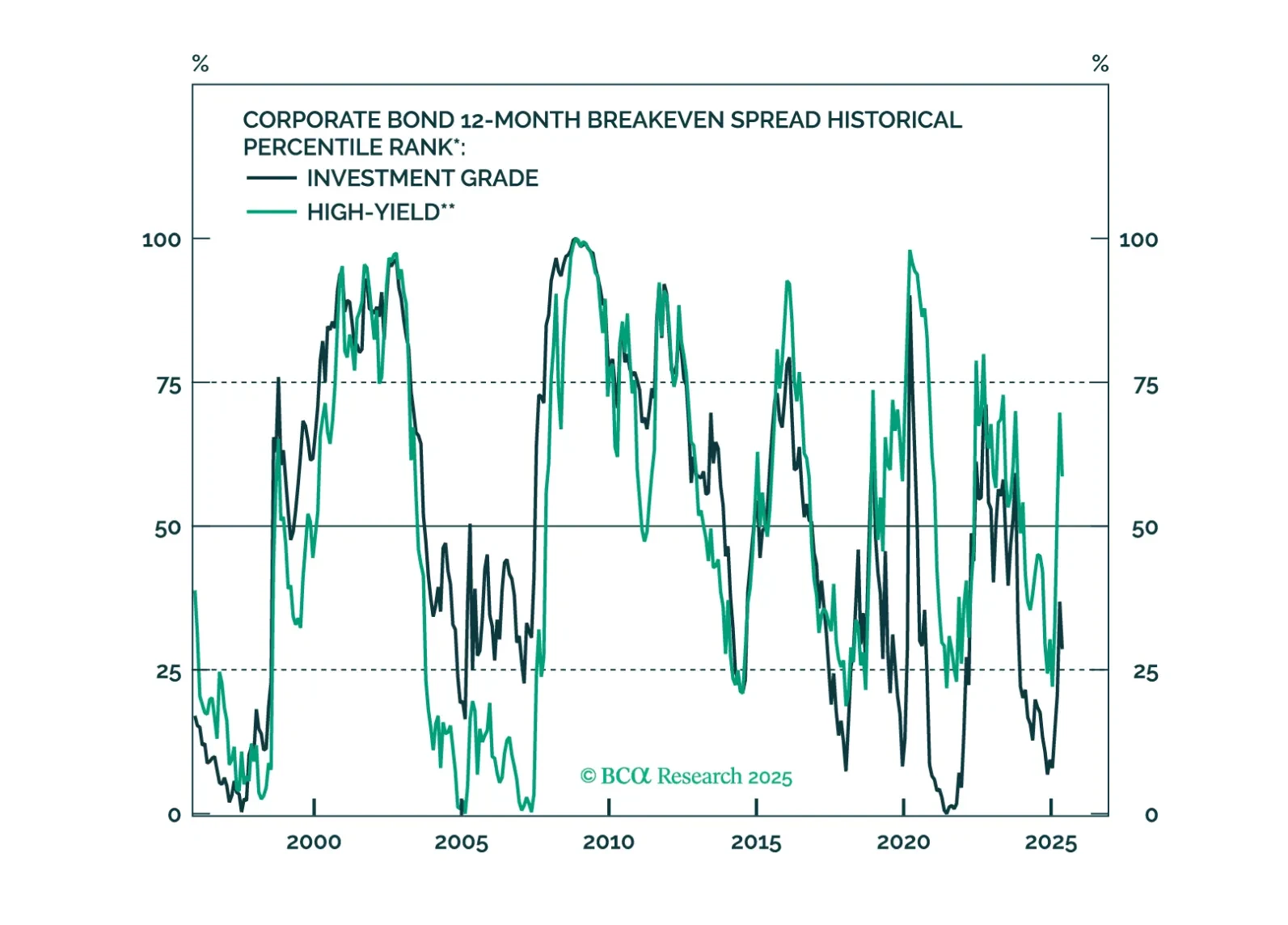

High-Yield

This year’s corporate bond sell off has hit high-yield more than investment grade, and high-yield spreads have turned relatively more attractive as a result.

