Hedge Funds

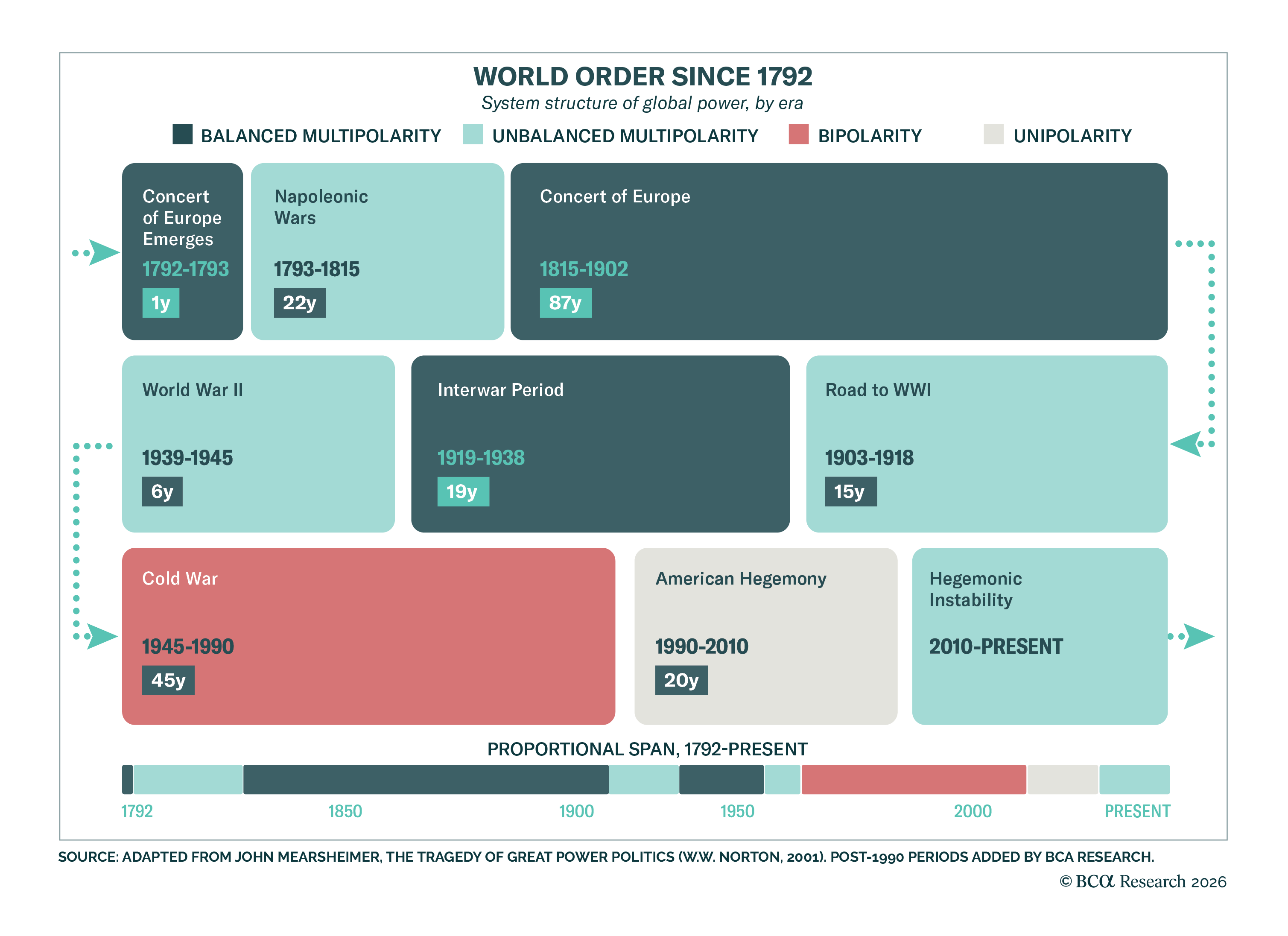

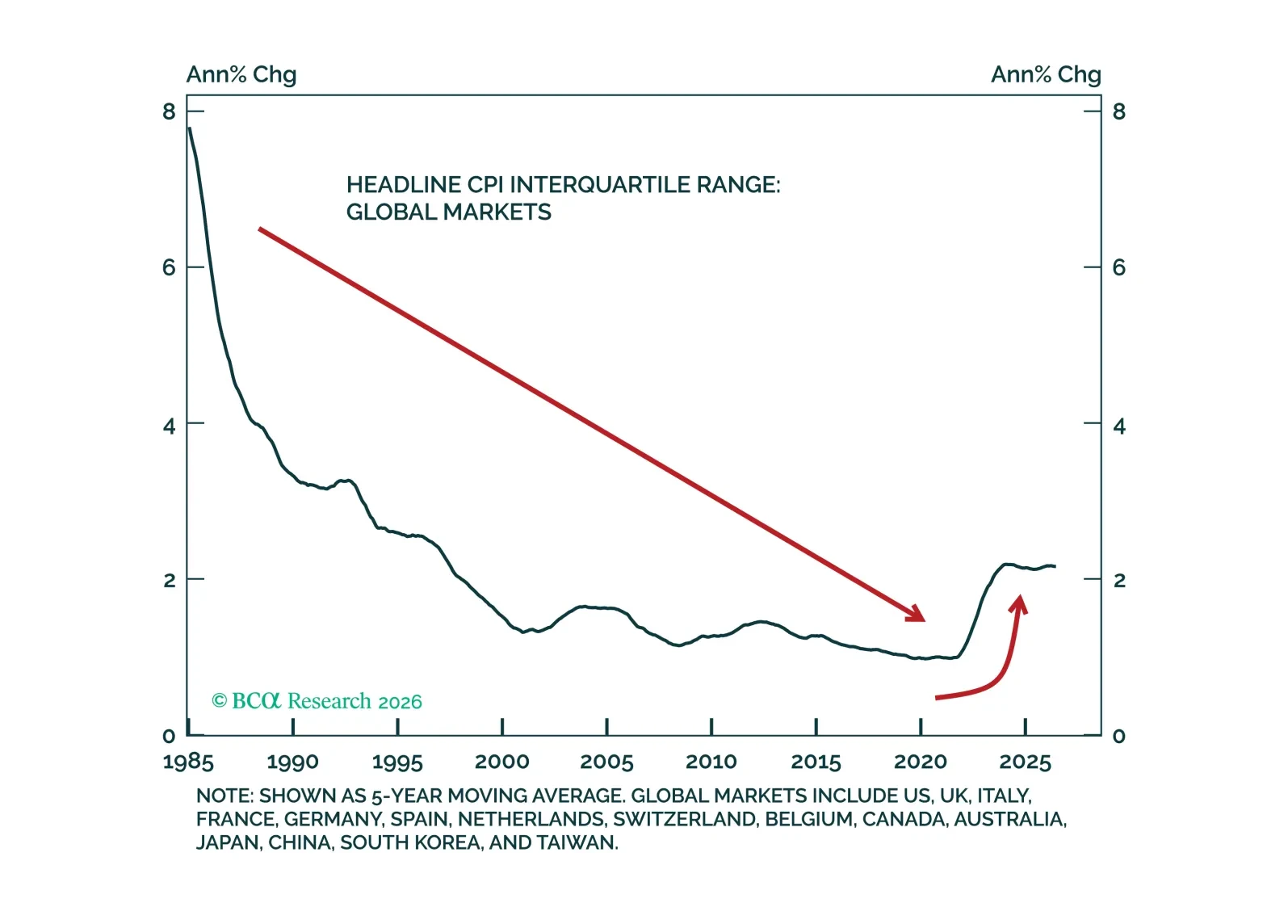

For almost two decades, beta was the only game in town and alpha a loser's game. This era is ending, and we lay out why a more multipolar, dirigiste, and AI-disrupted world is pushing dispersion structurally higher, creating renewed alpha opportunities.

