Grains

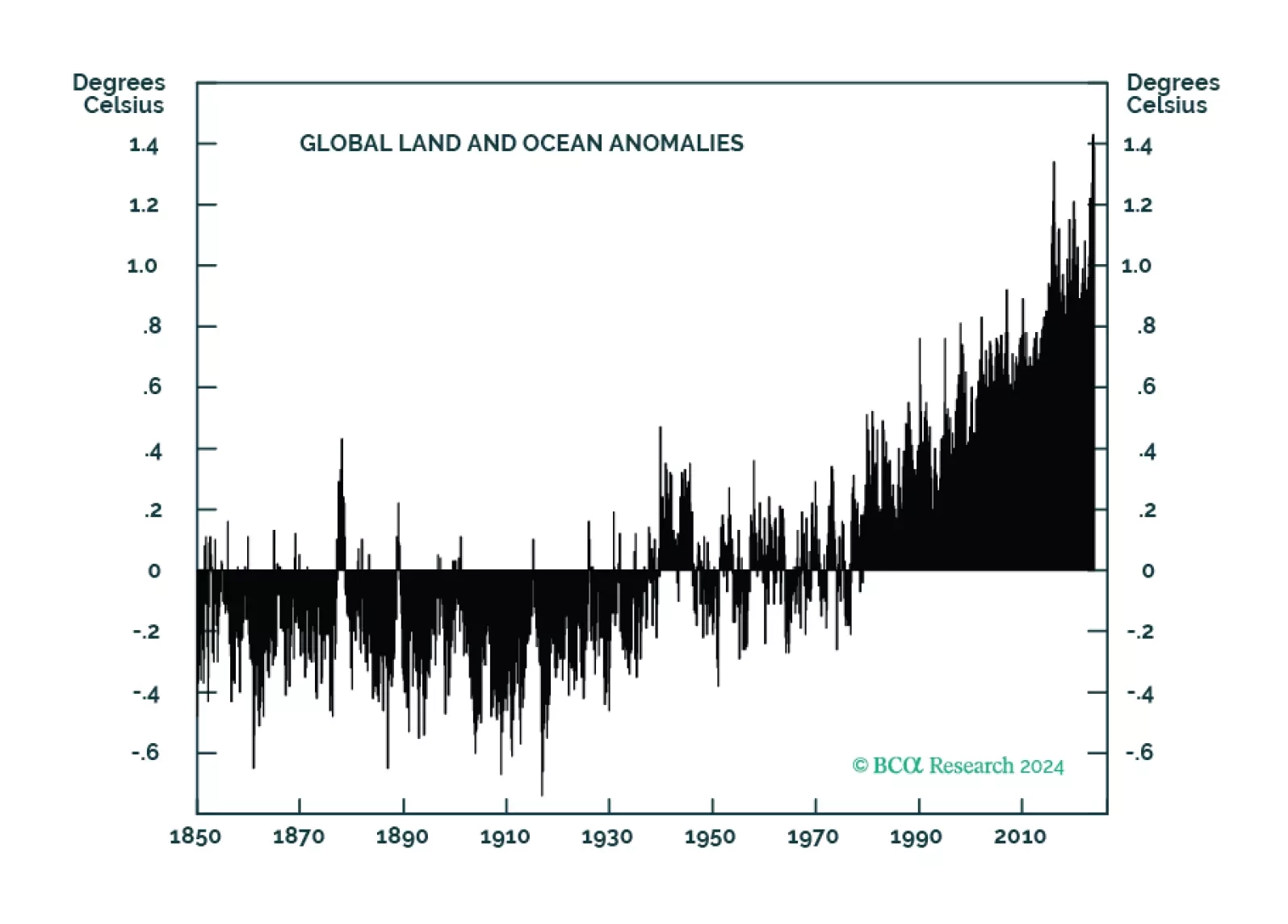

Global ag markets will become more volatile as anthropogenically induced climate change continues to degrade farmland. This will make price signals emanating from these markets less efficient in terms of processing supply-demand fundamentals. All else equal, food prices likely move higher, which will contribute to inflationary biases in the medium-to-long run. Investors will continue to seek out farmland investments as a way to diversify portfolio risk and raise absolute returns.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

