Inflation/Deflation

A restrictive policy by the ECB and a weak manufacturing sector will create headwinds for European stocks this summer. How should investors position their portfolios in this context?

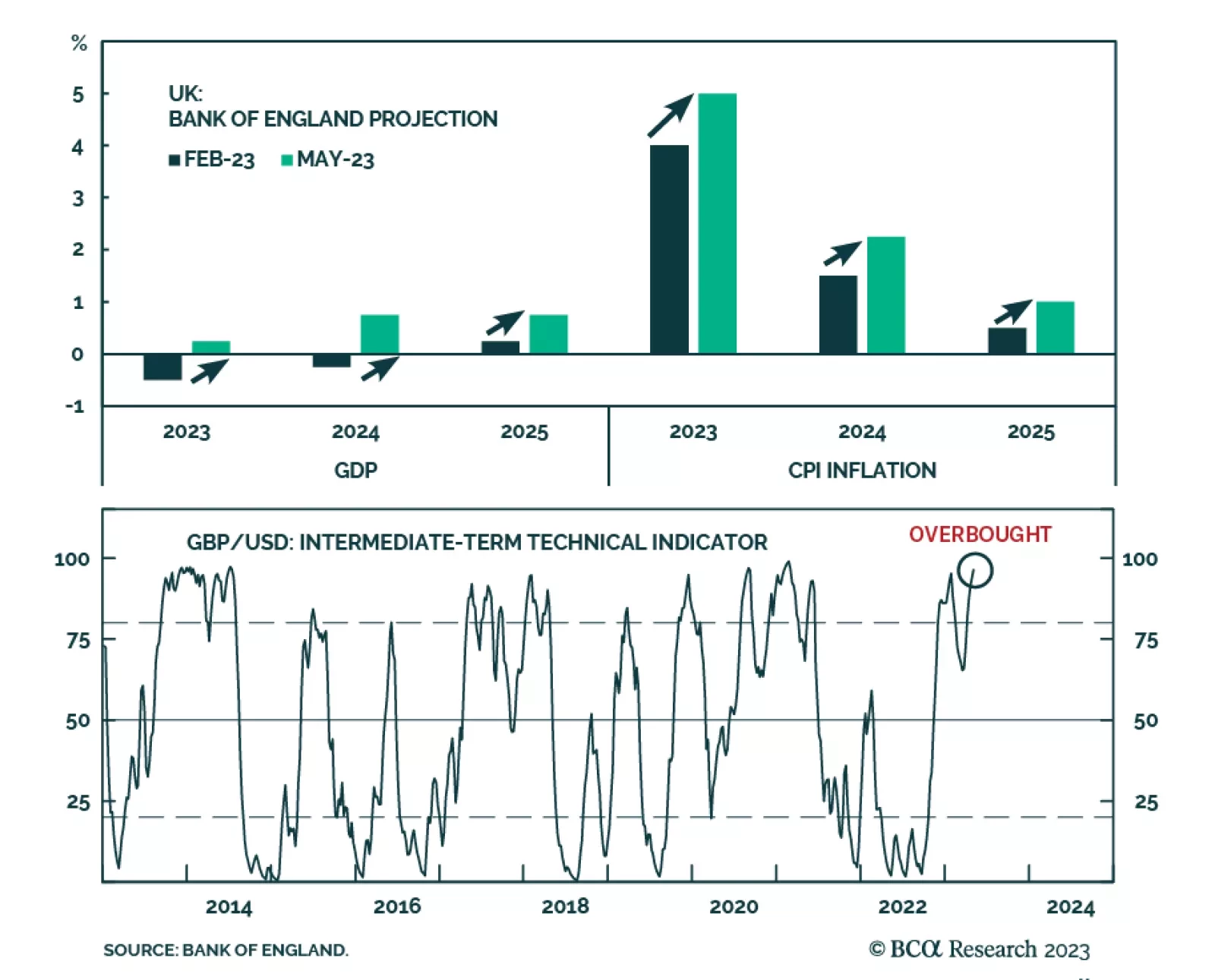

The change in the BoE’s tone has likely altered the path for sterling. In this report, we explore if the BoE’s lens for monetary policy is justified, and provide some targets for the pound.

