Health Care

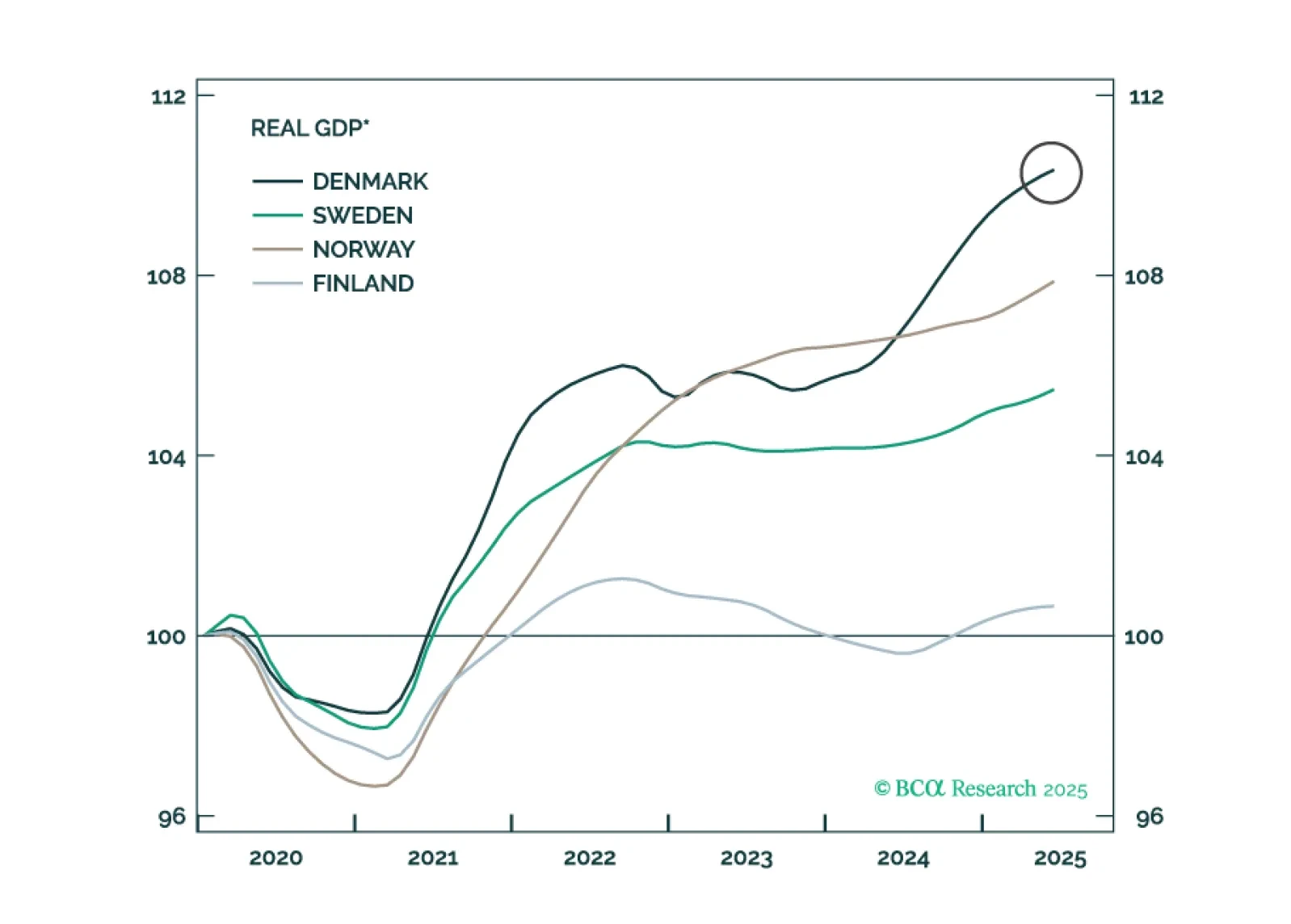

The Nordic central banks are now aligned in pause mode, but their economies are diverging. With Swedish prospects improving and Norwegian headwinds mounting, we are turning overweight on Swedish equities and shorting NOK/SEK.

