Gov Sovereigns/Treasurys

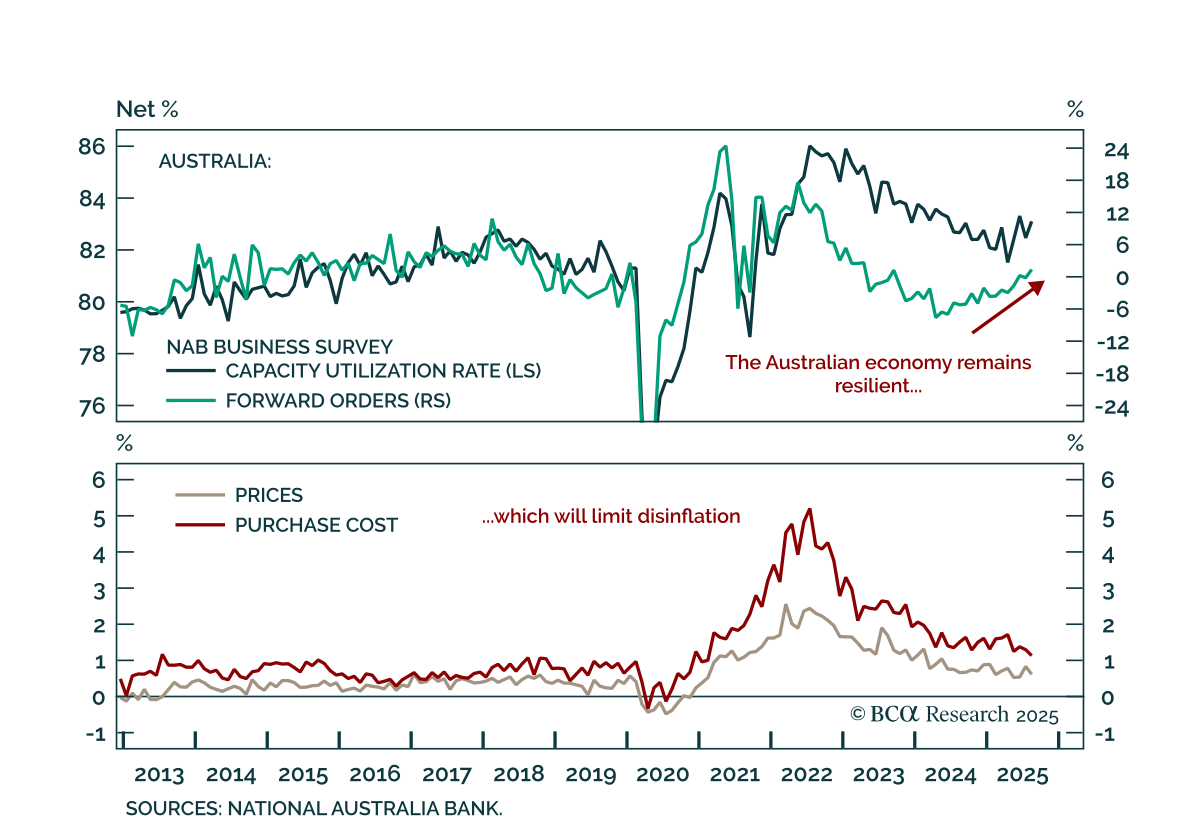

Australia’s NAB survey shows underlying resilience, reinforcing our underweight on ACGBs and the case for AUD flatteners vs. CAD steepeners. The August survey was mixed, with current conditions improving to 7 from 5, while business confidence softened to 4…

