Inflation/Deflation

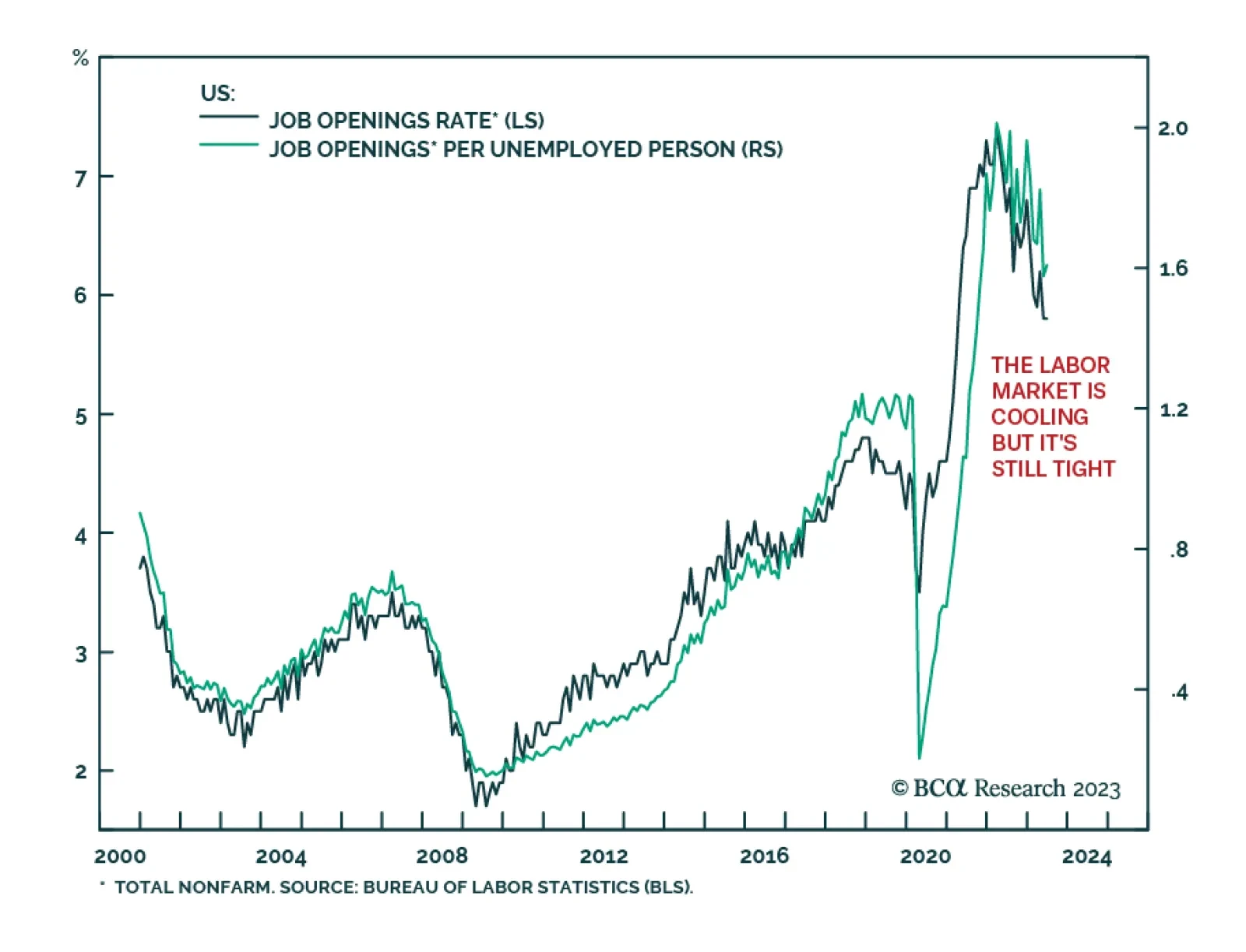

The ADP Jobs Report delivered a better-than-anticipated signal about the US labor market on Wednesday. The 324 thousand increase in private employment in July beat expectations of a 190 thousand rise and marks the second highest reading in a year following…