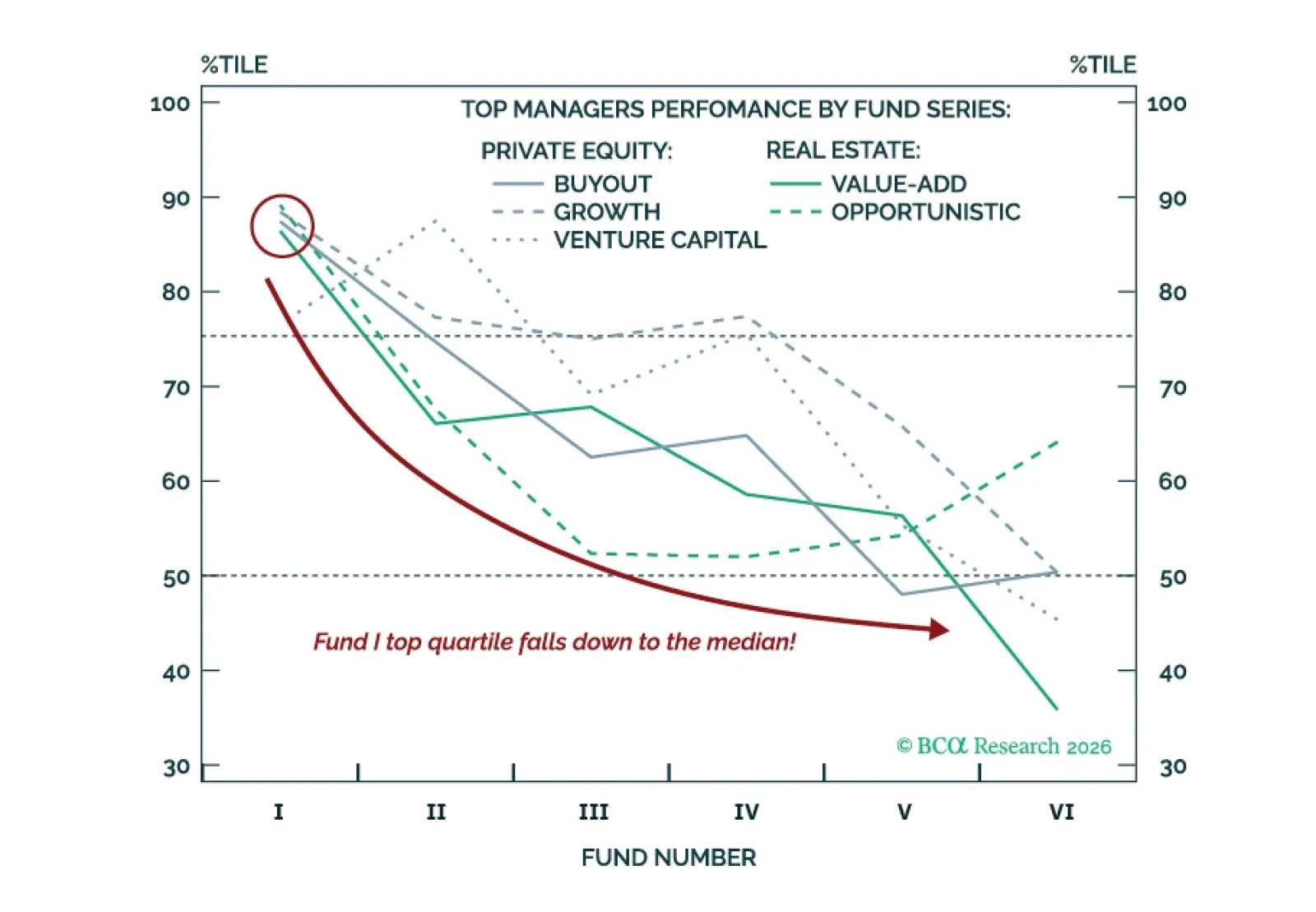

In Private Markets, yesterday’s winners often see outperformance fade. Top-quartile managers often regress toward the median as fund series mature. For investors evaluating the next Real Estate or Private Equity manager: Bias toward underweighting Funds V and beyond.