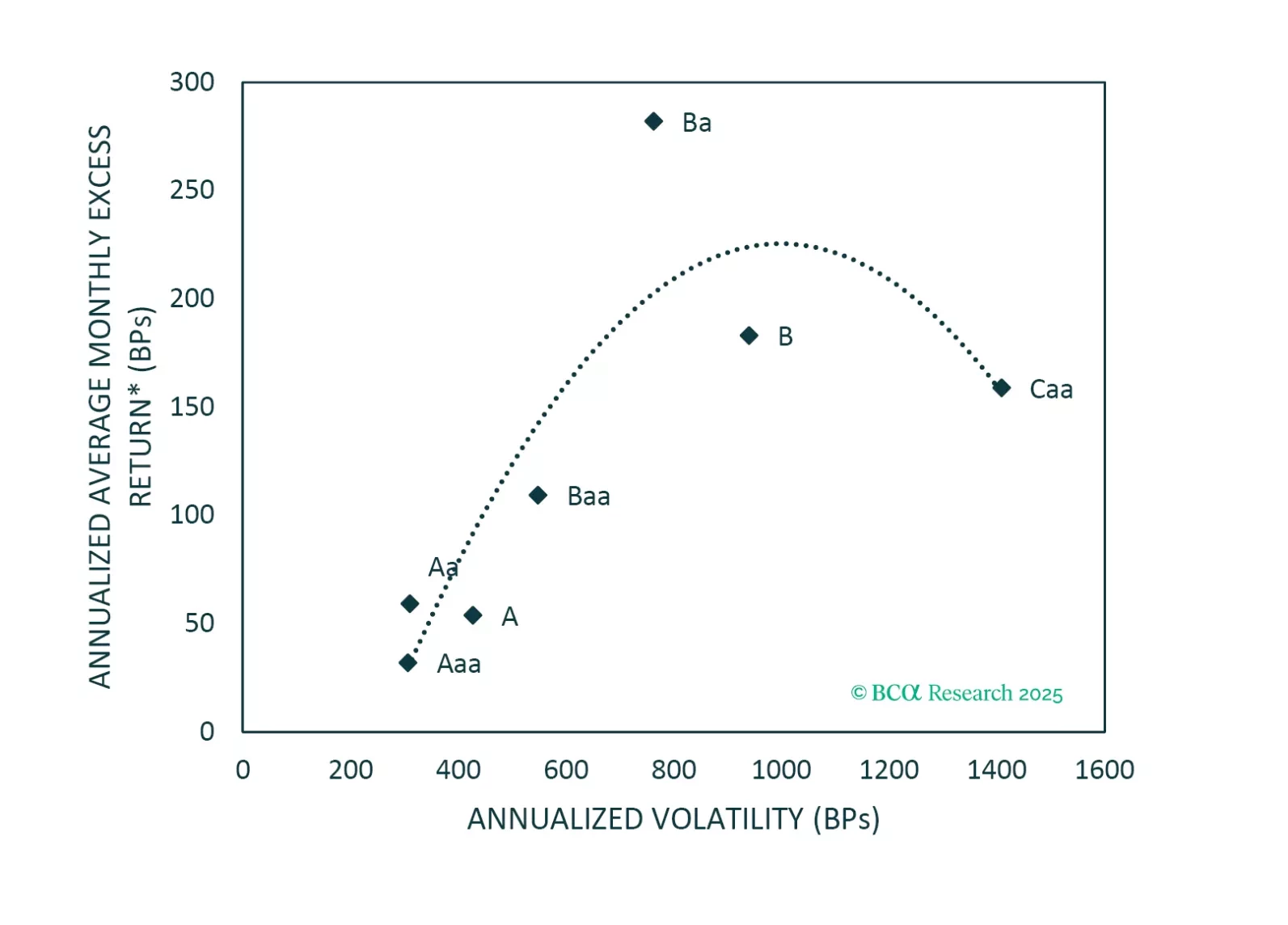

An analysis of historical data shows that Ba-rated bonds outperform other corporate credit tiers in the long-run on a risk-adjusted basis. That said, today’s fragile macro environment warrants a more cautious allocation.

