Inflation/Deflation

The Eurozone just experienced two consecutive quarters of GDP contraction. For the remainder of the year, can growth pick up or will the ECB decimate activity?

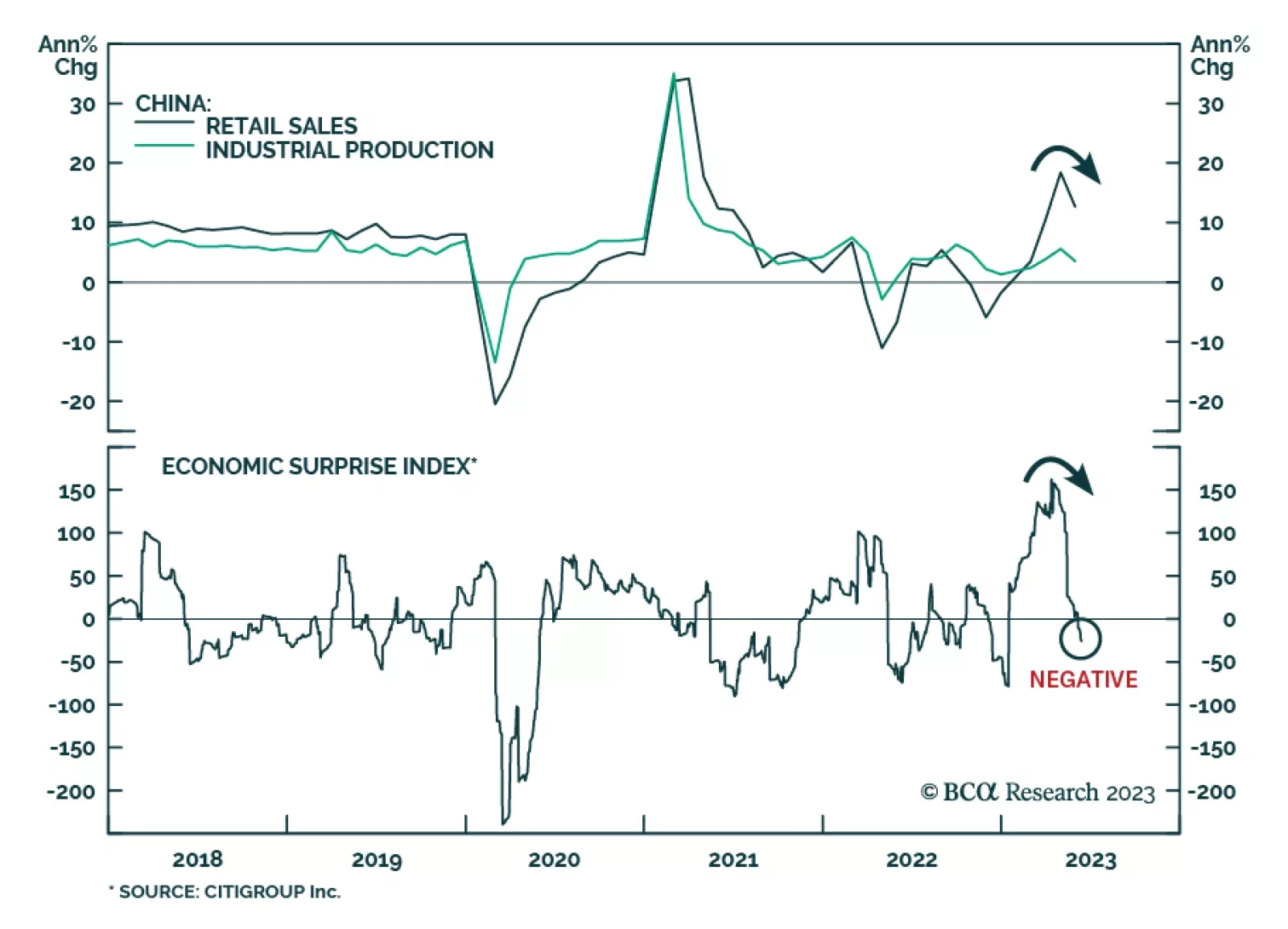

China’s economic data releases for May fell below consensus estimates. The 7.2% y/y contraction in property investment in the first five months of the year was worse than the expected 6.7% decline. The deceleration in retail sales growth from 18.4% y/y to…

