Gov Sovereigns/Treasurys

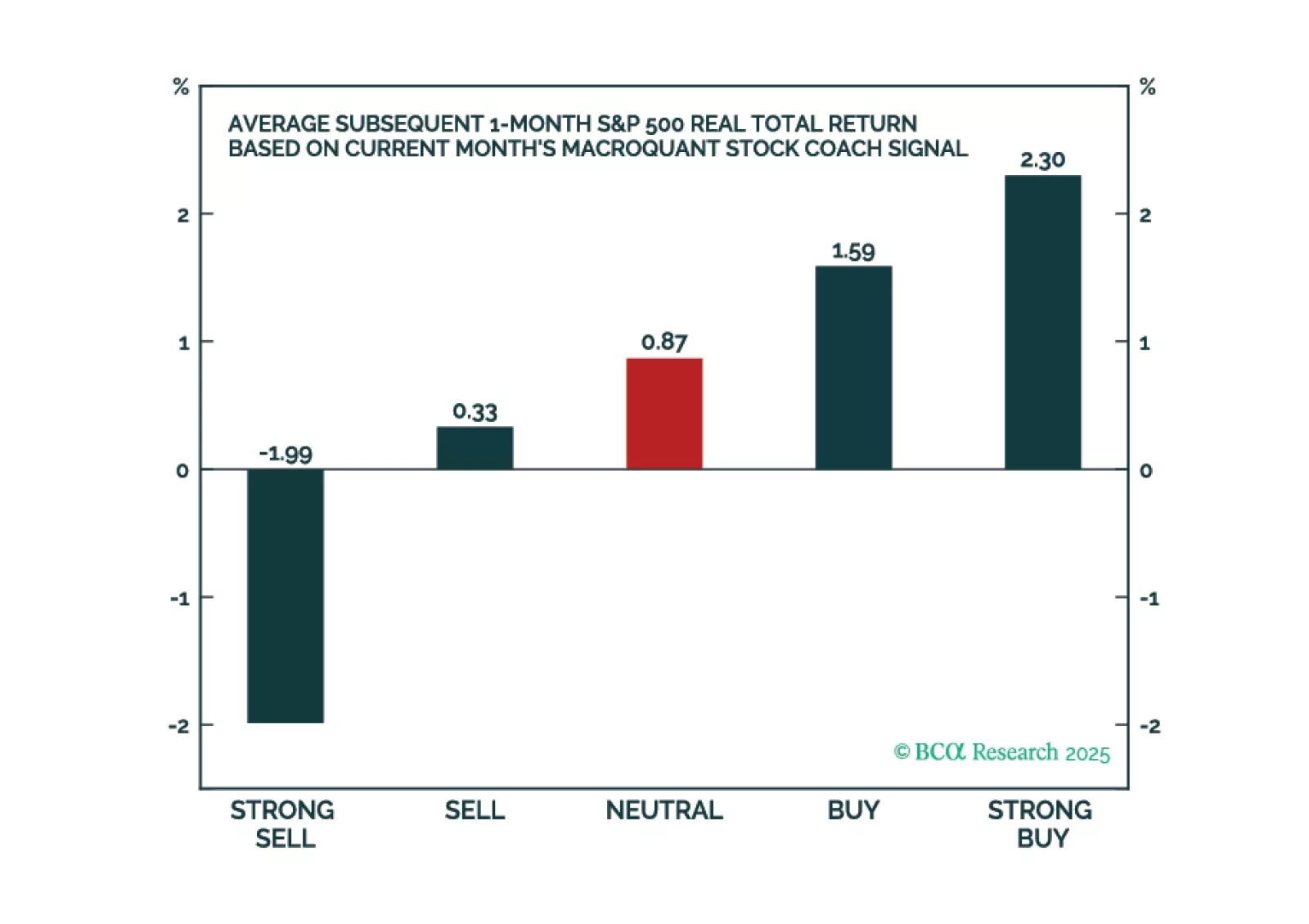

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