The change in the BoE’s tone has likely altered the path for sterling. In this report, we explore if the BoE’s lens for monetary policy is justified, and provide some targets for the pound.

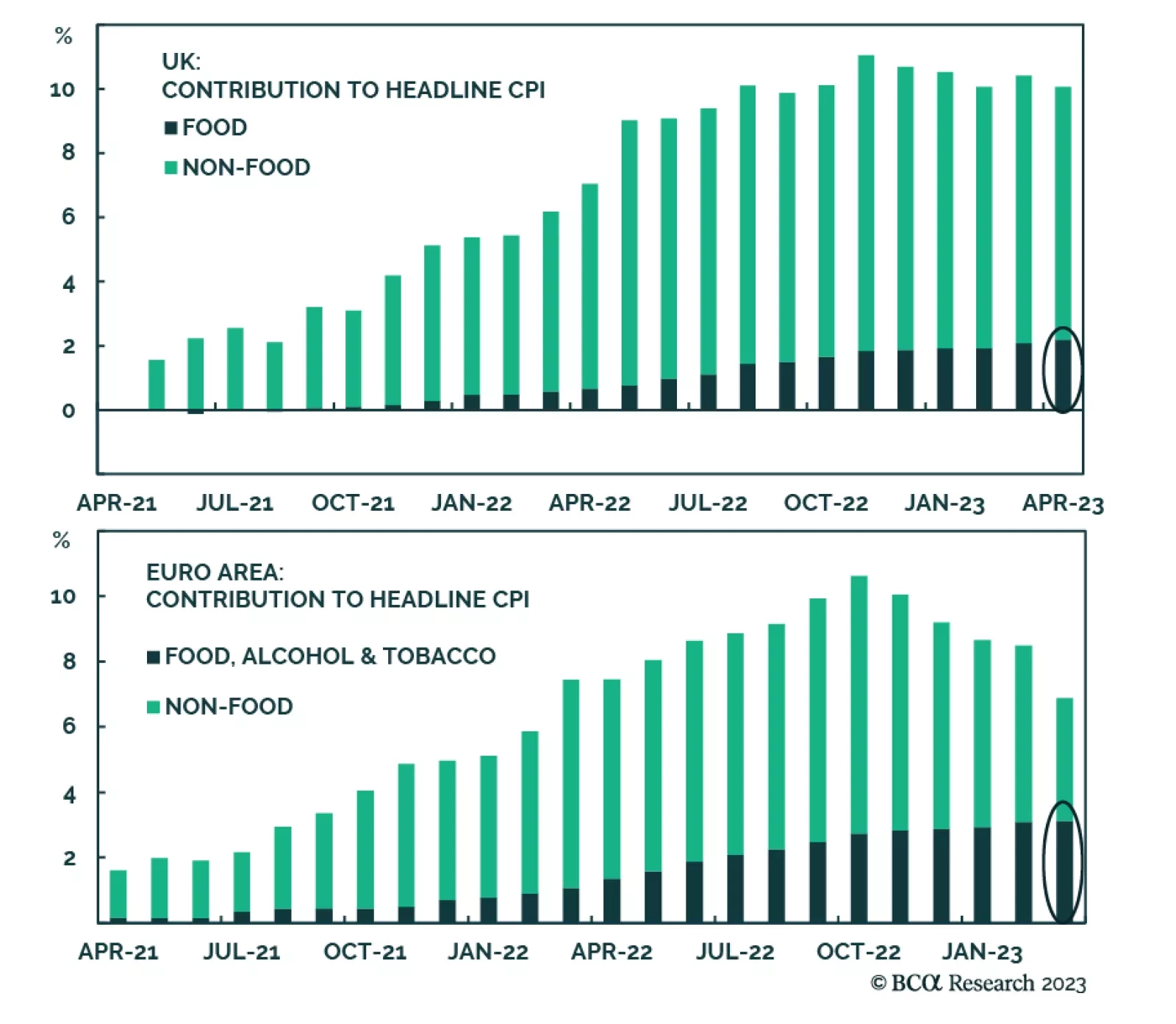

