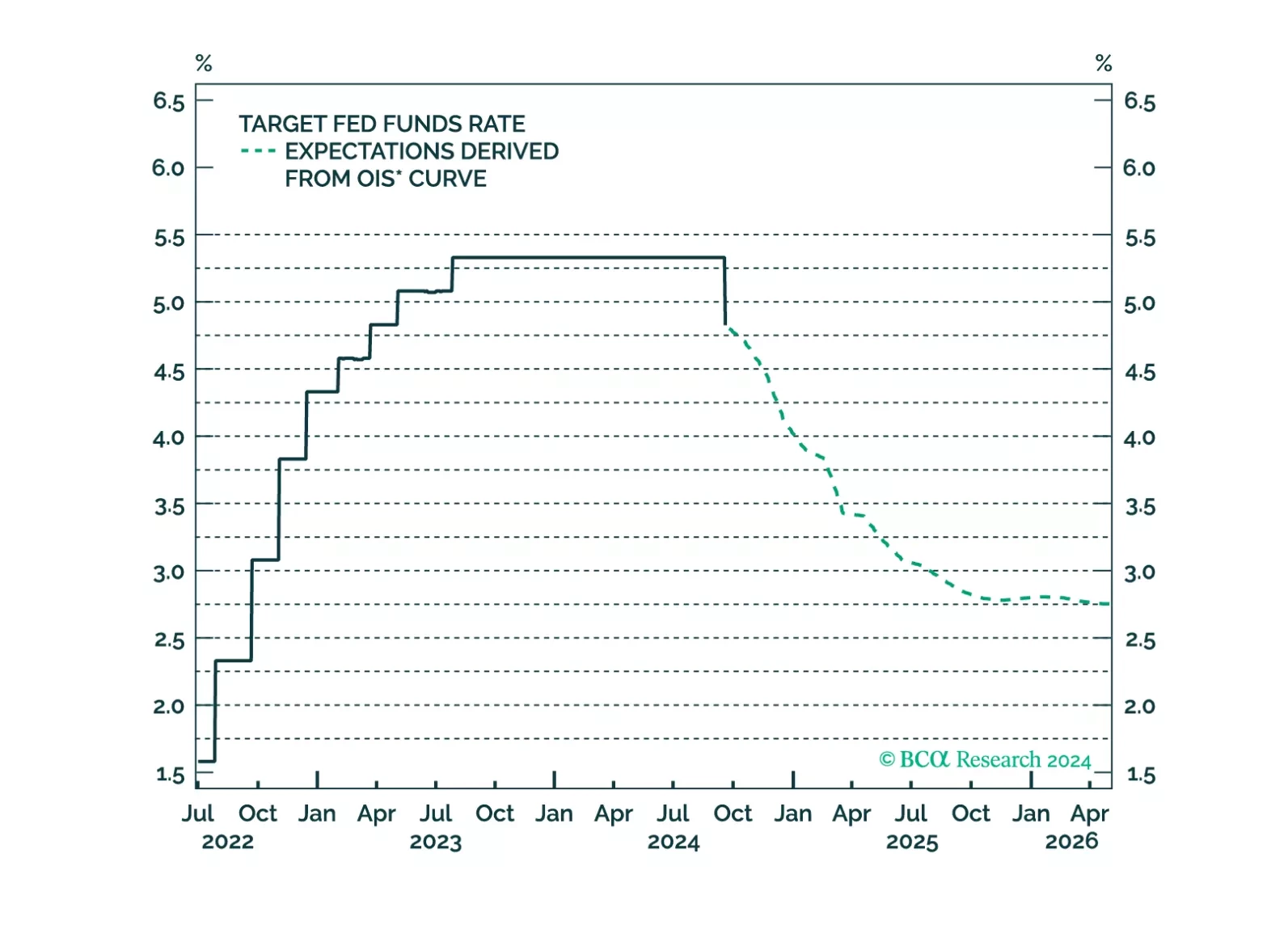

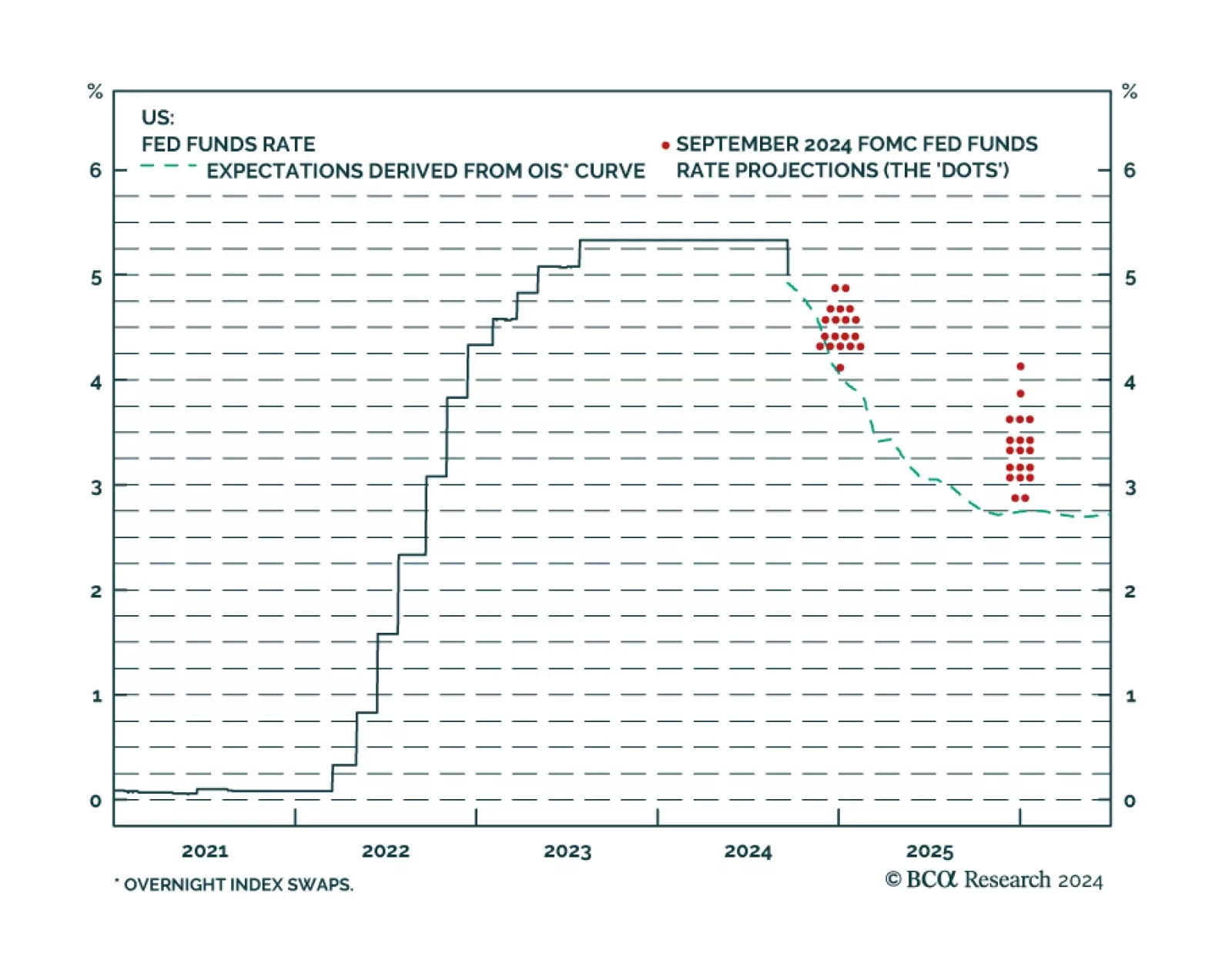

The 10-year Treasury yield rose in the aftermath of the Fed’s jumbo rate cut on Wednesday. Our US Bond strategists noted that this move reflects the fact that the downward revisions to the dots still fall short of the magnitude of cuts embedded in the…

