Gov Sovereigns/Treasurys

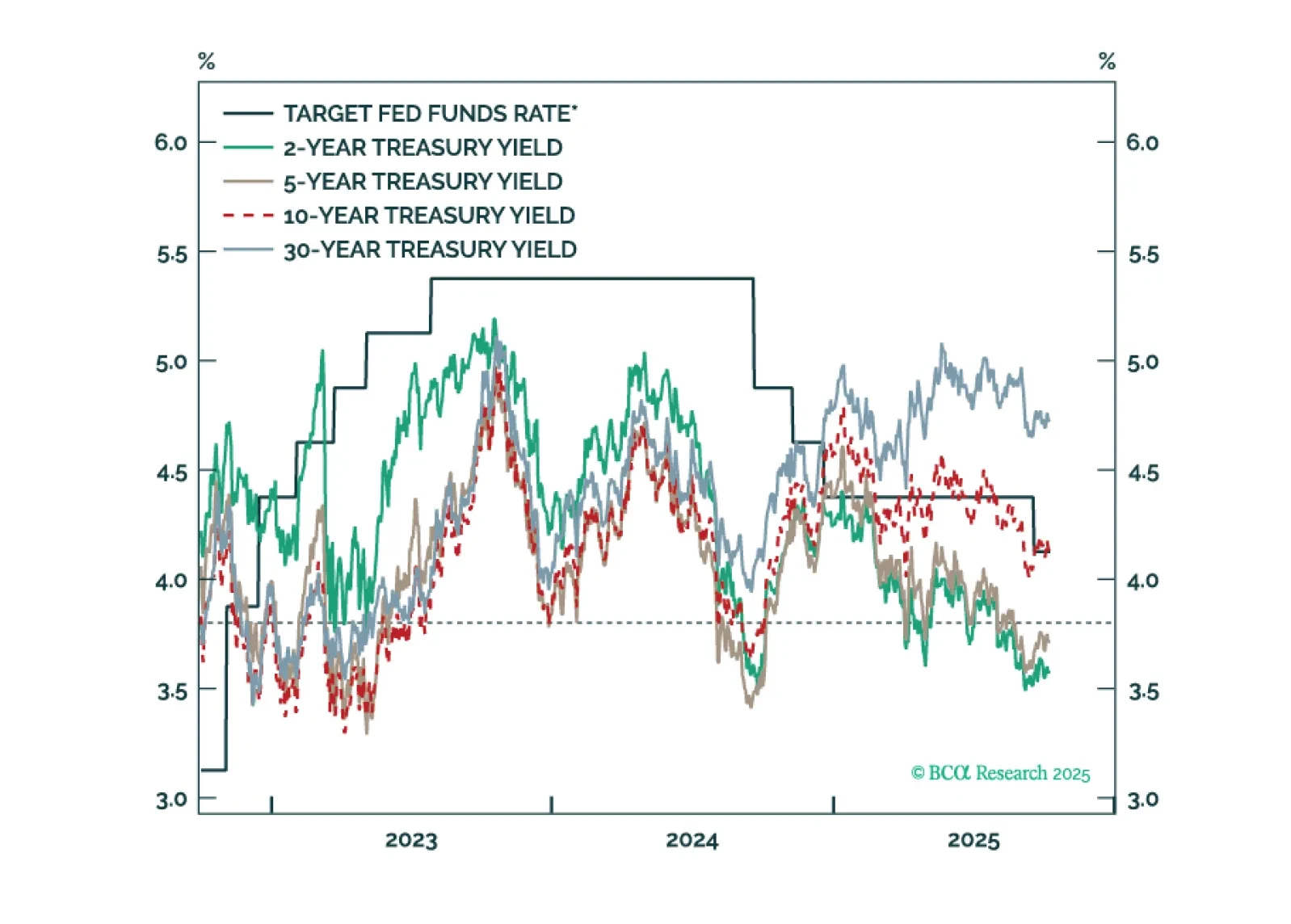

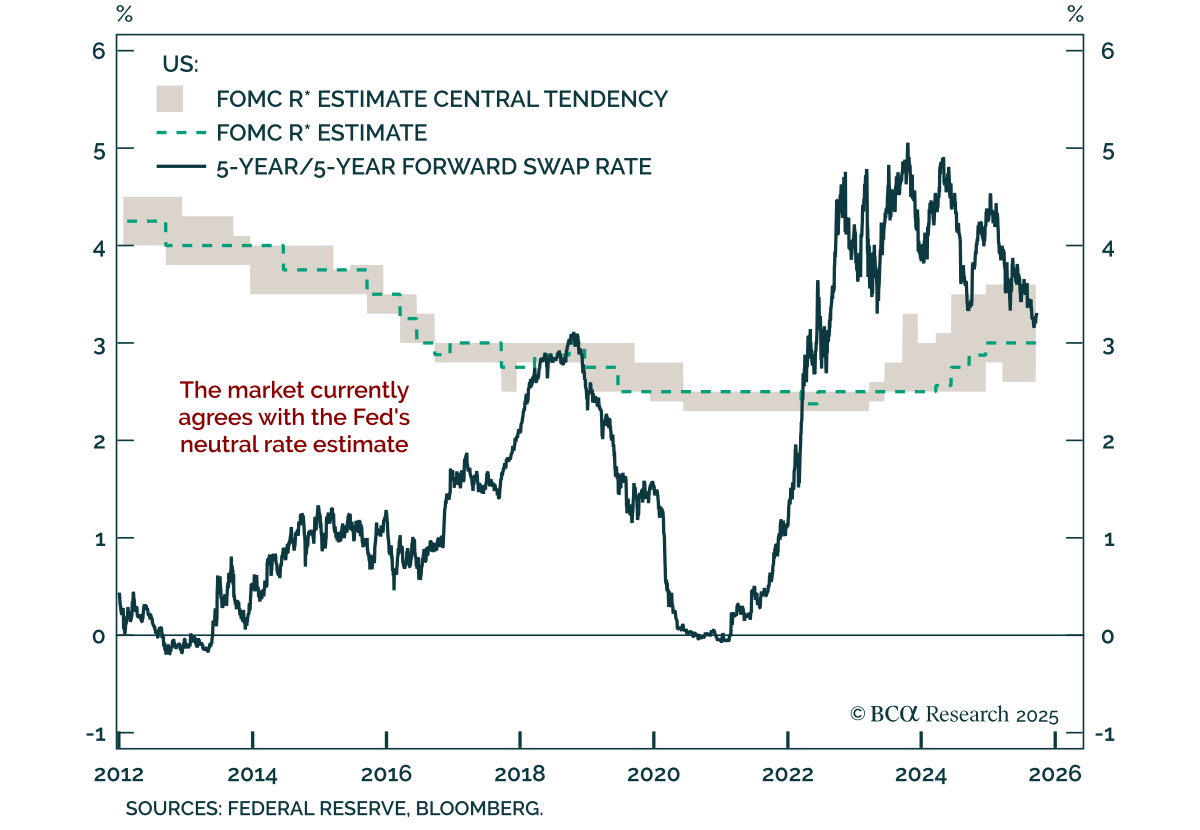

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

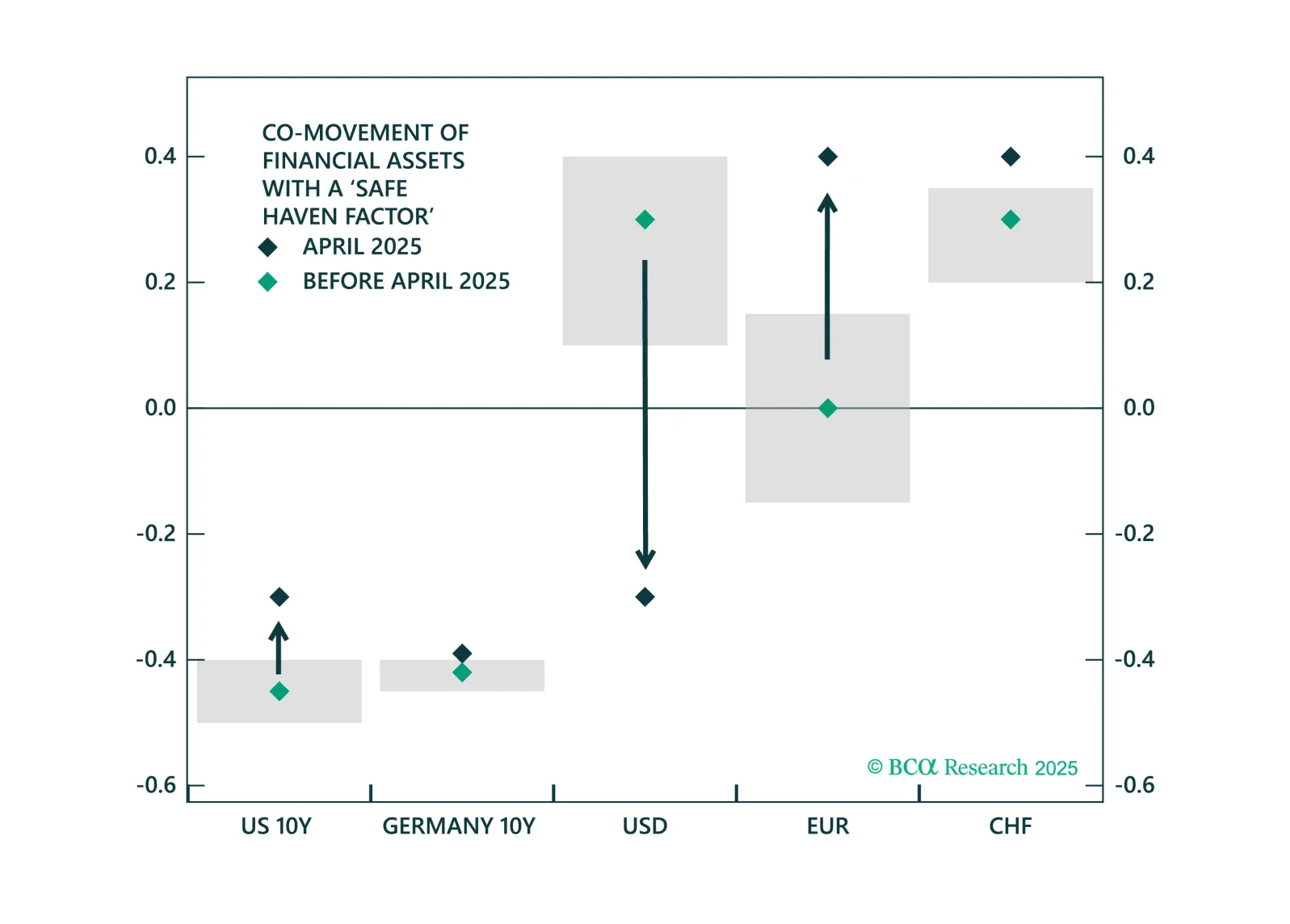

