Gold

Executive Summary Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

Macroeconomic Outlook: Global growth will reaccelerate in the second half of this year provided a ceasefire in Ukraine is reached. Inflation will temporarily come down as the dislocations caused by the war and the pandemic subside, before moving up again in late 2023. Equities: Maintain a modest overweight in stocks over a 12-month horizon, favoring non-US equities, small caps, and value stocks. Look to turn more defensive in the second half of 2023 in advance of another wave of inflation. Fixed income: The neutral rate of interest in the US is around 3.5%-to-4%, which is substantially higher than the consensus view. Bond yields will move sideways this year but will rise over the long haul. Overweight Germany, France, Japan, and Australia while underweighting the US and the UK in a global bond portfolio. Credit: Corporate debt will outperform high-quality government bonds over the next 12 months. Favor HY over IG and Europe over the US. Spreads will widen again in late 2023. Currencies: As a countercyclical currency, the US dollar will weaken later this year, with EUR/USD rising to 1.18. We are upgrading our view on the yen from bearish to neutral due to improved valuations. The CNY will strengthen as the Chinese authorities take steps to boost domestic demand. Commodities: Oil prices will dip in the second half of 2022 as the geopolitical premium in crude declines and more OPEC supply comes to market. However, oil and other commodity prices will start moving higher by mid-2023. Bottom Line: The cyclical bull market in stocks that began in 2009 is running long in the tooth, but the combination of faster global growth later this year and a temporary lull in inflation should pave the way for one final hurrah for equities. Dear Client, Instead of our regular report this week, we are sending you our Quarterly Strategy Outlook, where we explore the major trends that are set to drive financial markets in the rest of 2022 and beyond. Next week, please join me for a webcast on Monday, April 11 at 9:00 AM EDT (2:00 PM BST, 3:00 PM CEST, 9:00 PM HKT) where I will discuss the outlook. Best regards, Peter Berezin, Chief Global Strategist P.S. You can now follow me on LinkedIn and Twitter. I. Overview We continue to recommend overweighting global equities over a 12-month horizon. However, we see downside risks to stocks both in the near term (next 3 months) and long term (2-to-5 years). In the near term, stocks will weaken anew if Russia’s stated intentions to scale back operations in Ukraine turn out to be a ruse. There is also a risk that China will need to temporarily shutter large parts of its economy to combat the spread of the highly contagious BA.2 Omicron variant. While stocks could suffer a period of indigestion in response to monetary tightening by the Fed and a number of other central banks, we doubt that rates will rise enough over the next 12 months to undermine the global economy. This reflects our view that the neutral rate of interest in the US and most other countries is higher than widely believed. If the neutral rate ends up being between 3.5% and 4% in the US, as we expect, the odds are low that the Fed will induce a recession by raising rates to 2.75%, as the latest dot plot implies (Chart 1). Chart 1The Market Sees The Fed Raising Rates To Around 3% And Then Backing Off

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The downside of a higher neutral rate is that eventually, investors will need to value stocks using a higher real discount rate. How fast markets mark up their estimate of neutral depends on the trajectory of inflation. We were warning about inflation before it was cool to warn about inflation (see, for example, our January 2021 report, Stagflation in a Few Months?; or our February 2021 report, 1970s-Style Inflation: Yes, It Could Happen Again). Our view has been that inflation will follow a “two steps up, one step down” pattern. We are currently near the top of those two steps: US inflation will temporarily decline in the second half of this year, as goods inflation drops but service inflation is slow to rise. The decline in inflation will provide some breathing room for the Fed, allowing it to raise rates by no more than what markets are already discounting over the next 12 months. Unfortunately, the respite in inflation will not last long. By the end of 2023, inflation will start to pick up again, forcing the Fed to resume hiking rates in 2024. This second round of Fed tightening is not priced by the markets, and so when it happens, it could be quite disruptive for stocks and other risk assets. Investors should overweight equities on a 12-month horizon but look to turn more defensive in the second half of 2023. II. The Global Economy War and Pestilence Are Near-Term Risks BCA’s geopolitical team, led by Matt Gertken, was ringing the alarm bell about Ukraine well before Russia’s invasion. Recent indications from Russia that it will scale back operations in Ukraine could pave the way for a ceasefire; or they could turn out to be a ruse, giving Russia time to restock supply lines and fortify its army in advance of a new summertime campaign against Kyiv. It is too early to tell, but either way, our geopolitical team expects more fighting in the near term. The West is not keen to give Putin an easy off-ramp, and even if it were, it is doubtful he would take it. The only way that Putin can salvage his legacy among his fan base in Russia is to decisively win the war in order to ensure Ukraine’s military neutrality. For his part, Zelensky cannot simply agree to Russia’s pre-war demands that Ukraine demilitarize and swear off joining NATO unless Russian forces first withdraw. To give in to such demands without any concrete security guarantees would raise the question of why Ukraine fought the war to begin with. The Impact of the Ukraine War on the Global Economy The direct effect of the war on the global economy is likely to be small. Together, Russia and Ukraine account for 3.5% of global GDP in PPP terms and 1.9% in dollar terms. Exports to Russia and Ukraine amount to only 0.2% of G7 GDP (Chart 2). Most corporations have little direct exposure to Russia, although there are a few notable exceptions (Chart 3). Chart 2Little Direct Trade Exposure To Russia And Ukraine