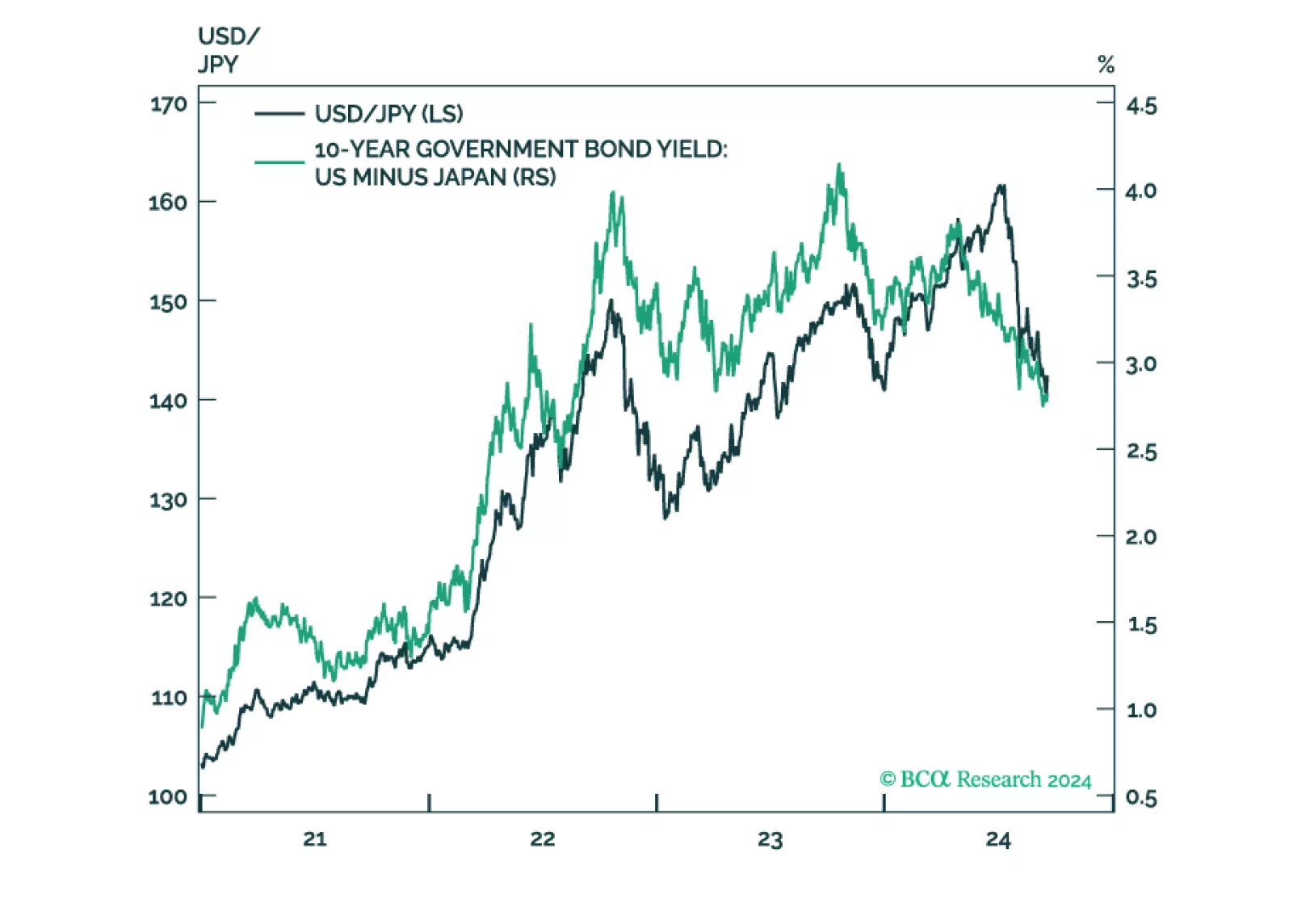

In this report, we argue that the Bank of Japan is unlikely to hike interest rates this week, but the relative trajectory of bond yields in Japan is higher. This warrants an underweight position in JGBs and a leveraged bet on a higher yen. The positioning for equity investors is murkier, as progress on corporate reforms is necessary for a rerating in Japanese shares. That is not yet very clear. The bottom line is: Stay long the yen.

We update our bond views following today’s 50 bps rate cut.