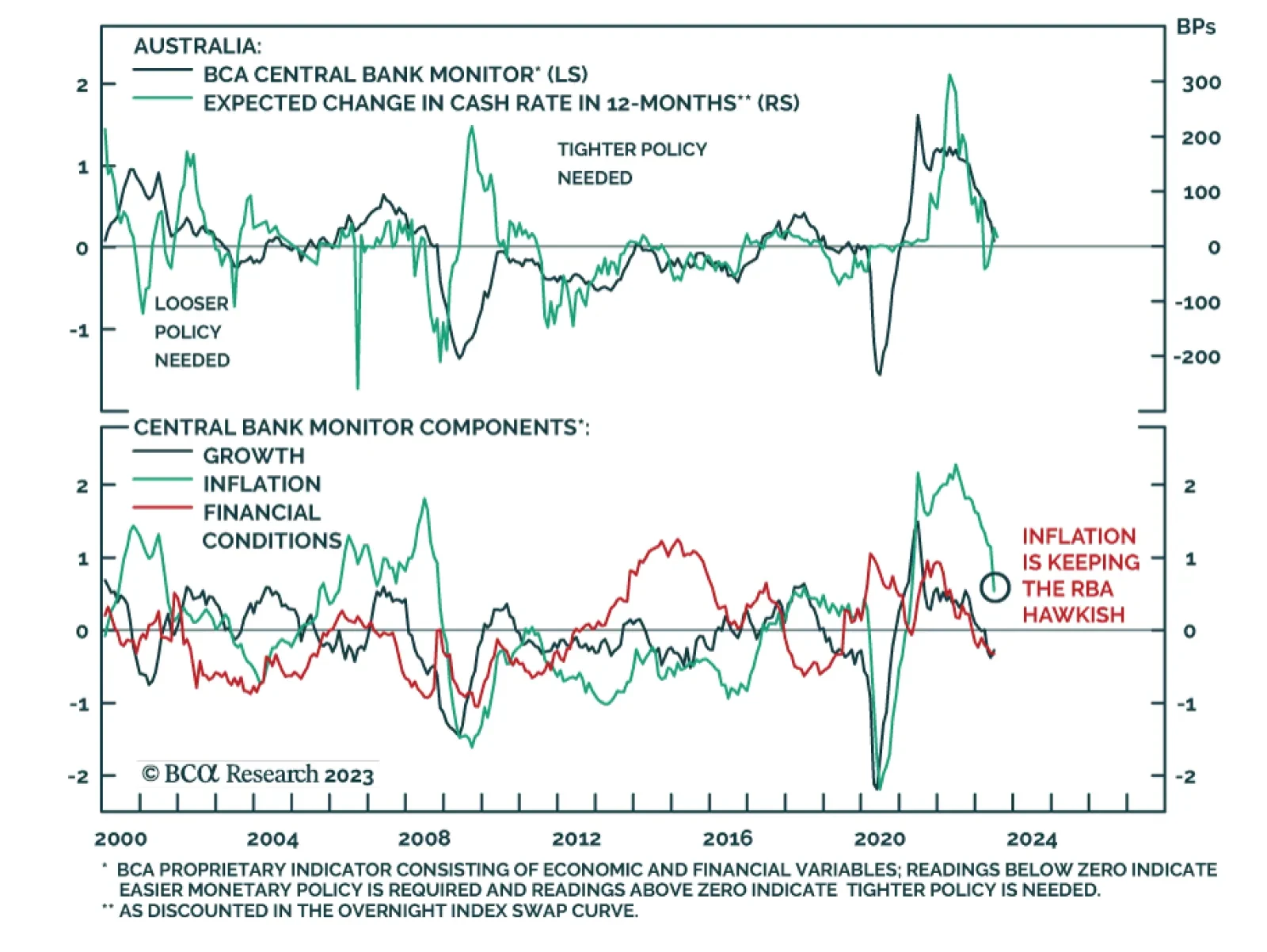

The Reserve Bank of Australia kept interest rates on hold at 4.1% on Tuesday, surprising expectations of a 25bps increase. Governor Philip Lowe’s statement underscores that the decision “will provide further time to assess the impact of” the 4 percentage…

History suggests that a “soft landing” is highly unlikely after such an aggressive Fed tightening cycle. The rally could continue for a little longer but, on the 12-month horizon, market risks are very skewed to the downside.