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

In contrast to the direct effects, the indirect effects have the potential to be sizable. Russia is the world’s second largest oil producer, accounting for 12% of annual global output (Chart 4). It is the world’s top exporter of natural gas. About half of European natural gas imports come from Russia. Russia is also a significant producer of nickel, copper, aluminum, steel, and palladium. Chart 3Only A Handful Of Firms Have Significant Sales Exposure To Russia

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 4Russia is The World's Second Largest Oil Producer

Russia is The World's Second Largest Oil Producer

Russia is The World's Second Largest Oil Producer

Russia and Ukraine are major agricultural producers. Together, they account for a quarter of global wheat exports, with much of it going to the Middle East and North Africa (Chart 5). They are also significant producers of potatoes, corn, sugar beets, and seed oils. In addition, Russia produces two-thirds of all ammonium nitrate, the main source of nitrogen-based fertilizers. Largely as a result of higher commodity prices and other supply disruptions, the OECD estimates that the war could shave about 1% off of global growth this year, with Europe taking the brunt of the hit (Chart 6). At present, the futures curves for most commodities are highly backwardated (Chart 7). While one cannot look to the futures as unbiased predictors of where spot prices are heading, it is fair to say that commodity markets are discounting some easing in prices over the next two years. If that does not occur, global growth could weaken more than the OECD expects. Chart 5Developing Economies Buy The Bulk Of Russian And Ukrainian Wheat

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 6The War In Ukraine Could Shave One Percentage Point Off Of Global Growth

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 7Futures Curves For Most Commodities Are Backwardated

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Another Covid Wave Two years after “two weeks to flatten the curve,” the world continues to underappreciate the power of exponential growth. Suppose that it takes five days for someone with Covid to infect someone else. If everyone with Covid infects an average of six people, the cumulative number of Covid cases would rise from 1,000 to 10 million in around four weeks. Suppose you could cut the number of new infections in half to three per person. In that case, it would take about six weeks for 10 million people to be infected. In other words, mitigation measures that cut the infection rate by half would only extend how long it takes for 10 million people to be infected by two weeks. That’s not a lot. The point is that any infection rate above one will generate an explosive rise in cases. In the pre-Omicron days, keeping the infection rate below one was difficult, but not impossible for countries with the means and motivation to do so. As the virus has become more contagious, however, keeping it at bay has grown more difficult. The latest strain of Omicron, BA.2, appears to be 40% more contagious than the original Omicron strain, which itself was about 4-times more contagious than Delta. BA.2 is quickly spreading around the world. The number of cases has spiked across much of Europe, parts of Asia, and has begun to rise in North America (Chart 8). In China, the authorities have locked down Shanghai, home to 25 million people. Chart 8Covid Cases Are On The Rise Again

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The success that China has had in suppressing the virus has left its population with little natural immunity; and given the questionable efficacy of its vaccines, with little artificial immunity as well. Moreover, as is the case in Hong Kong, a large share of mainland China’s elderly population remains completely unvaccinated. Chart 9New Covid Drugs Are Set To Hit The Market

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

This presents the Chinese authorities with a difficult dilemma: Impose severe lockdowns over much of the population, or let the virus run rampant. As the logic of exponential change described above suggests, there is not much of a middle ground. Our guess is that the Chinese government will choose the former option. China has already signed a deal to commercialize Pfizer’s Paxlovid. The drug is highly effective at preventing hospitalization if taken within five days from the onset of symptoms. Fortunately, Paxlovid production is starting to ramp up (Chart 9). China will probably wait until it has sufficient supply of the drug before relaxing its zero-Covid policy. While beneficial to growth later this year, this strategy could have a negative near-term impact on activity, as the authorities continue to play whack-a-mole with Covid. Chart 10Inflation Is Running High, Especially In The US