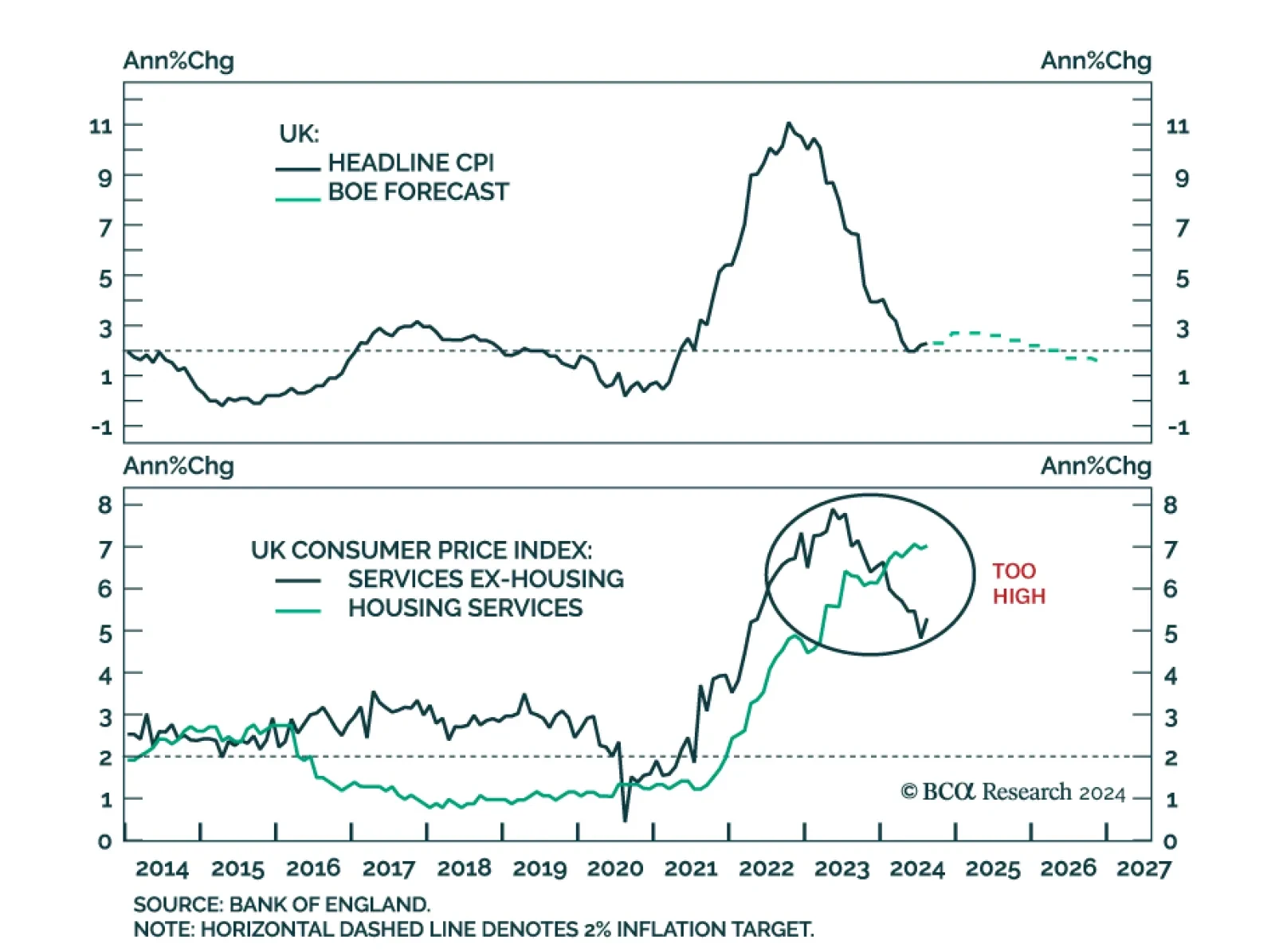

UK headline CPI grew at a stable 2.2% y/y in August, though the core measure accelerated from 3.3% to 3.6%, in line with expectations. An 11.6% annual increase in airfare largely drove core CPI higher, while offsetting contributions from food and alcohol led…