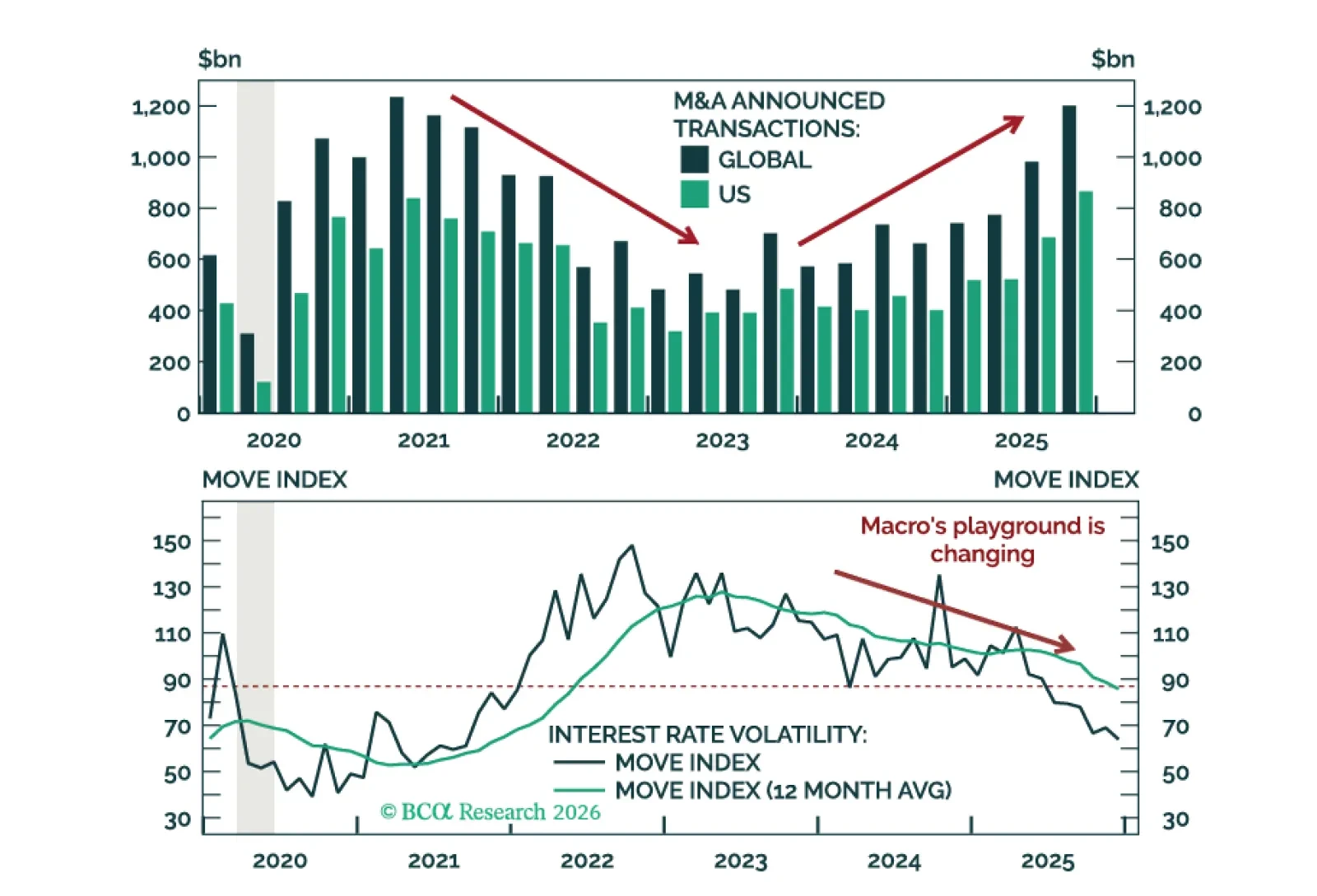

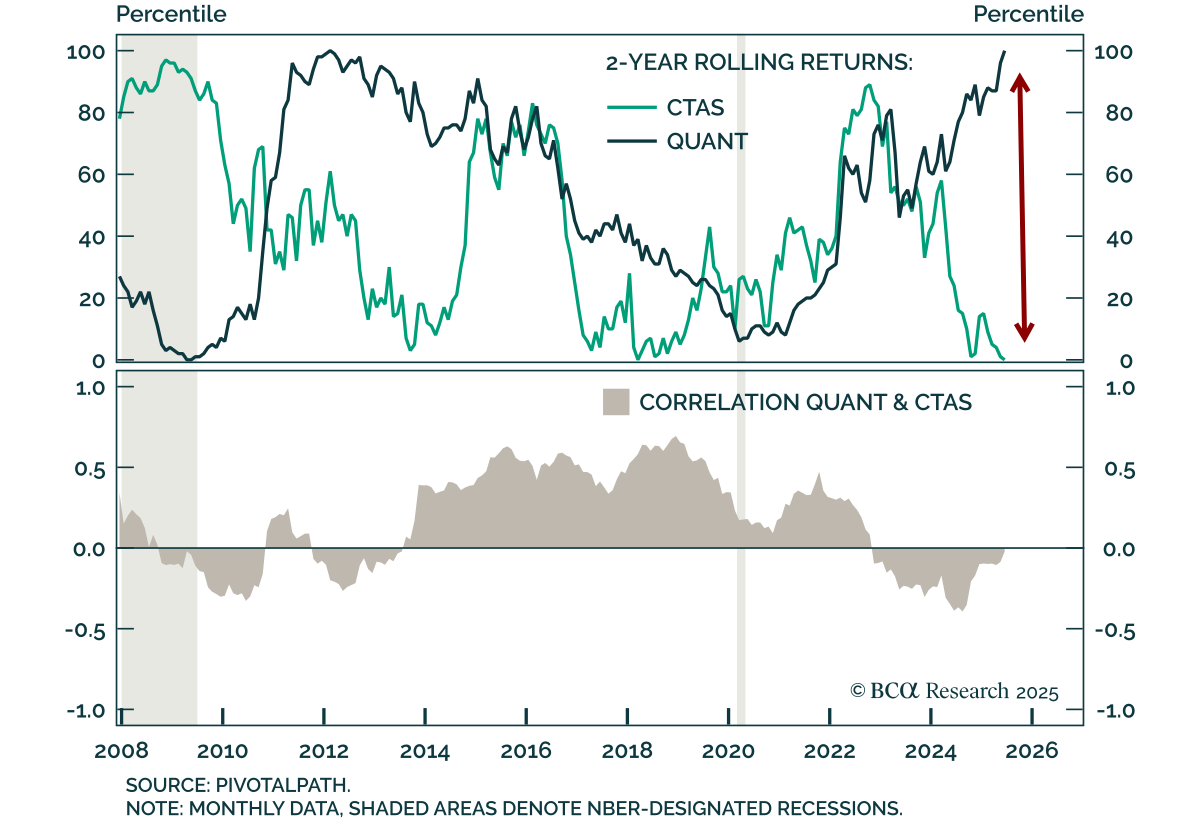

M&A activity finally reaccelerated in Q4 2025—it’s just the start. Macro Hedge Funds have outperformed with top-decile performance from Discretionary Macro—but that’s towards the end. We move Macro from overweight to underweight and Event Driven from neutral to overweight.

