Inflation/Deflation

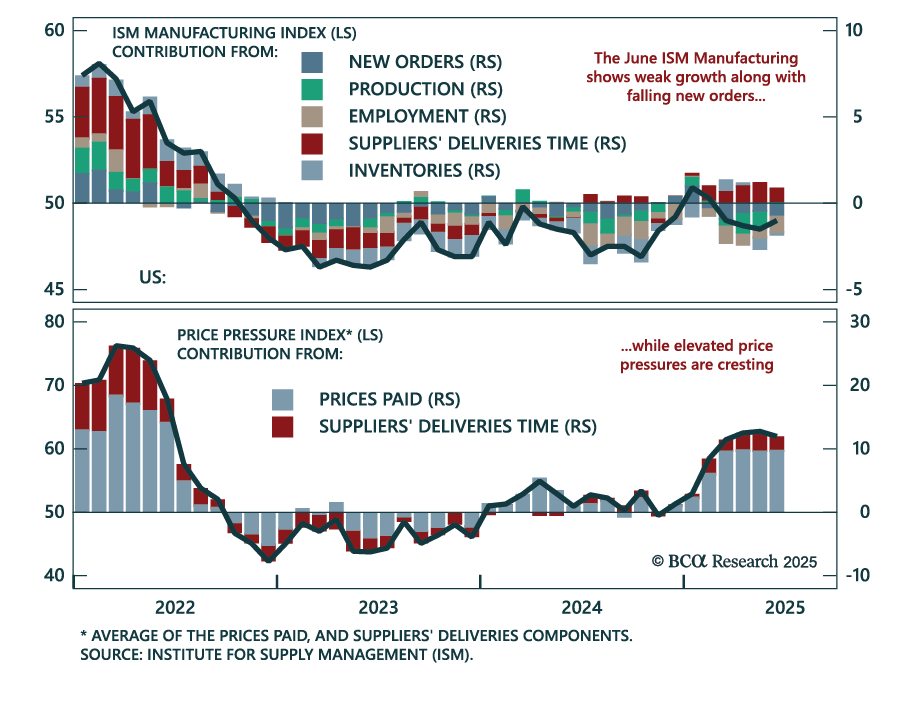

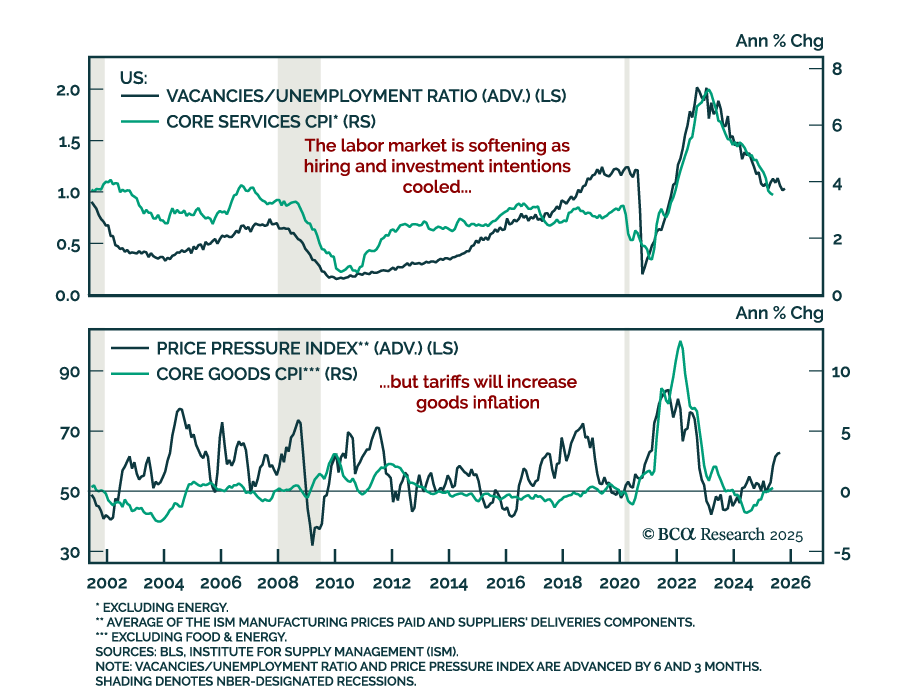

The June ISM points to sluggish US manufacturing and reinforces long duration positioning amid peaking price pressures. The index rose modestly to 49.0 from 48.5 in May, with the rebound driven by slightly higher production and slower supplier deliveries due…