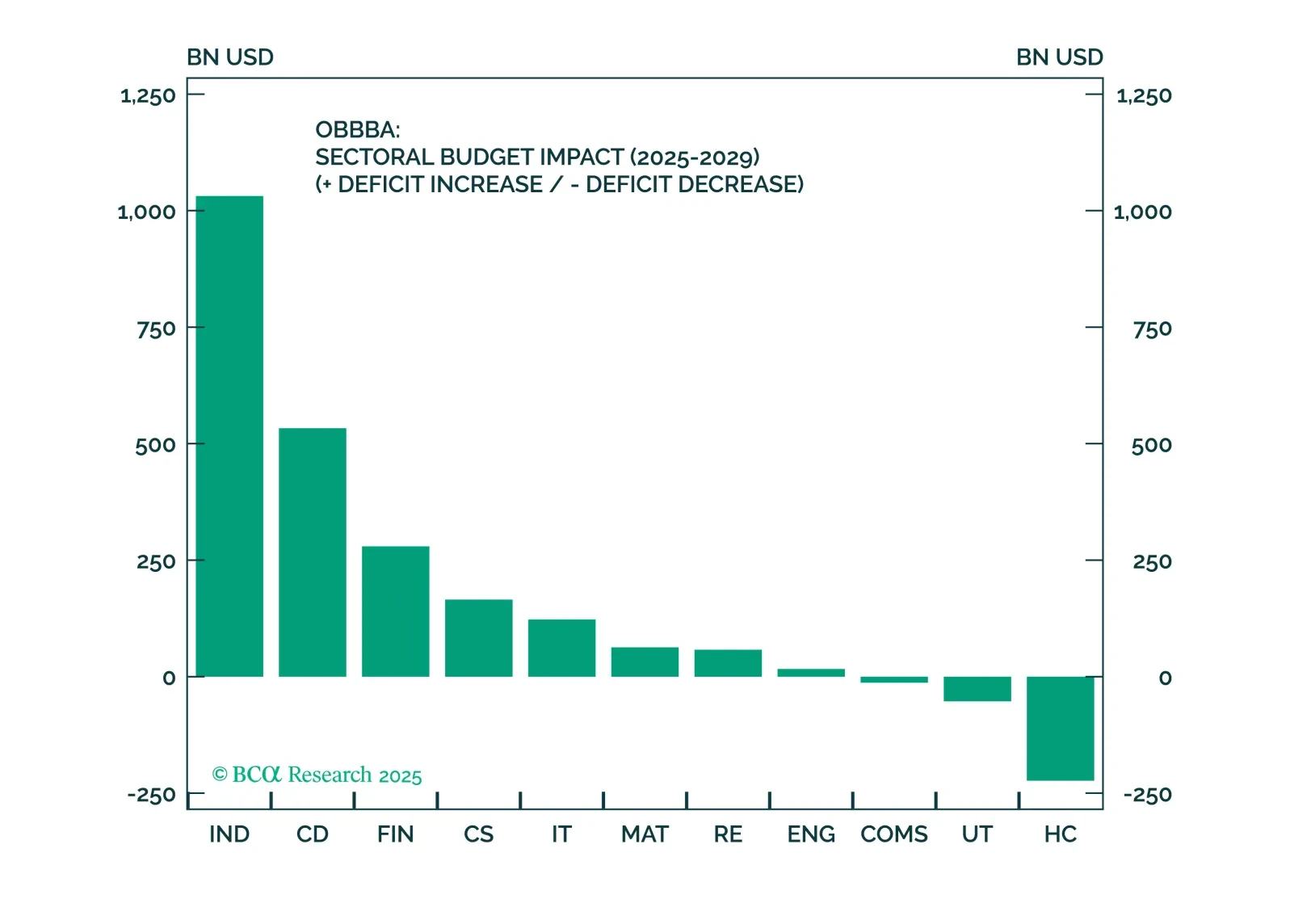

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

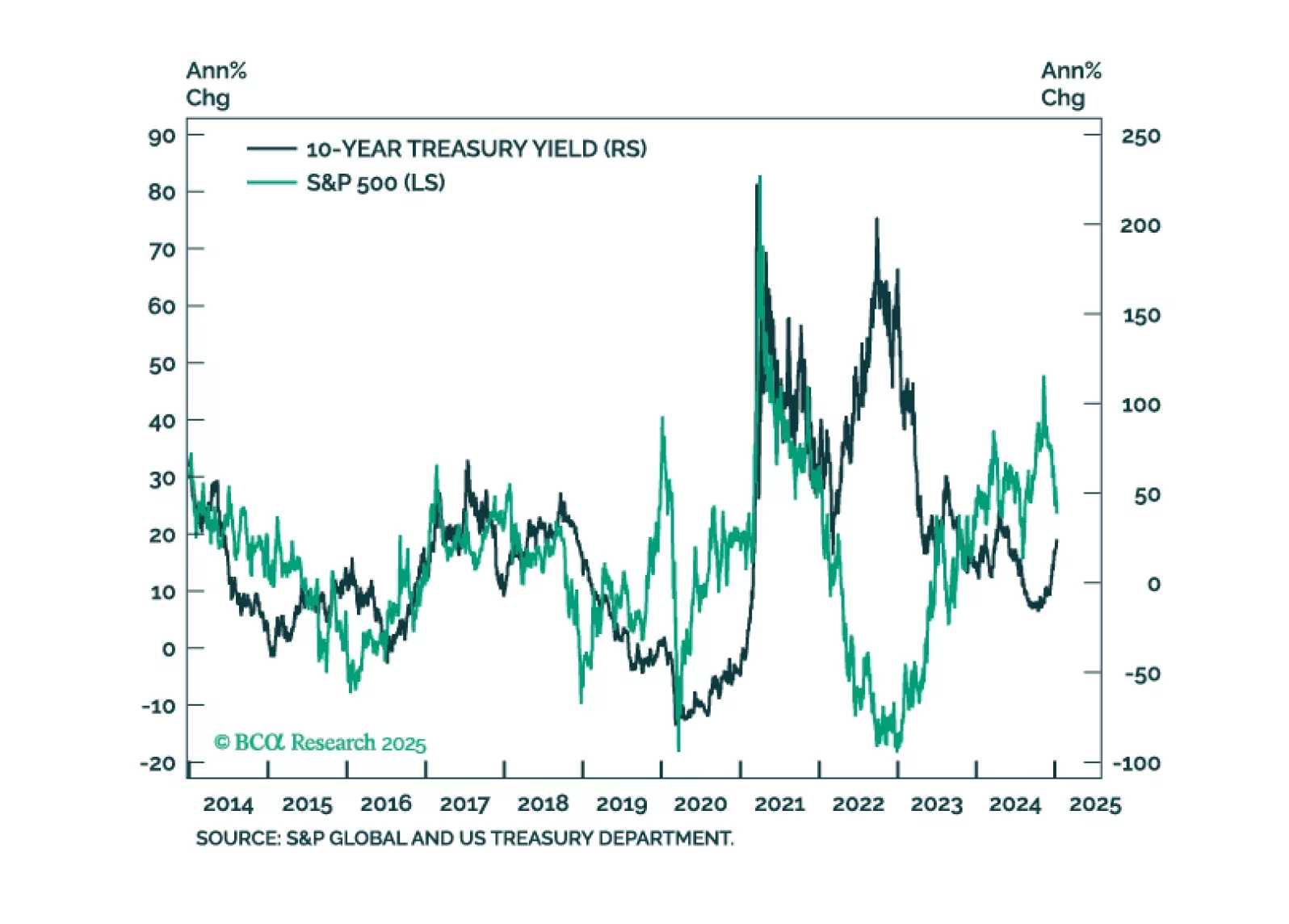

In this first presentation of 2025, we start with an overview of the 2025 outlook webcast polls, and a brief post-mortem of the 2024 market performance. Then, we shift gears and examine what is behind the recent surge in bond yields and its implications for equities. We also review market technicals and positioning and conclude with a list of trades to prepare our portfolio for continued moves in yields.

The post-COVID recovery has been one of excesses. Government deficits have ballooned, tight labor markets have led to a windfall of consumer spending, and equity valuations have soared on the back of lofty growth expectations. But these excesses will no longer be sustainable in 2025. Our theme for next year is Thin Is Back In. Government budgets, economic growth, and equity valuations will be leaner than investors expect. We discuss this the reasoning behind this macro view and the asset allocation implications that follow from it.