Inflation Is Running High, Especially In The US

Inflation Is Running High, Especially In The US

Central Banks in a Bind Standard economic theory says that central banks should adjust interest rates in response to permanent shocks, while ignoring transitory ones. This is especially true if the shock in question emanates from the supply side of the economy. After all, higher rates cool aggregate demand; they do not raise aggregate supply. The lone exception to this rule is when a supply shock threatens to dislodge long-term inflation expectations. If long-term inflation expectations become unanchored, what began as a transitory shock could morph into a semi-permanent one. The problem for central banks is that the dislocations caused by the Ukraine war are coming at a time when inflation is already running high. Headline CPI inflation reached 7.9% in the US in February, while core CPI inflation clocked in at 6.4%. Trimmed-mean inflation has increased in most economies (Chart 10). Fortunately, while short-term inflation expectations have moved up, long-term expectations have been more stable. Expected US inflation 5-to-10 years out in the University of Michigan survey stood at 3.0% in March, down a notch from 3.1% in January, and broadly in line with the average reading between 2010 and 2015 (Chart 11). Survey-based measures of long-term inflation expectations are even more subdued in the euro area and Japan (Chart 12). Market-based inflation expectations have risen, although this partly reflects higher oil prices. Even then, the widely-watched 5-year, 5-year forward TIPS inflation breakeven rate remains near the bottom of the Fed’s comfort range of 2.3%-to-2.5% (Chart 13).1 Chart 11Long-Term Inflation Expectations Remain Contained In The US...

Long-Term Inflation Expectations Remain Contained In The US...

Long-Term Inflation Expectations Remain Contained In The US...

Chart 12... And In The Euro Area And Japan

... And In The Euro Area And Japan

... And In The Euro Area And Japan

Chart 13The Market's Long-Term Inflation Expectations Are Near The Bottom Of The Fed's Comfort Zone

The Market's Long-Term Inflation Expectations Are Near The Bottom Of The Fed's Comfort Zone

The Market's Long-Term Inflation Expectations Are Near The Bottom Of The Fed's Comfort Zone

Goods versus Services Inflation Most of the increase in consumer prices has been concentrated in goods rather than services (Chart 14). This is rather unusual in that goods prices usually fall over time; but in the context of the pandemic, it is entirely understandable. Chart 14Goods Prices Have Been A Major Driver Of Overall Inflation

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The pandemic caused spending to shift from services to goods (Chart 15). This occurred at the same time as the supply of goods was being adversely affected by various pandemic-disruptions, most notably the semiconductor shortage that is still curtailing automobile production. Chart 15AGoods Inflation Should Fade As Consumption Shifts Back Towards Services (I)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (I)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (I)

Chart 15BGoods Inflation Should Fade As Consumption Shifts Back Towards Services (II)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (II)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (II)

Looking out, the composition of consumer spending will shift back towards services. Supply chain bottlenecks should also abate, especially if the situation in Ukraine stabilizes. It is worth noting that the number of ships on anchor off the coast of Los Angeles and Long Beach has already fallen by half (Chart 16). The supplier delivery components of both the manufacturing and nonmanufacturing ISM indices have also come off their highs (Chart 17). Even used car prices appear to have finally peaked (Chart 18). Chart 16Shipping Delays Are Abating

Shipping Delays Are Abating

Shipping Delays Are Abating

Chart 17Delivery Times Are Slowly Coming Down

Delivery Times Are Slowly Coming Down

Delivery Times Are Slowly Coming Down

Chart 18Used Car Prices May Have Finally Peaked

Used Car Prices May Have Finally Peaked

Used Car Prices May Have Finally Peaked

On the Lookout for a Wage-Price Spiral Could rising services inflation offset any decline in goods inflation this year? It is possible, but for that to happen, wage growth would have to accelerate further. For now, much of the acceleration in US wage growth has occurred at the bottom end of the income distribution (Chart 19). It is easy to see why. Chart 20 shows that low-paid workers have not returned to the labor market to the same degree as higher-paid workers. However, now that extended unemployment benefits have lapsed and savings deposits are being drawn down, the incentive to resume work will strengthen. Chart 19Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Chart 20More Low-Wage Employees Should Return To Work