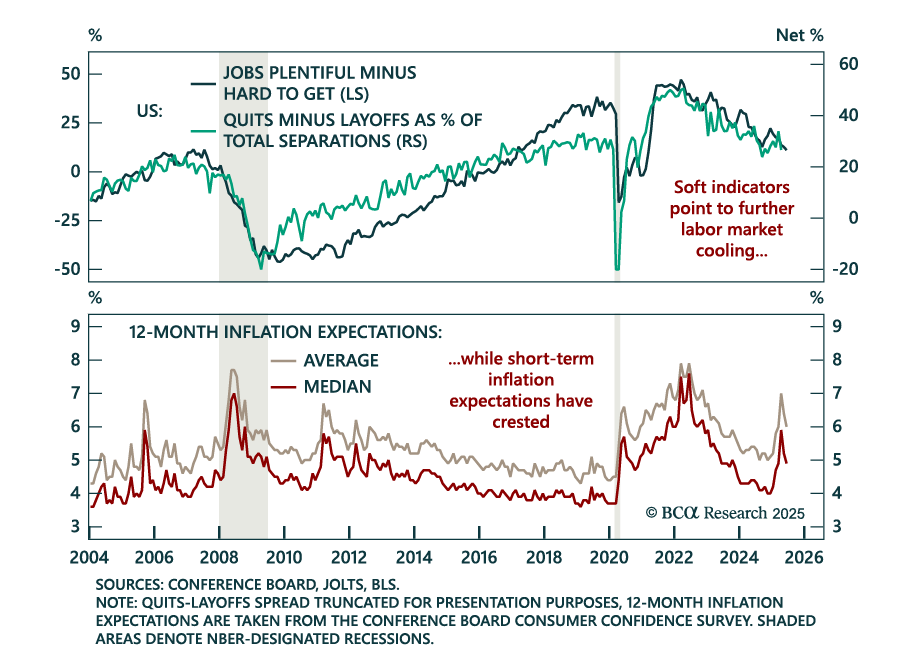

Weakening consumer confidence and fading labor momentum support a long duration stance as inflation fears recede. The June Conference Board Consumer Confidence index dropped 5 points to 93.0, missing expectations. Both present conditions and expectations…

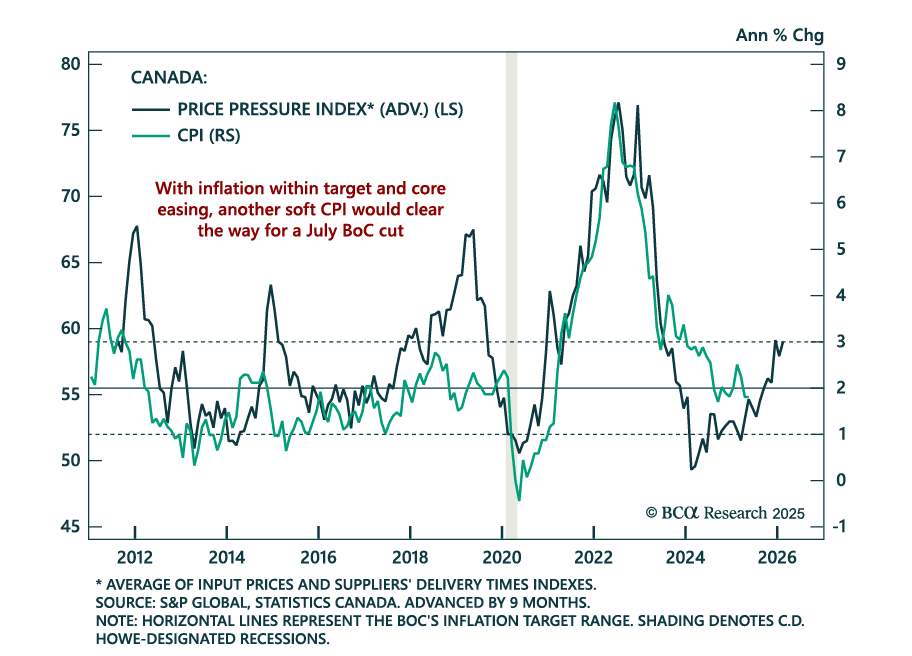

Contained Canadian inflation and soft macro conditions support our overweight on Canadian government bonds. May CPI was in line with expectations, with headline inflation holding at 1.7% y/y and core measures slowing to 3.0%, the upper bound of the BoC’s…

