Gov Sovereigns/Treasurys

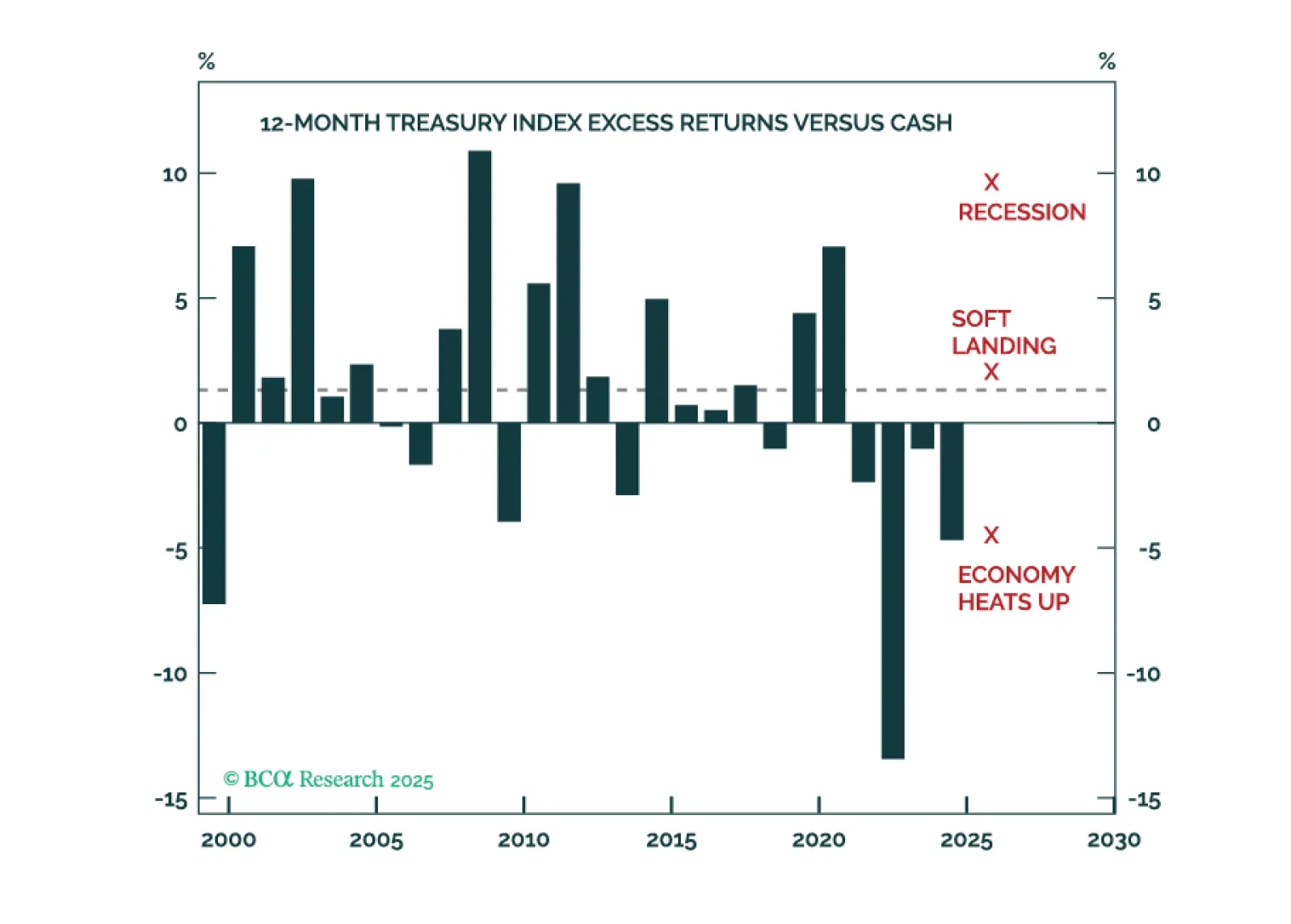

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

Jay Powell won’t be removed as Fed Chair before the expiry of his term next May, but we will learn the identity of his replacement this year, setting up a potentially awkward “shadow Fed Chair” situation.