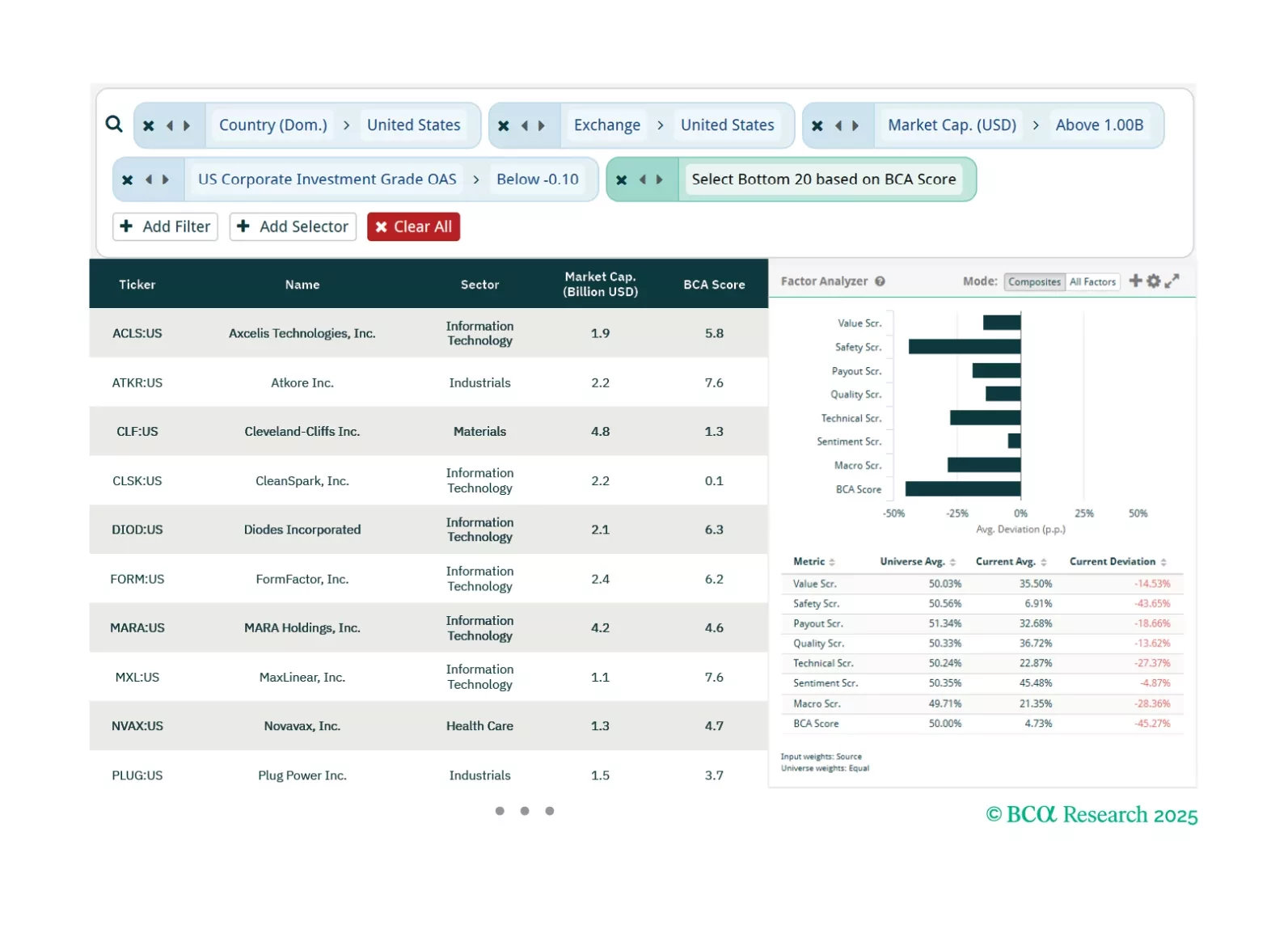

This week, our three screeners cover equity plays in US OAS Spreads, US Exceptionalism, and “DIVE”.

