Inflation/Deflation

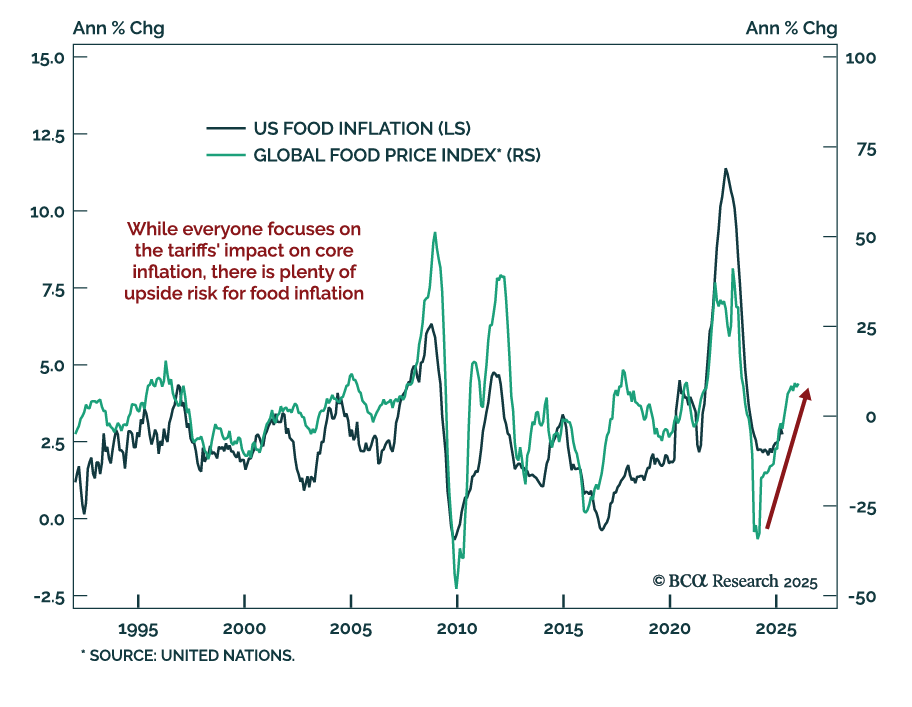

The upward trend in global food prices suggests that food inflation risks re-accelerating in the US. Historically, US food inflation lags the United Nations’ global food price index by about nine months. The annual growth in global food prices has been…