The Fed started its easing cycle with a bang, cutting the policy rate by 50 basis points in September, above consensus expectations but in line with odds embedded in the futures and OIS curves. Our US Bond strategists had highlighted it is unusual for the…

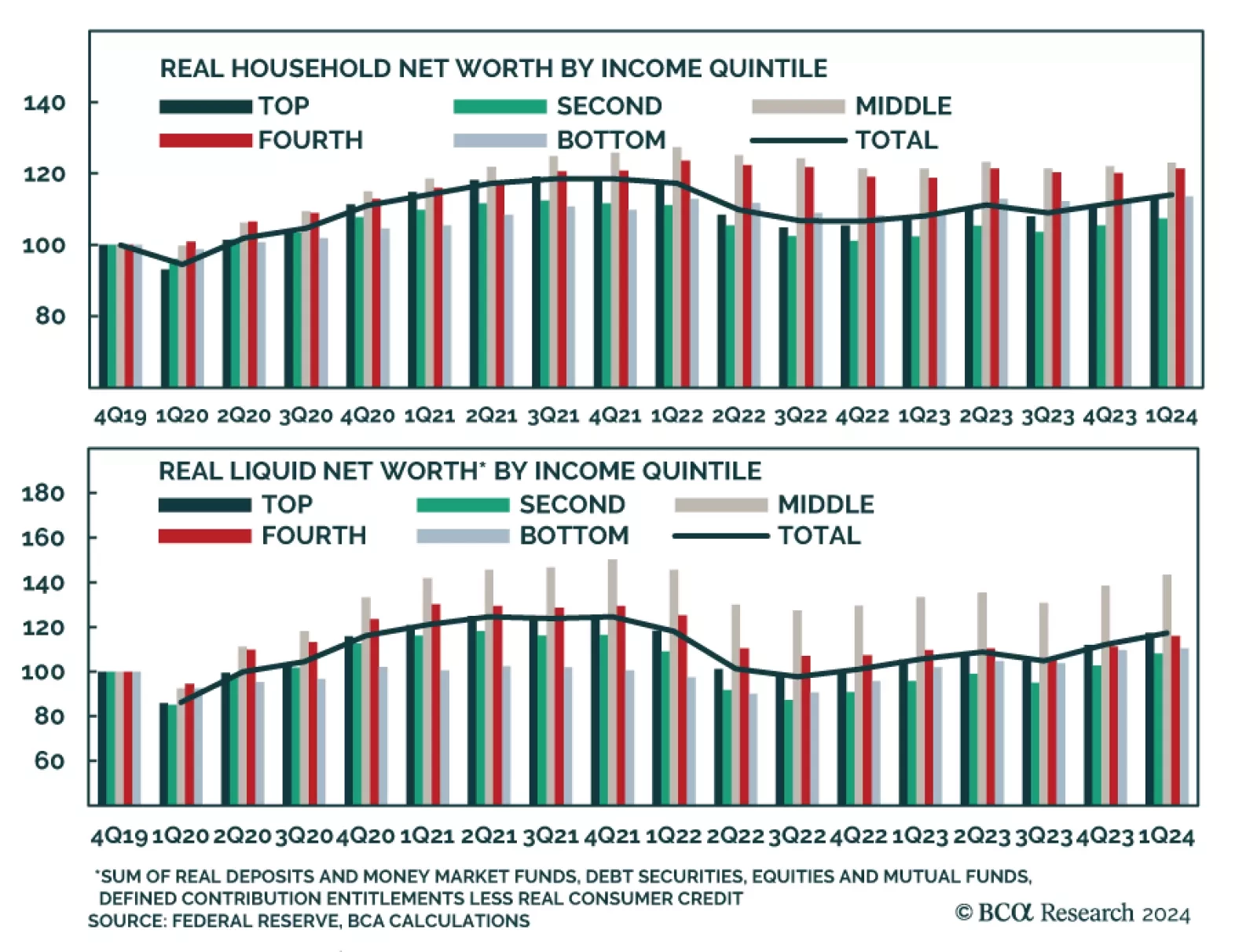

Stress among lower-income households is often cited as an early indication of deteriorating aggregate consumer fundamentals. The data indeed suggests that this cohort’s cash holdings are depleting. However, the Fed’s quarterly estimates of household wealth…