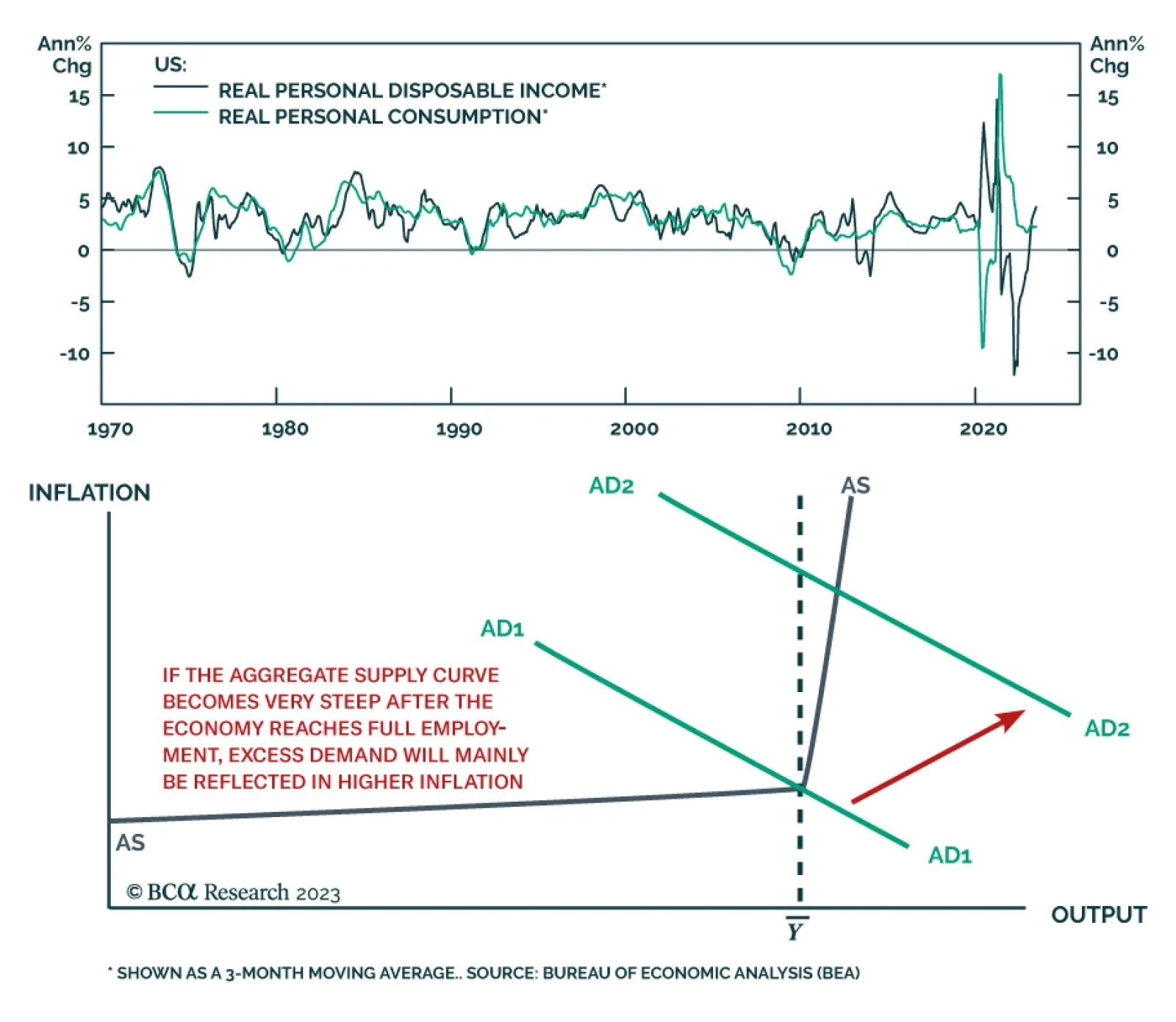

According to BCA Research’s Global Investment Strategy service, it is too early to conclude that the Fed can stop raising rates. Consumption and real income growth are highly correlated. If inflation continues to fall, real wages will rise further. If that…

