Health Care

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

Disinflation coupled with sticky wage growth is likely to result in either a second wave of inflation or layoffs and a recession. In the meantime, market expectations for sales, growth, and margins are overly optimistic and are inconsistent with macroeconomic headwinds. We recommend gradually realigning the portfolio to a more defensive stance.

The Republican Party’s odds of winning the 2024 election will benefit, if anything, from state courts’ attempts to exclude President Trump from primary or general election ballots. Higher odds of a change of ruling party will increase stock and bond market volatility.

We expect the US economy to slow and potentially downshift into a recession sometime in 2024, as tighter monetary policy weighs on consumers and businesses. In addition, (geo)political tensions may increase market volatility. The risk/return for US equities is unfavorable. We recommend that our clients reduce portfolio beta and increase allocations to defensives and quality growth.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

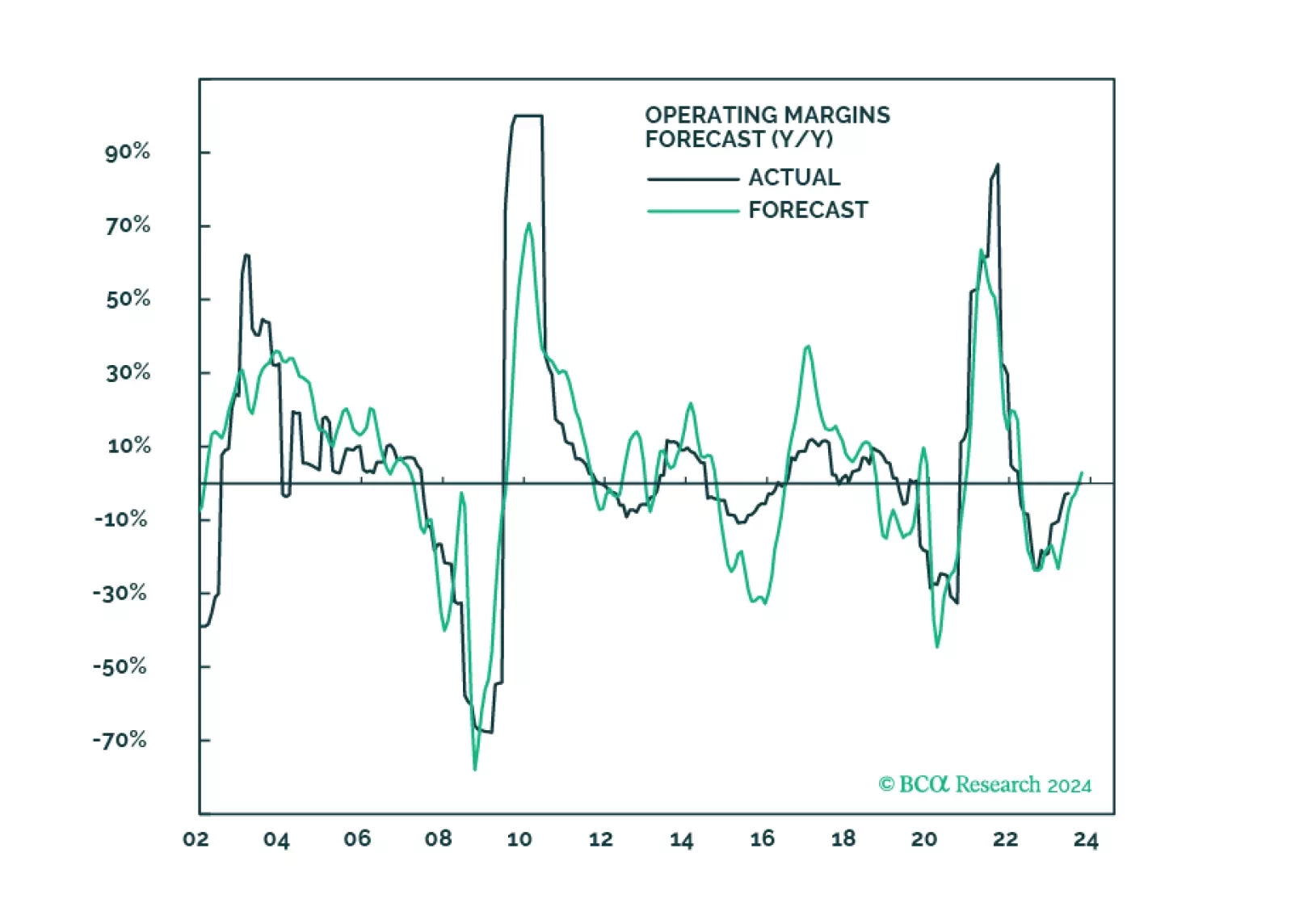

Q3-2023 is expected to mark the end of the earnings recession for the past three quarters, opening the door to positive earnings growth. Whether that would be sustainable or will sputter once the recession settles in as expected in 2024 remains to be seen. However, much of earnings growth is already priced in.

More equity volatility is coming in the short run. Trump’s nomination looks to be smooth, which marginally reduces the incumbent party advantage and increases policy uncertainty.

In June, the rally gained momentum and broadened due to positive economic data, particularly in the housing market. We expect cheaper cyclical sectors and styles to mark a change in leadership as the rally broadens, helped on by excess cash on the sidelines. We upgrade Banks to equal-weight, and Homebuilders to overweight. The rally may continue but a soft landing continues to be elusive - disappointment may be in store.

Investors are still cautious and have significant cash that needs to be put to work. Trickle-down of it into the US equity market may extend the rally. Overly bearish futures positioning is also a strong contrarian indicator. Disinflation is good for real earnings growth, and imminent earnings rebound may add support for equities.