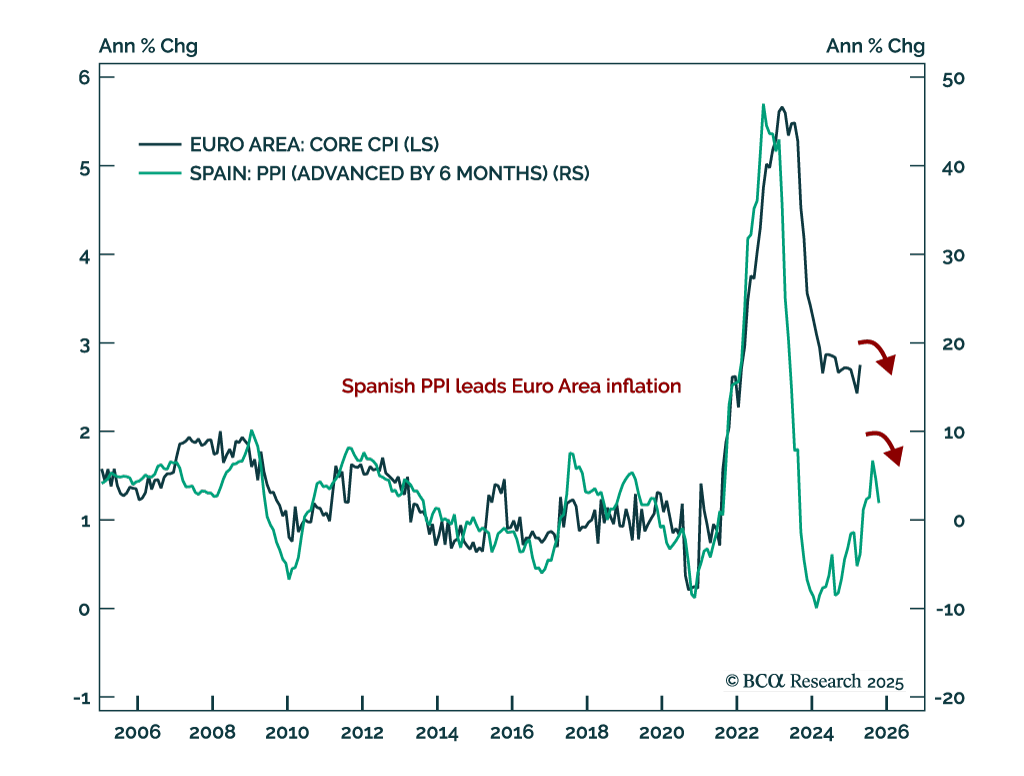

Producer prices in Spain surprised to the downside, foreshadowing a relapse in Euro Area inflation and cementing the ECB’s dovish stance. The Spanish PPI index fell to 1.9% in April, continuing the disinflation trend from the last period while recording the…