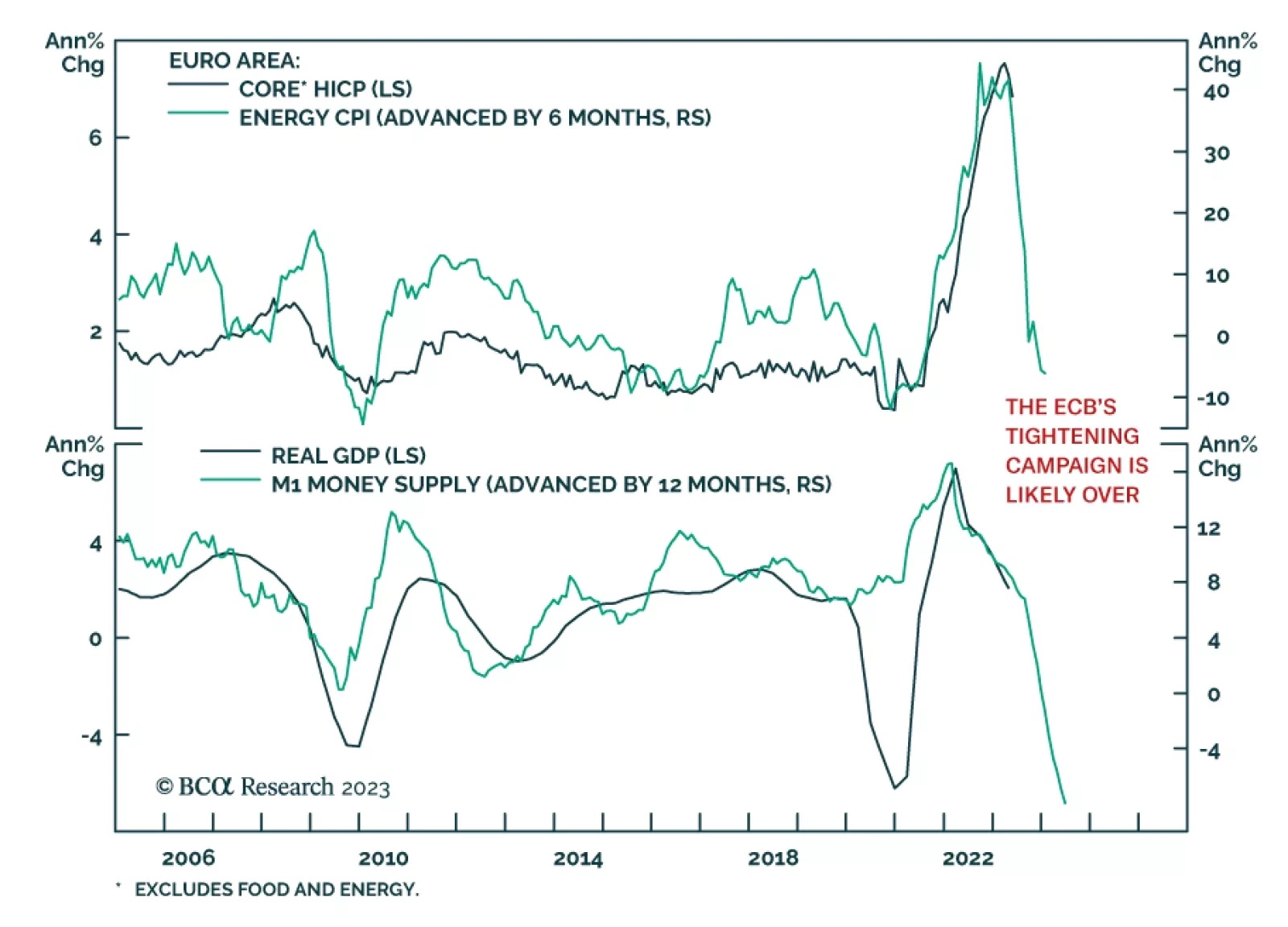

The Eurozone economy returned to expansion in the second quarter with real GDP rising by 0.3% q/q – beating expectations of 0.2% q/q. This follows an upwardly revised 0.0% in Q1 and a 0.1% contraction in Q4 2022. In particular, Ireland (+3.3%) and Lithuania,…

The ECB’s tone has changed decisively. Intransigent forward guidance is gone; data dependency is in. What does this transition mean for the path of European interest rates and the euro?