According to BCA Research’s Counterpoint service, making inflation imperceptible will require making unemployment perceptible, meaning a recession. Our non-linear world often surprises our linear-thinking minds. For linear thinkers, inflation falling from…

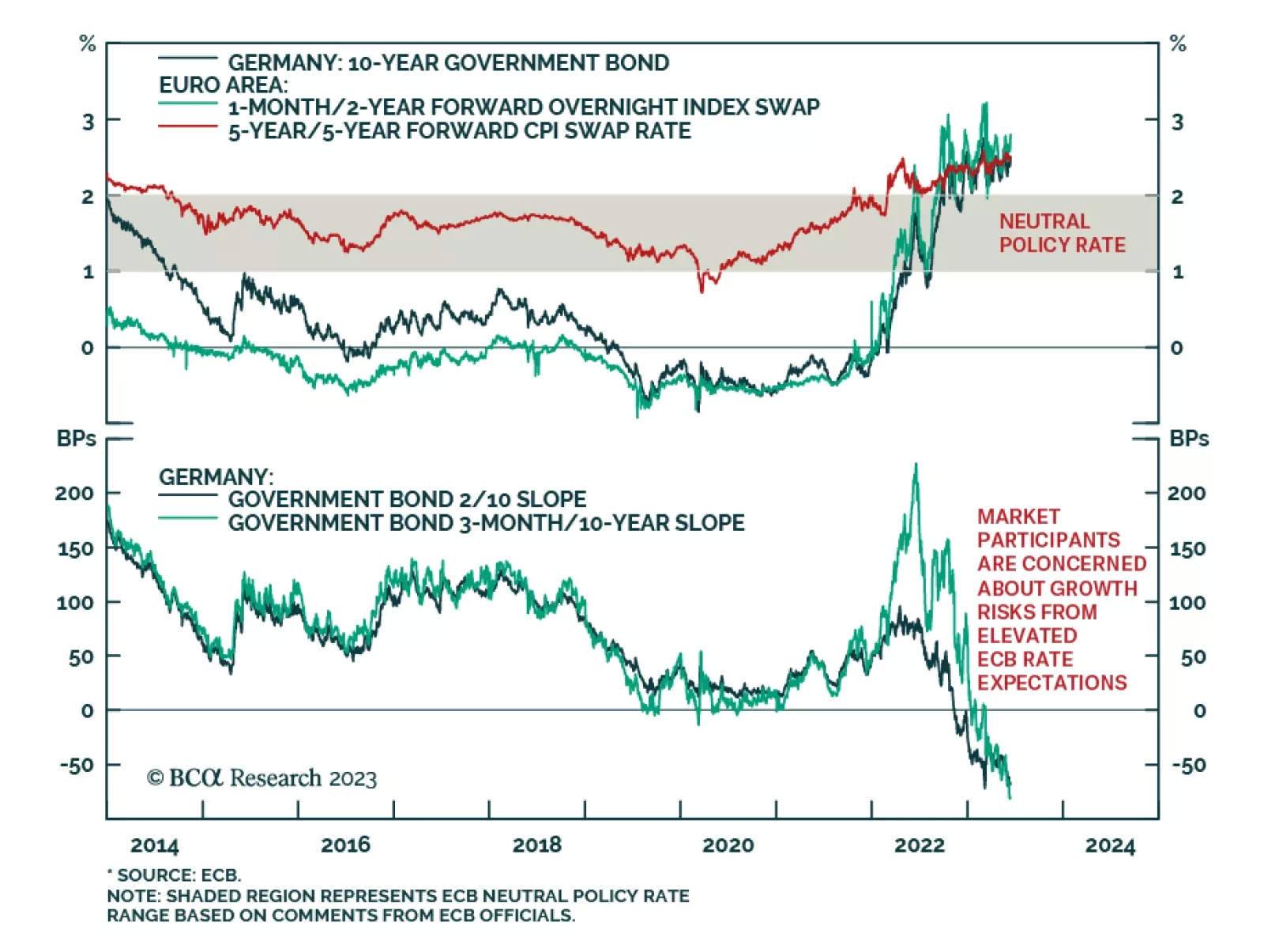

As expected, the European Central Bank (ECB) delivered a 25bps rate hike on Thursday, raising the policy rate to 3.5% — the highest since August 2001. Moreover, the central bank maintained a hawkish bias, signaling that further rate hikes are likely in…