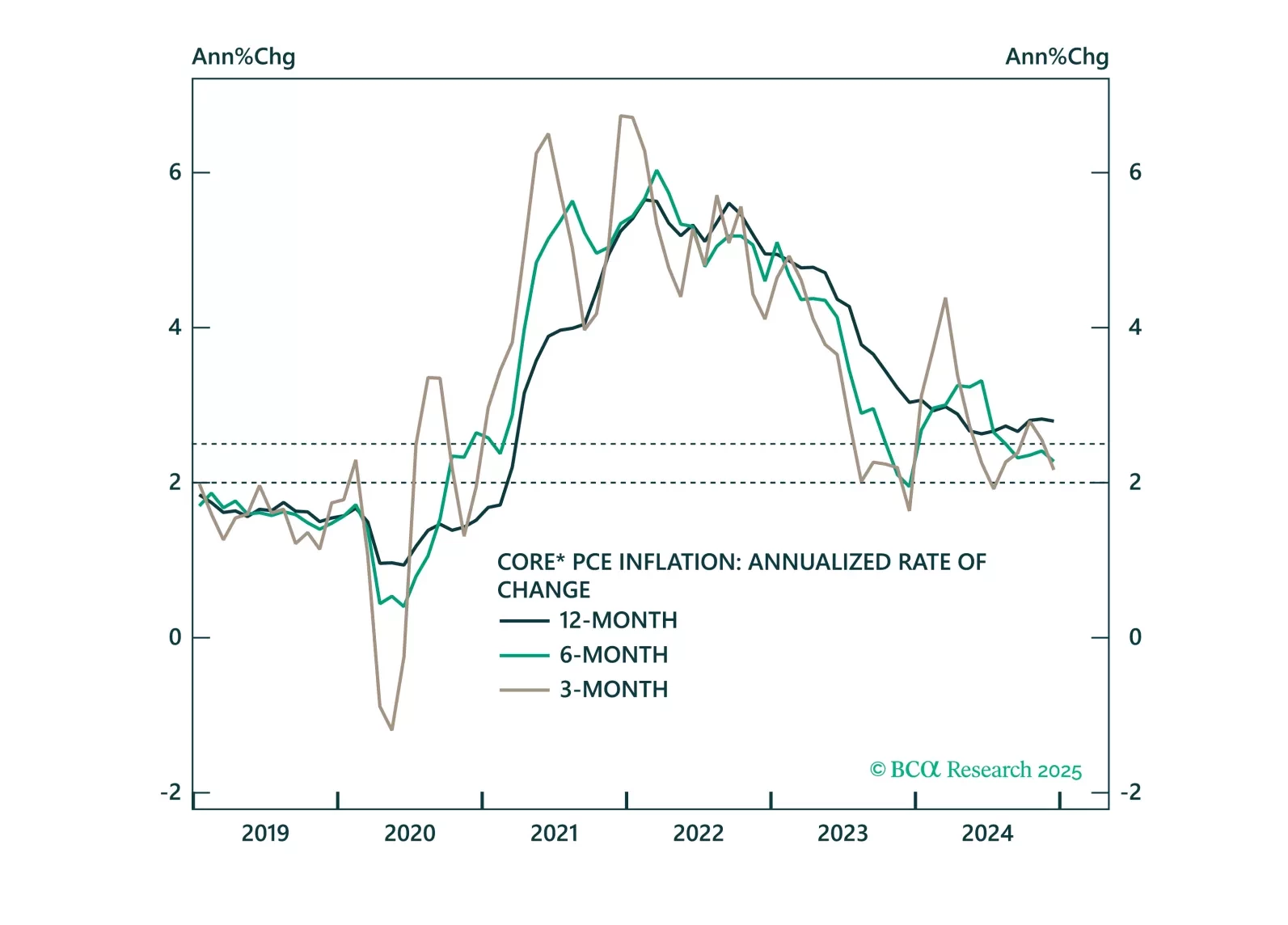

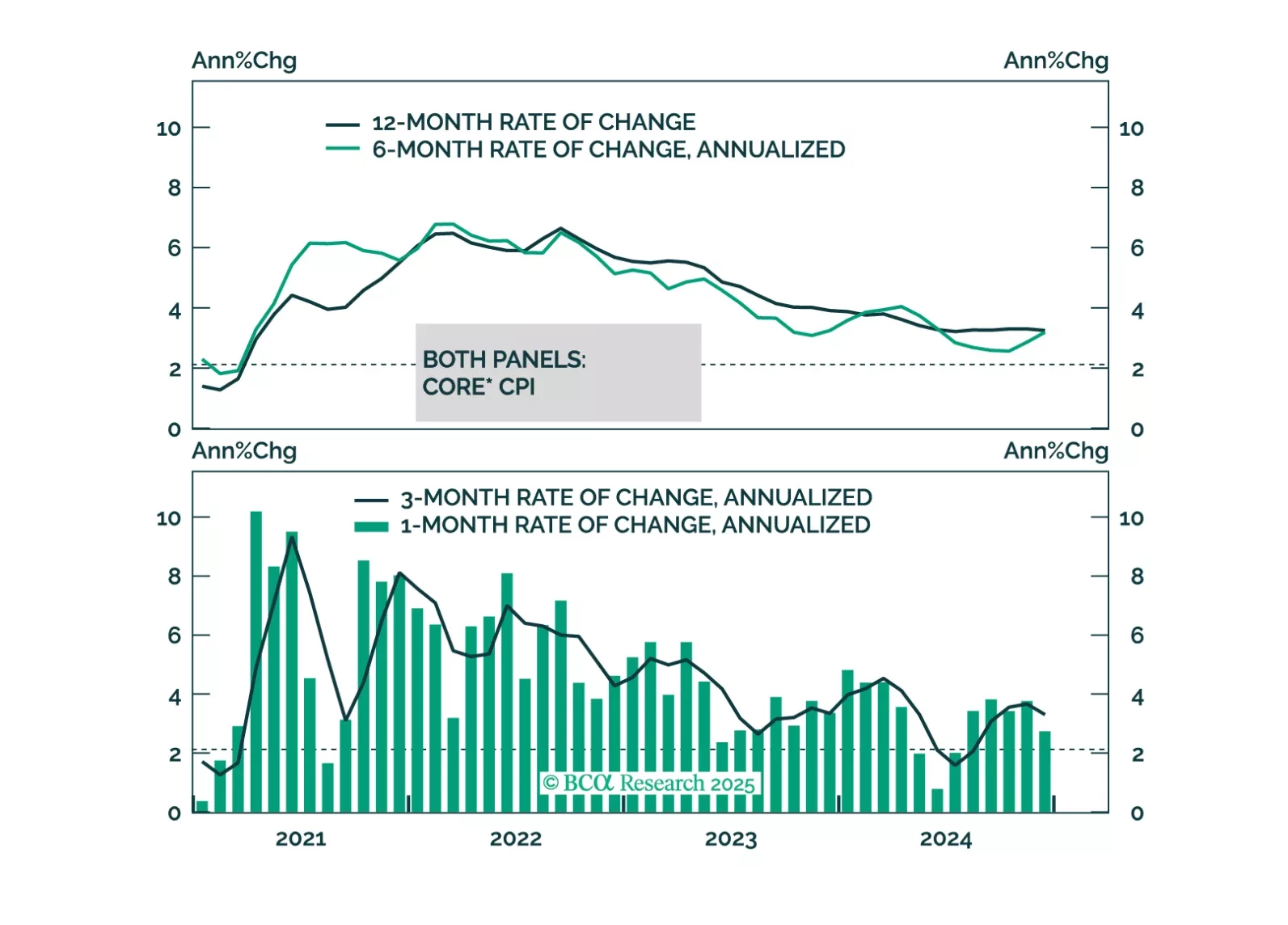

Core PCE inflation came in soft this morning and is tracking well below the Fed’s 2025 forecast. We highlight three upside risks to inflation and preview next week’s employment report.