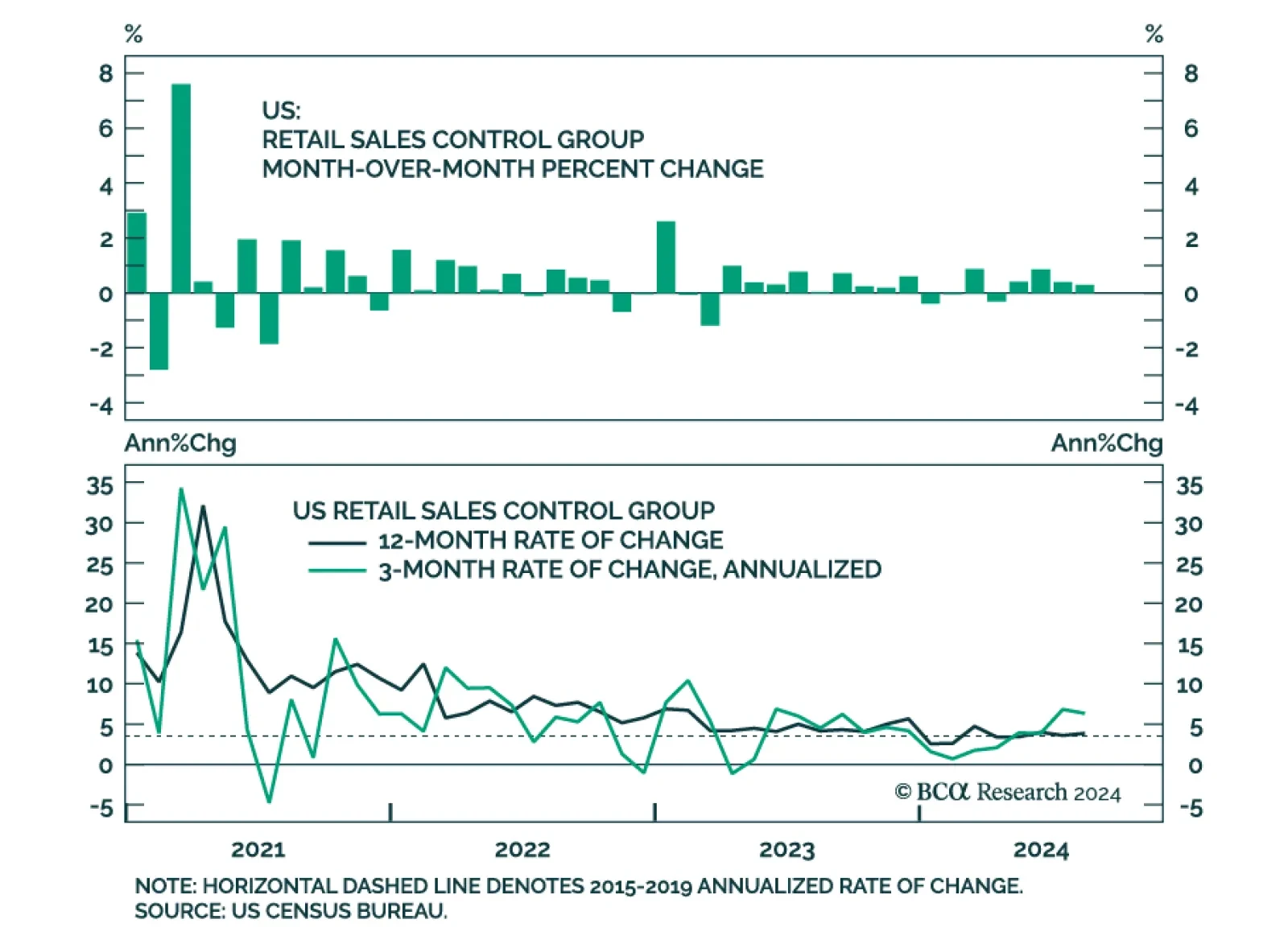

US retail sales grew 0.1% m/m in August and beat expectations of a 0.2% monthly contraction. The positive surprise seemingly spurred equity market gains on Tuesday morning. However, details do not paint as rosy a picture as the headline number…