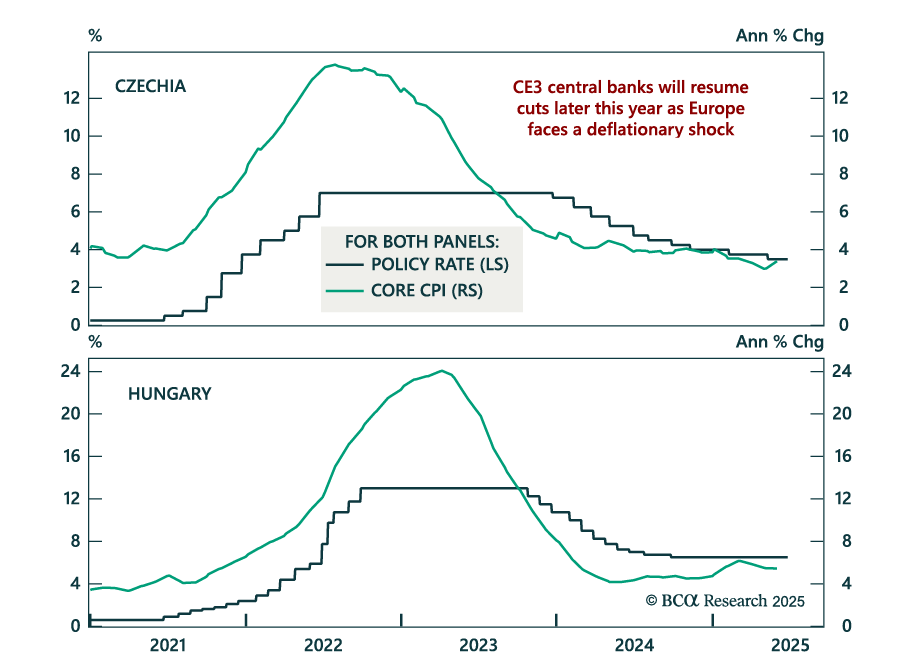

Deflationary pressures and weak core Europe growth support CE3 bond longs as rate cuts loom. The Czech and Hungarian central banks held rates steady at 3.5% and 6.5% this week, following Poland’s earlier decision to keep rates unchanged at 5.25%. While citing…