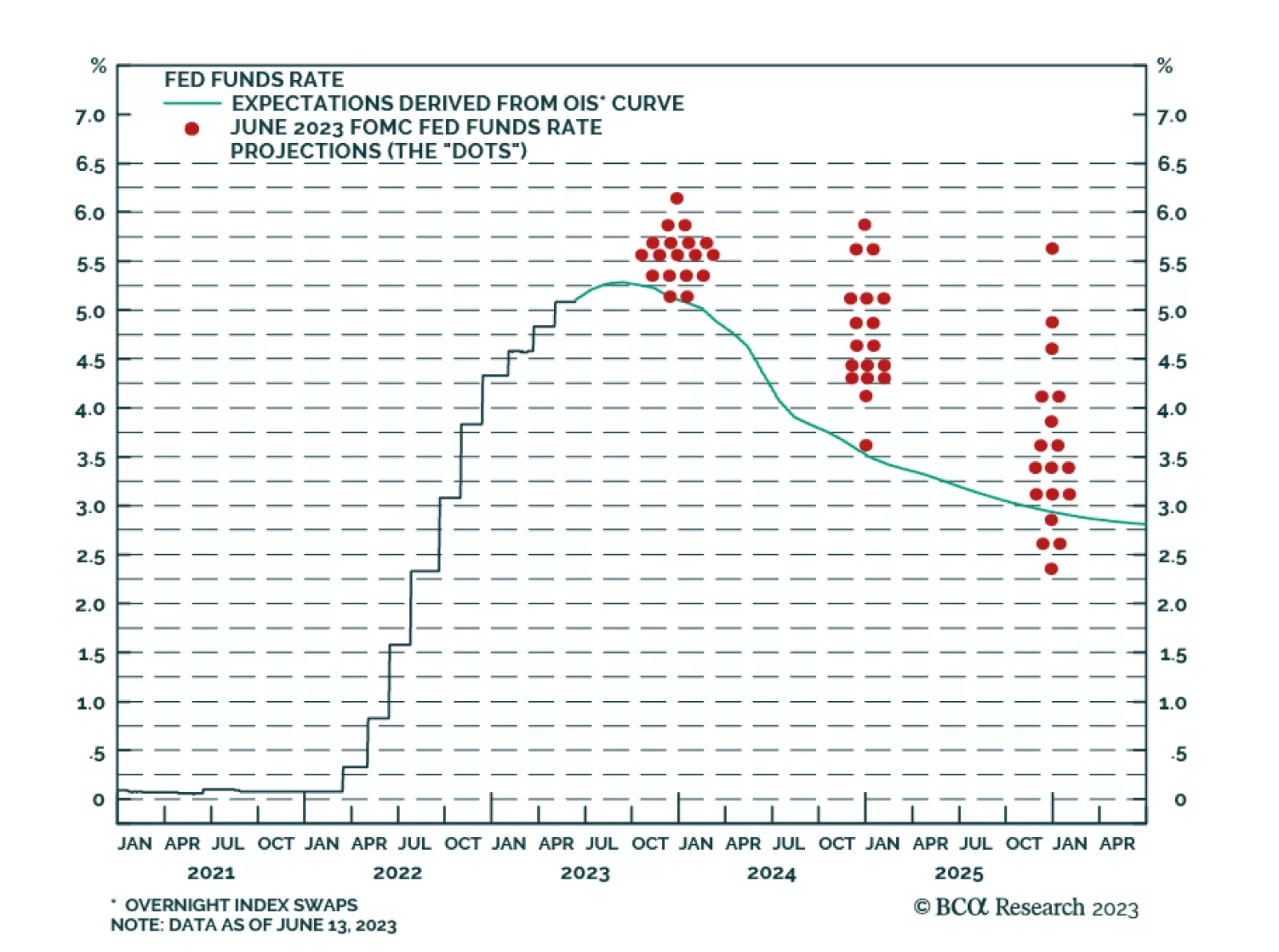

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.