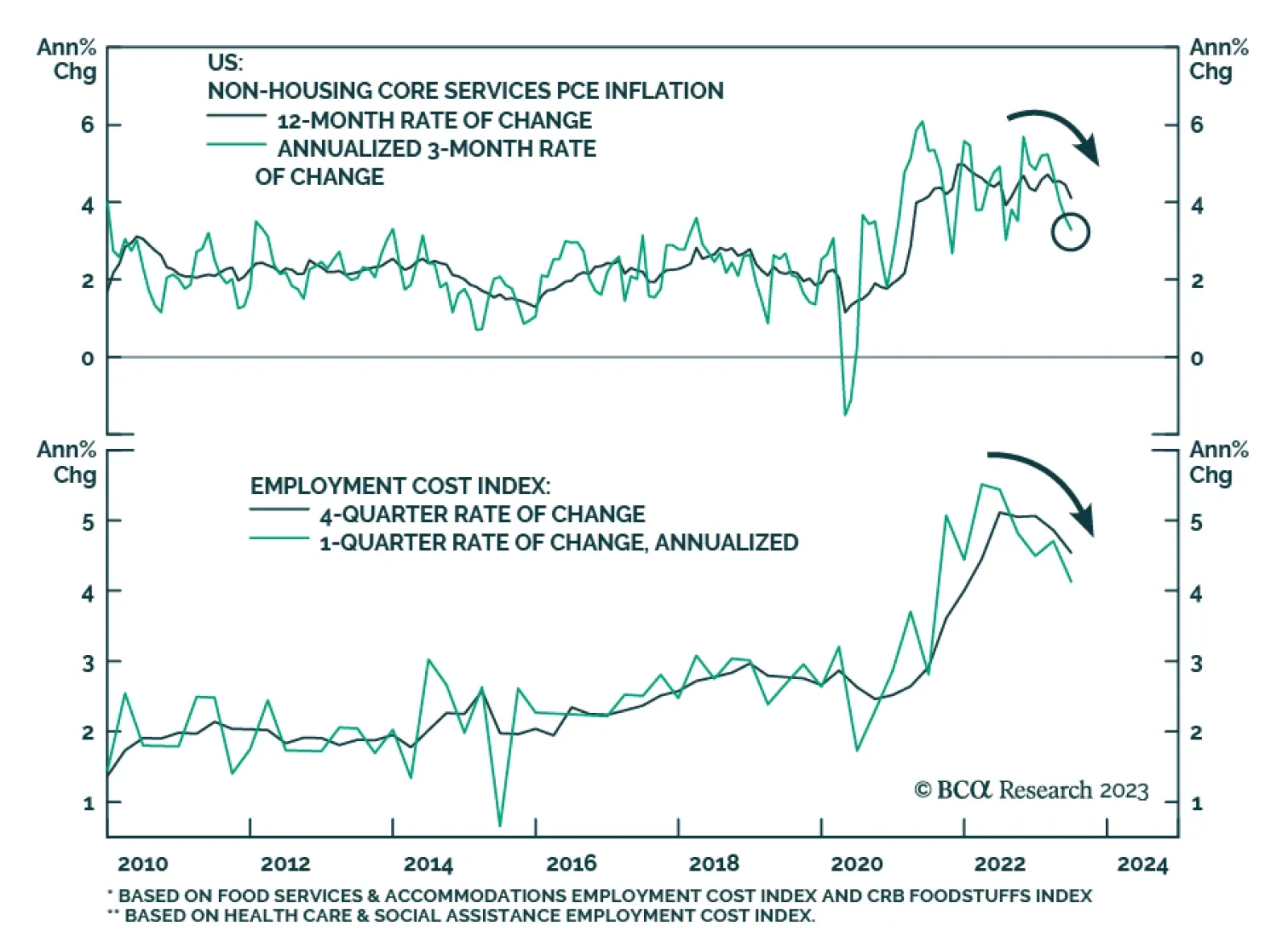

US economic data released on Friday continued the string of good news about the US economy. On the inflation front, core PCE inflation – the Fed’s preferred gauge of underlying price pressures – softened to 0.165% m/m in June. On an annualized basis, this…