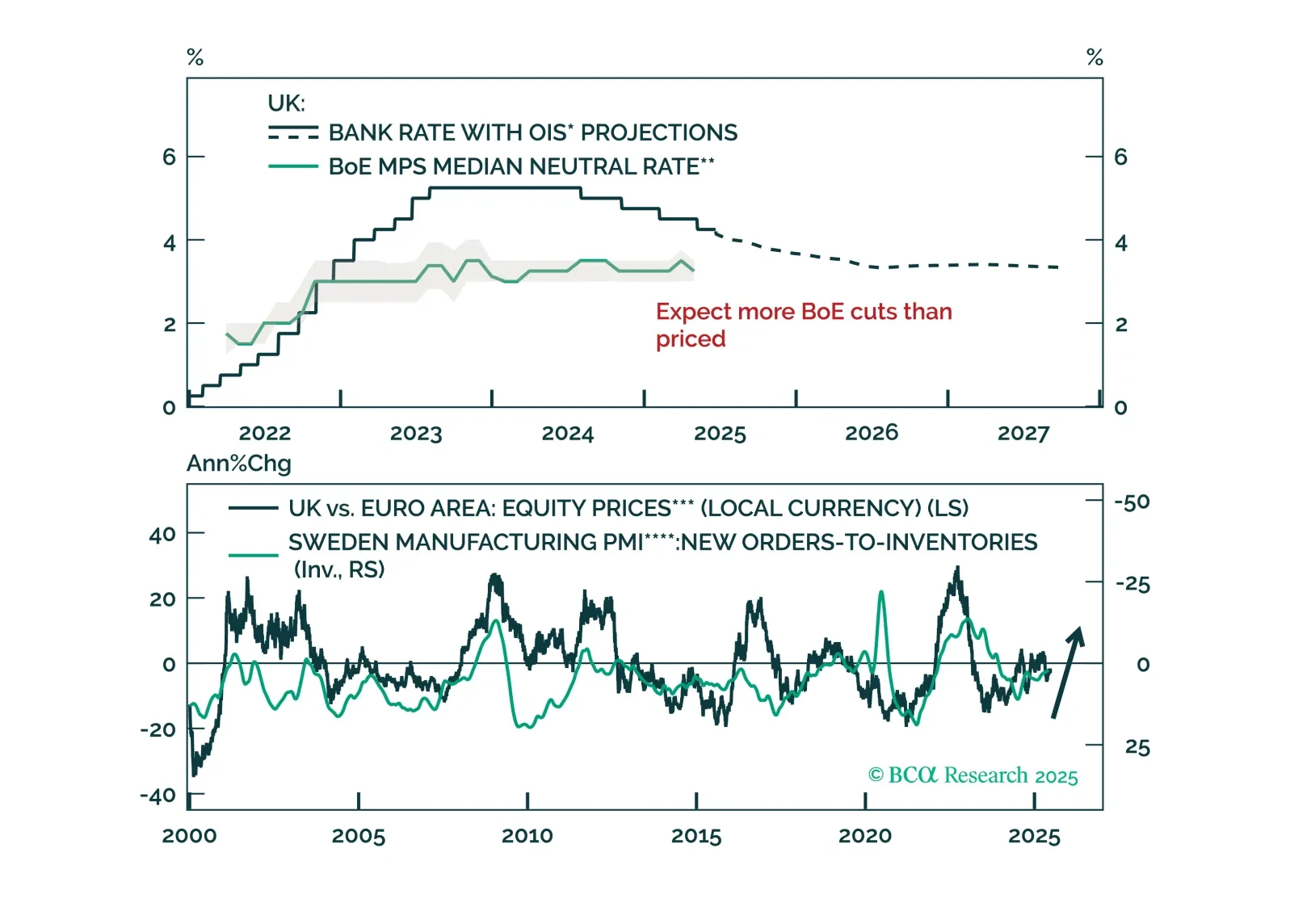

UK inflation risks are falling on the back of a weakening labor market. Read why Gilts and UK stocks are poised to outperform as BoE easing resumes.