More Low-Wage Employees Should Return To Work

More Low-Wage Employees Should Return To Work

Chart 21More Workers Will Return To Their Jobs Once The Pandemic Ends

More Workers Will Return To Their Jobs Once The Pandemic Ends

More Workers Will Return To Their Jobs Once The Pandemic Ends

The end of the pandemic should allow more workers to remain at their jobs. In January, during the height of the Omicron wave, 8.75 million US workers (5% of the total workforce) were absent from work due to the virus (Chart 21). How High Will Interest Rates Eventually Rise? If goods inflation comes down swiftly later this year, and services inflation is slow to rise, then overall inflation will decline. This should allow the Fed to pause tightening in early 2023. Whether the Fed will remain on hold beyond then depends on where the neutral rate of interest resides. Chart 22The Yield Curve Inverted in Mid-2019 But Growth Accelerated

The Yield Curve Inverted in Mid-2019 But Growth Accelerated

The Yield Curve Inverted in Mid-2019 But Growth Accelerated

The neutral rate, or equilibrium rate as it is sometimes called, is the interest rate consistent with full employment and stable inflation. If the Fed pauses hiking before interest rates have reached neutral, the economy will eventually overheat, forcing the Fed to resume hiking. In contrast, if the Fed inadvertently raises rates above neutral, unemployment will start rising, requiring the Fed to cut rates. Markets are clearly worried about the latter scenario. The 2/10 yield curve inverted earlier this week. With the term premium much lower than in the past, an inversion in the yield curve is not the powerful harbinger of recession that it once was. After all, the 2/10 curve inverted in August 2019 and the economy actually strengthened over the subsequent six months before the pandemic came along (Chart 22). Nevertheless, an inverted yield curve is consistent with markets expectations that the Fed will raise rates above neutral. That is always a dangerous undertaking. Raising rates above neutral would likely push up the unemployment rate. There has never been a case in the post-war era where the 3-month moving average of the unemployment rate has risen by more than 30 basis points without a recession occurring (Chart 23). Chart 23When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

As discussed in the Feature Section below, the neutral rate of interest is probably between 3.5% and 4% in the US. This is good news in the short term because it lowers the odds that the Fed will raise rates above neutral during the next 12 months. It is bad news in the long run because it means that the Fed will find itself even more behind the curve than it is now, making a recession almost inevitable. The Feature Section builds on our report from two weeks ago. Readers familiar with that report should feel free to skip ahead to the next section. III. Feature: A Higher Neutral Rate Conceptually, the neutral rate is the interest rate that equates the amount of investment a country wants to undertake at full employment with the amount of savings that it has at its disposal.2 Anything that reduces savings or increases investment would raise the neutral rate (Chart 24). Chart 24The Savings-Investment Balance Determines The Neutral Rate Of Interest

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

A number of factors are likely to lower desired savings in the US over the next few years: Households will spend down their accumulated pandemic savings. US households are sitting on $2.3 trillion (10% of GDP) in excess savings, the result of both decreased spending on services during the pandemic and the receipt of generous government transfer payments (Chart 25). Household wealth has soared since the start of the pandemic (Chart 26). Conservatively assuming that households spend three cents of every additional dollar in wealth, the resulting wealth effect could boost consumption by 4% of GDP. Chart 25Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

Chart 26Net Worth Has Soared Since The Pandemic

Net Worth Has Soared Since The Pandemic

Net Worth Has Soared Since The Pandemic

The household deleveraging cycle has ended (Chart 27). Household balance sheets are in good shape. After falling during the initial stages of the pandemic, consumer credit has begun to rebound. For the first time since the housing boom, mortgage equity withdrawals are rising. Banks are easing lending standards on consumer loans across the board. Chart 27US Household Deleveraging Pressures Have Abated

US Household Deleveraging Pressures Have Abated

US Household Deleveraging Pressures Have Abated

Chart 28Baby Boomers Have Amassed A Lot Of Wealth

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Baby boomers are retiring. They hold over half of US household wealth, considerably more than younger generations (Chart 28). As baby boomers transition from being savers to dissavers, national savings will decline. Government budget deficits will stay elevated. Fiscal deficits subtract from national savings. While the US budget deficit will come down over the next few years, the IMF estimates that the structural budget deficit will still average 4.9% of GDP between 2022 and 2026 compared to 2.0% of GDP between 2014 and 2019 (Chart 29).Chart 29Fiscal Policy: Tighter But Not Tight