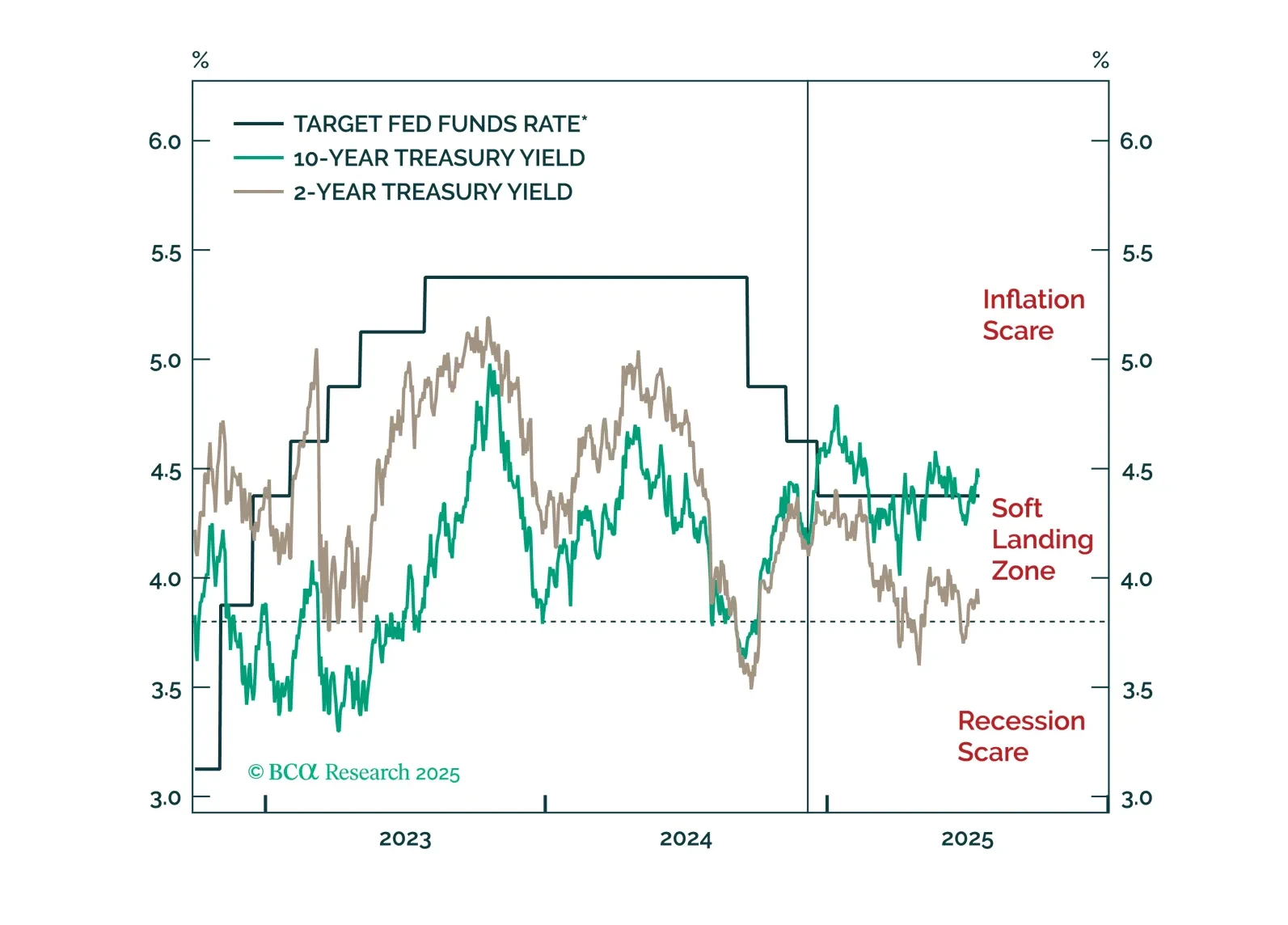

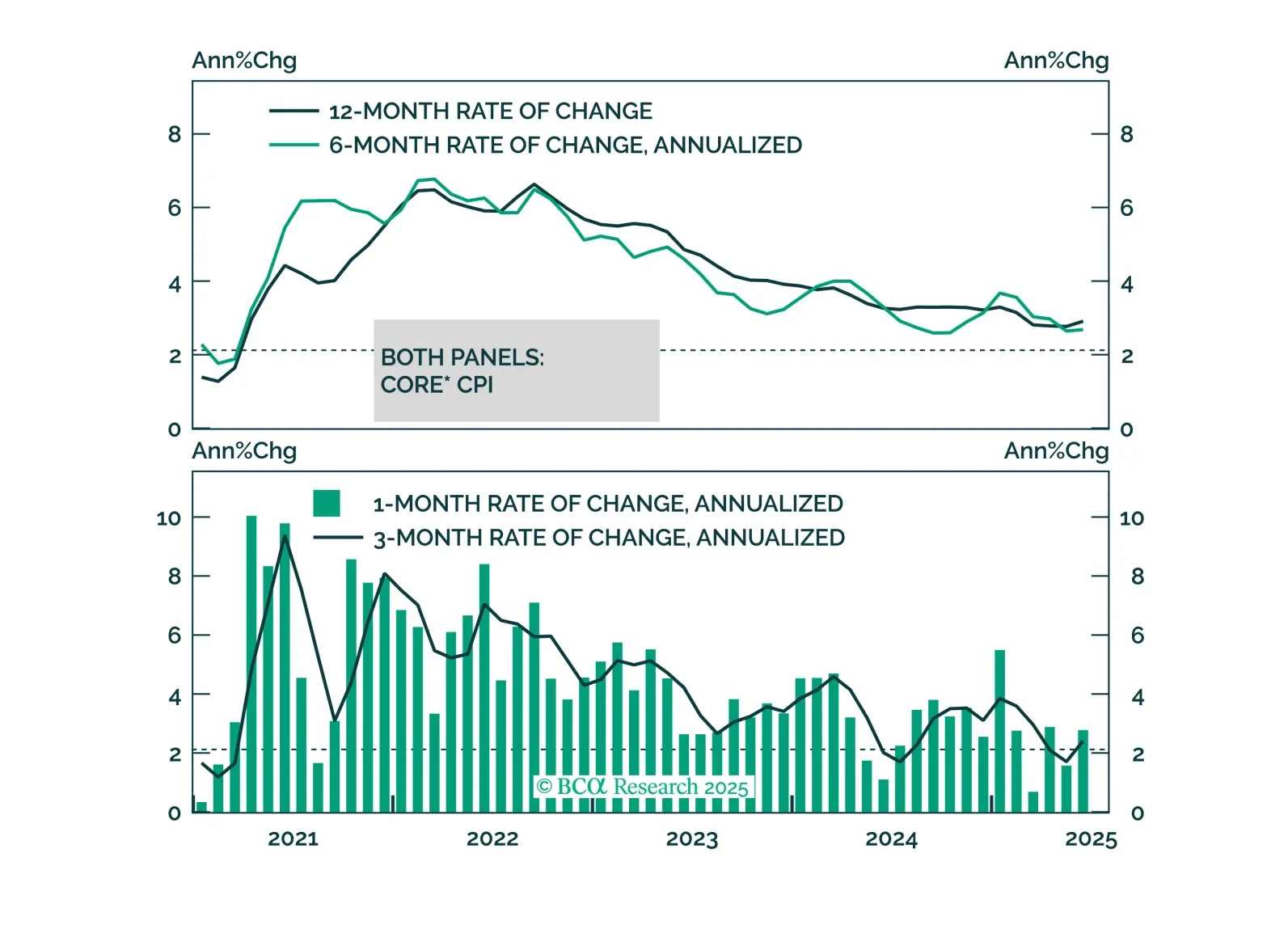

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.