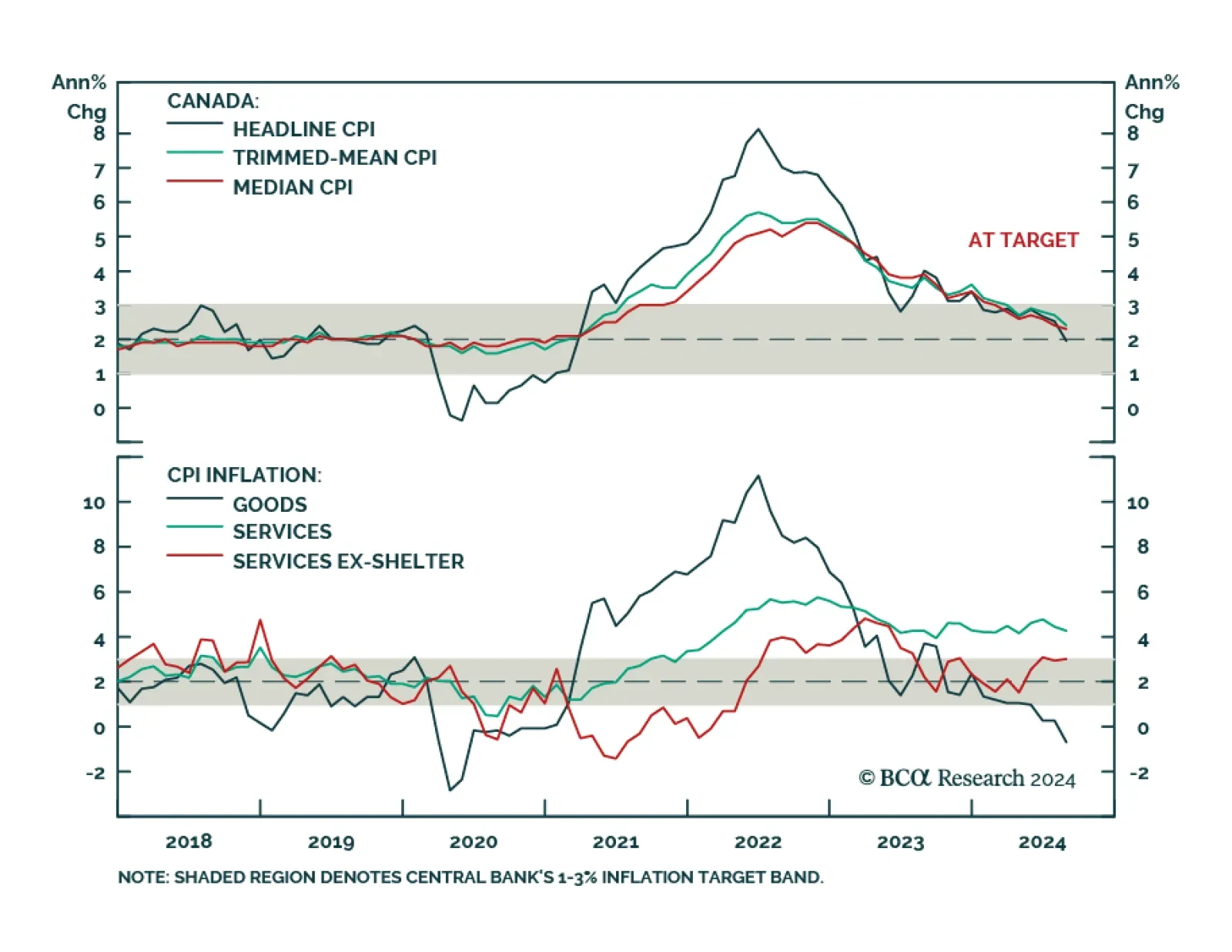

Canadian headline CPI inflation decelerated at a faster-than-anticipated pace from 2.5% y/y to 2.0% in August, the slowest since 2021. Notably, core median and trimmed-mean CPI ticked 0.1 ppt and 0.3 ppt lower to 2.3% and 2.4%, respectively. Lower oil…