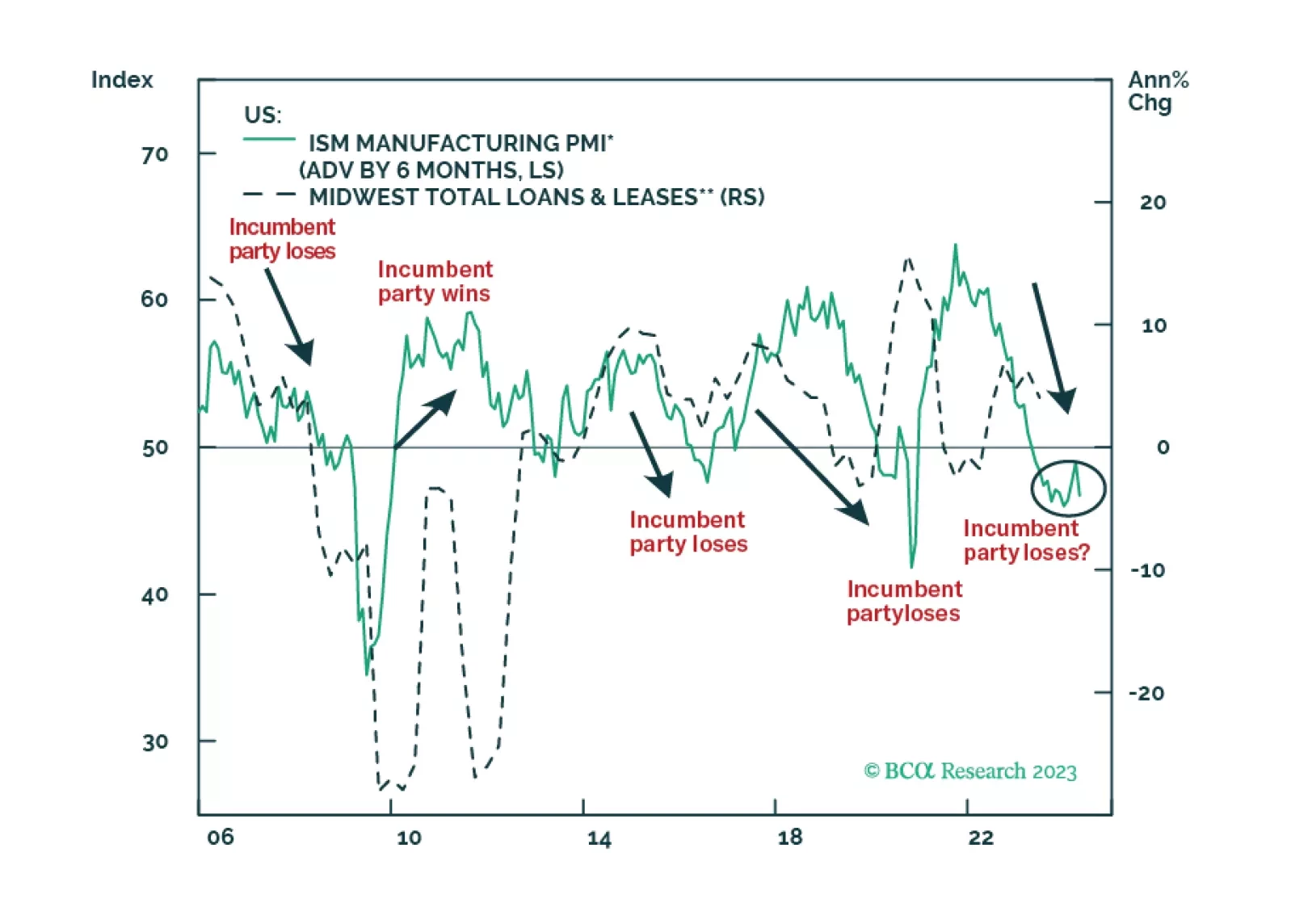

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

Markets continue to be tossed to and fro by central-bank policy, and risks of higher commodity prices. These are due to fiscal stimulus and exogenous weather and war-related risk, which could send food and energy prices higher this winter. We remain long gold outright, energy and metals producers via the XOP, XME and PICK ETFs, direct commodity exposure via the COMT ETF, and futures exposure to backwardation in copper (long 4Q23 copper futures vs. short 4Q24 copper futures).

Fertilizer prices will continue to move lower as the natgas price shock touched off by the Russian invasion of Ukraine dissipates. As a result, we expect grain prices to soften another 10% this year. Food-price inflation will move lower over the course of the year as grain prices weaken, provided a weather- or geopolitical shock does not once again send natgas prices higher.

Energy and metal supplies are becoming increasingly scarce. In such a market, we will re-establish our long commodity exposure via the COMT ETF after being stopped out with a -4% return this week. We remain long equity exposure to oil and gas producers, and metals miners via the XOP and XME ETFs, respectively. Our energy recommendations closed this year posted an average 18.4% gain.