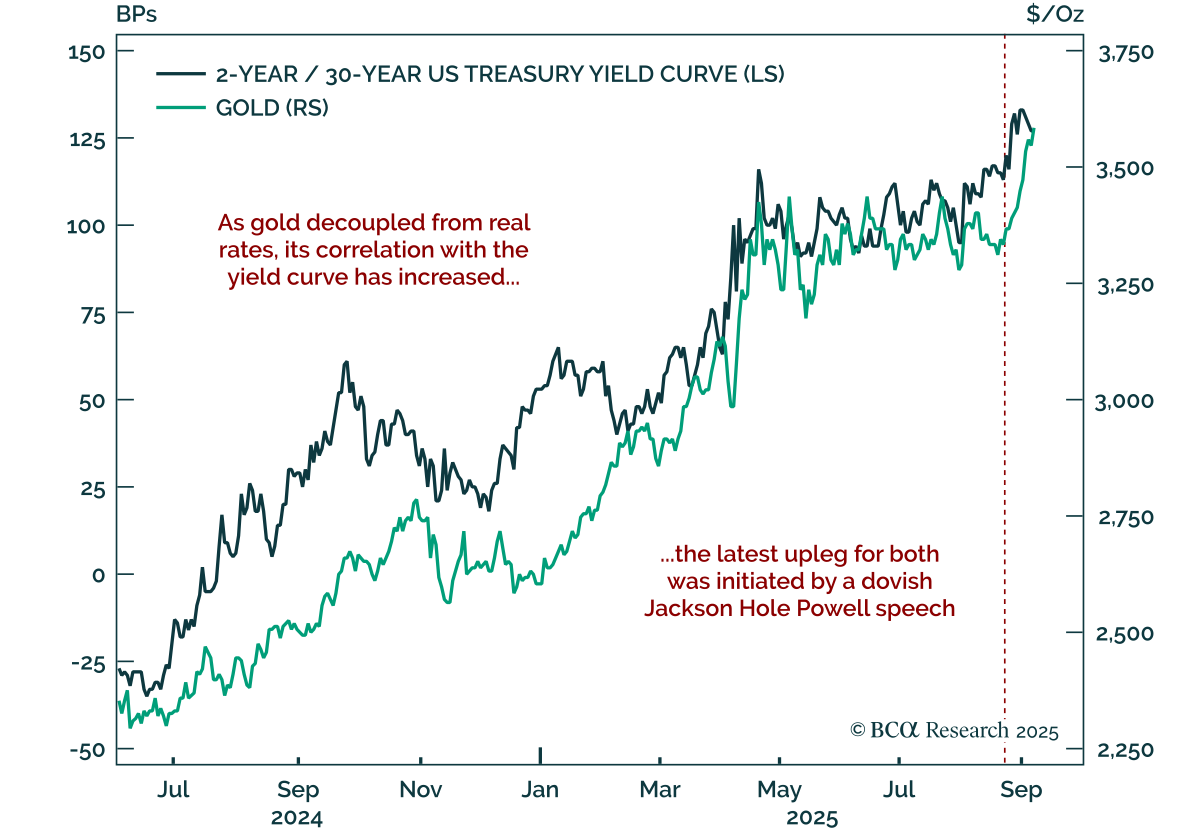

Gold and steepeners remain core trades, supported by structural shifts in markets and policy. Gold broke out of the consolidation range it had been in since April, supported by central-bank buying and heightened policy uncertainty. Moreover, the…

