Gov Sovereigns/Treasurys

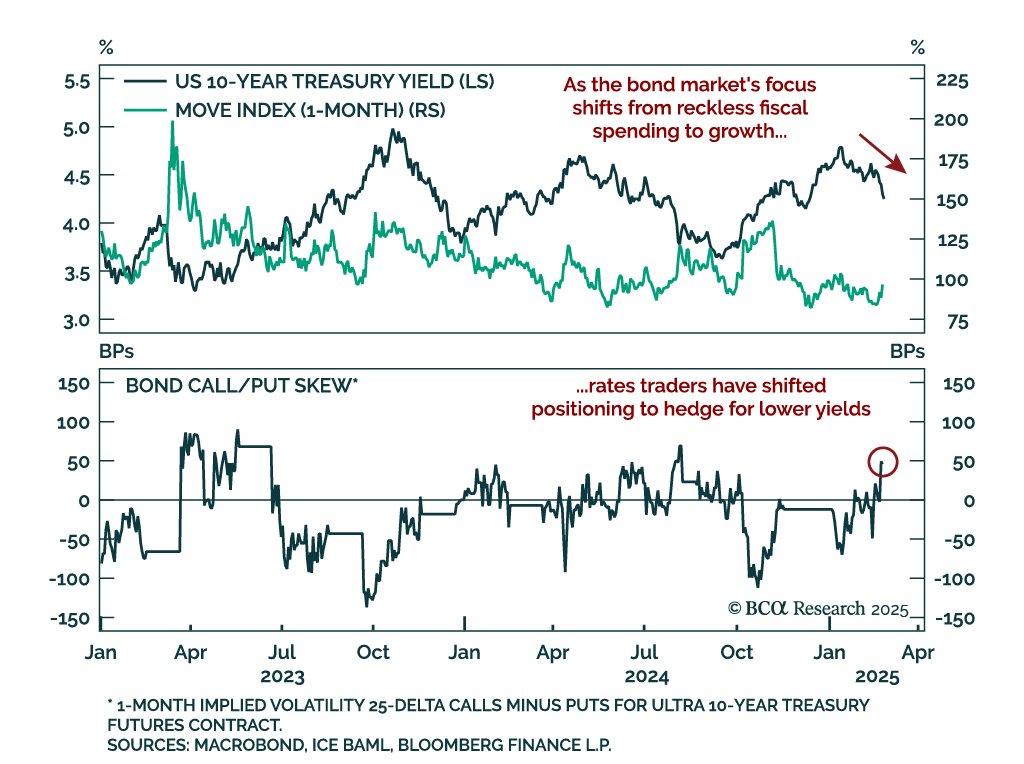

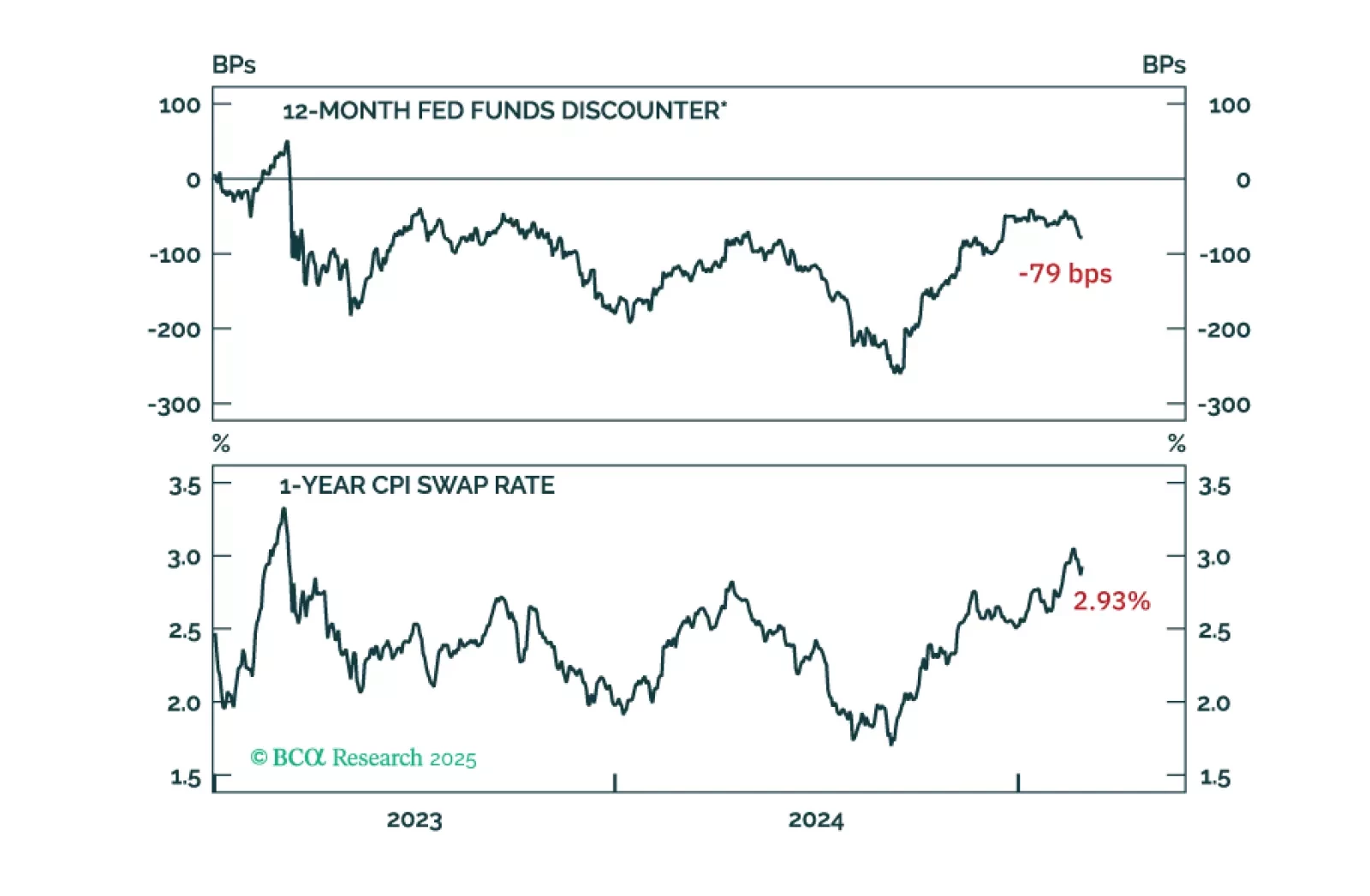

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

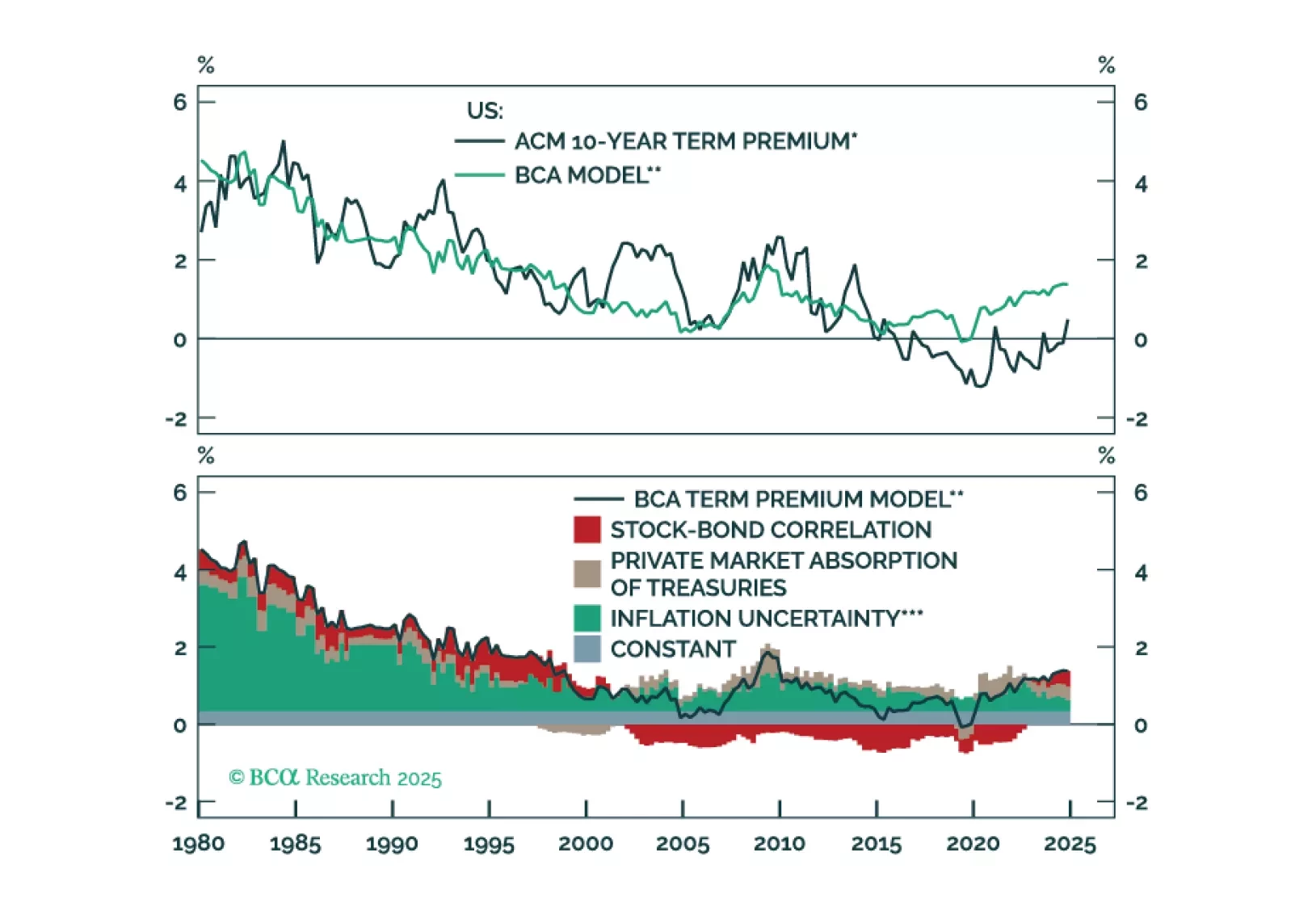

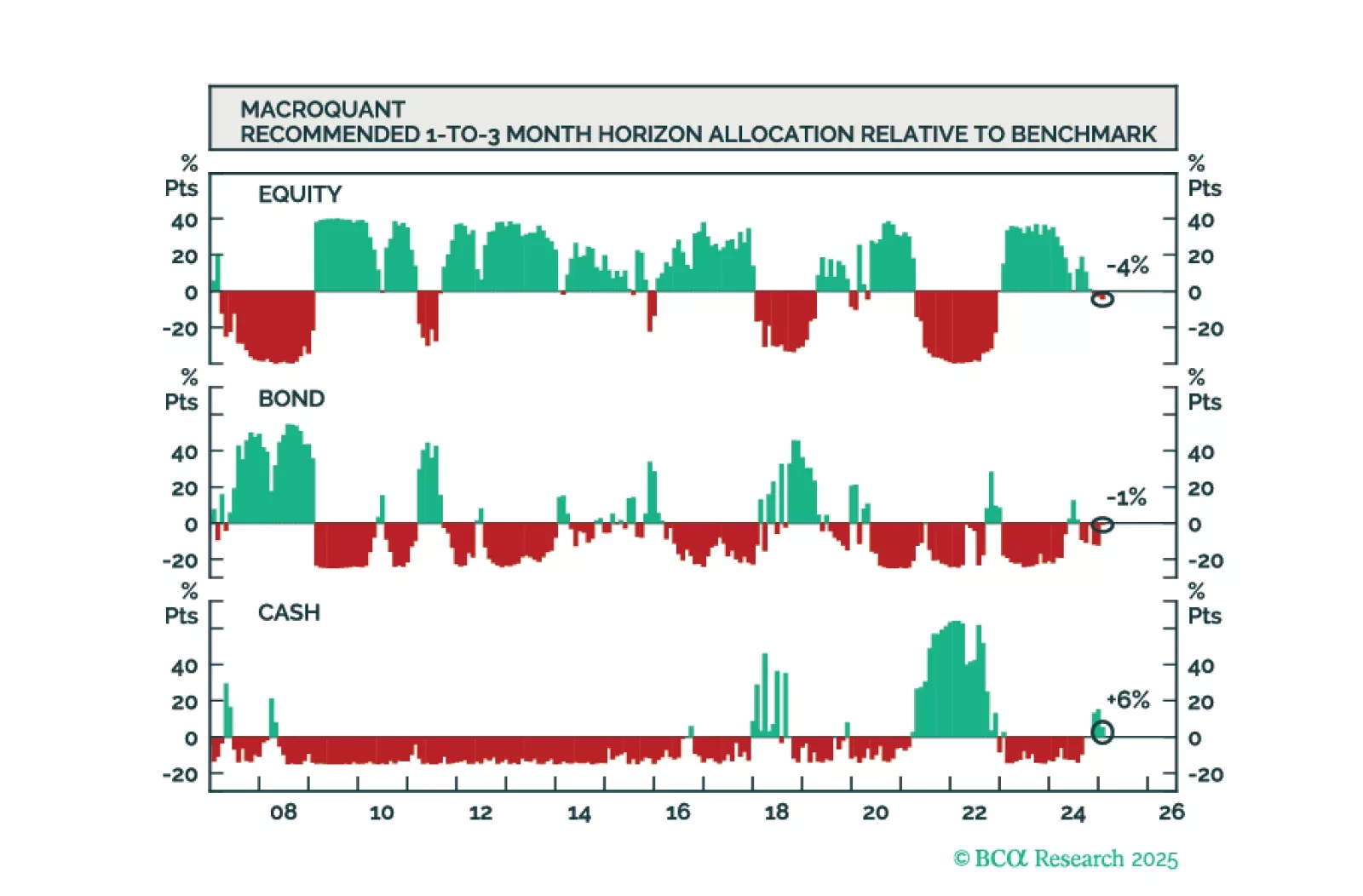