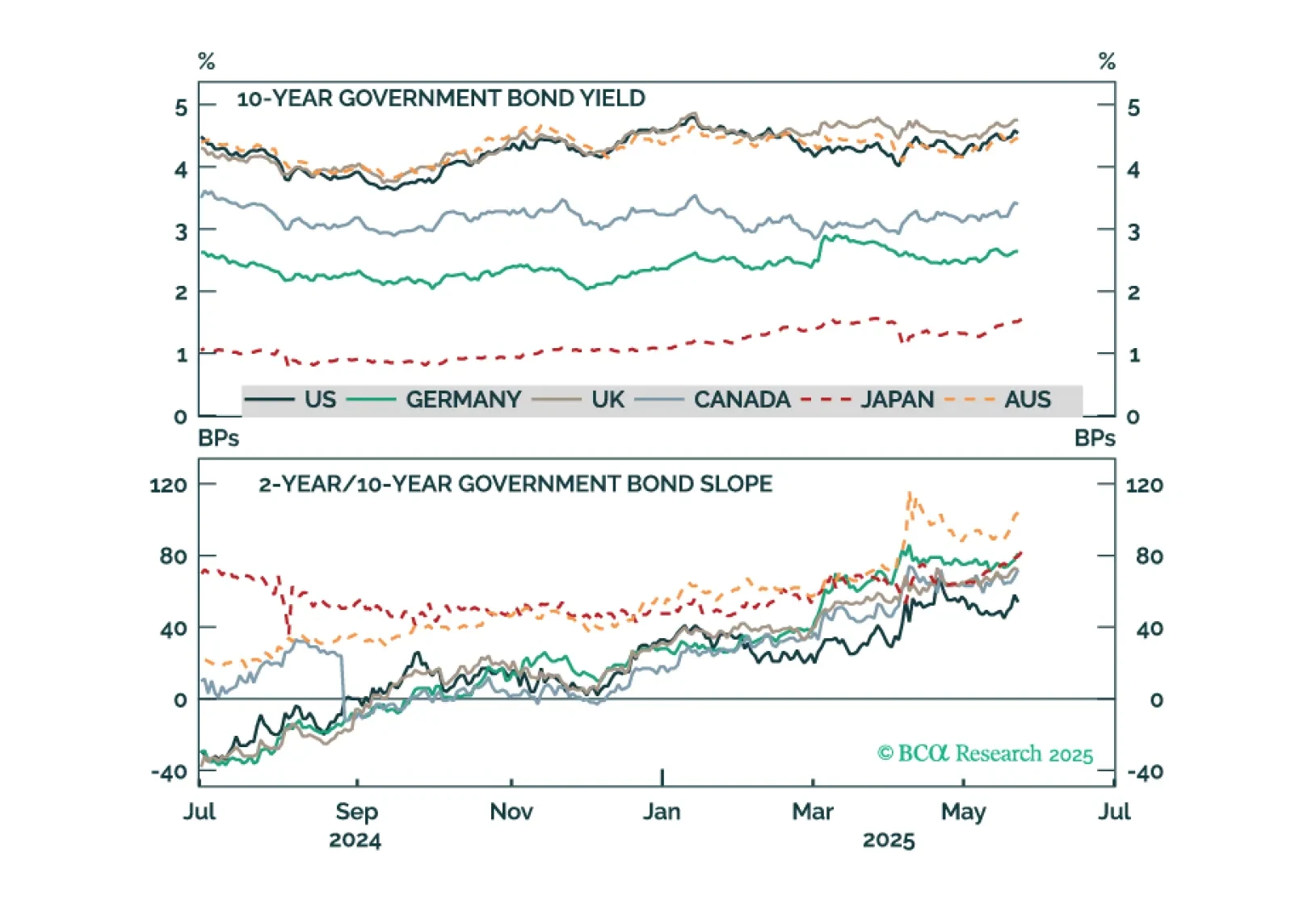

We perform a decomposition of yields moves across six major developed government bond markets to get to the bottom of what’s been driving the global bond selloff of the past eight months.

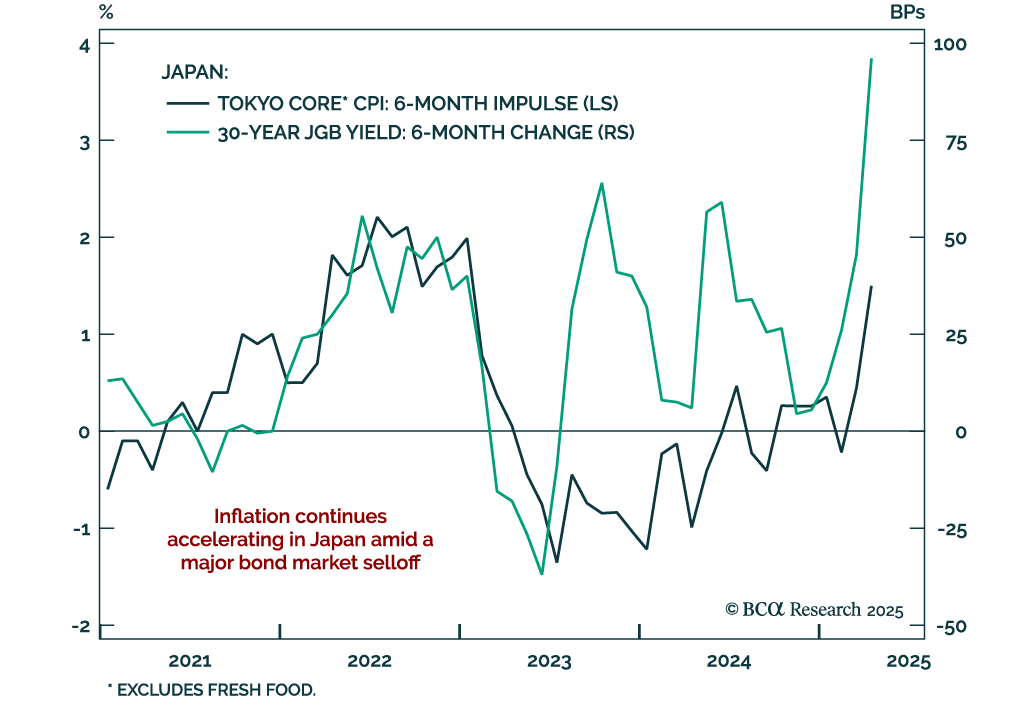

Tokyo CPI surprised to the upside in April, signaling that Japanese inflation shows no sign of deceleration and putting the Bank of Japan (BoJ) in a complicated position. Investors should remain maximum underweight in JGBs and overweight in…