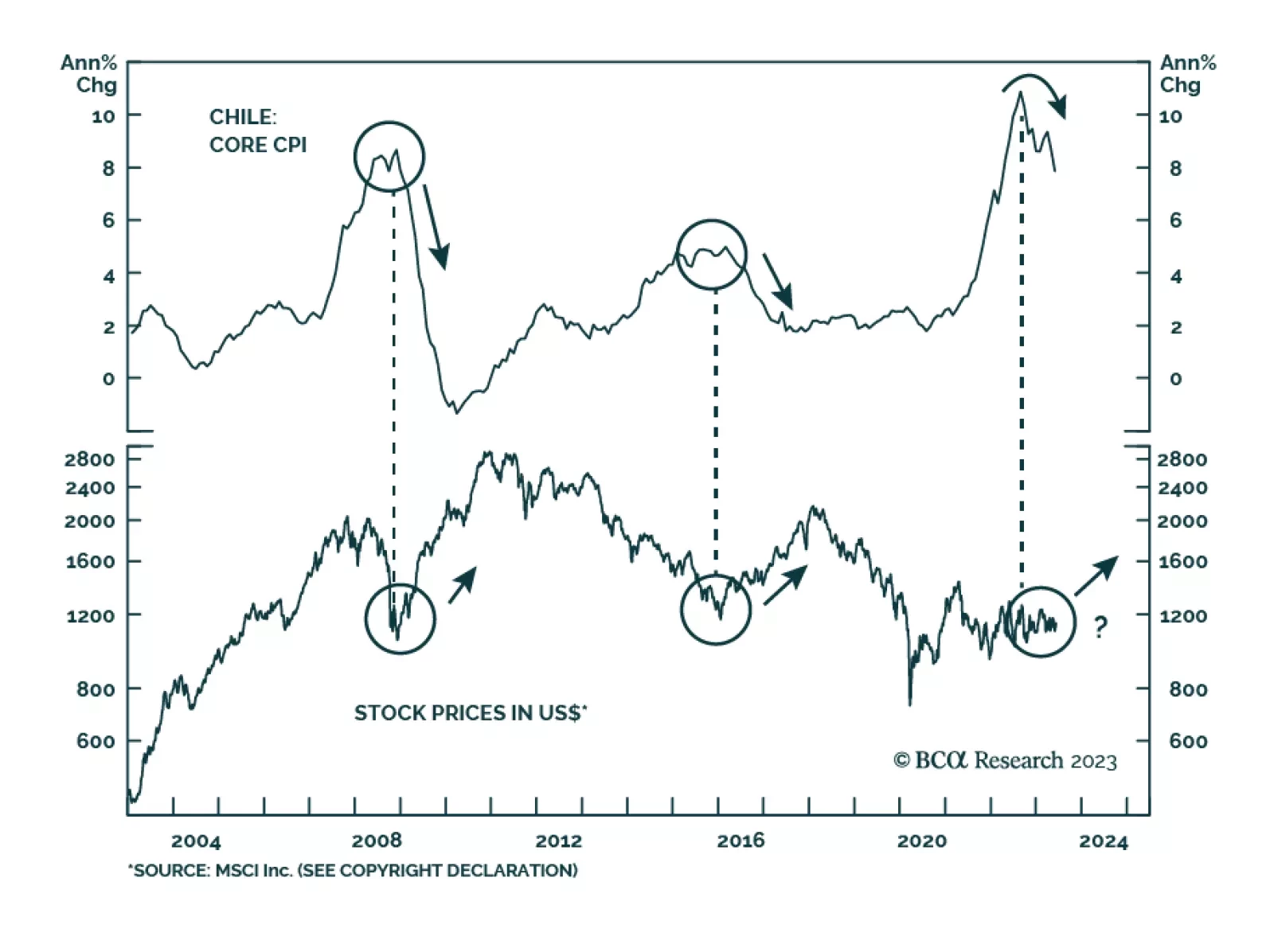

The Chilean economy is entering a recession. After two years of tightening fiscal and monetary policies, real economic growth is beginning to contract and inflation is tumbling. Our Emerging Markets strategists expect the economic contraction to deepen in…