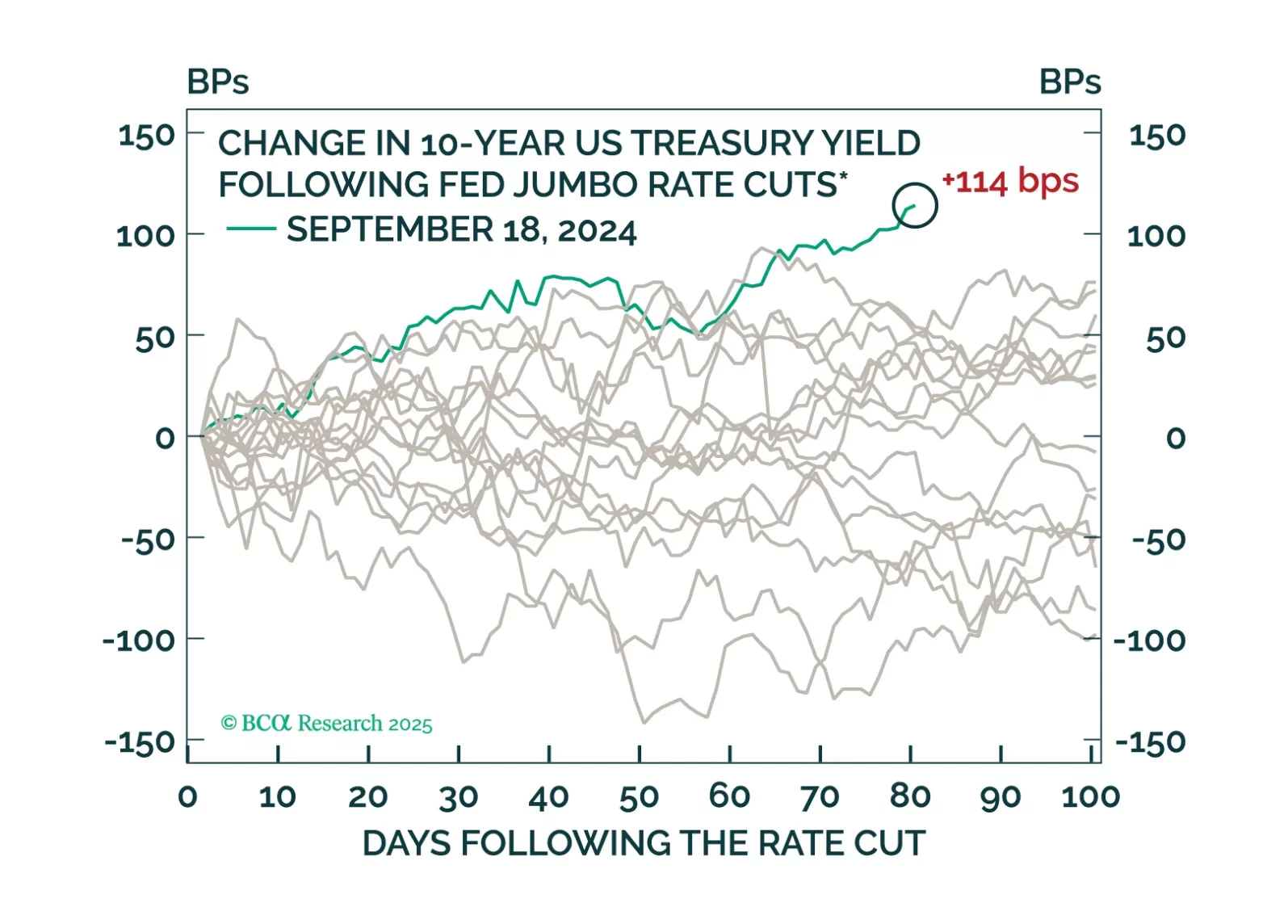

Jay Powell didn’t say much at this afternoon’s FOMC press conference, and monetary policy will continue to take a back seat to fiscal for the next few months.