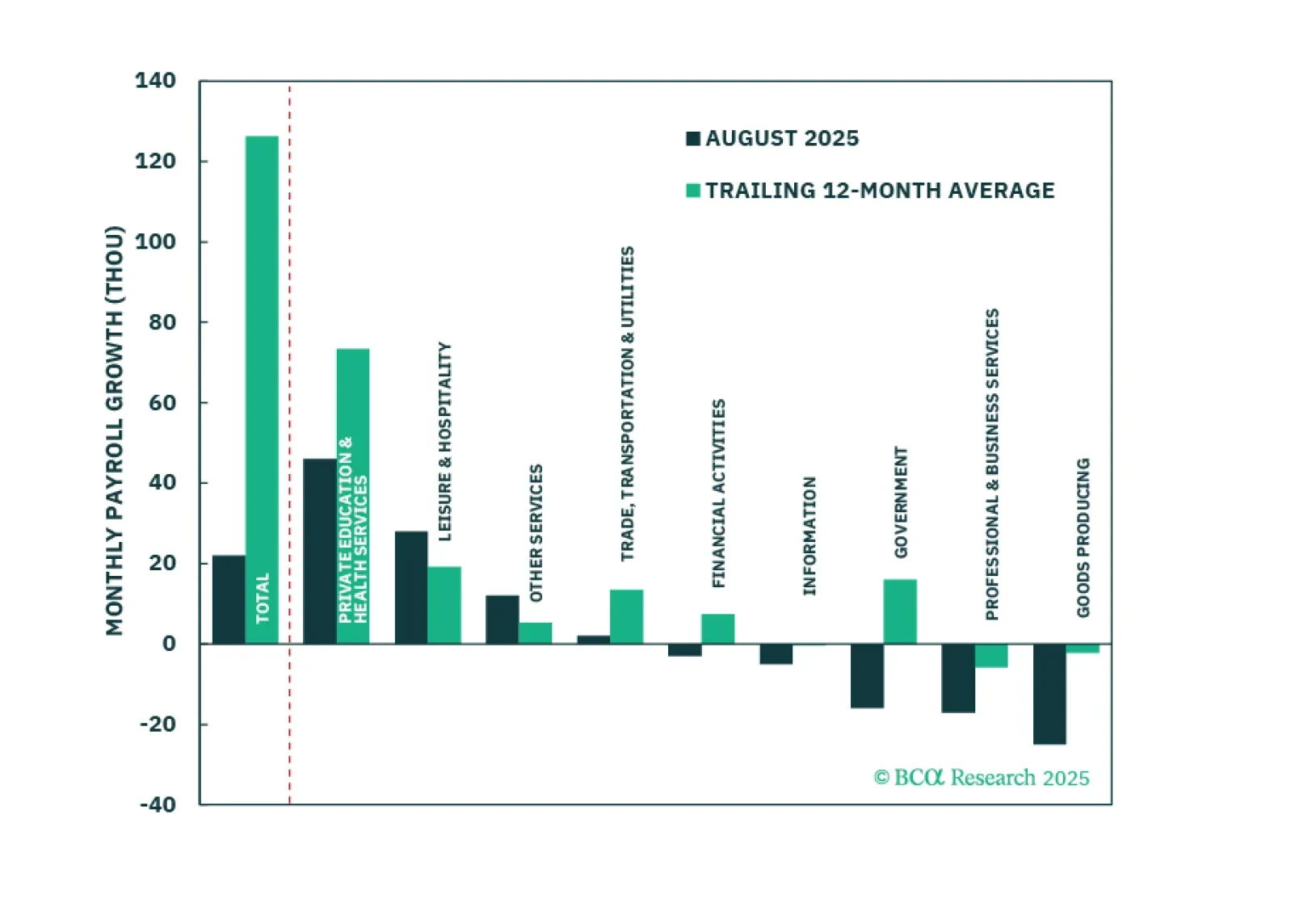

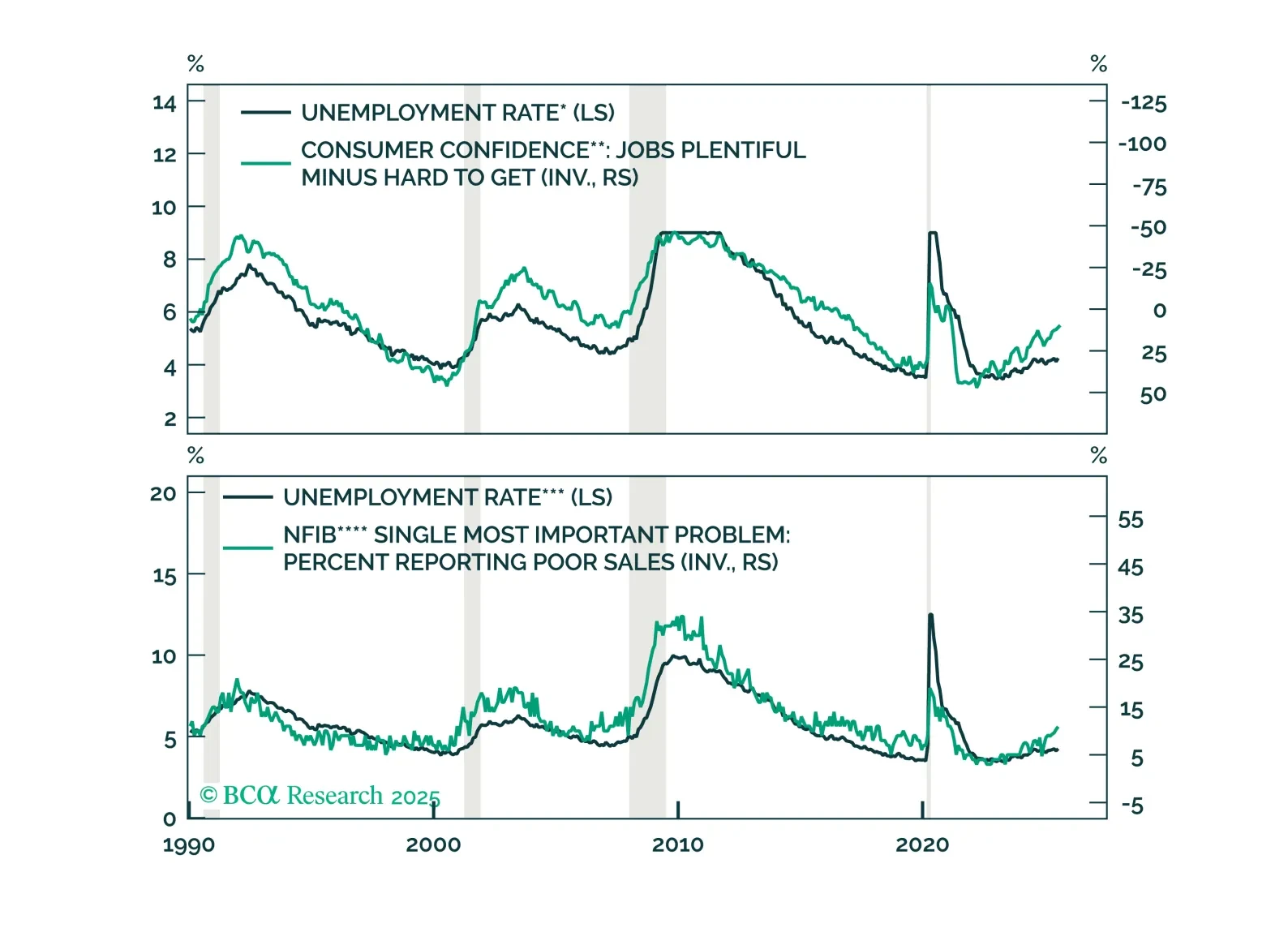

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

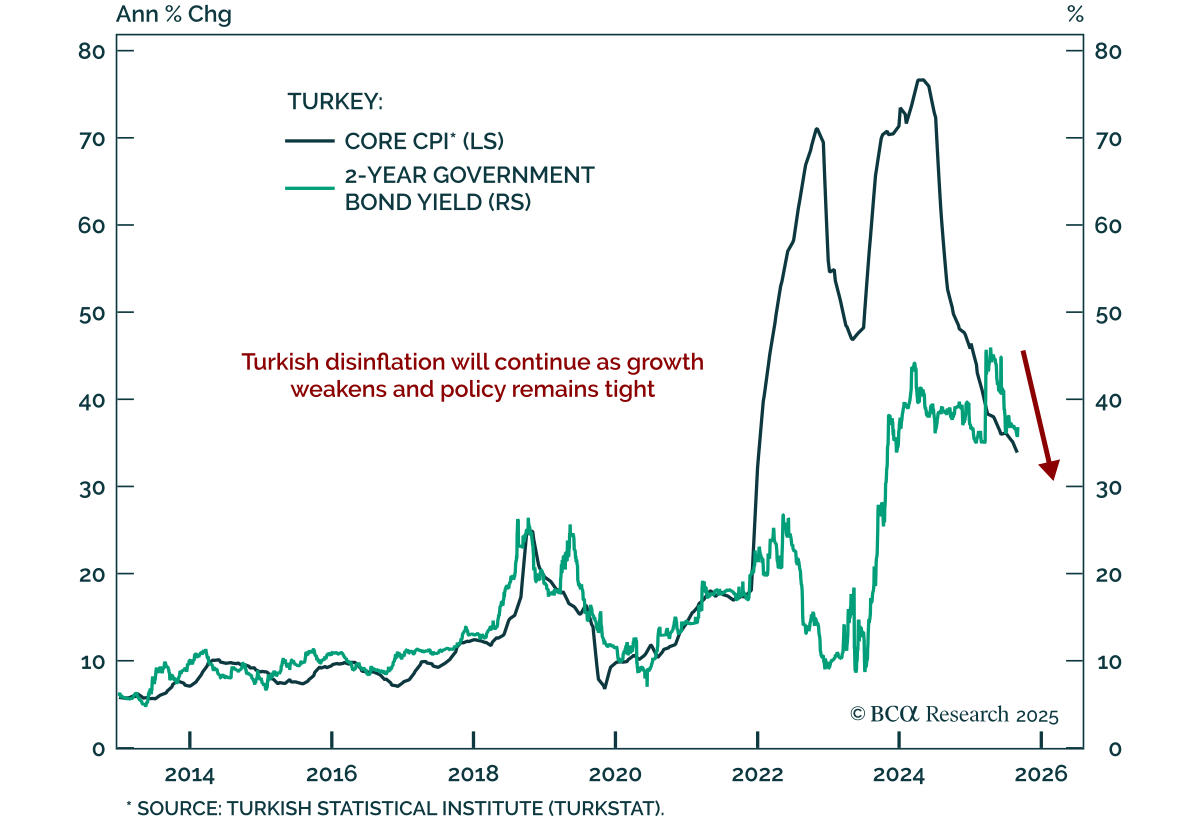

Turkey’s disinflation trend remains intact, supporting a bullish case for short-term bonds. Headline inflation eased to 33% y/y in August from 33.5% in July. Our Emerging Markets strategists expect further slowing as monetary and fiscal policy stay tight.…