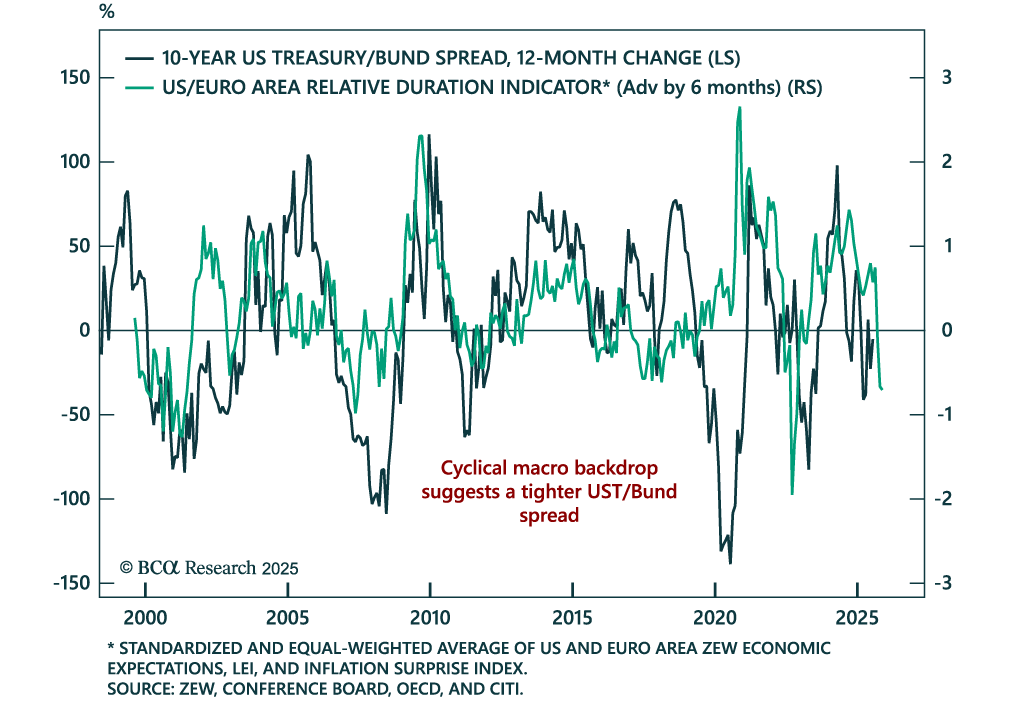

Volatility is back in UST/Bund spreads. We unpack what’s driving the moves and explain what we are watching for tactical opportunities in the UST/Bund spread.