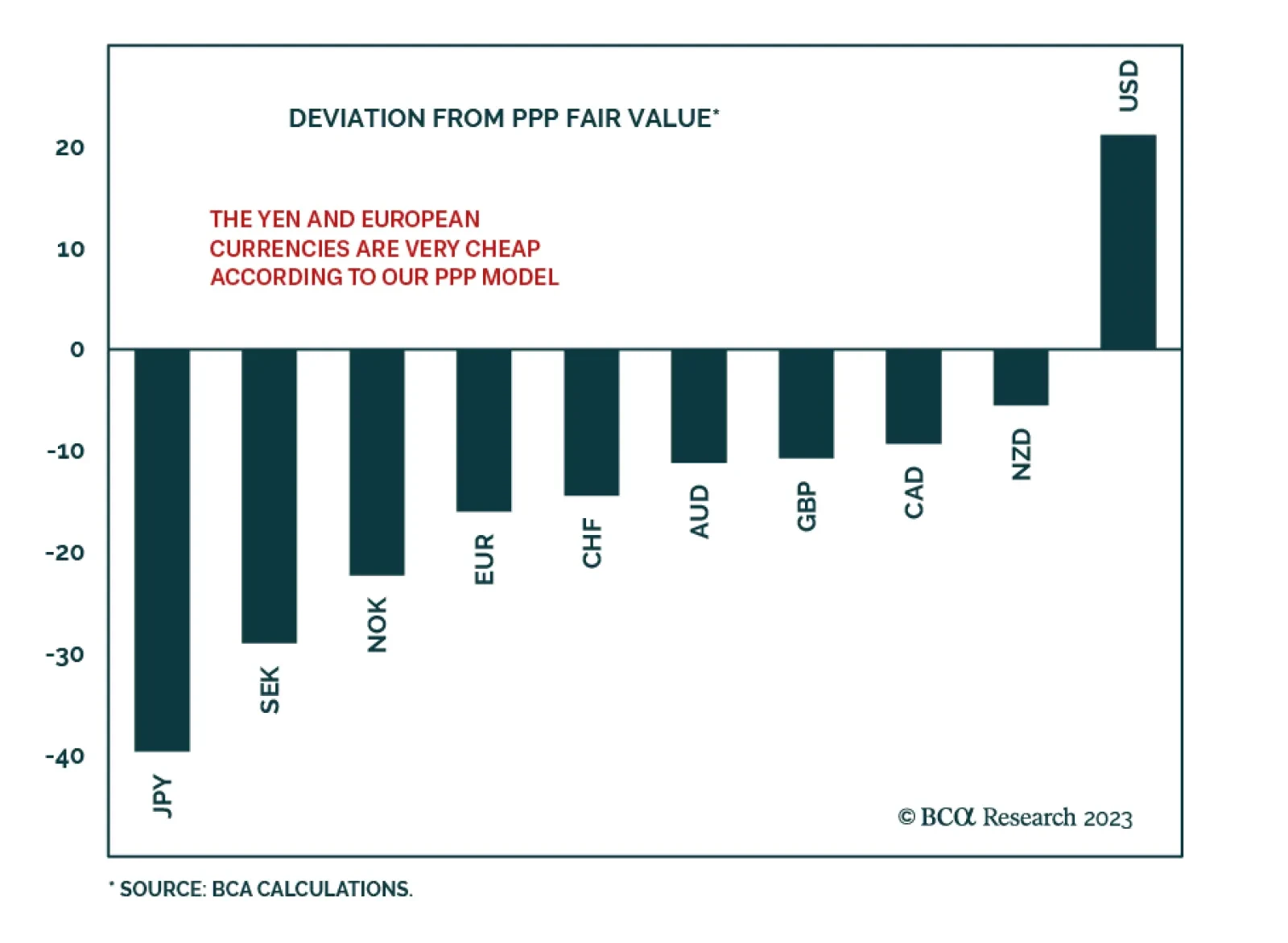

BCA Research’s Bank Credit Analyst service recently featured currency valuation models developed by our Foreign Exchange Strategy service. According to these models, the US dollar is extremely overvalued and thus vulnerable to a structural decline. When…