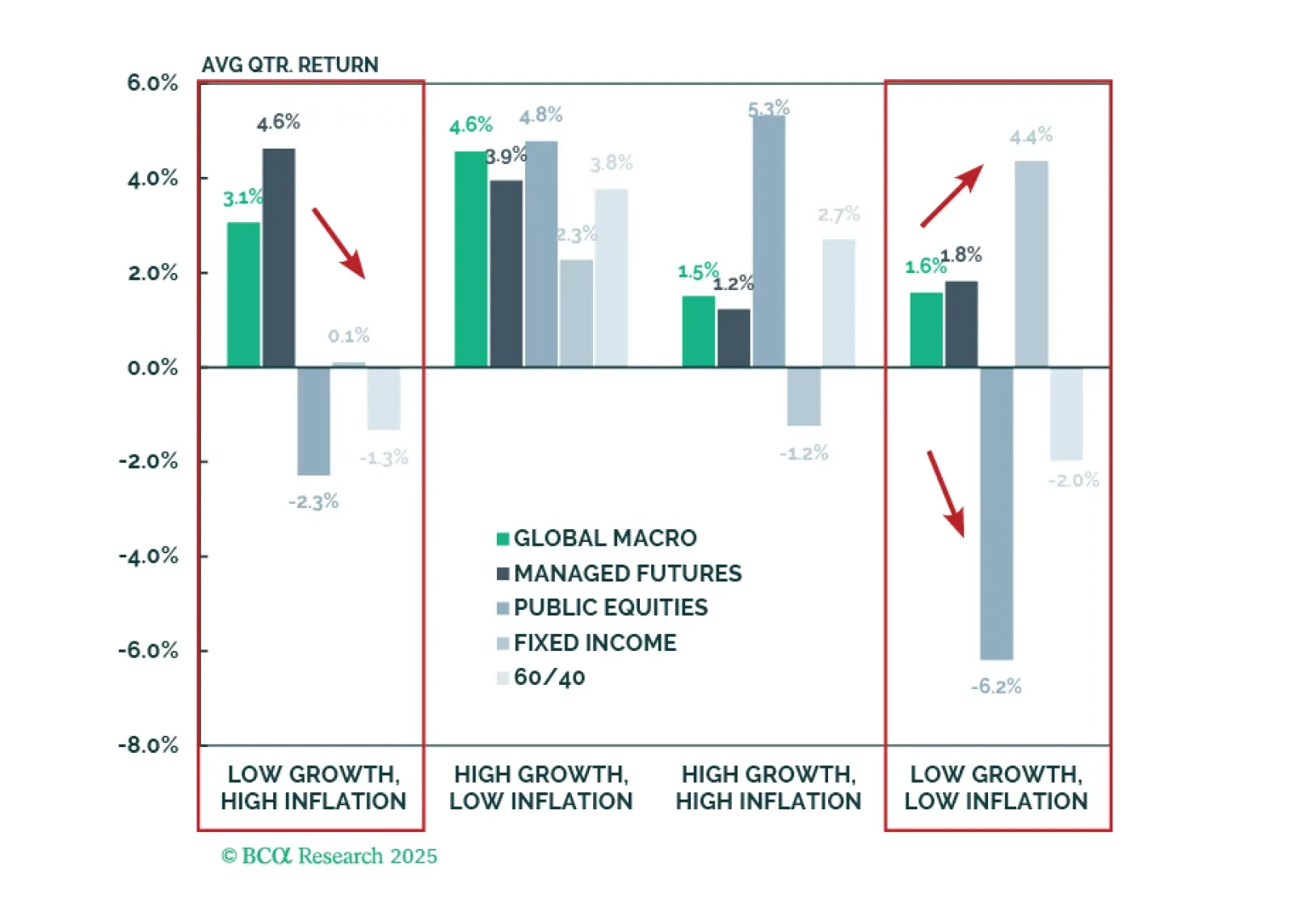

Understanding asset performance across Growth and Inflation regimes helps investors construct and manage balanced portfolios. Our first G&I Catalog report examines Hedge Fund strategies. Global Macro and Managed Futures offer the strongest protection in Stagflation-like periods, when traditional assets typically struggle. Since 1998, these regimes have occurred less than 10% of the time—but that may not hold true going forward.

