High-Yield

Our Portfolio Allocation Summary for June 2024.

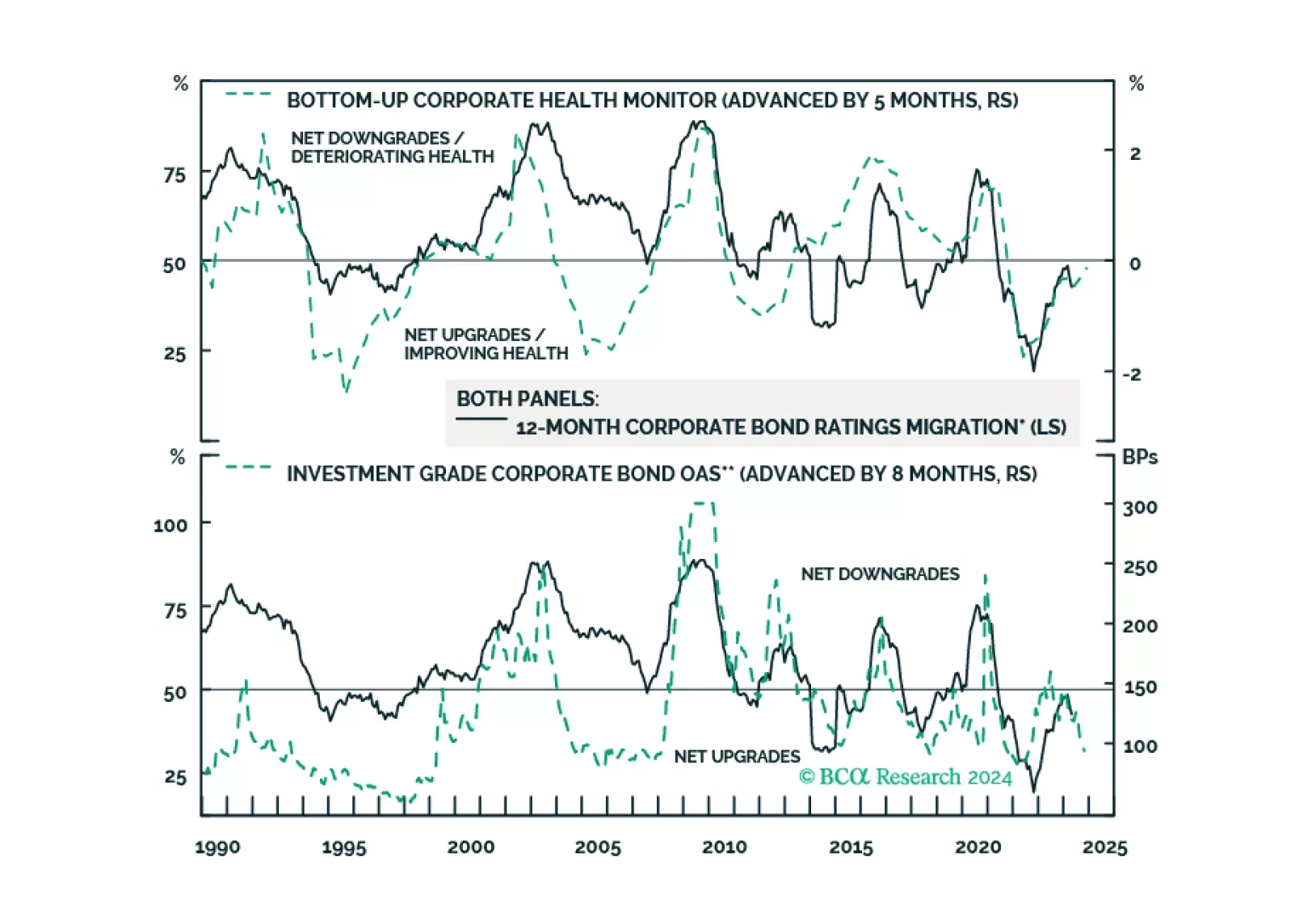

Nonfinancial corporate balance sheets are generally in good shape, but there are signs of deterioration at the bottom-end of the credit spectrum. We present evidence showing that credit deterioration at the bottom-end of the credit spectrum has a habit of migrating upwards.