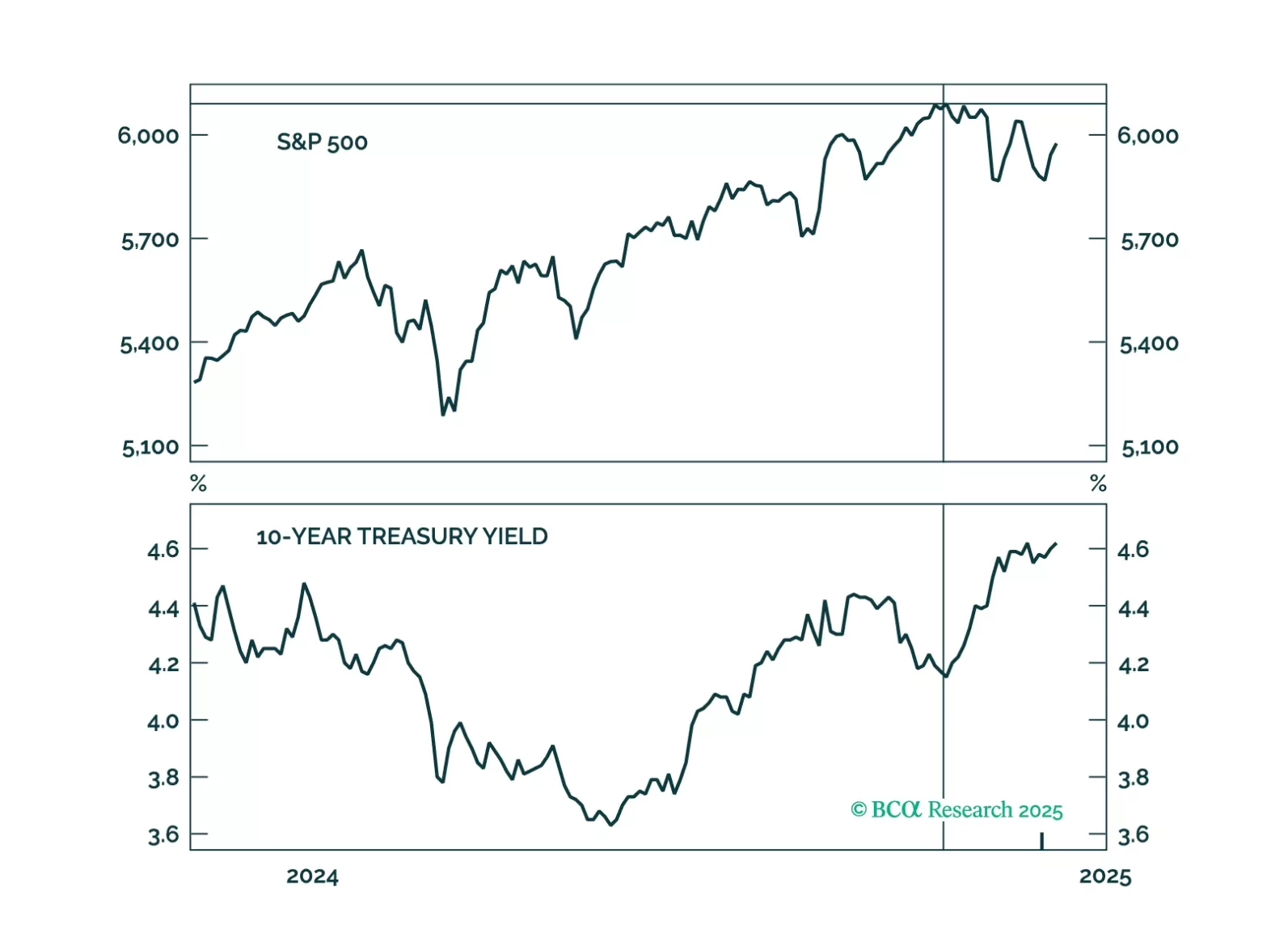

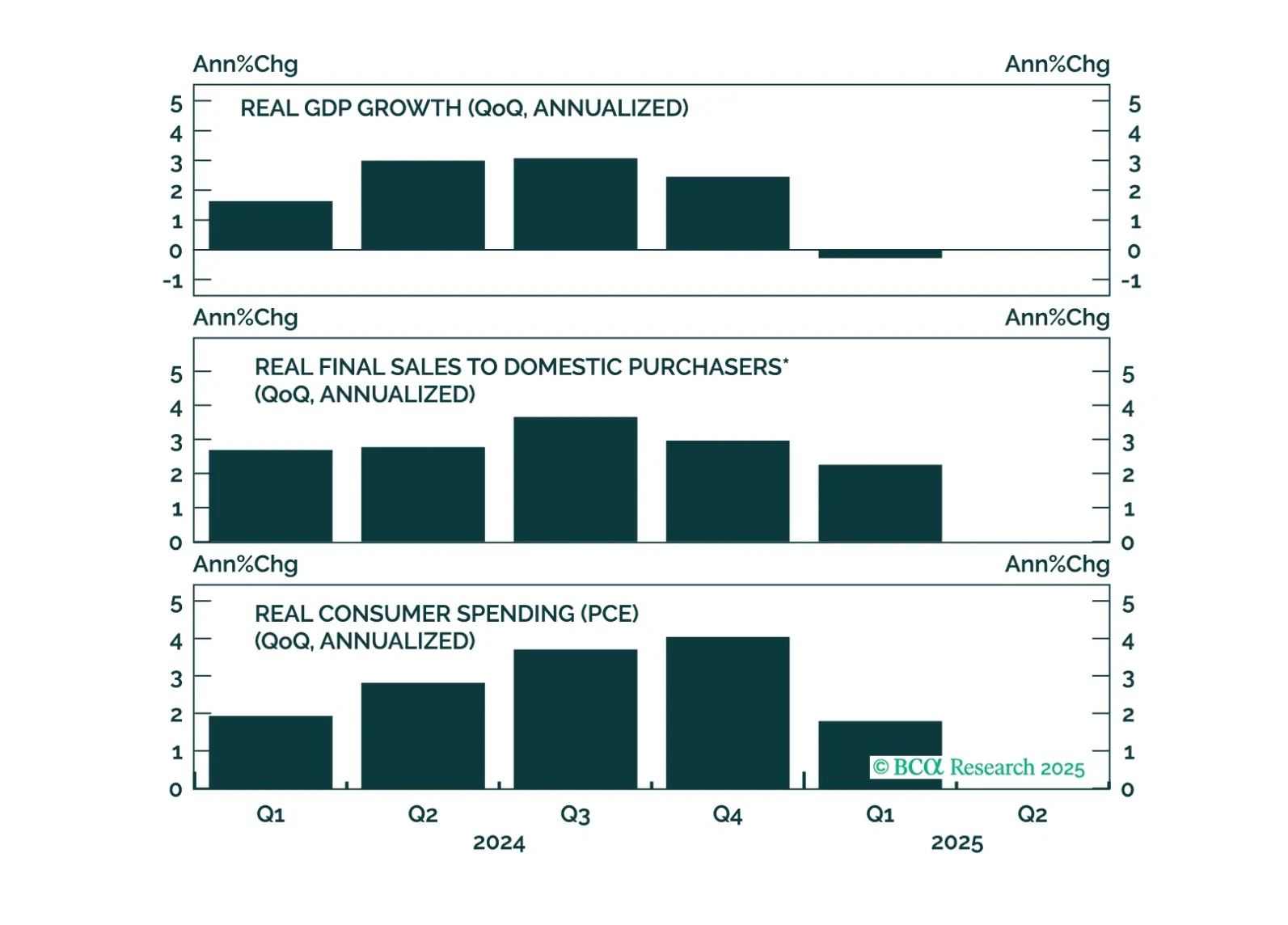

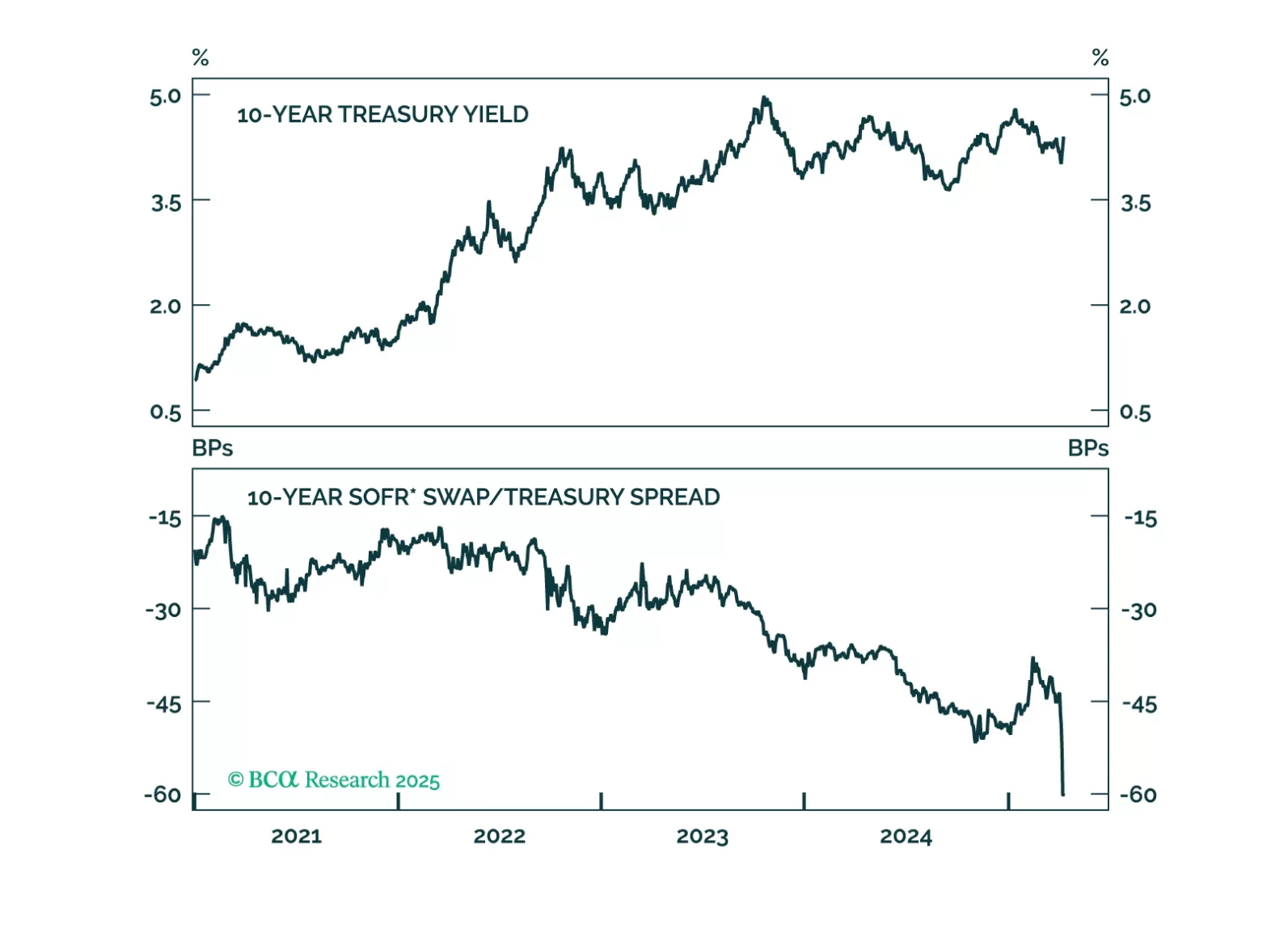