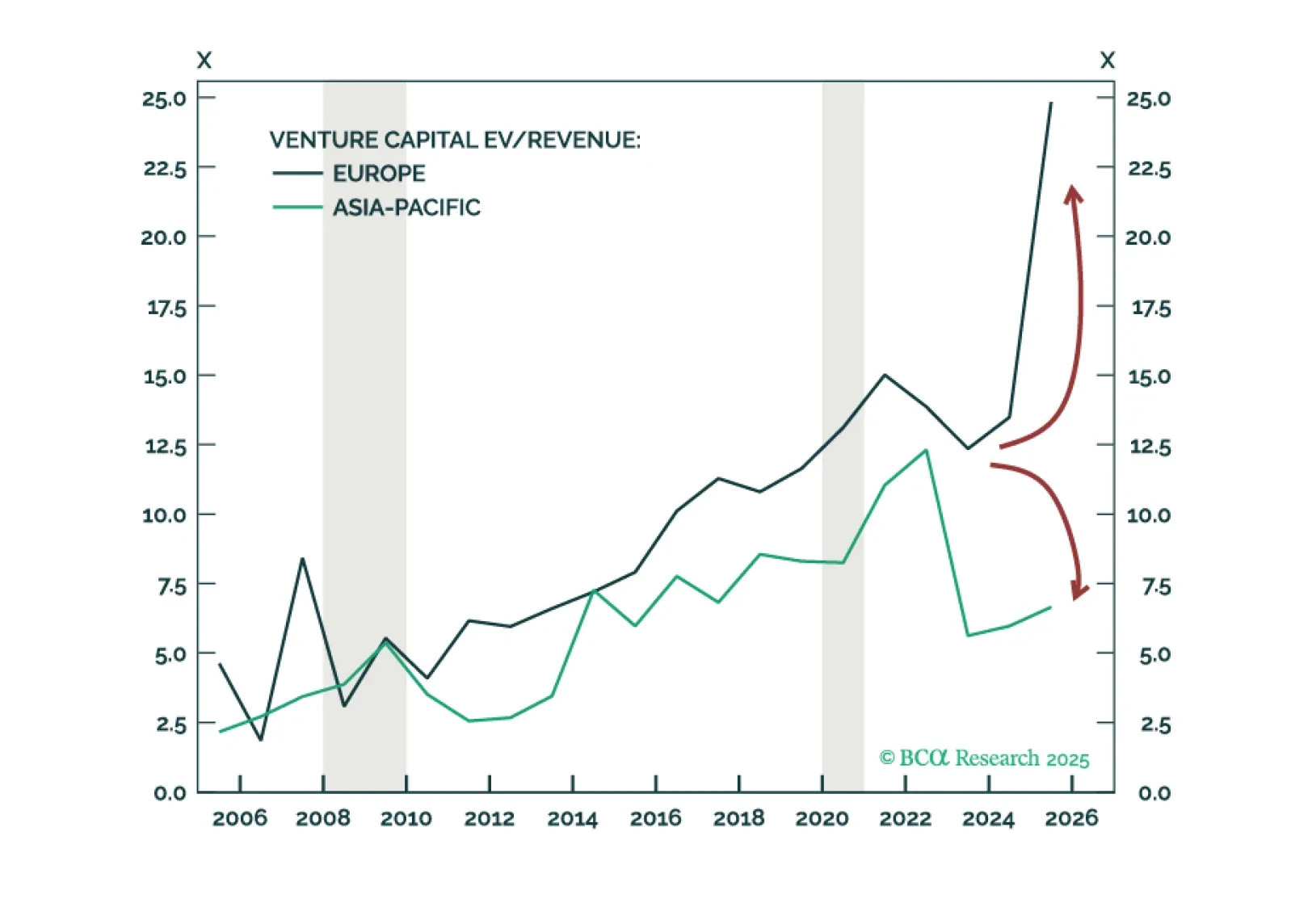

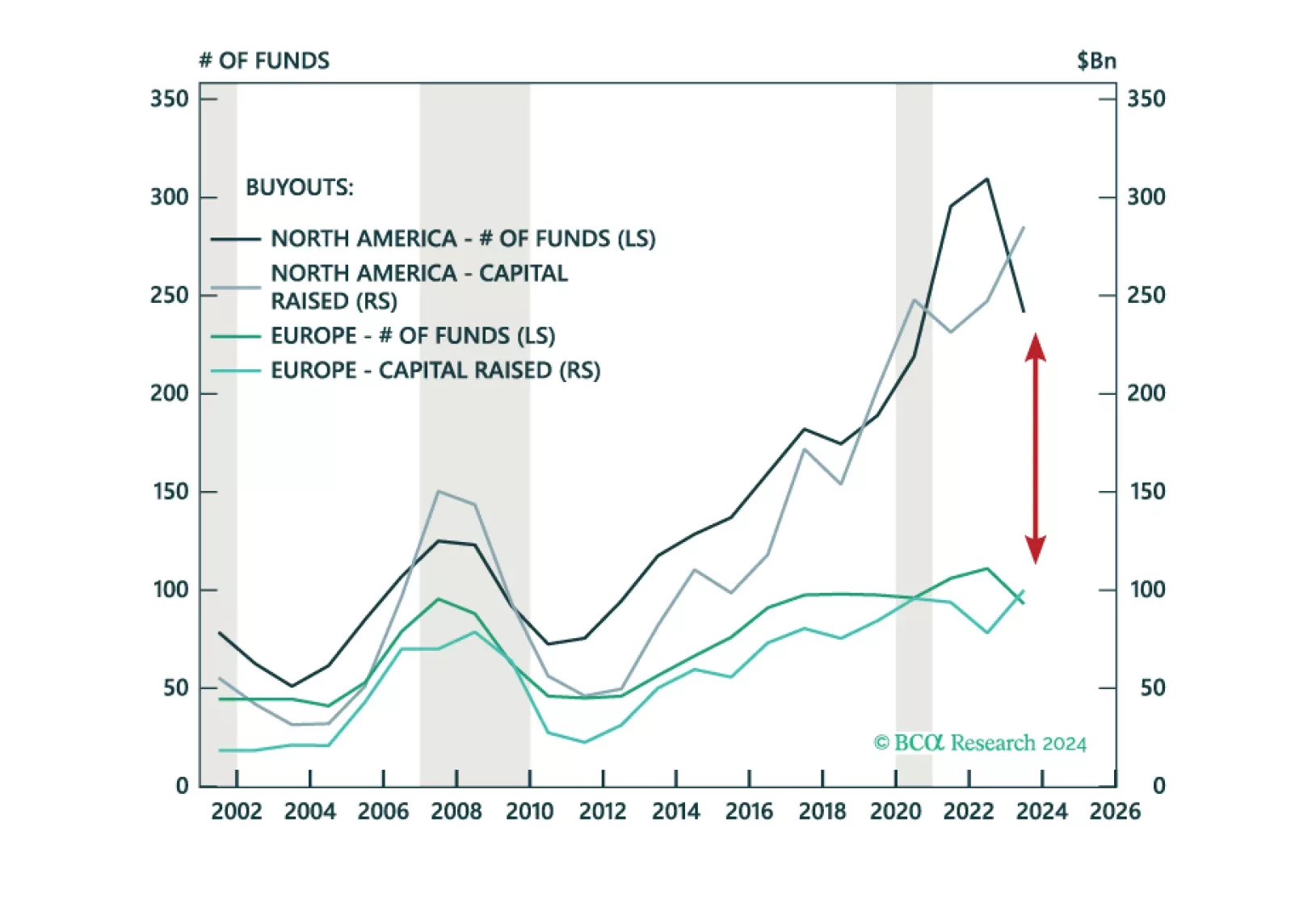

European euphoria is overdone. The most exceptional asset class in Europe is Infrastructure, but granular opportunities span other asset classes by sector and country. Venture Capital is a North America and Asia-Pacific play. We downgrade Private Credit, and upgrade Global Buyouts. Time to take profits on Long-Short Equity Hedge Funds.