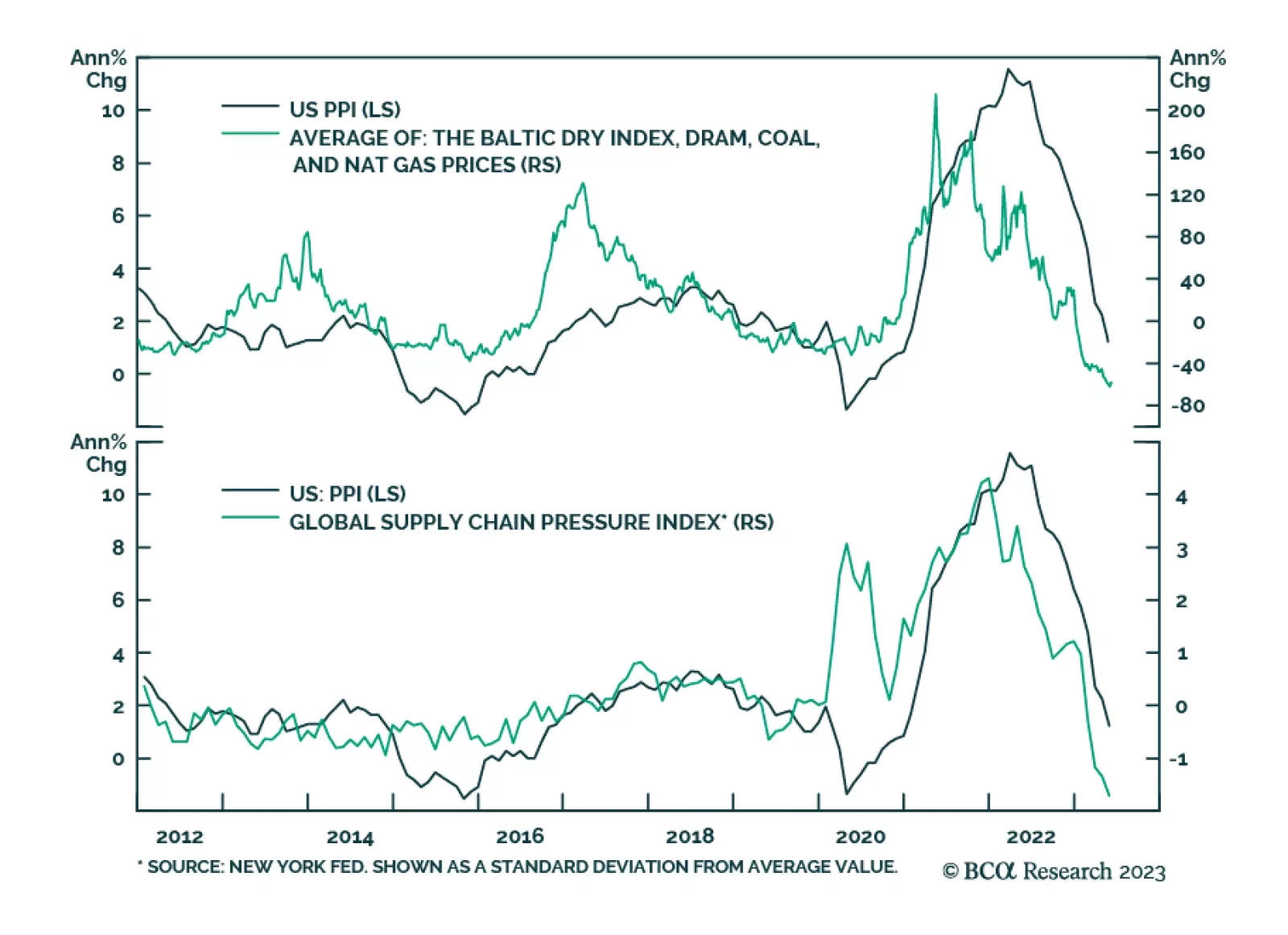

The US May PPI report indicates that pipeline inflationary pressures are cooling. Headline PPI inflation fell from 2.3% y/y to 1.1% y/y – below expectations of 1.5% y/y and the lowest since December 2020. PPI for final demand was also lower than anticipated…