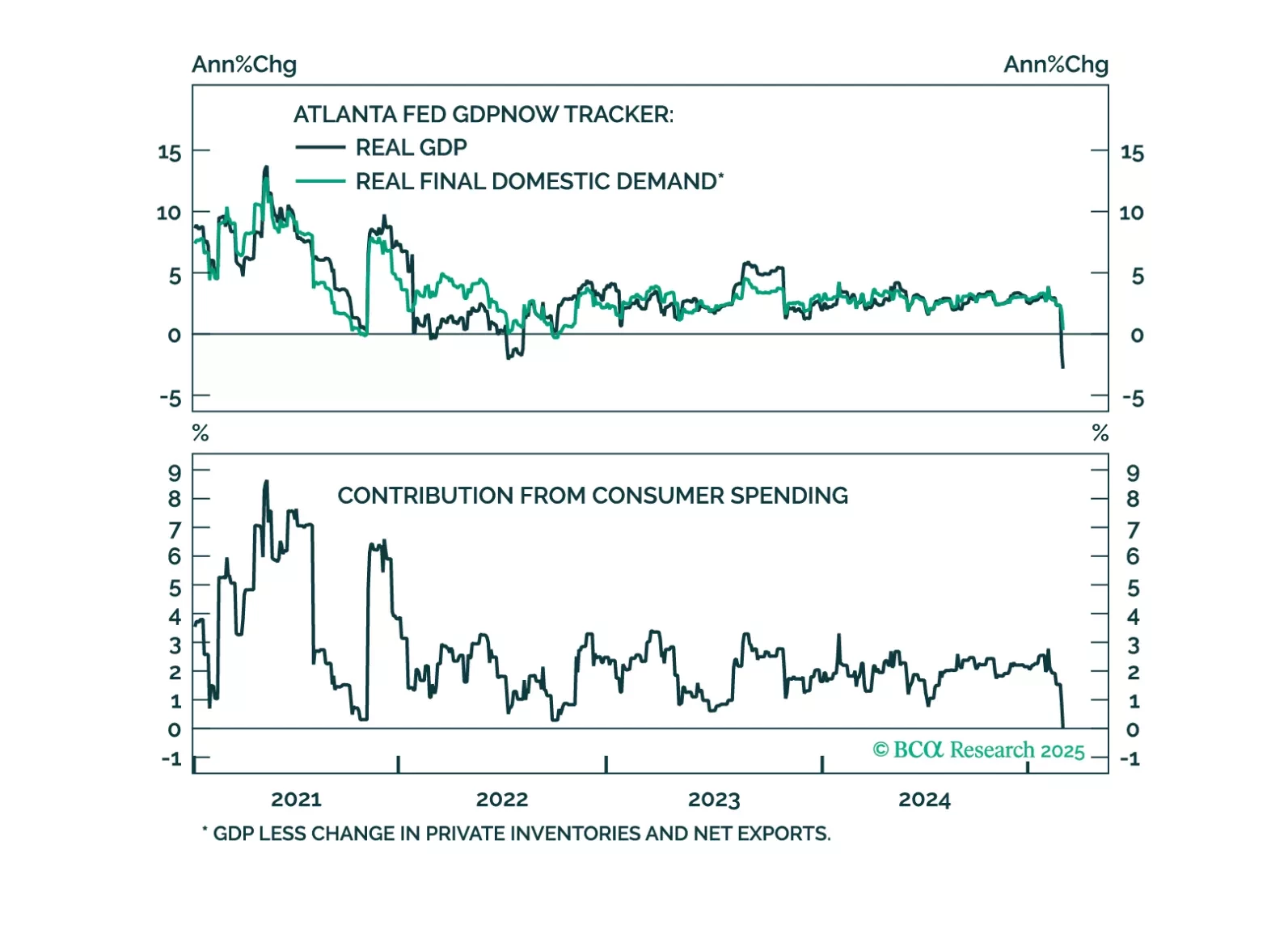

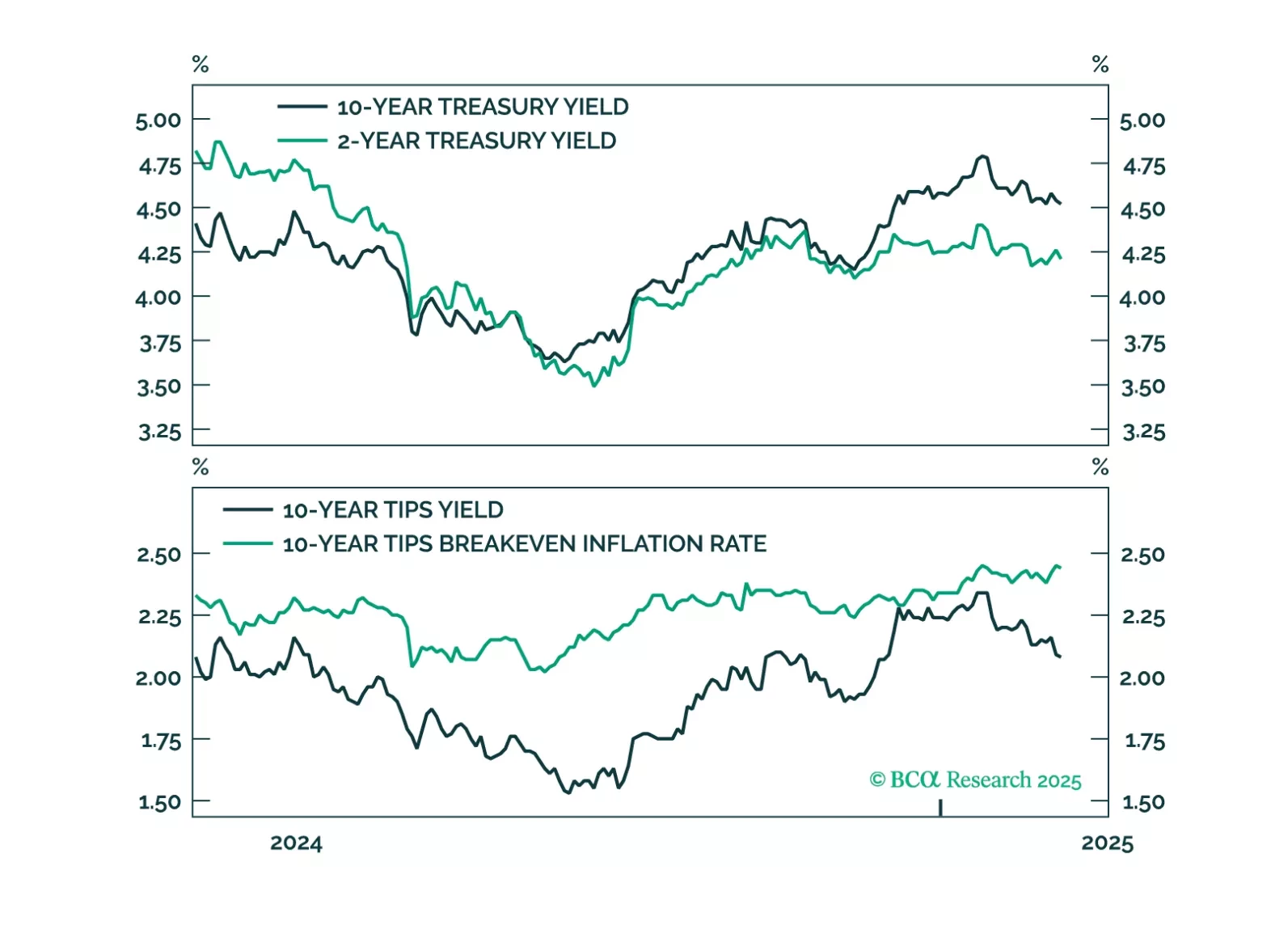

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