We attempt to model the term premium in this report with inflation uncertainty, the stock-bond correlation, and “Private Treasury Absorption.” Using our model, we estimate the fair value for the US term premium is 89 basis points above the current level. We also find that fiscal concerns are overrated as a term premium driver and instead, the hedging properties of bonds are more important. Over the cyclical horizon, we continue to recommend an above benchmark duration, given our expectations of an economic slowdown. However, if our term premium estimates are correct, US Treasuries still do not have a high enough risk premia to warrant a large structural allocation in a multi-asset portfolio.

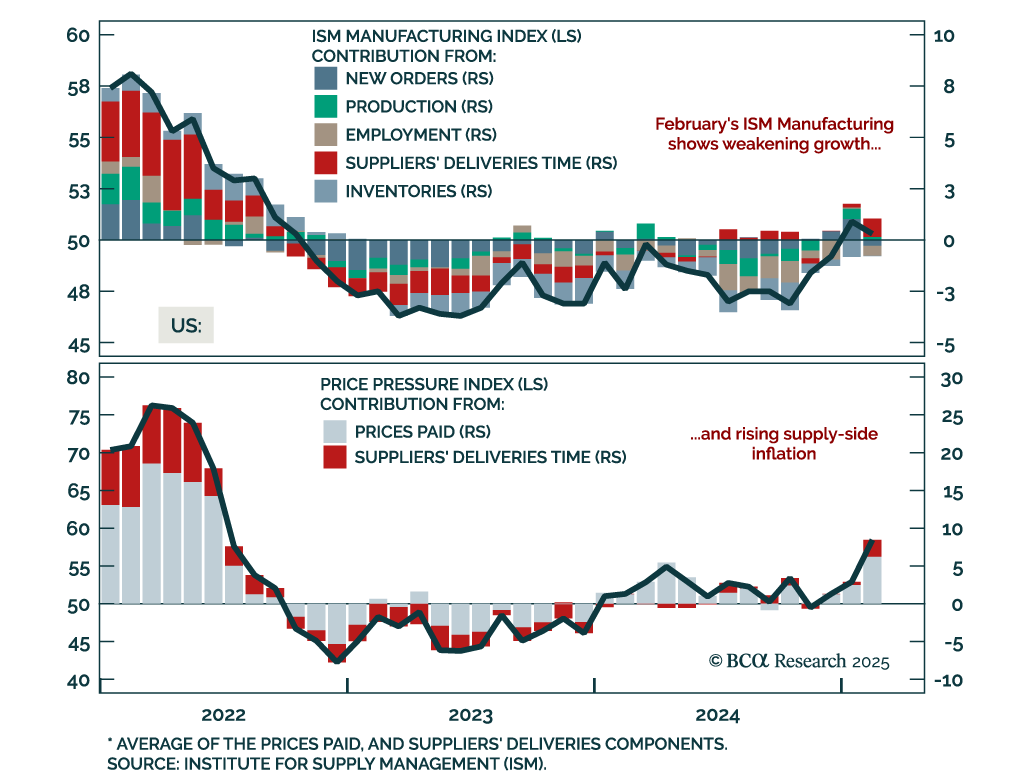

Core PCE inflation was tame this morning, but with large tariffs looming we anticipate loftier inflation readings in the months ahead.