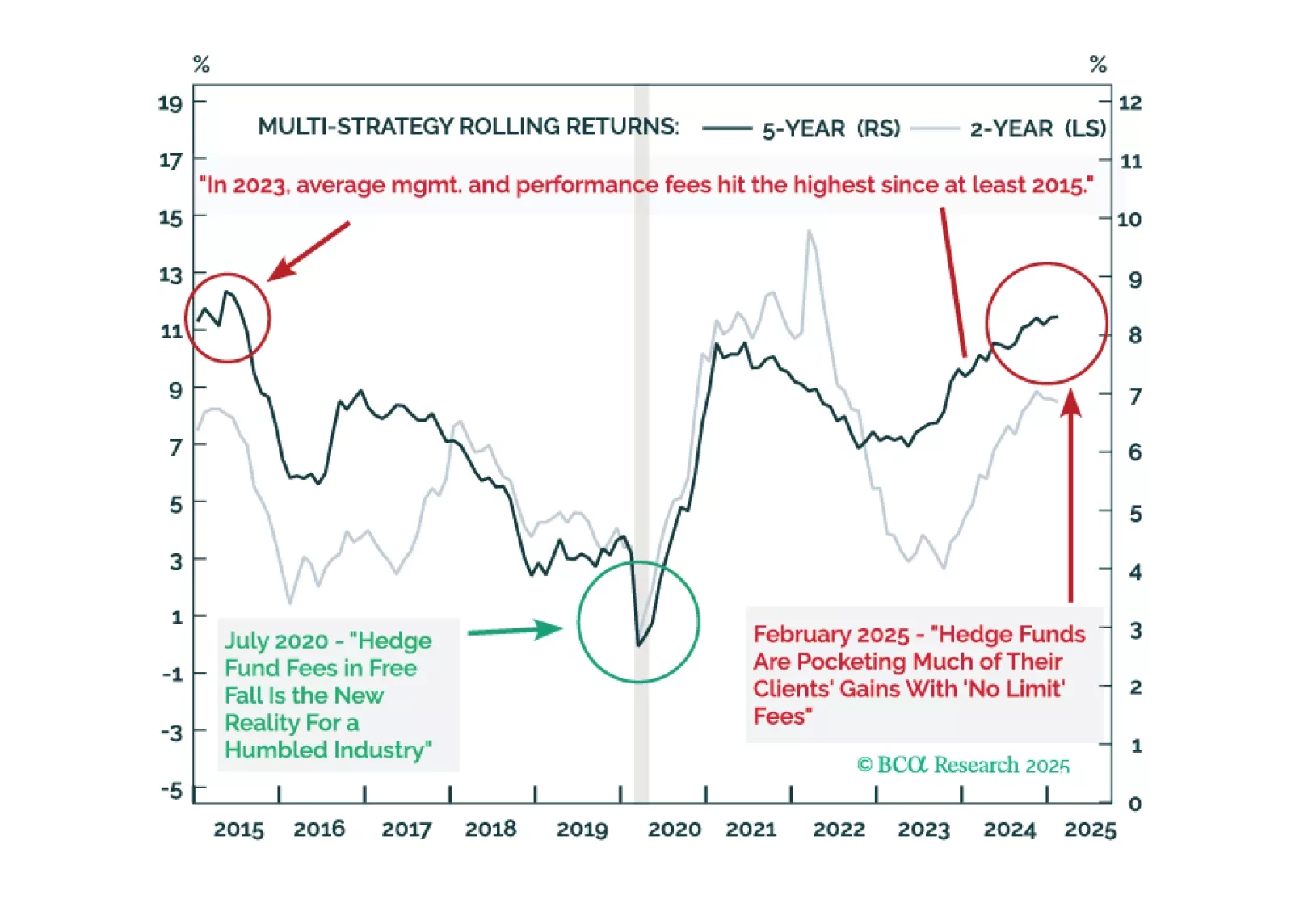

It is easy to hate Multi-Strategy Hedge Funds—they are no underdogs. The truth is they have been cheap, not expensive. Going forward, they come at a higher cost not just in the form of fees. The biggest risk is not to financial markets but to investors. We remain underweight cyclically, long structurally.