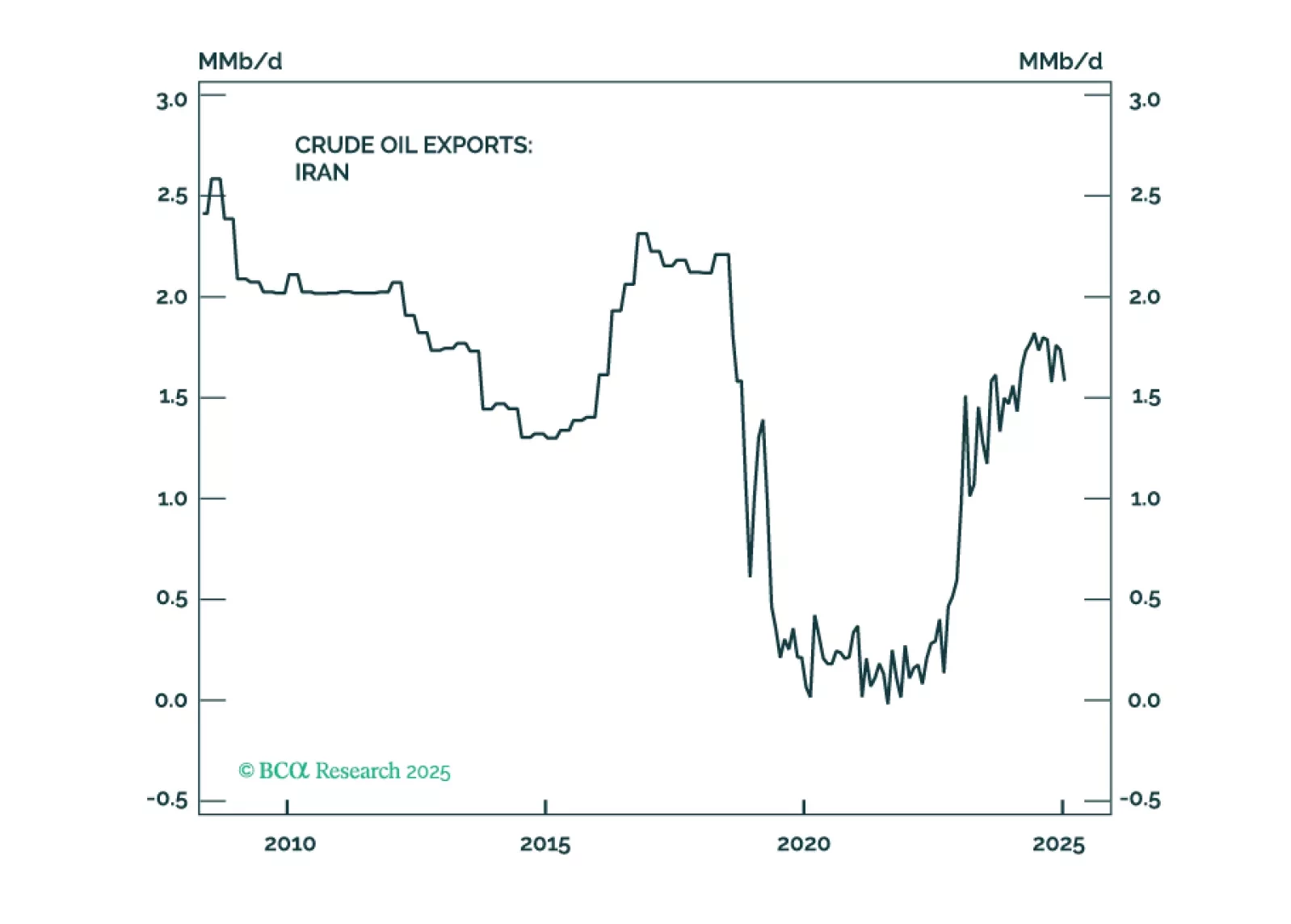

Interest rates will decline if the disinflationary trend continues, deficits are reduced, or economic growth falters. Oil prices are likely to spike over the short term, but the long-term outlook is unfavorable. Not all GenAI investments will pay off, and GenAI-induced productivity improvements do not justify current valuations.

Our Portfolio Allocation Summary for January 2025.