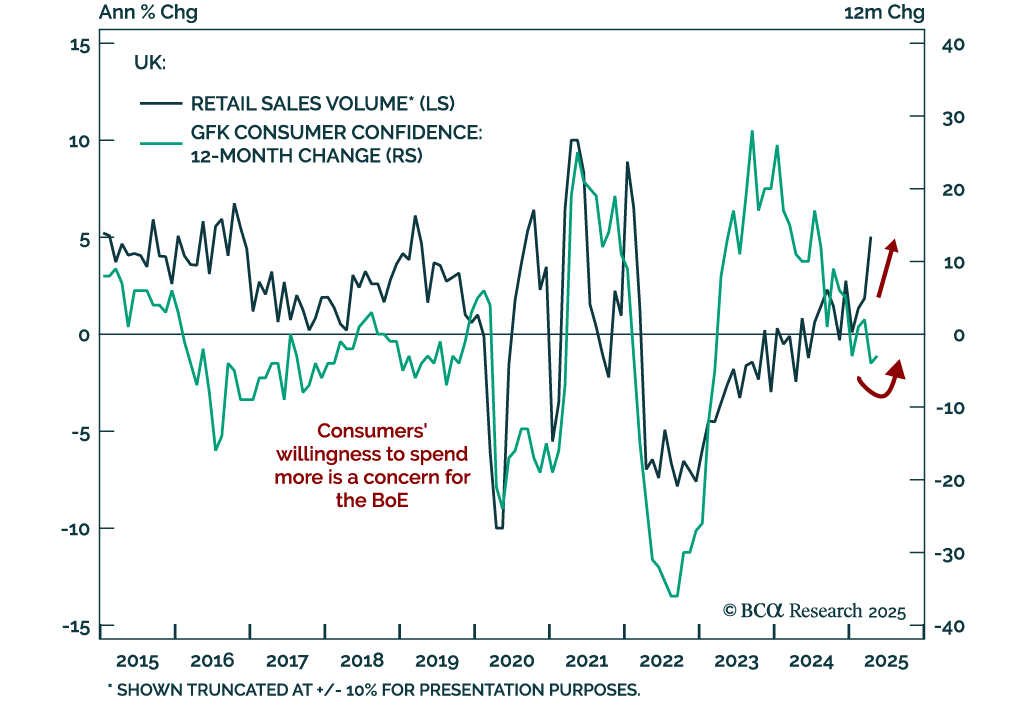

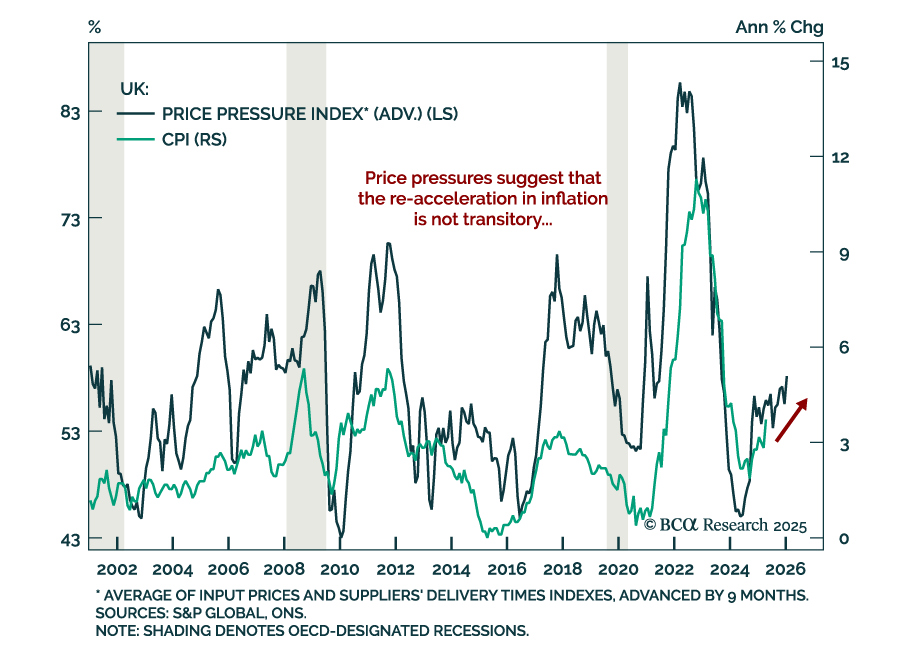

The rebound in UK retail sales and consumer confidence surprised to the upside, and suggests that the re-acceleration in inflation observed earlier this week may not be transitory. UK retail sales rose 1.2% m/m in April from 0.1% m/m, significantly…