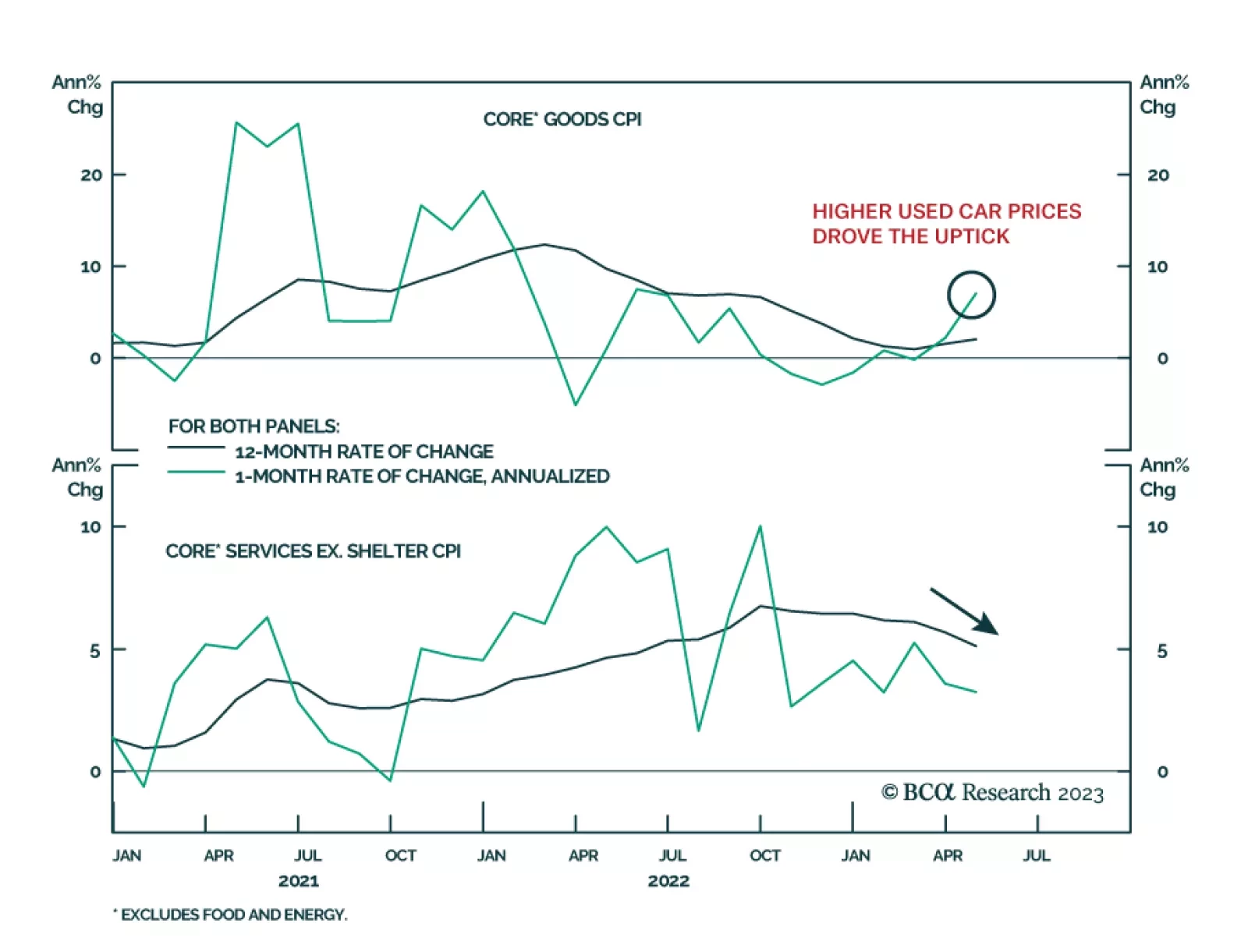

April’s CPI report was soft enough to justify a Fed pause in June. However, the overall economic data still don’t justify the magnitude of rate cuts priced into the yield curve.