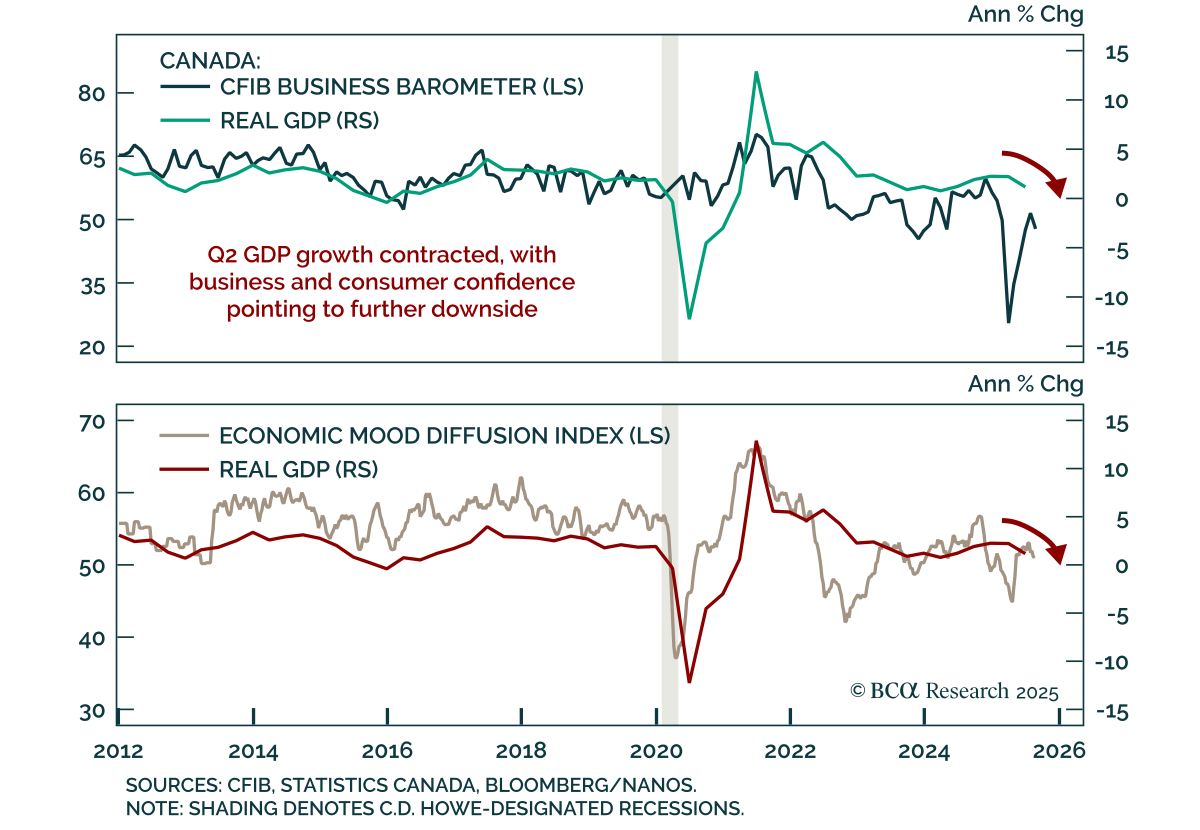

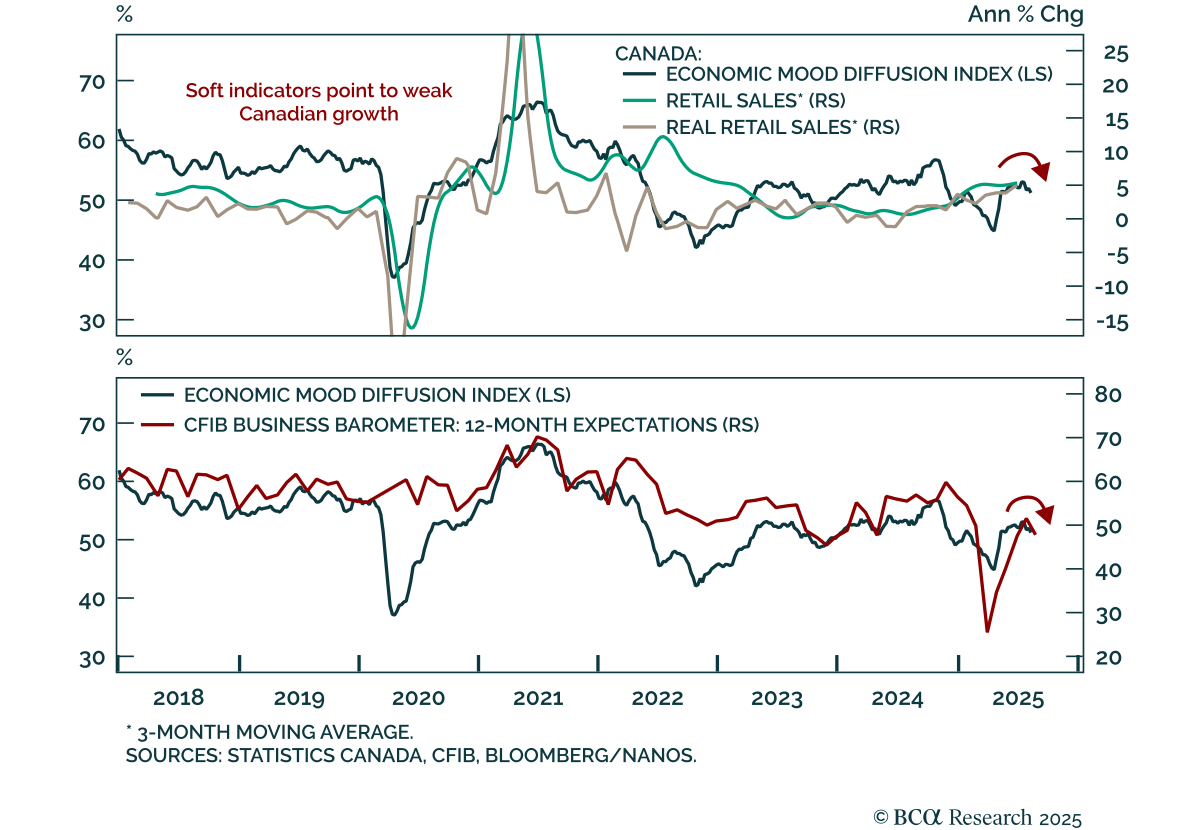

Canada’s Q2 GDP contraction underscores a fragile backdrop where growth risks will outweigh inflation, supporting further BoC easing. Real GDP contracted at an annualized 1.6% after expanding 2.2% in Q1, consistent with survey data showing weaker confidence…

