Hedge Funds

Investors often misjudge Global Macro managers. We outline key manager evaluation criteria and highlight the power of combining Macro Hedge Funds and Private Equity. Even for those who are not Macro Traders nor invest in Hedge Funds, this report may change the way you assess potential employees, partners, and even yourself—the most critical elements of any investment strategy.

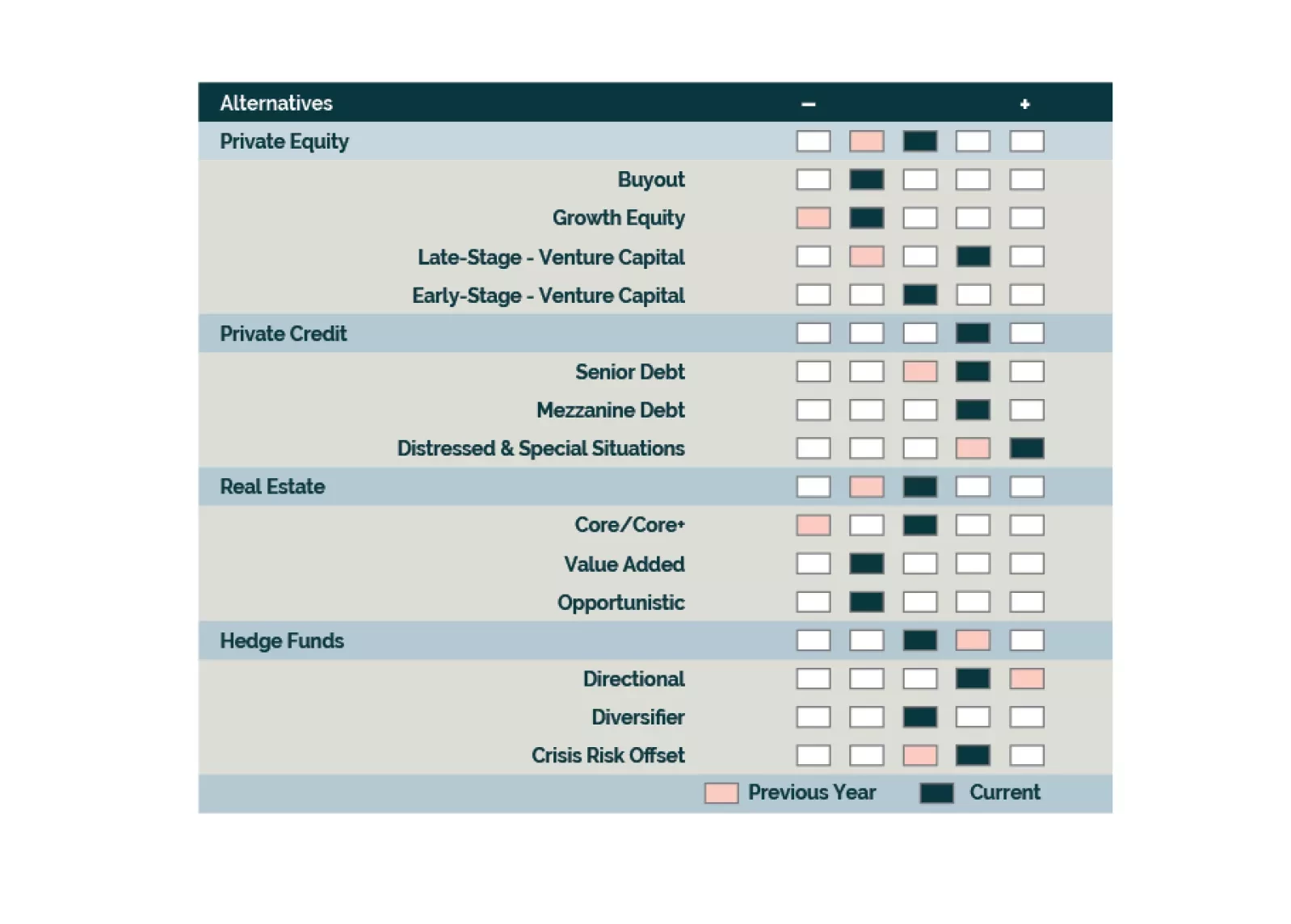

We go overweight Late-Stage Venture Capital and APAC Private Equity but remain underweight North America Buyouts. We maintain our neutral outlook towards Hedge Funds and are positive on Long-Short Equity, Event Driven, and CRO strategies. We are cooling towards Direct Lending strategies as competition and relative opportunities increase. CRE’s downturn continues to unfold; we are starting to be buyers.

Investors should be tactically tilting allocations towards Direct Lending, Distressed Debt, and Directional Hedge Fund strategies at the expense of Real Estate, Private Equity, and Diversifier Hedge Funds. Structural opportunities are emerging in Real Estate and Venture Capital.

We do not see a 1990s type of backdrop but we do see a departure from the 2010s. Structural forces make it unlikely that we will return to the 1990s heydays for LSE. However, evolving cyclical forces provide tailwinds over the next market cycle. In this Special Report we provide a quantitative assessment of what investors can expect.

We see challenges ahead for Global Buyout across geographies as valuations need further resetting. While we are concerned with capital controls and flight risk in Asia-Pacific Venture Capital, the upside potential from AI may be worth a look. The current entry point for Private Credit is opportune across North America and Europe with the distressed pipeline building. Real Estate does not look appealing with the macro and relative opportunity set driving our underweight. Hedge Funds have a favorable backdrop in the near-term, although prospects differ across Directional, Diversifier, and Crisis Risk Offset strategies.

We see a more positive backdrop for credit providers, with bilateral and structuring features as tailwinds for Private Credit. While there may be potential green shoots in some areas of Private Equity, current valuations are not attractive. We prefer Directional Hedge Funds over Diversifier and Risk Mitigation strategies. Real Estate has been an effective hedge against inflation, but now historically low cap rates are a headwind.