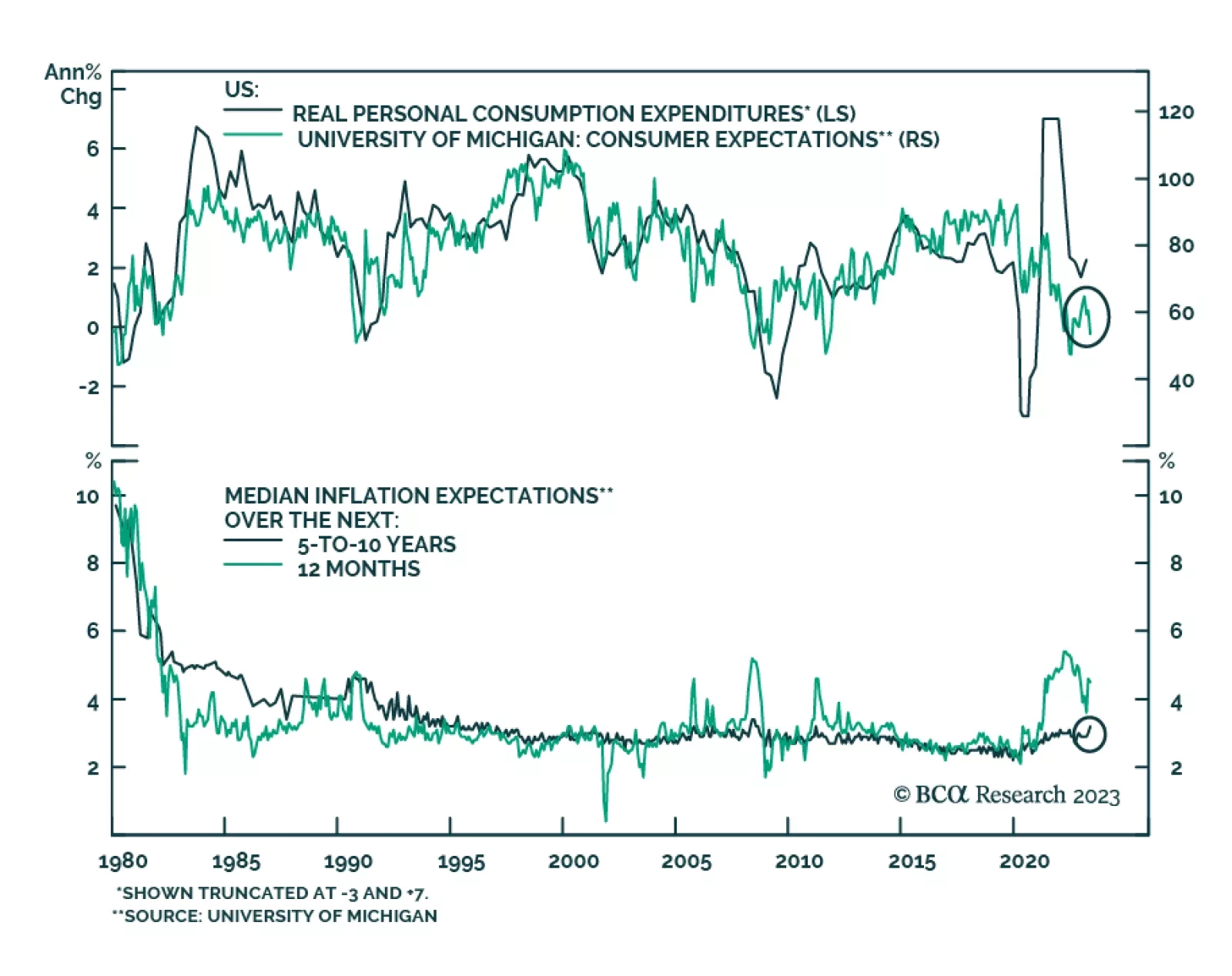

There is a 50:50 chance of experiencing a major deflationary shock in the next two years, and an even greater likelihood on a longer timeframe. The good news is that several assets provide a good insurance against this risk, and that this insurance is now cheap. Plus we highlight a compelling commodity pair-trade.

If the recession begins this year, it is unlikely to be mild, because inflation will not have fallen by enough to allow the Fed to cut rates aggressively. In contrast, if the recession starts in 2024 or later, when inflation is likely to be much lower, the Fed will be able to cushion the blow. Our base case remains a 2024 recession but the risks around that view have increased in light of recent banking stresses.