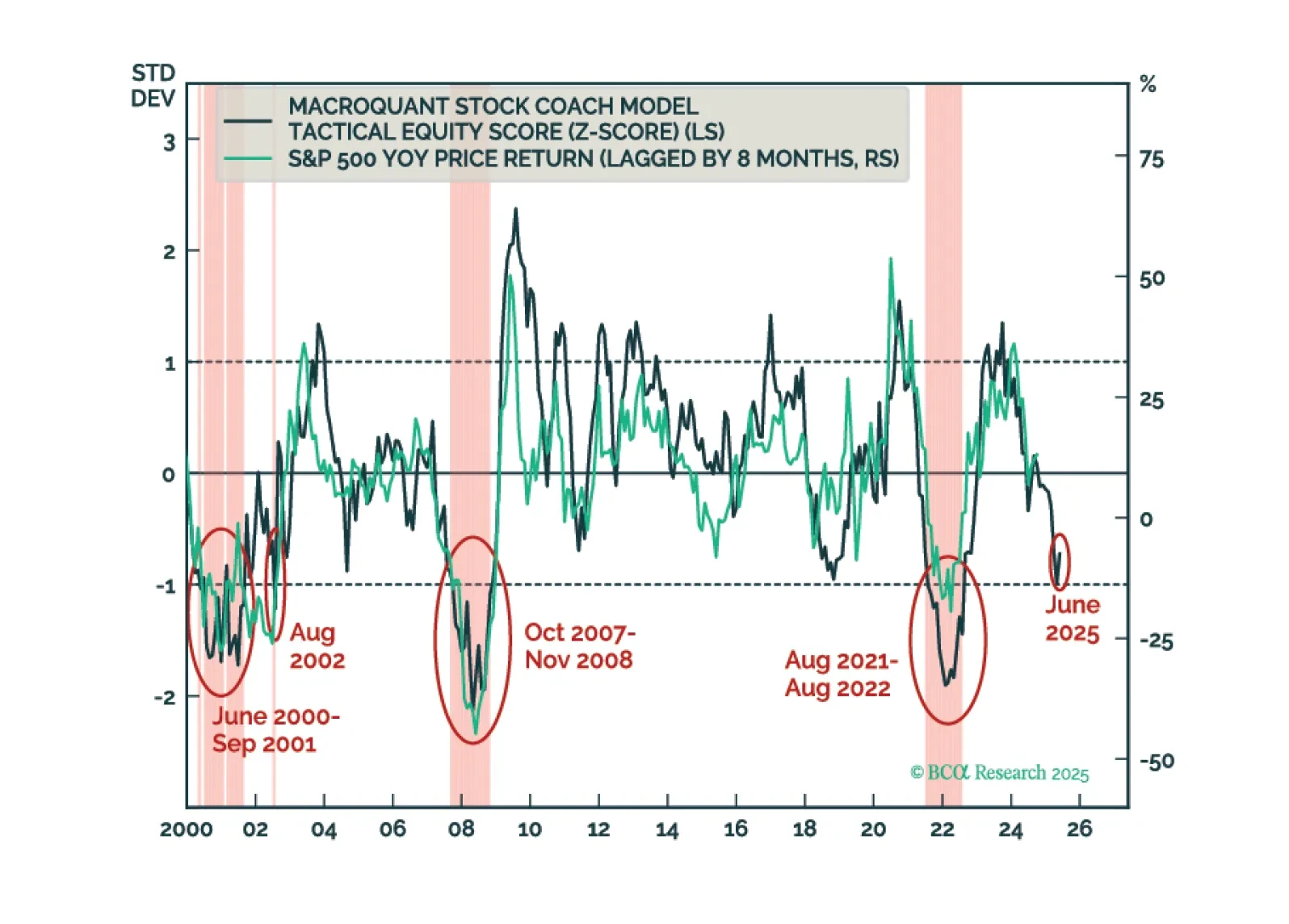

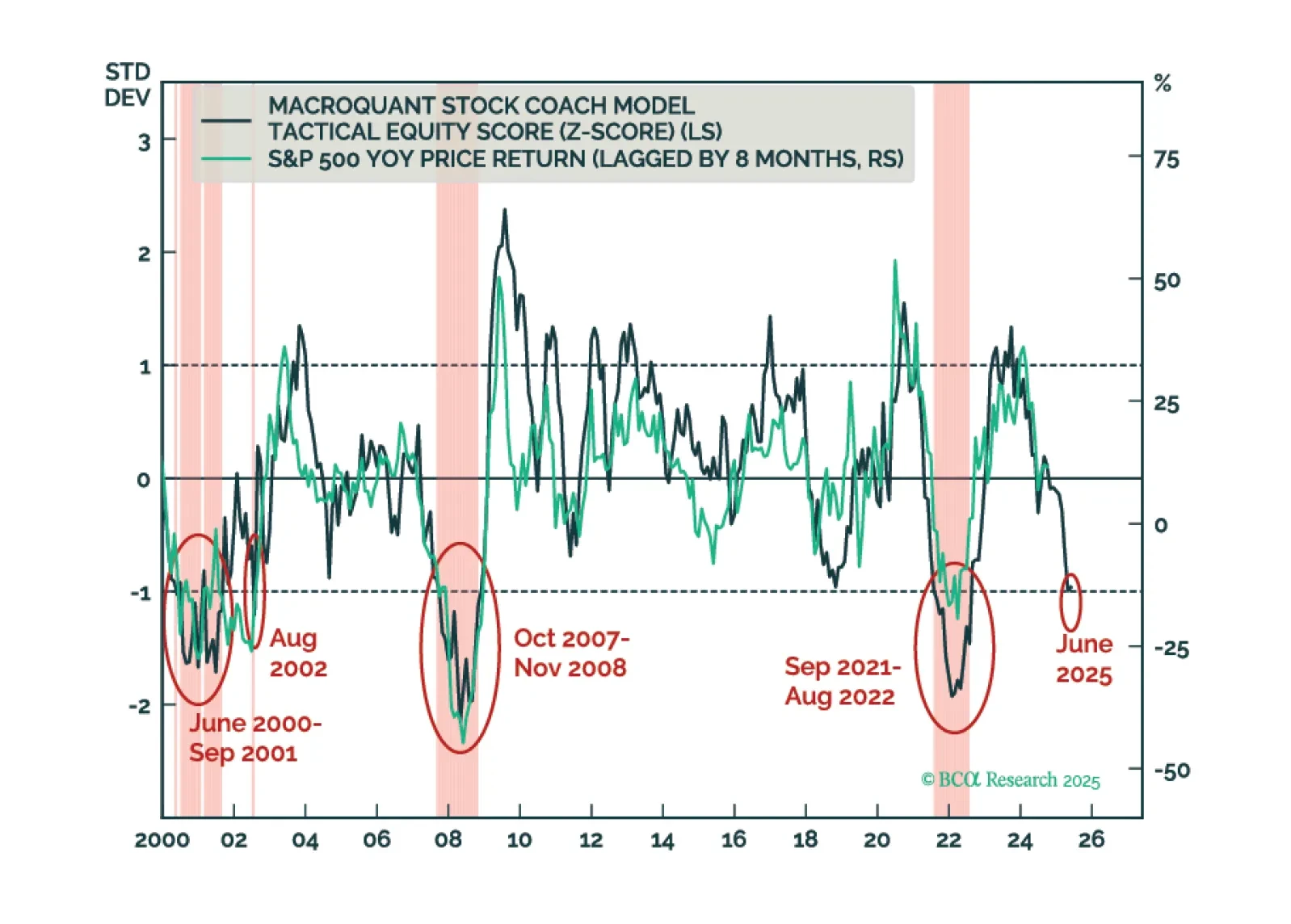

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.