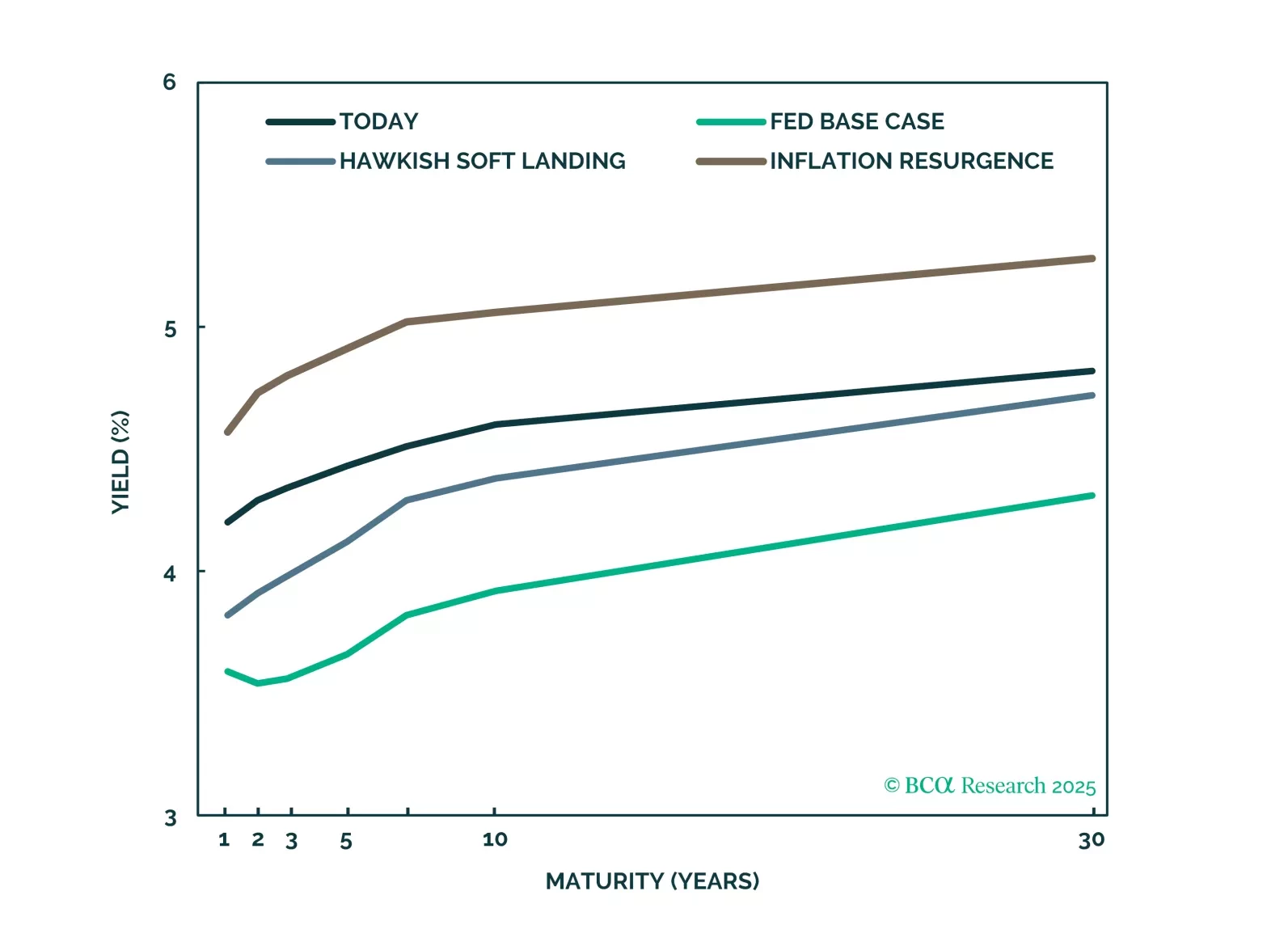

We forecast Treasury and corporate bond returns in three different economic scenarios. This report focuses on what returns might look like in a scenario where inflation is sticky and the Fed makes a hawkish pivot.