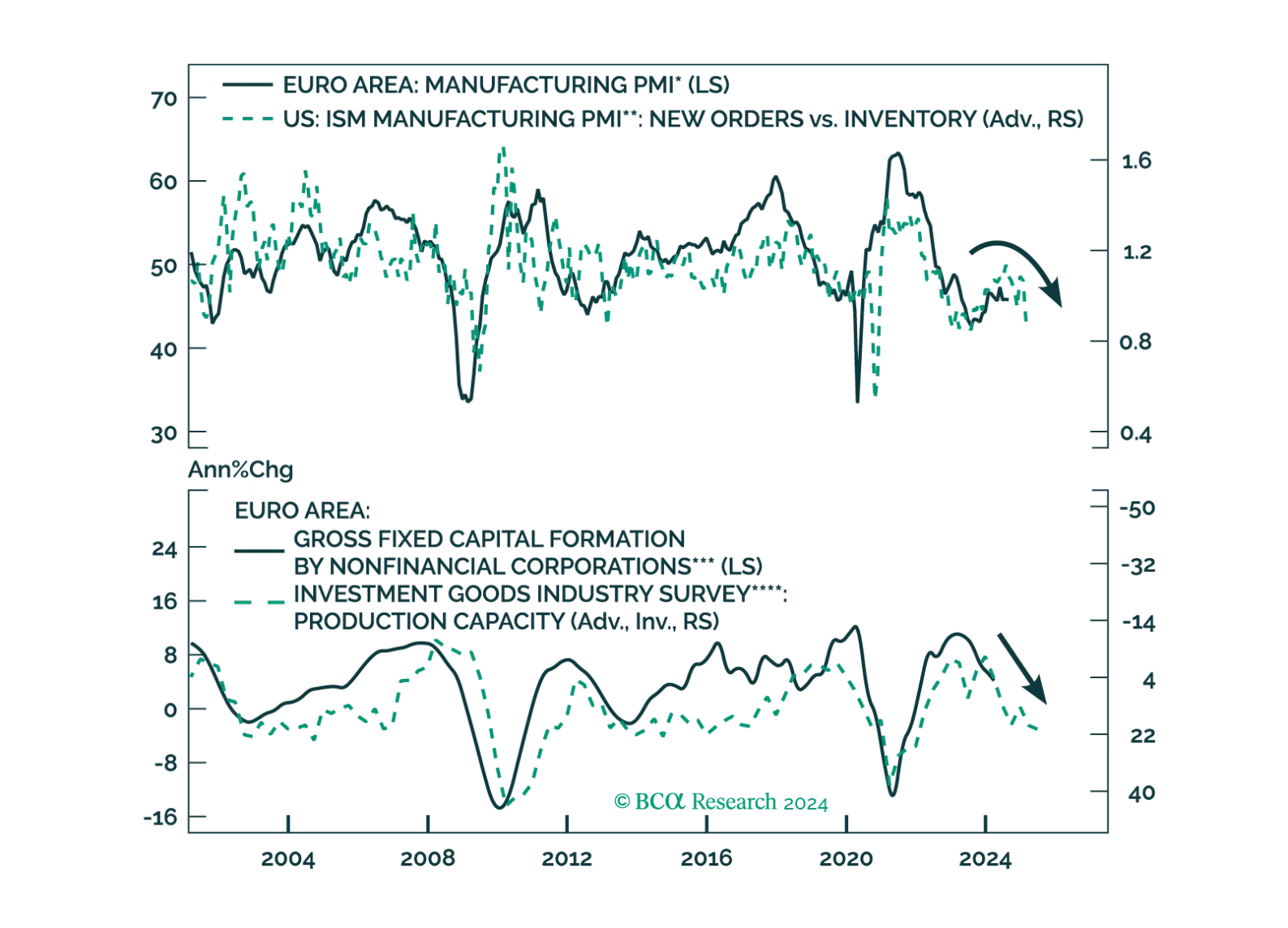

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?