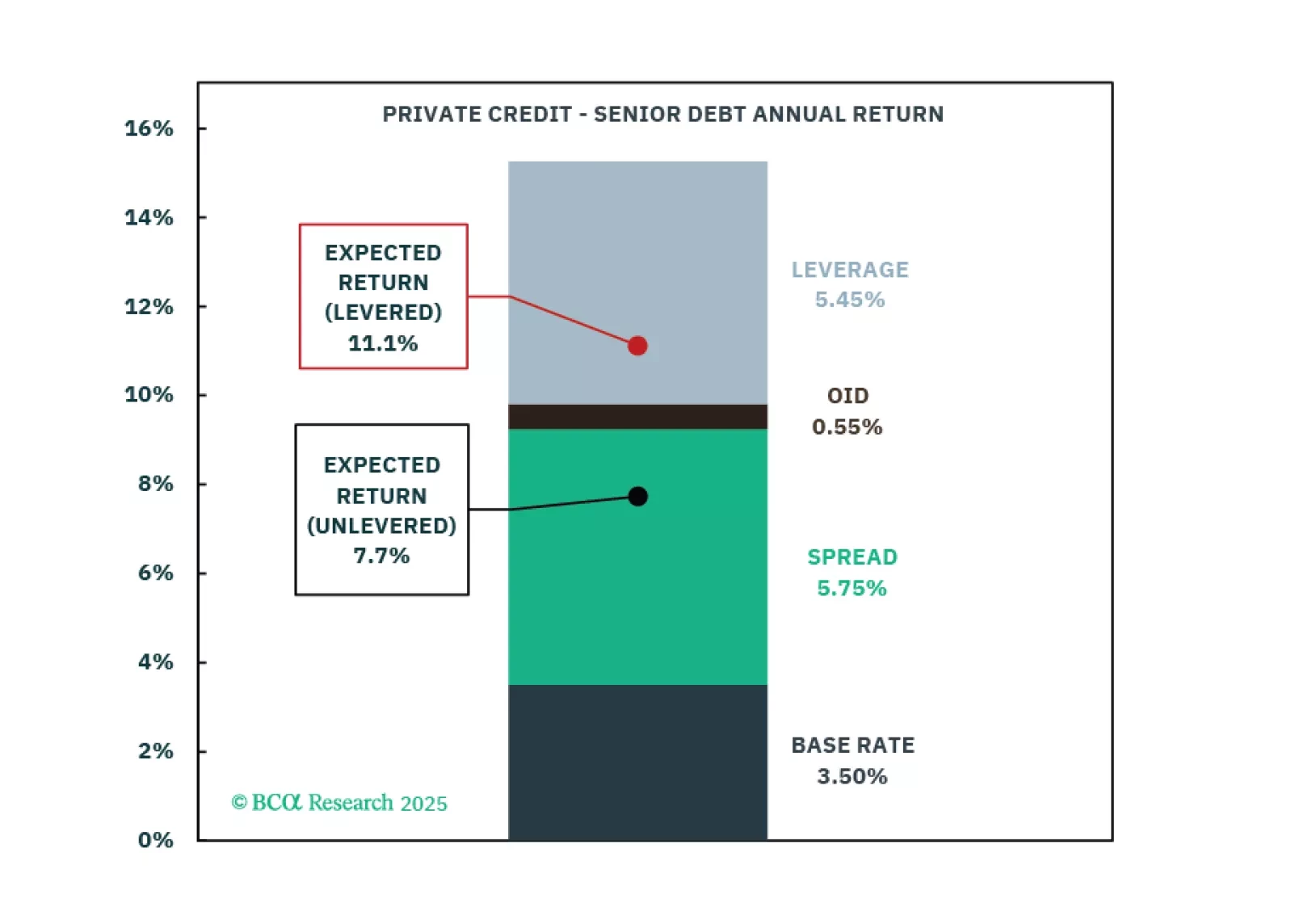

Asset class expectations show mixed shifts from 2024, with Real Estate seeing substantial upgrades and Private Equity benefiting from Venture Capital improvements. Private Credit return expectations decline from 2024 but remain relatively attractive. Infrastructure shows varied dynamics across sub-strategies, with Value-Add offering strong return potential. Within Hedge Funds, Long-Short Equity shows higher tactical returns while Multi-Strategy leads strategic projections.

We are growing positive on Growth assets with recession expectations increasing our optimism on entry points. Equities are led by APAC Private Equity, North America Venture Capital, and Europe Buyouts. Our outlook continues to improve on CRE within the Inflation & Diversification bucket while we are underweight Multi-Strategy amongst Hedge Funds. We maintain an overweight to Senior Direct Lending for Income with a preference for North America.