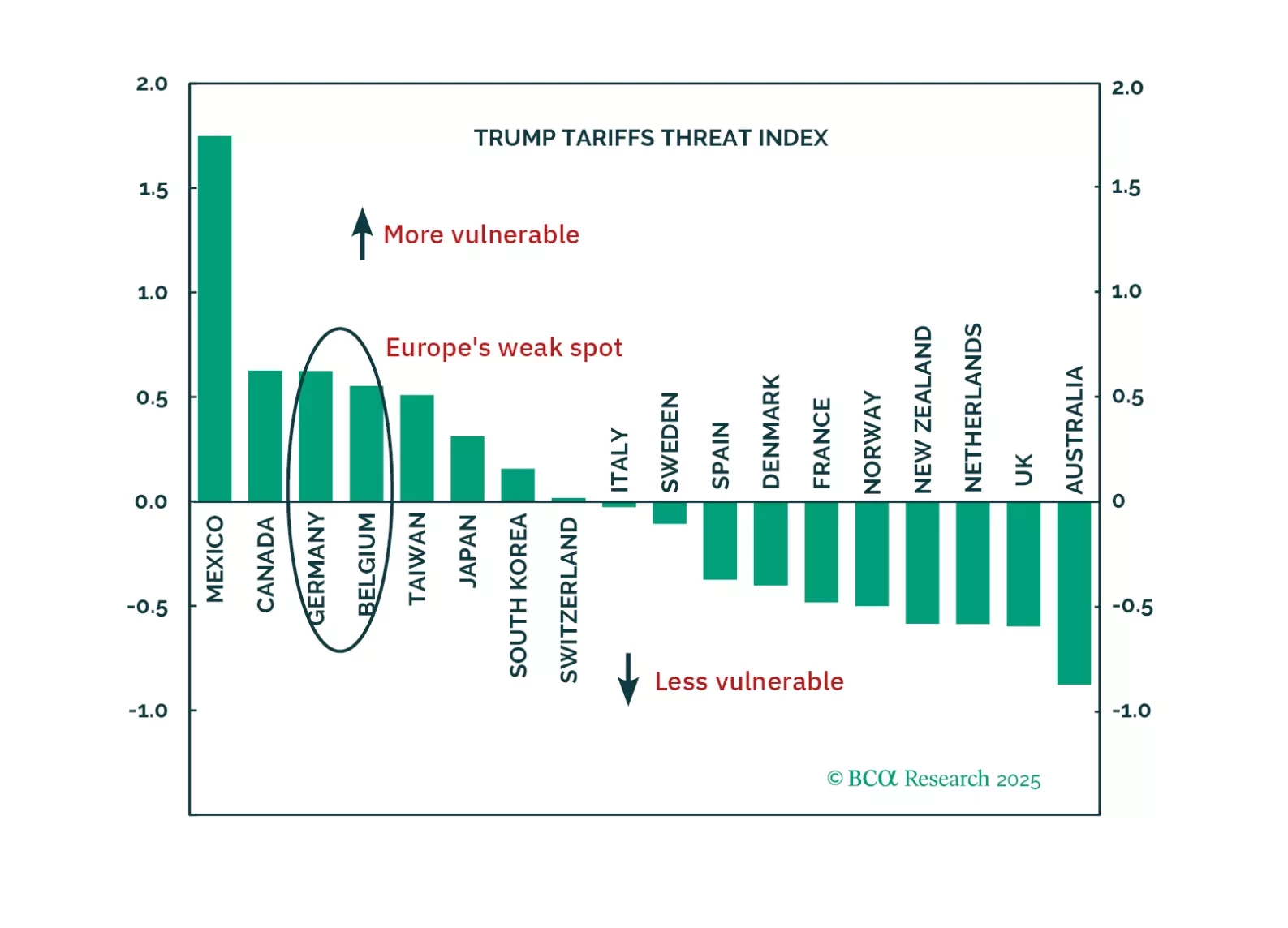

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

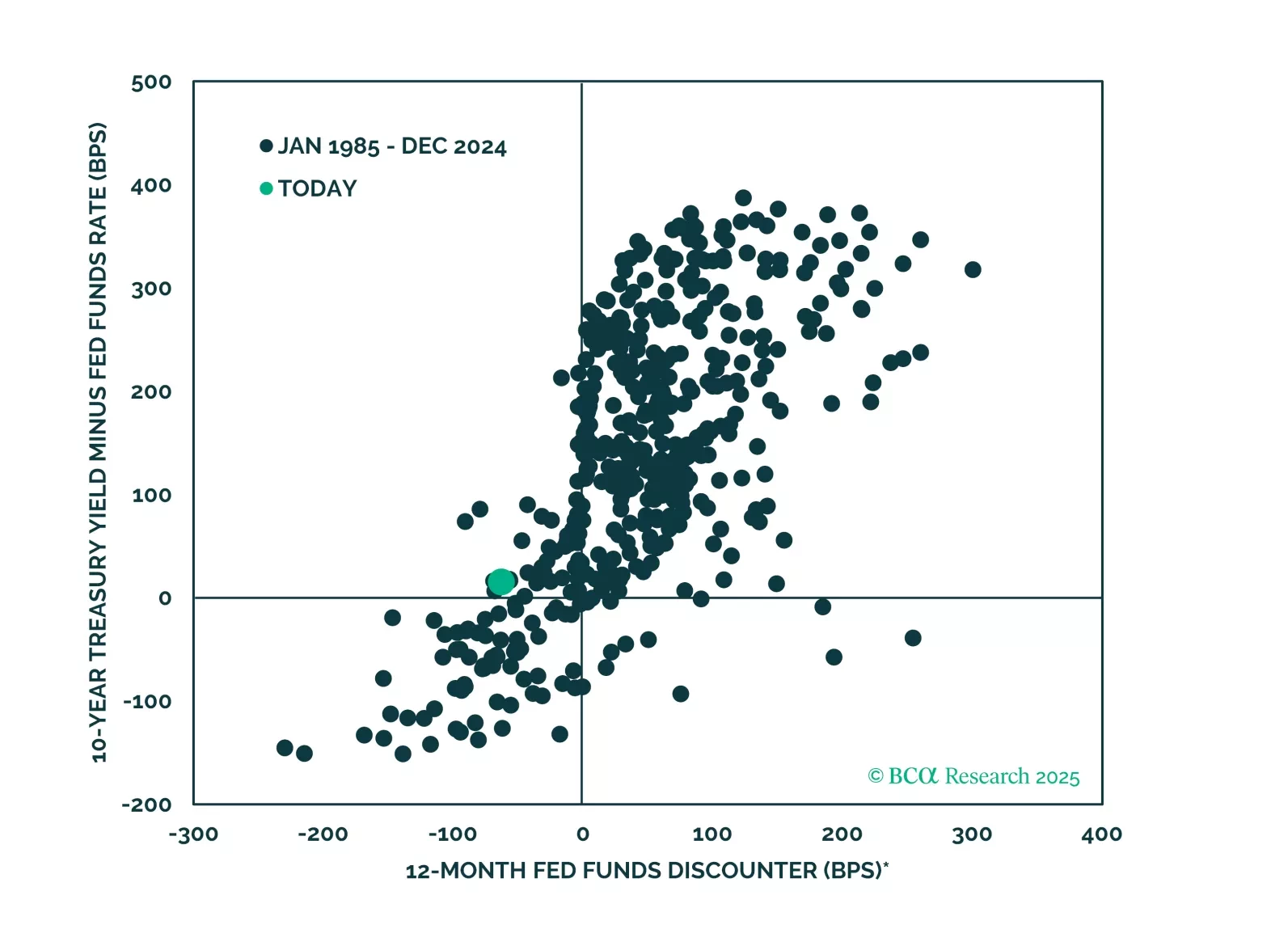

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.

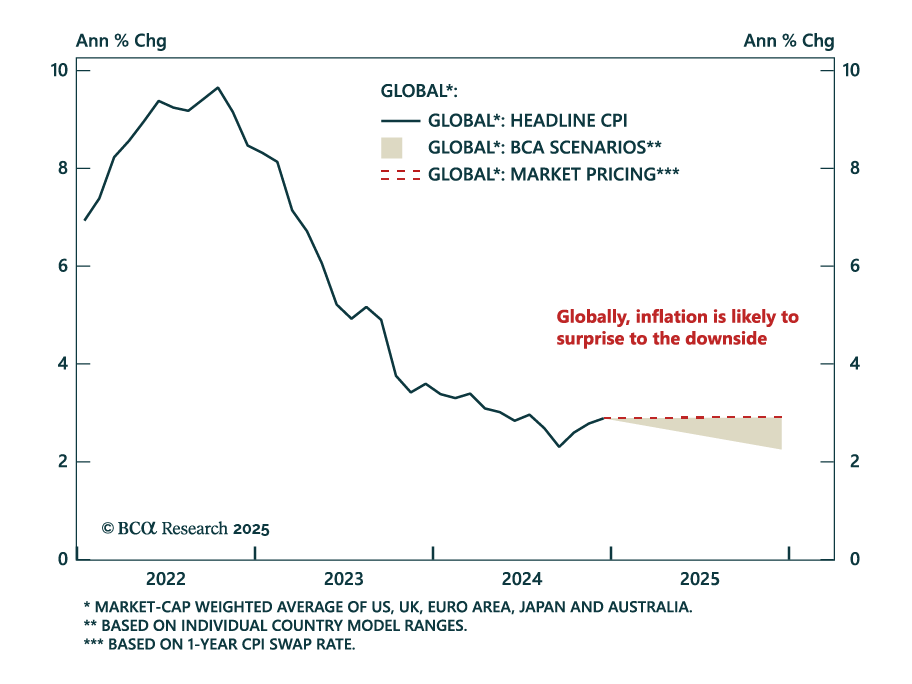

Our thoughts on this morning’s CPI release and some upside risks to inflation that could flare up in the months ahead.

This month, our Here, There, And Everywhere chartpack reiterates our main thesis for 2025: the three main narratives driving markets today – fiscal profligacy, trade war, and geopolitical conflict – will peak at some point in 2025. Why does this matter? All three have been tailwinds to US assets, and their peak should help usher in the peak in US outperformance relative to RoW. We conclude with some slides on our bullish Europe thesis.