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

On the investment front: The deceleration in trend GDP growth, which depressed investment spending, has largely run its course.3 According to the Congressional Budget Office, real potential GDP growth fell from over 3% in the early 1980s to about 1.9% today. The CBO expects potential growth to edge down only slightly to 1.7% over the next few decades (Chart 30). After moving broadly sideways for two decades, core capital goods orders – a leading indicator for capital spending – have broken out to the upside (Chart 31). Capex intention surveys remain upbeat (Chart 32). The average age of the nonresidential capital stock currently stands at 16.3 years, the highest since 1965 (Chart 33). Chart 30Much Of The Deceleration In Potential Growth Has Already Happened

Much Of The Deceleration In Potential Growth Has Already Happened

Much Of The Deceleration In Potential Growth Has Already Happened

Chart 31Positive Signs For Capex (I)

Positive Signs For Capex (I)

Positive Signs For Capex (I)

Chart 32Positive Signs For Capex (II)

Positive Signs For Capex (II)

Positive Signs For Capex (II)

Chart 33An Aging Capital Stock

An Aging Capital Stock

An Aging Capital Stock

Similar to nonresidential investment, the US has been underinvesting in residential real estate (Chart 34). The average age of the housing stock has risen to a 71-year high of 31 years. The homeowner vacancy rate has plunged to the lowest level on record. The number of newly finished homes for sale is half of what it was prior to the pandemic. Chart 34US Housing Is In Short Supply

US Housing Is In Short Supply

US Housing Is In Short Supply

The New ESG: Energy Security and Guns The war in Ukraine will put further upward pressure on the neutral rate, especially outside of the United States. After staging a plodding recovery following the euro debt crisis, European capital spending received a sizable boost from the launch of the NextGenerationEU Recovery Fund (Chart 35). As Mathieu Savary points out in his latest must-read report on Europe, capital spending will rise further in the years ahead as European governments accelerate efforts to make their economies less reliant on Russian energy. Germany has already announced plans to construct three new LNG terminals. The push to build out Europe’s energy infrastructure is coming at a time when businesses are looking to ramp up capital spending. As in the US, Europe’s capital stock has aged rapidly over the past decade (Chart 36). Chart 35European Capex Should Recover

European Capex Should Recover

European Capex Should Recover

Chart 36European Machines Need More Than Just An Oil Change

European Machines Need More Than Just An Oil Change

European Machines Need More Than Just An Oil Change

Chart 37The War In Ukraine Calls For More Spending Across Europe

The War In Ukraine Calls For More Spending Across Europe

The War In Ukraine Calls For More Spending Across Europe

Meanwhile, European governments are trying to ease the burden from rising energy costs. For example, France has introduced a rebate on fuel. It is part of a EUR 20 billion package aimed at cutting heating and electricity bills. European military spending will rise. Military spending currently amounts to 1.5% of GDP, well below NATO’s threshold of 2% (Chart 37). Germany has announced that it will spend EUR 100 billion more on defense. European governments will also need to boost spending to accommodate Ukrainian refugees. The UN estimates that four million refugees have left Ukraine, with the vast majority settling in the EU. A Smaller Chinese Current Account Surplus? The difference between what a country saves and invests equals its current account balance. Historically, China has been a major exporter of savings, which has helped depress interest rates abroad. While China’s current account surplus has declined as a share of its own GDP, it has remained very large as a share of global ex-China GDP, reflecting China’s growing weight in the global economy (Chart 38). Many analysts assume that China will double down on efforts to boost exports in order to offset the drag from falling property investment. However, there is a major geopolitical snag with that thesis: A country that runs a current account surplus must, by definition, accumulate assets from the rest of the world. As the freezing of Russia’s foreign exchange reserves demonstrates, that is a risky proposition for a country such as China. Rather than increasing its current account surplus, China may seek to bolster its economy by raising domestic demand. This could be achieved by either boosting domestic infrastructure spending or raising household consumption. Notably, China’s credit impulse appears to have bottomed and is set to increase in the second half of the year. This is good news not just for Chinese growth but growth abroad (Chart 39). Chart 38Will China Be A Source Of Excess Savings?

Will China Be A Source Of Excess Savings?

Will China Be A Source Of Excess Savings?