UK inflation surprised to the upside in April. Headline inflation rose to a 15-month high of 3.5%, from 2.6% the month before. Core inflation also surprised above estimates, printing 3.8% vs. 3.4% in March. Services inflation climbed to 5.4% from 4.7%. Higher…

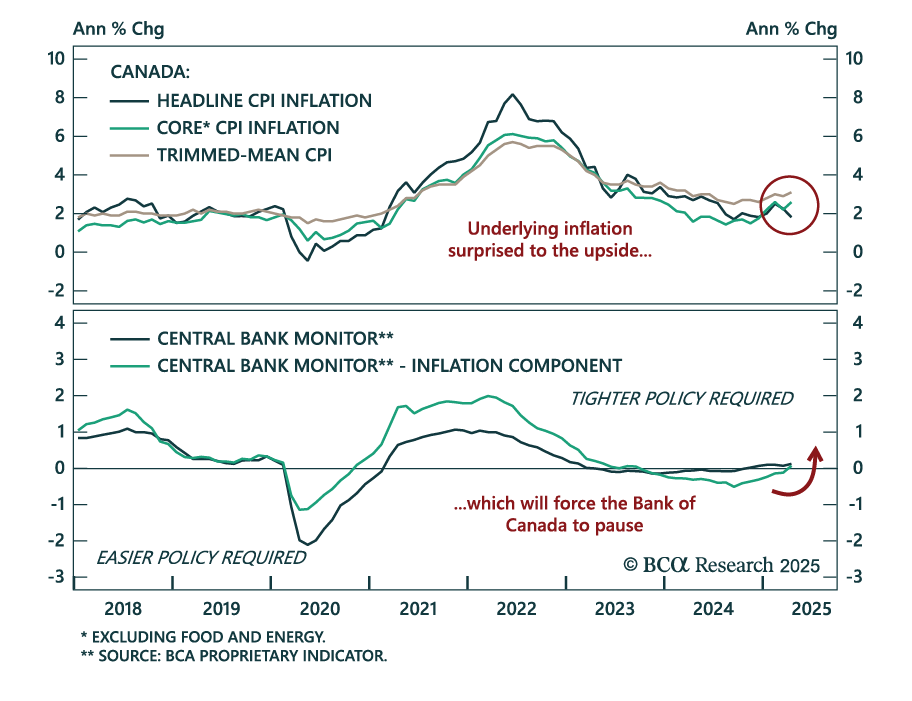

Although Canada’s headline CPI slowed to 1.7% y/y from 2.3% on Tuesday, most measures of underlying inflation surprised to the upside, thus raising the likelihood that the Bank of Canada (BoC) will stay put at its next meeting in three weeks. The…