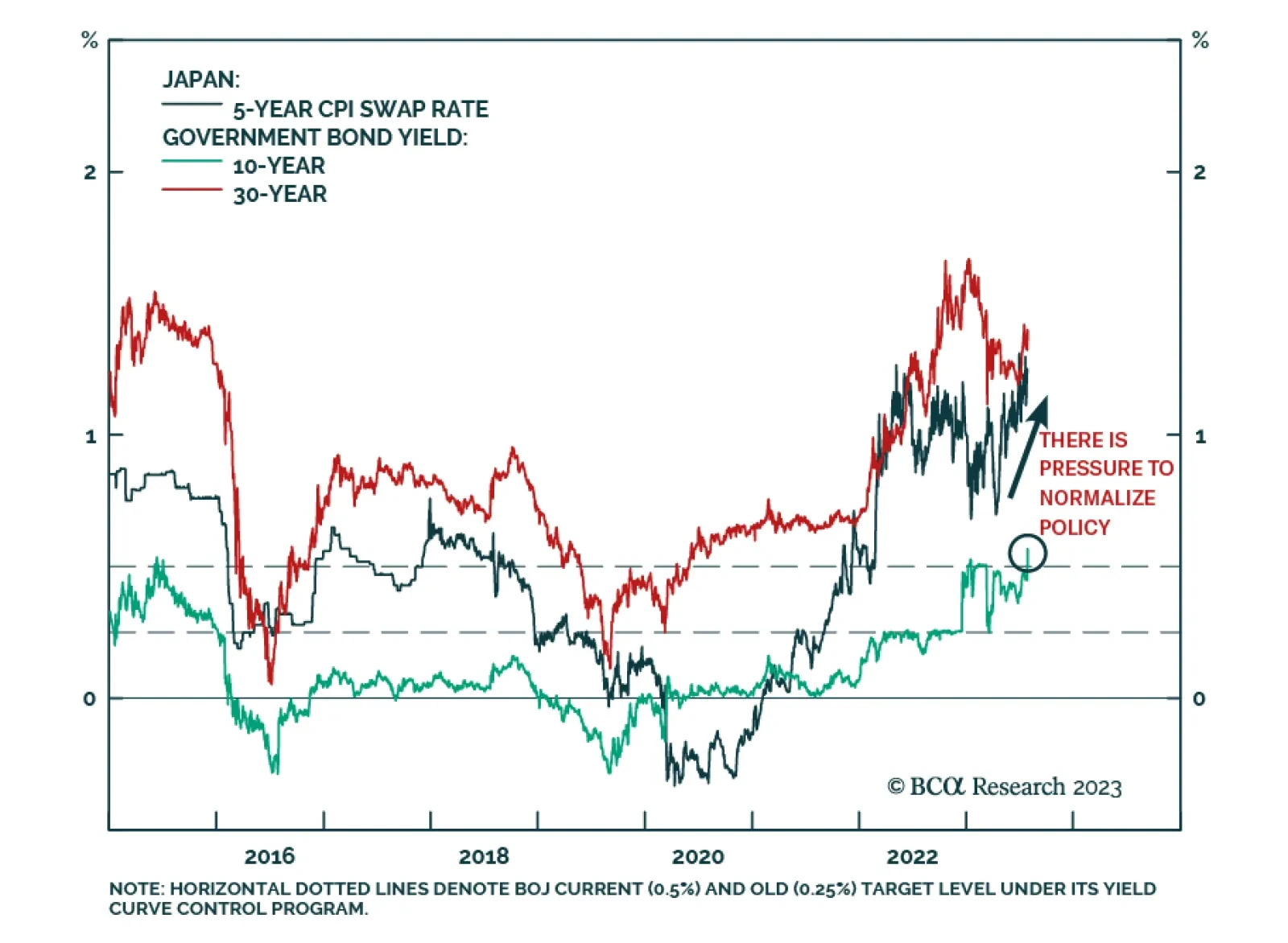

On Friday, the Bank of Japan announced an important tweak to its yield curve control (YCC) program. Although it maintained the 0.5% cap on 10-year bond yields, it indicated that it will manage the program with “greater flexibility” such that the 0.5% level is…

A look at recent US data on economic growth and inflation, with an update on the implications for monetary policy and bond yields.