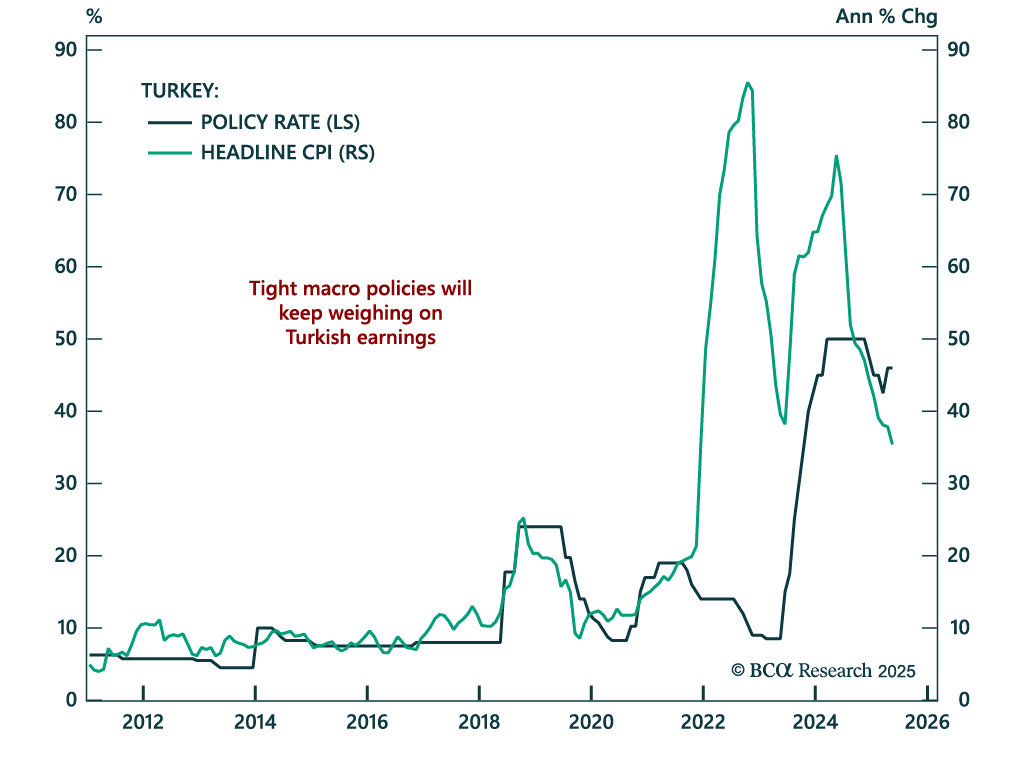

Turkey’s tight policy stance will weigh on growth and earnings, reinforcing our bearish view on Turkish equities. The central bank held rates at 46% and maintained a hawkish bias, consistent with efforts to bring inflation down from 35% to single digits.…

While consumer sentiment is rebounding, sticky inflation expectations and slowing growth warrant staying long duration and steepeners. The preliminary June University of Michigan Consumer Sentiment Index surprised to the upside, rising to 60.5 from 52.2.…

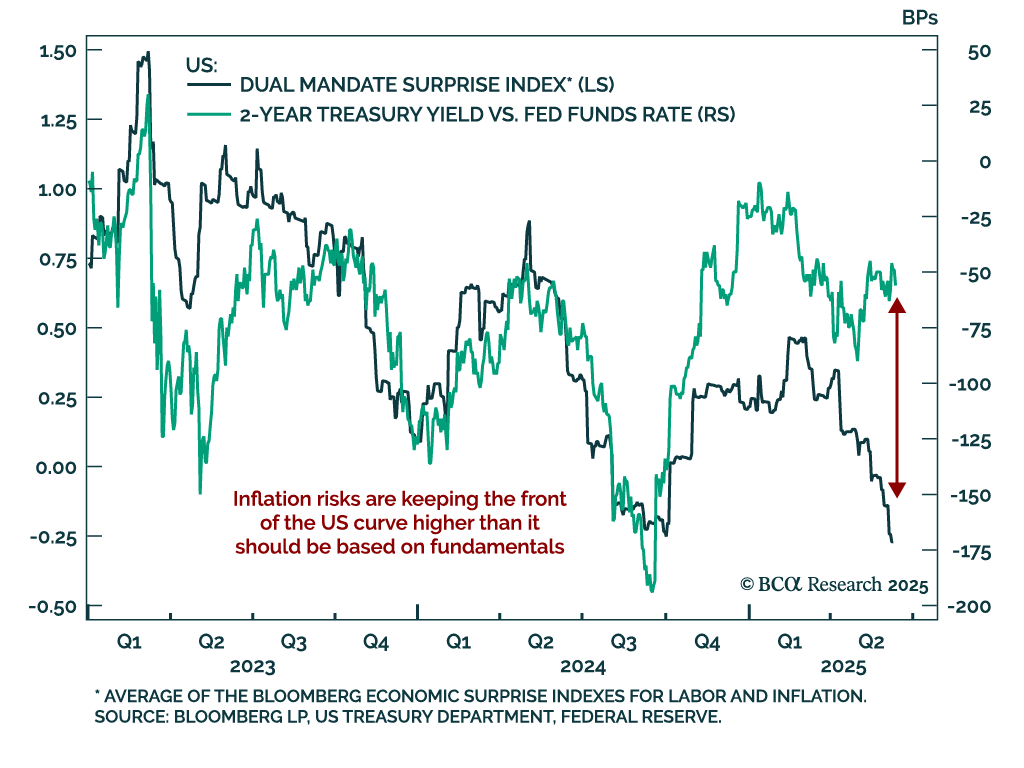

Elevated inflation expectations are keeping the Fed sidelined, reinforcing our long-duration and steepener bias in US rates. The US May CPI would have normally supported cuts, but the Fed cannot risk elevated short-term inflation expectations feeding…