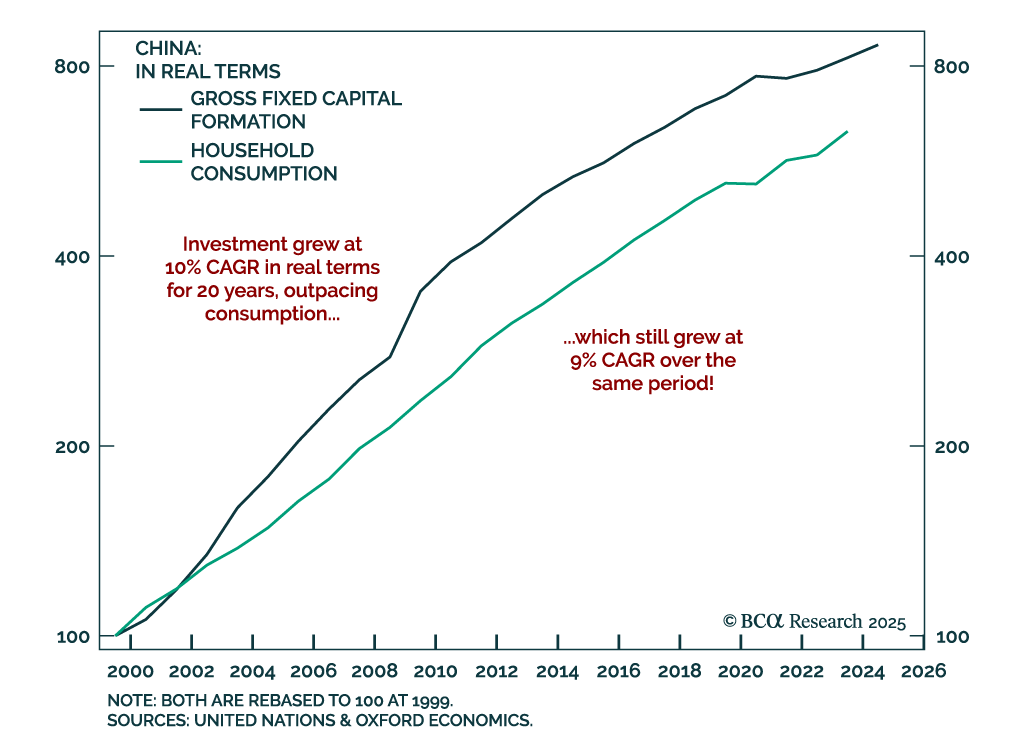

Our EM strategists warn that China’s overinvestment problem has no quick fix, keeping deflationary pressures in place and limiting upside for Chinese equities. Excessive domestic investment, driven by aggressive credit creation, is at the heart of China’s…

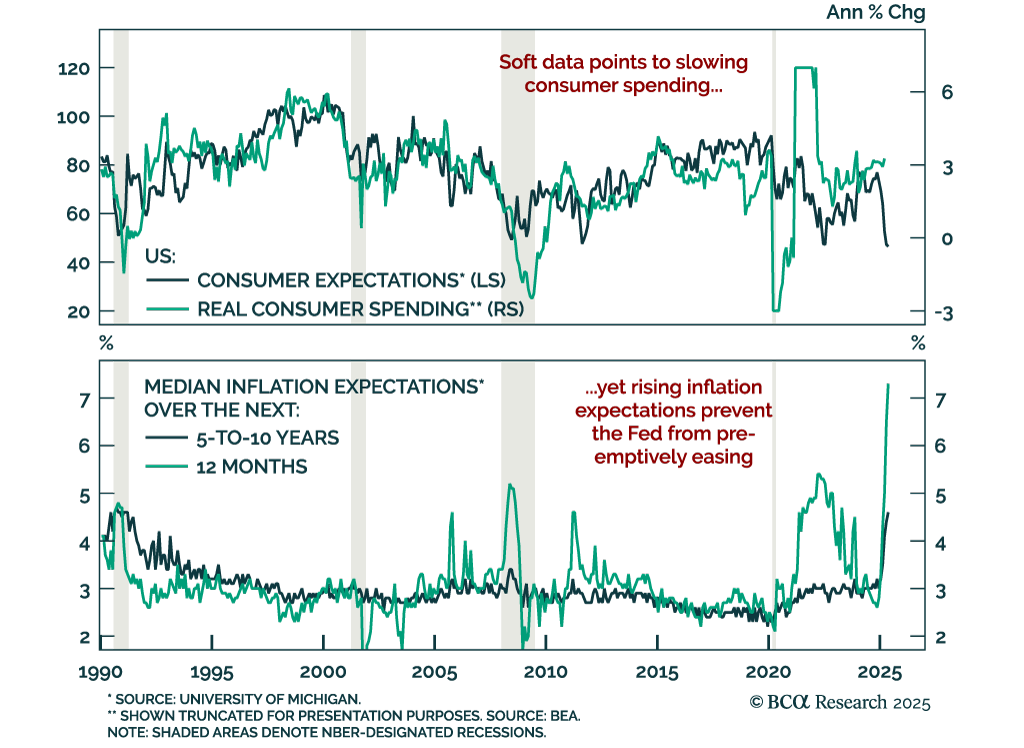

Deteriorating US consumer sentiment and surging inflation expectations add to growth concerns and reinforce our long-duration bond stance. The preliminary May University of Michigan Consumer Sentiment Index missed expectations, falling to 50.8 from 52.2. The…

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.