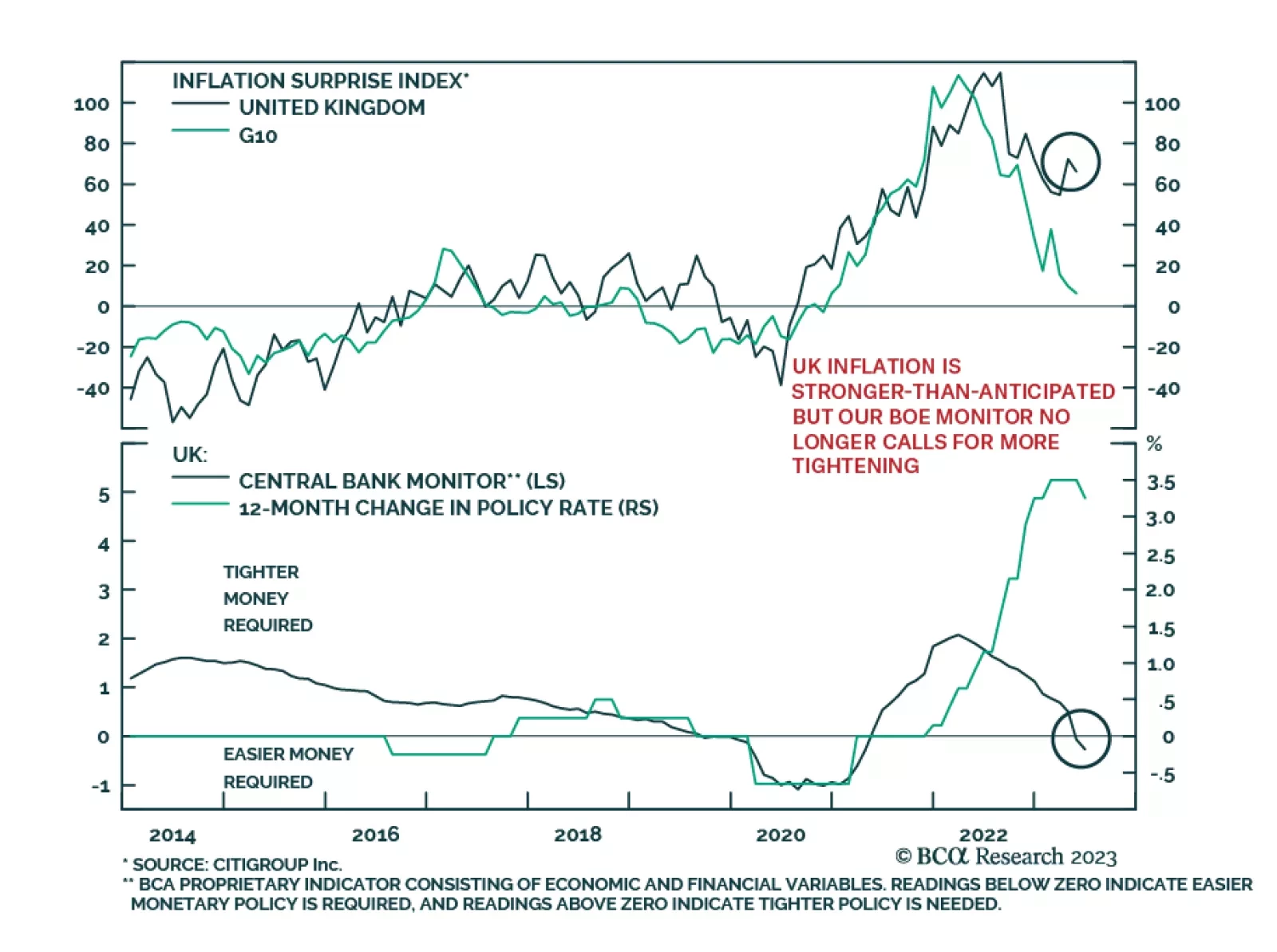

UK gilts have sold off sharply over the past month, particularly at the short end of the yield curve. The two-year yield has risen by over 100bps since mid-May, while 10-year yields have increased by just over 70bps – causing the 2-year/10-year yield curve to…

As expected, the Fed kept interest rates unchanged on Wednesday in order to give policymakers time to assess the impact of the aggressive tightening cycle. Chair Powell indicated that the decision to pause is consistent with policy getting closer to its…

As the major central banks once again mull their policy options, they face a daunting task. They must phase-transition inflation back to imperceptible, without phase-transitioning unemployment to perceptible. This report explains why this will prove impossible, and what central banks will likely prioritise. Plus: the collapsed complexity of the recent stock market rally signals excessive trend-following. Until the complexity normalises, we are reluctant to chase the rally.