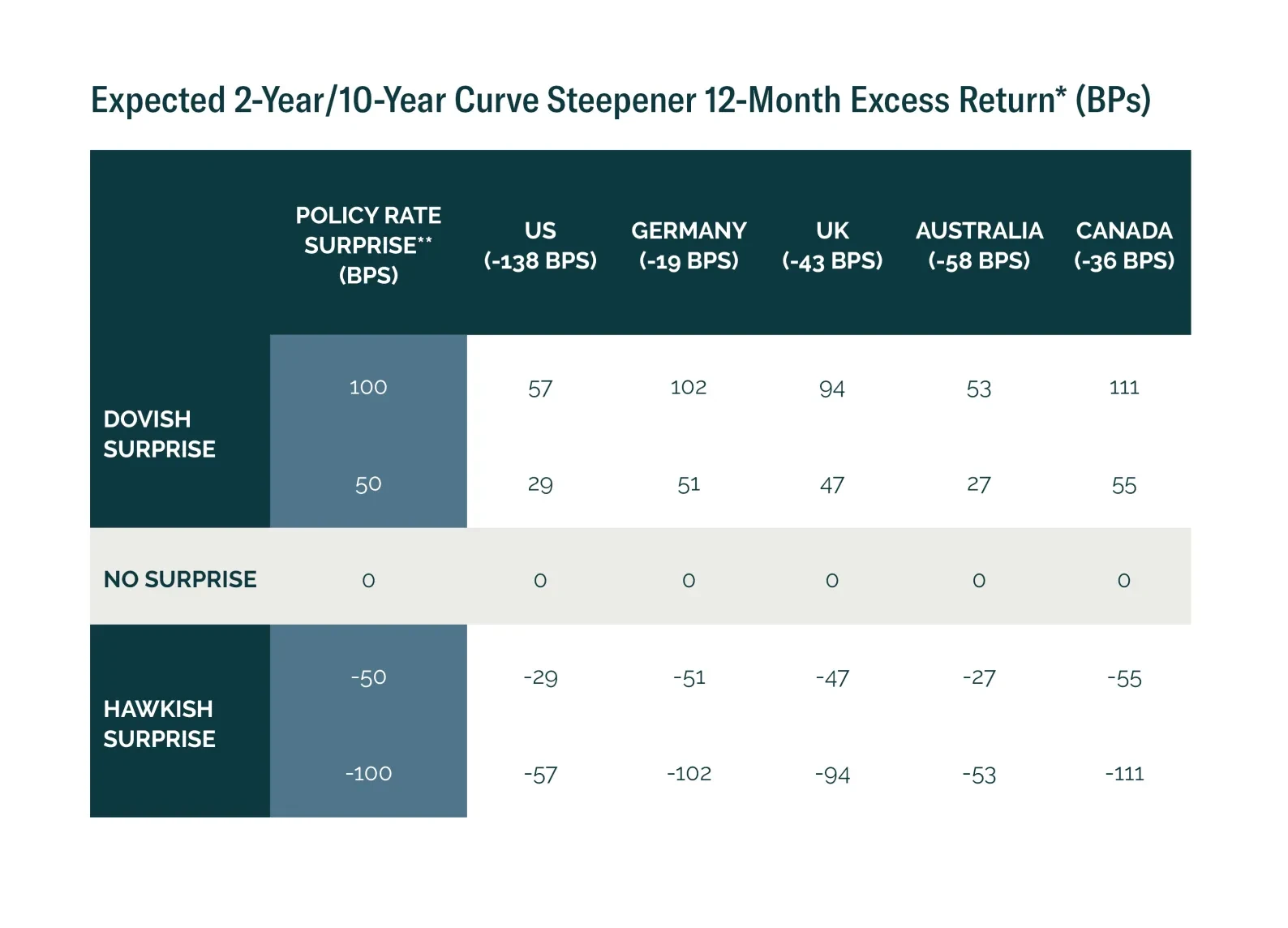

Monetary policy surprises shape curve trade returns. We show where steepeners and flatteners offer the best risk-reward in today’s market.

