Income Inequality and Populism

The cyclical economy is slowing today. Republicans are now more likely to win a full sweep, crack down on immigration and trade, and at least modestly stimulate the economy. Uncertainty and volatility will rise.

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.

Europe did not witness a major policy reversal. Inflationary pressures are coming down, enabling the ECB to cut rates and European states to maintain soft budgets. Geopolitical challenges ensure that European parties continue to cooperate on national defense, economic security, and energy security.

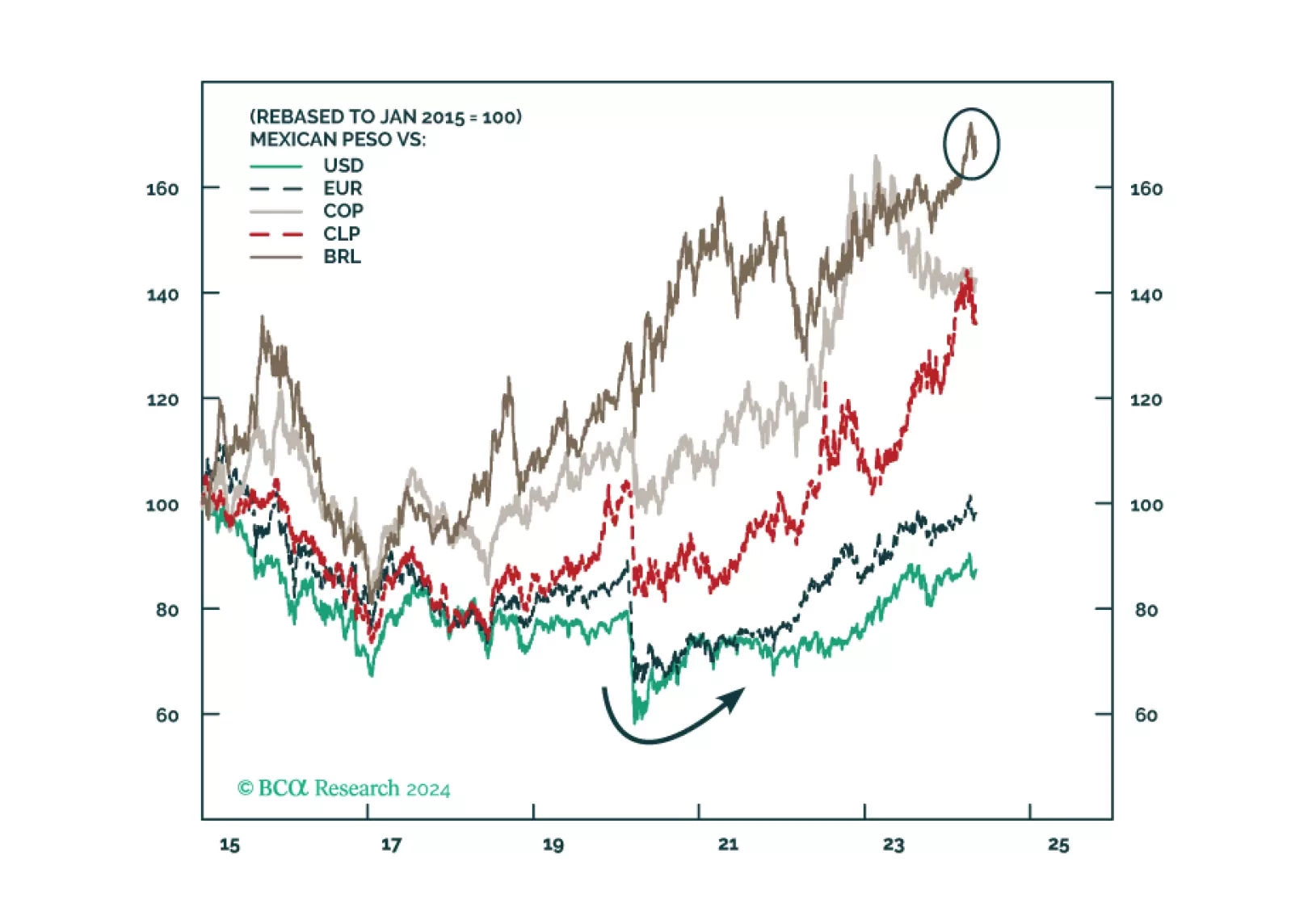

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

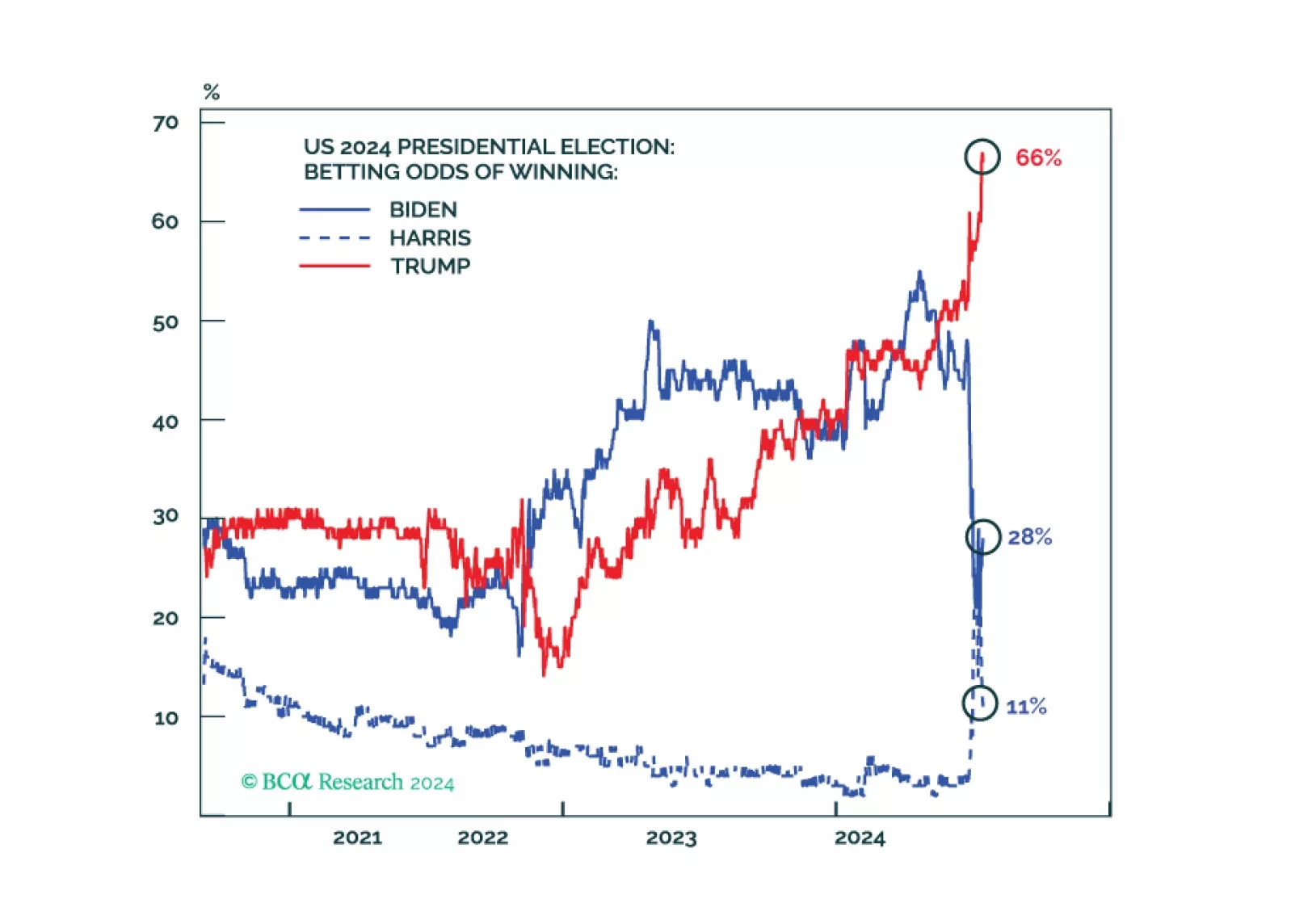

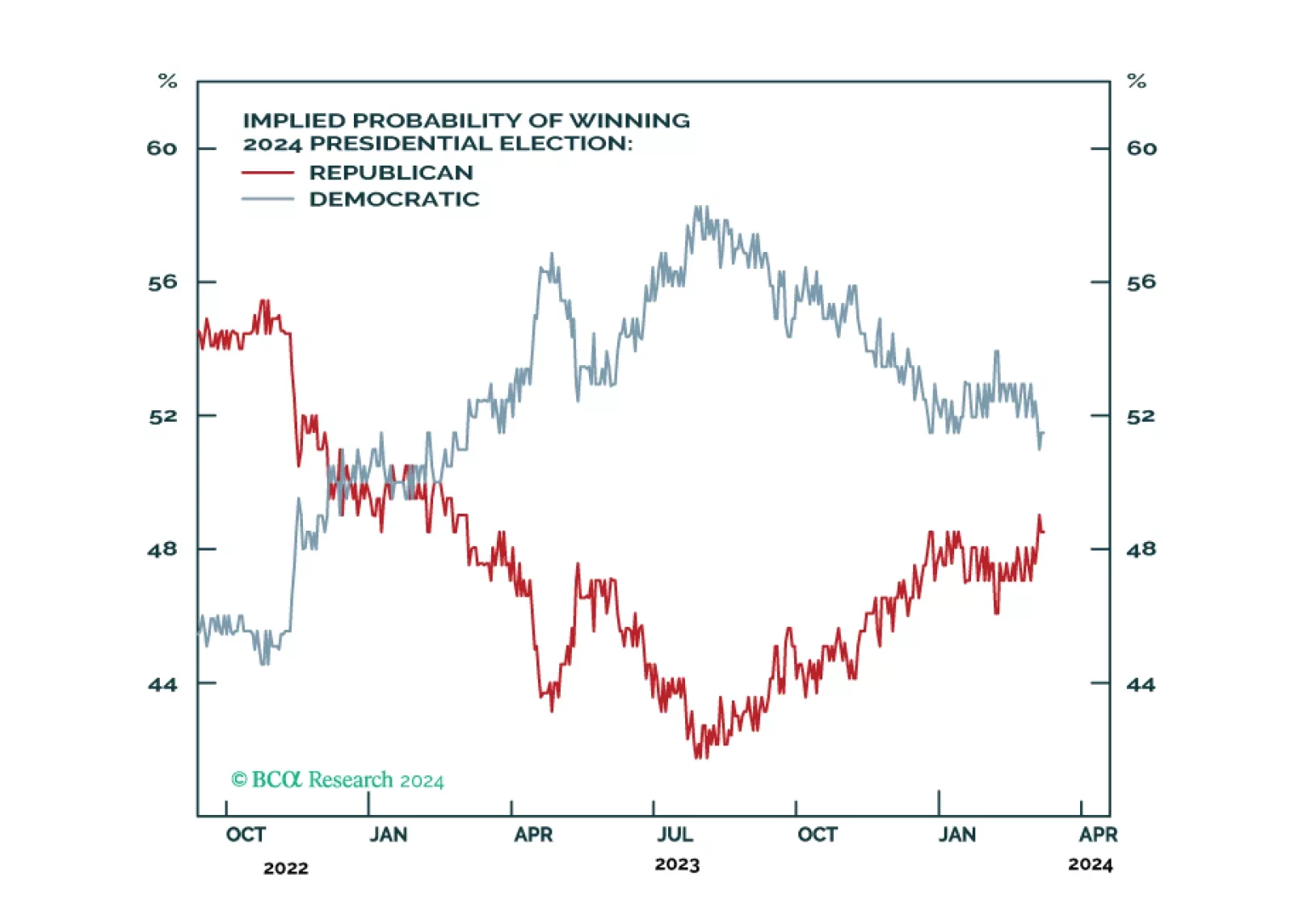

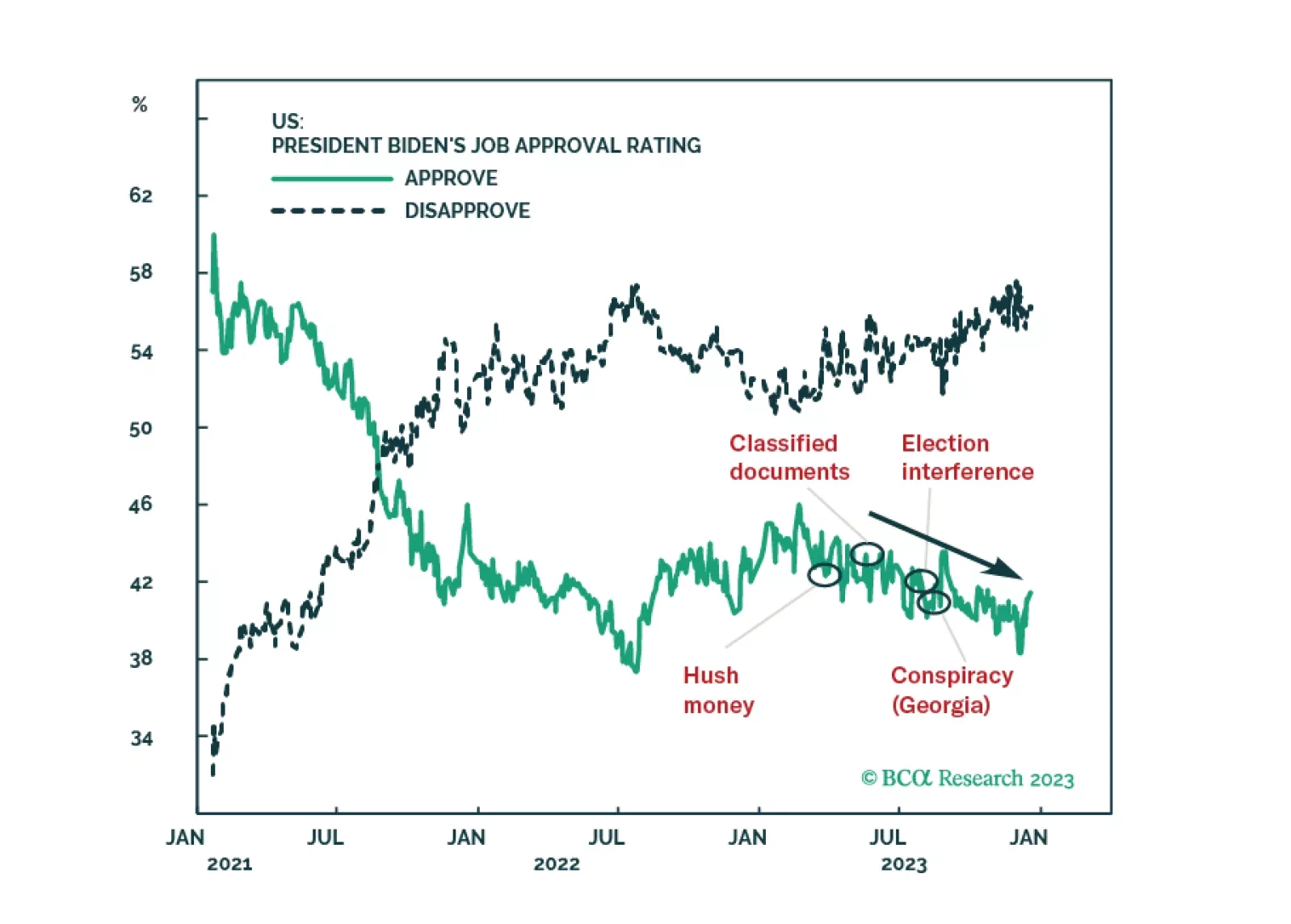

Democrats are still slightly favored for reelection as the incumbent party is presiding over a growing economy. However, Biden’s strong showing in the primary election is not lifting his popular approval yet, and that is a worrying sign. Policy uncertainty should rise sharply, which is marginally negative for the stock market.

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.

Democrats remain favored for reelection in 2024, which implies gridlock and policy status quo in 2025. That is not negative for stocks in the near term. However, economic, political, and geopolitical risks will escalate from here, causing volatility.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

The market will eventually be forced to react to rising odds of a sharp US national policy reversal. Investors should overweight government bonds and defensive equity sectors.

The Republican Party’s odds of winning the 2024 election will benefit, if anything, from state courts’ attempts to exclude President Trump from primary or general election ballots. Higher odds of a change of ruling party will increase stock and bond market volatility.