Chart 39China's Credit Impulse Appears To Have Bottomed

China's Credit Impulse Appears To Have Bottomed

China's Credit Impulse Appears To Have Bottomed

The IMF’s latest projections foresee China’s current account surplus falling by more than half between 2021 and 2026 as a share of global ex-China GDP. If this were to happen, the neutral rate in China and elsewhere would rise. IV. Financial Markets A. Portfolio Strategy Chart 40The Markets Wobbled And Then Recovered After The Beginning Of The Last Four Fed Rate Cycles

The Markets Wobbled And Then Recovered After The Beginning Of The Last Four Fed Rate Cycles

The Markets Wobbled And Then Recovered After The Beginning Of The Last Four Fed Rate Cycles

As noted in the overview, if the neutral rate turns out to be higher than currently perceived, the Fed is unlikely to induce a recession by raising rates over the next 12 months. That is good news for equities. A look back at the past four Fed tightening cycles shows that stocks often wobble when the Fed starts hiking rates, but then usually rise as long as rates do not move into restrictive territory (Chart 40). Unfortunately, a higher neutral rate also means that investors will eventually need to value stocks using a higher discount rate. It also means that any decline in inflation this year will not last. The US economy will probably start to overheat again in the second half of 2023. This will set the stage for a second, and more painful, tightening cycle in 2024. Admittedly, there is a lot of uncertainty over our “two steps up, one step down” forecast for inflation. It is certainly possible that the “one step down” phase does not last long and that the resurgence in inflation we are expecting in the second half of next year occurs earlier. It is also possible that investors will react negatively to rising rates, even if the economy is ultimately able to withstand them. As such, only a modest overweight to equities is justified over the next 12 months, with risks tilted to the downside in the near term. More conservative asset allocators should consider moving to a neutral stance on equities already, as my colleague Garry Evans advised clients to do in his latest Global Asset Allocation Quarterly Portfolio Outlook. B. Fixed Income Stay Underweight Duration Over a 2-to-5 Year Horizon Our recommendation to maintain below-benchmark duration in fixed-income portfolios panned out since the publication of our Annual Outlook in December, with the US 10-year Treasury yield rising from 1.43% to 2.38%. We continue to expect bond yields in the US to rise over the long haul. Conceptually, the yield on a government bond equals the expected path of policy rates over the duration of the bond plus a term premium. The term premium is the difference between the return investors can expect from buying a long-term bond that pays a fixed interest rate, and the return from rolling over a short-term bill. The term premium has been negative in recent years. Investors have been willing to sacrifice return to own long-term bonds because bond prices usually rise when the odds of a recession go up. The fact that monthly stock returns and changes in bond yields have been positively correlated since 2001 underscores the benefits that investors have received from owning long-term bonds as a hedge against unfavorable economic news (Chart 41). However, now that inflation has emerged as an increasingly important macroeconomic risk, the correlation between stock returns and changes in bond yields could turn negative again. Unlike weak economic growth, which is bad for only stocks, high inflation is bad for both bonds and stocks. Chart 41Correlation Between Stock Returns And Bond Yields Could Turn Negative

Correlation Between Stock Returns And Bond Yields Could Turn Negative

Correlation Between Stock Returns And Bond Yields Could Turn Negative

If bond yields start to rise whenever stock prices fall, the incentive to own long-term bonds will decline. This will cause the term premium to increase. Assuming the term premium rises to about 0.5%, and a neutral rate of 3.5%-to-4%, the long-term fair value for the 10-year US Treasury yield is 4%-to-4.5%. This is well above the 5-year/5-year forward yield of 2.20%. Move from Underweight to Neutral Duration Over a 12-Month Horizon Below benchmark duration positions usually do well when the Fed hikes rates by more than expected over the subsequent 12 months (Chart 42). Chart 42The Golden Rule Of Bond Investing

The Golden Rule Of Bond Investing

The Golden Rule Of Bond Investing

Given our view that US inflation will temporarily decline later this year, the Fed will probably not need to raise rates over the next 12 months by more than the 249 basis points that markets are already discounting. Thus, while a below-benchmark duration position is advisable over a 2-to-5-year time frame, it could struggle over a horizon of less than 12 months. Our end-2022 target range for the US 10-year Treasury yield is 2.25%-to-2.5%. Chart 43Bond Sentiment And Positioning Are Bearish