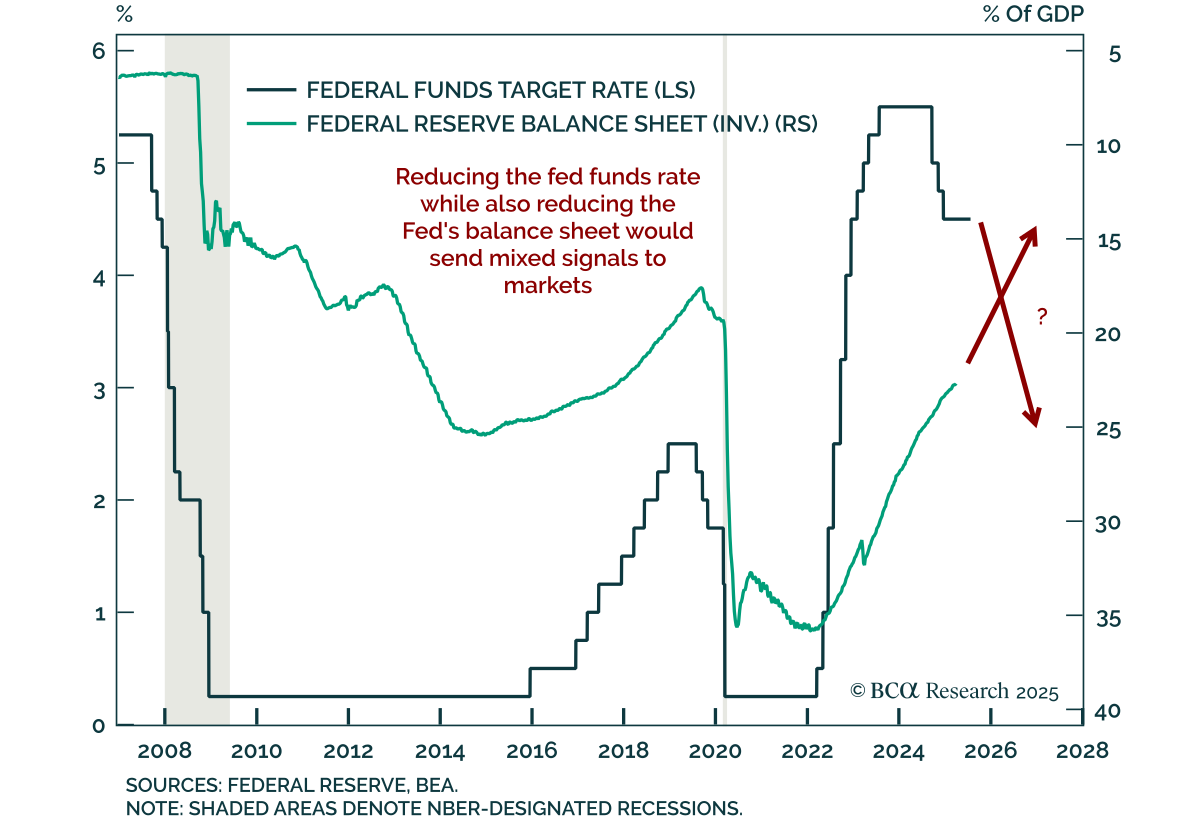

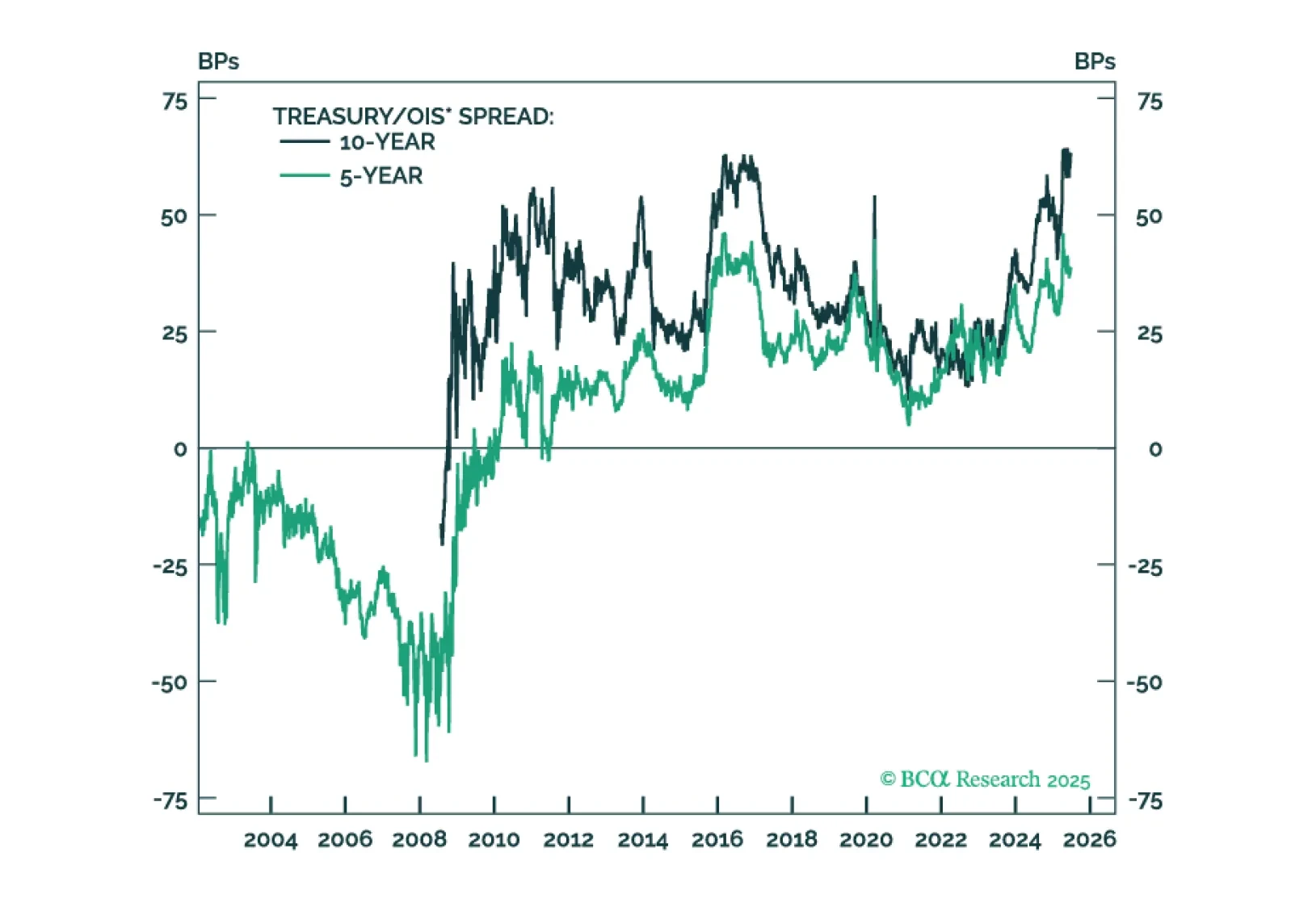

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.