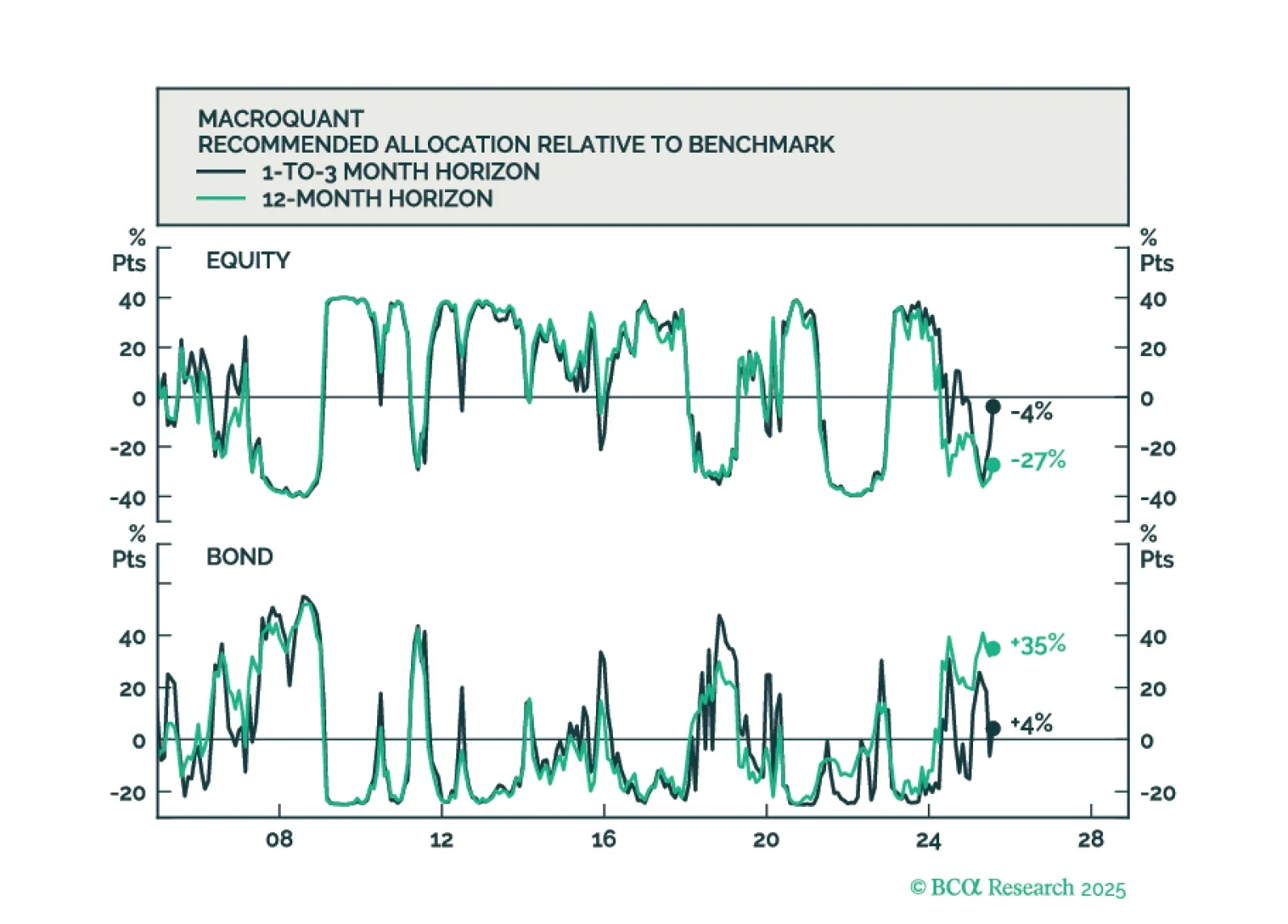

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

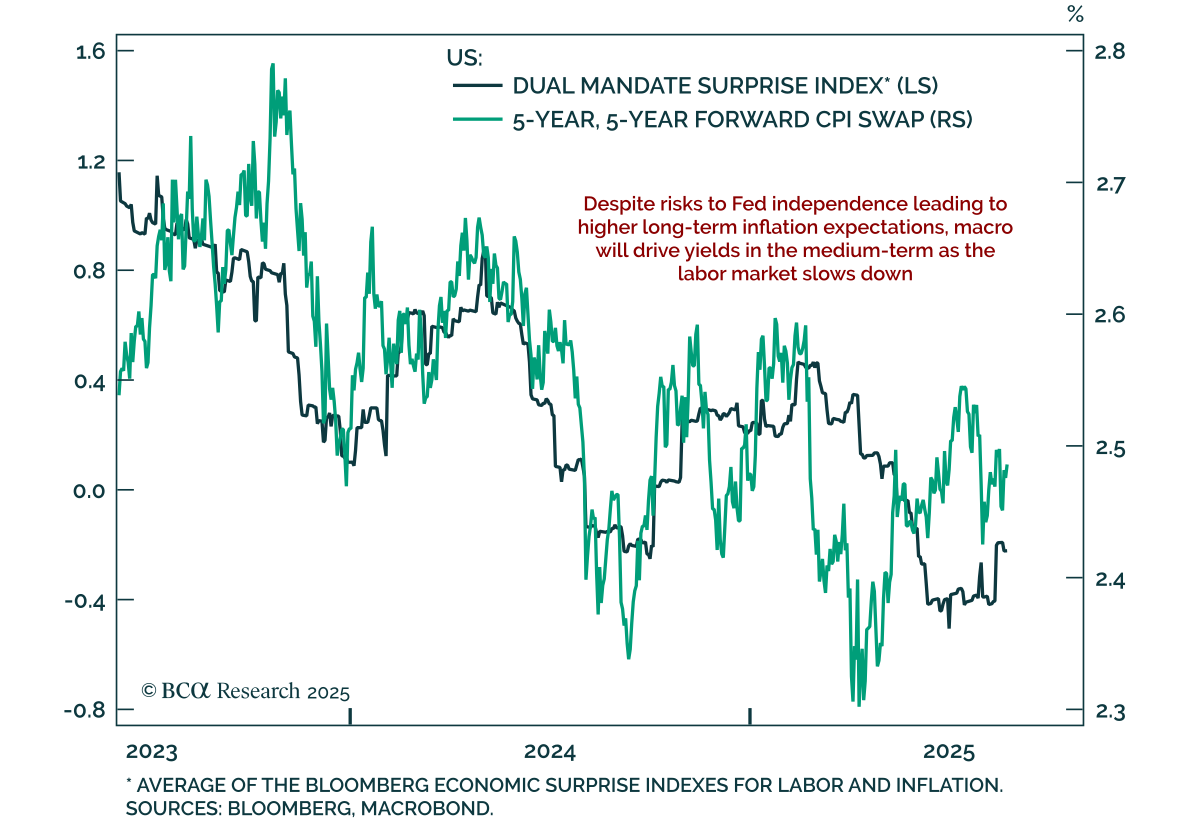

Trump’s firing of Fed Governor Cook raises Fed-independence risks, reinforcing steepener trades. The announcement, aimed at expanding presidential control over the central bank, saw equities fall and bonds initially rally on the prospect of more cuts…

Canada’s fragile growth backdrop reinforces the case for more BoC easing than markets price. June retail sales rose 1.5% m/m, in line with expectations. Excluding autos, sales were stronger at 1.9%. However, the advance estimate for July points to a 0.8%…