The US Treasury safe haven status is being seriously questioned. We assess whether US Treasuries are still unrivaled or which bond markets and assets are gaining ground. We do so by breaking down which global bond markets are best positioned to absorb risk-off flows in a shifting macro regime.

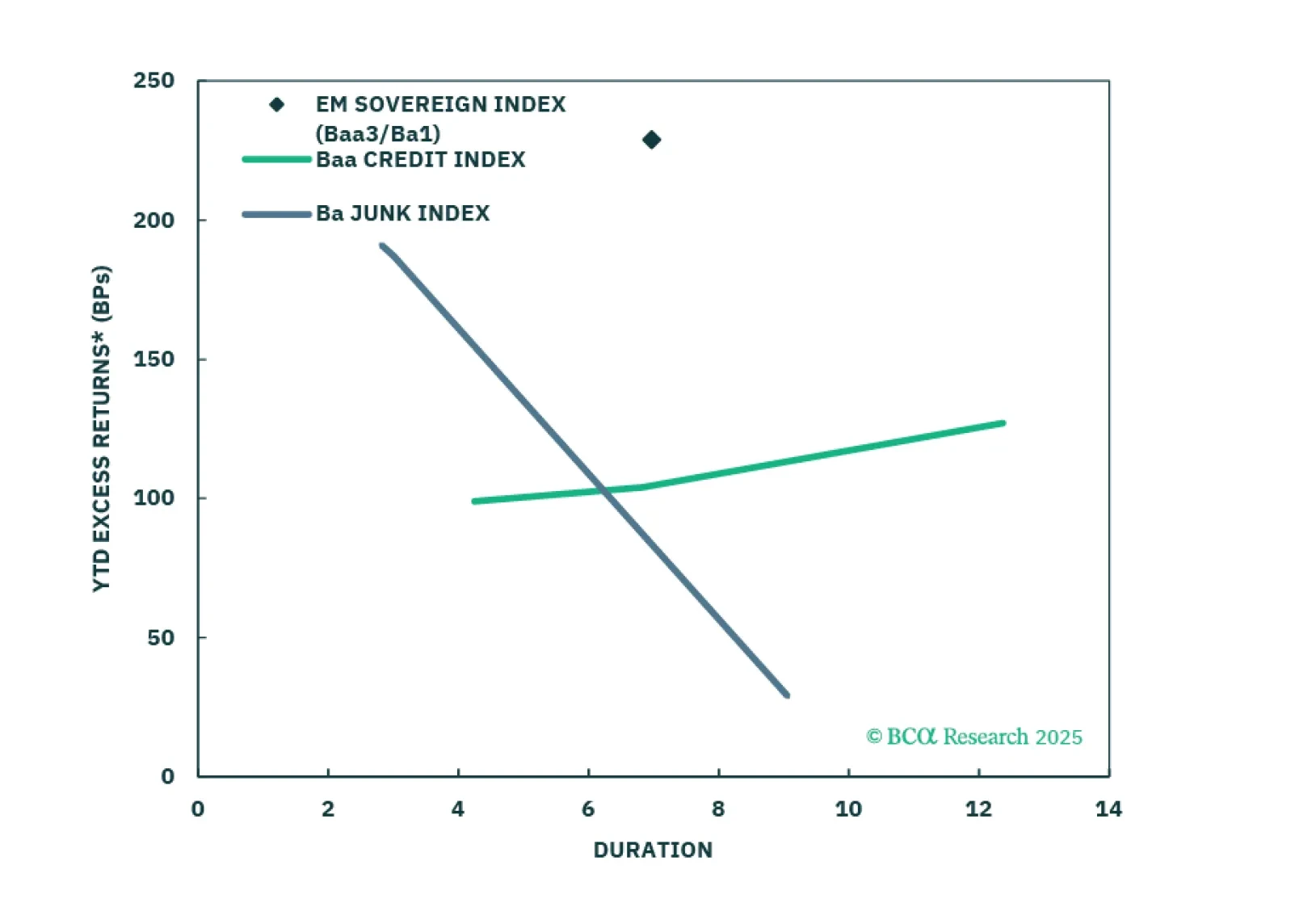

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.