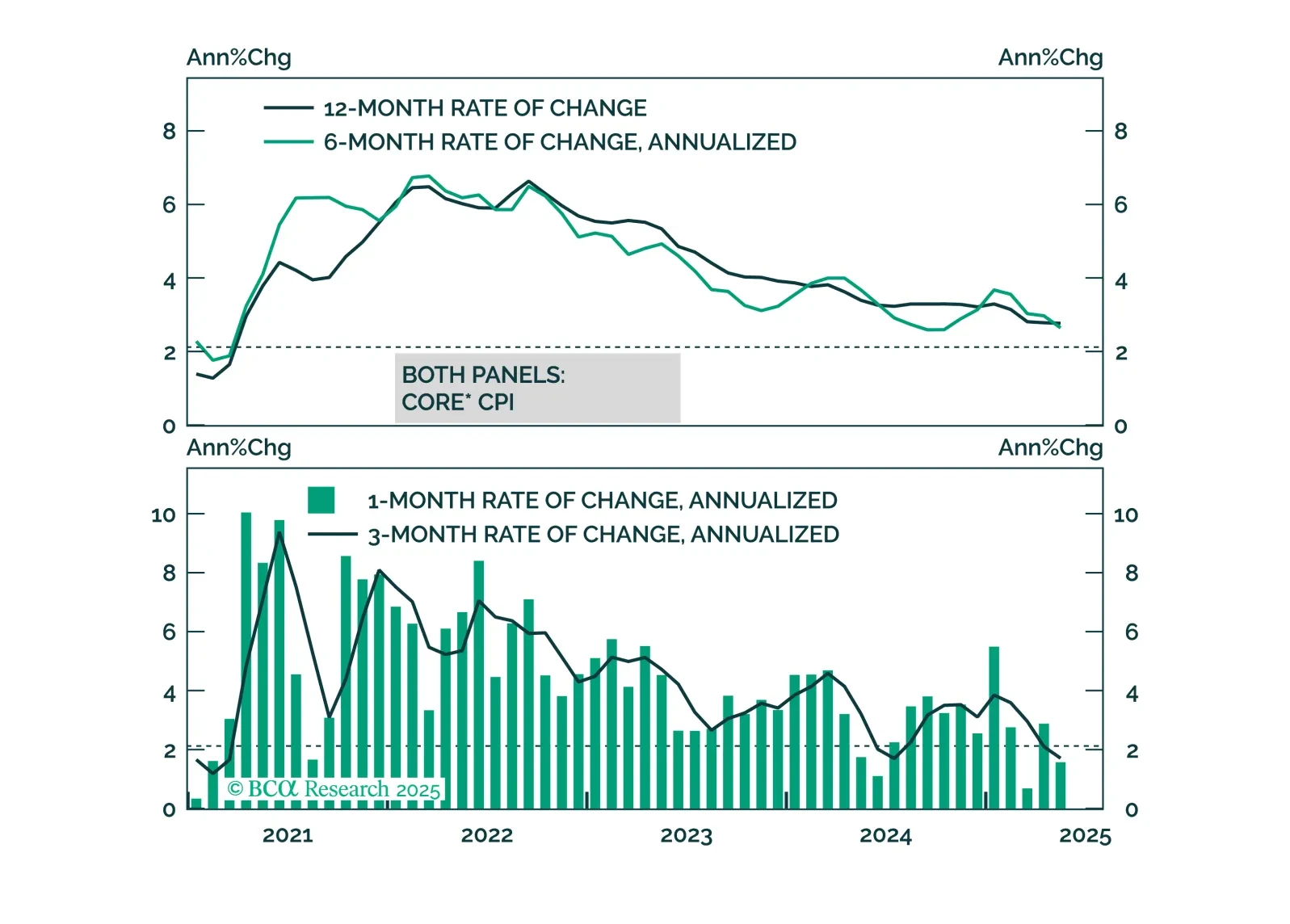

Colder May CPI reinforces our overweight in government bonds and tactical steepener trades as growth slows and the Fed stays cautious. Headline inflation rose 0.1% (2.4% y/y), below expectations, as did core CPI (2.8% y/y). Goods inflation was flat, and…

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.