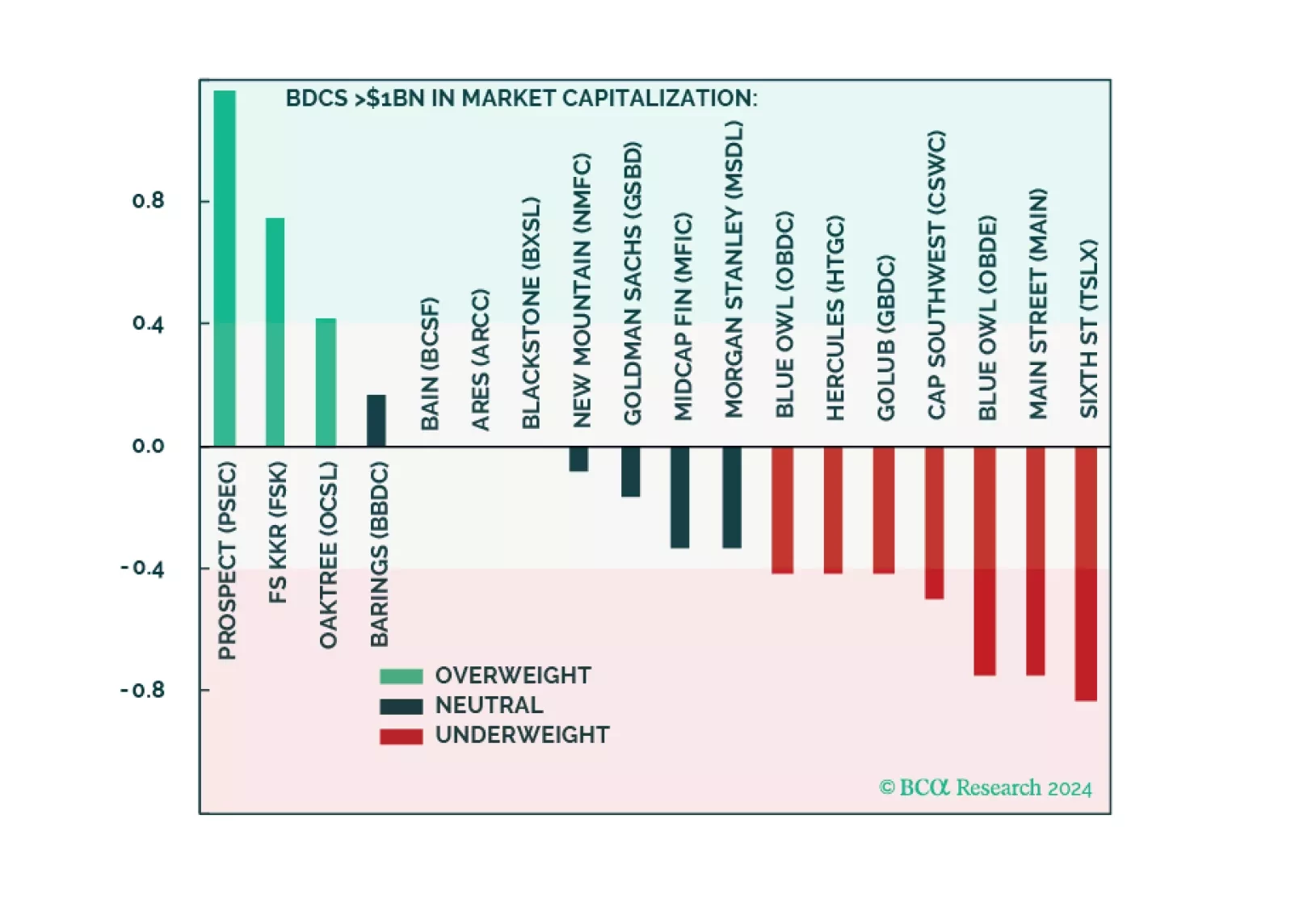

We are positive Private Credit but currently underweight Public BDCs. Today’s market pricing and sentiment in BDCs are excessively optimistic. Long-term investors should await a better entry point. Traders may find an attractive short. This report also peels back the Public BDC onion and presents over/underweights across individual BDCs via our filtering methodology.

Also included at the end of this report is an updated presentation titled 'Private Credit: Drivers Of The Boom And Understanding Risks On The Horizon,' recently presented at GII’s Private Credit Roundtable in Australia. It features updated charts and additional analysis.

Our Portfolio Allocation Summary for May 2024.

Our Portfolio Allocation Summary for April 2024.

Our Portfolio Allocation Summary for March 2024.

We rank the US spread sectors in terms of risk versus reward.