Bond Sentiment And Positioning Are Bearish

Bond Sentiment And Positioning Are Bearish

Supporting our decision to move to a neutral benchmark duration stance over a 12-month horizon is that investor positioning and sentiment are both bond bearish (Chart 43). From a contrarian point of view, this is supportive of bonds. Global Bond Allocation BCA’s global fixed-income strategists recommend overweighting German, French, Australian, and Japanese government bonds, while underweighting those of the US and the UK. They are neutral on Italy and Spain given that the ECB is set to slow the pace of bond buying. The neutral rate of interest has risen in the euro area, partly on the back of more expansionary fiscal policy across the region. In absolute terms, however, the neutral rate in the euro area is still quite low, and possibly negative. Unlike in the US, where inflation has risen to uncomfortably high levels, much of Europe would benefit from higher inflation expectations, as this would depress real rates across the region, giving growth a boost. This implies that the ECB is unlikely to raise rates much over the next two years. As with the euro area, Japan would benefit from lower real rates. The Bank of Japan’s yield curve control policy has been put to the test in recent weeks. To its credit, the BoJ has stuck to its guns, buying bonds in unlimited quantities to prevent yields from rising. We expect the BoJ to stay the course. Unlike in the euro area and Japan, inflation expectations are quite elevated in the UK and wage growth is rising quickly there. This justifies an underweight stance on UK gilts. Although job vacancies in Australia have climbed to record levels, wage growth is still not strong enough from the RBA’s point of view to justify rapid rate hikes. As a result, BCA’s global fixed-income strategists remain overweight Australian bonds. Finally, our fixed-income strategists are underweight Canadian bonds but are contemplating upgrading them given that markets have already priced in 238 basis points in tightening over the next 12 months. Unlike in the US, high levels of consumer debt will also limit the Bank of Canada’s ability to raise rates. Modest Upside in High-Yield Corporate Bonds Credit spreads have narrowed in recent days but remain above where they were prior to Russia’s invasion of Ukraine. Since the start of the year, US investment-grade bonds have underperformed duration-matched Treasurys by 154 basis points, while high-yield bonds have underperformed by 96 basis points (Chart 44). The outperformance of high-yield relative to investment-grade debt can be explained by the fact that the former has more exposure to the energy sector, which has benefited from rising oil prices. Looking out, falling inflation and a rebound in global growth later this year should provide a modestly supportive backdrop for corporate credit. High-yield spreads are still pricing in a default rate of 3.8% over the next 12 months (Chart 45). This is well above the trailing 12-month default rate of 1.3%. Our fixed-income strategists continue to prefer US high-yield over US investment-grade. Chart 44Spreads Have Narrowed Over The Past Two Weeks But Remain Above Pre-War Levels

Spreads Have Narrowed Over The Past Two Weeks But Remain Above Pre-War Levels

Spreads Have Narrowed Over The Past Two Weeks But Remain Above Pre-War Levels

Chart 45Spread-Implied Default Rate Is Too High

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

European credit is attractively priced and should benefit from any stabilization in the situation in Ukraine. Our fixed-income strategists prefer both European high-yield and investment-grade bonds over their US counterparts. As with equities, the bull market in corporate credit will end in late 2023 as the Fed is forced to resume raising rates in 2024 in the face of an overheated economy. C. Currencies Chart 46Widening Interest Rate Differentials Have Supported The Dollar

Widening Interest Rate Differentials Have Supported The Dollar

Widening Interest Rate Differentials Have Supported The Dollar

The US Dollar Will Weaken Starting in the Second Half of 2022 Since bottoming last May, the US dollar has been trending higher. While the dollar could strengthen further in the near term if the war in Ukraine escalates, the fundamental backdrop supporting the greenback is starting to fray. If US inflation comes down later this year, the Fed is unlikely to raise rates by more than what markets are already discounting over the next 12 months. Thus, widening rate differentials will no longer support the dollar (Chart 46). The dollar is a countercyclical currency: It usually weakens when global growth is strengthening and strengthens when global growth is weakening (Chart 47). The dollar tends to be particularly vulnerable when growth expectations are rising more outside the US than in the US (Chart 48). Chart 47The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 48Better Growth Prospects Abroad Will Weigh On The US Dollar

Better Growth Prospects Abroad Will Weigh On The US Dollar

Better Growth Prospects Abroad Will Weigh On The US Dollar

Global growth should rebound in the second half of the year once the pandemic finally ends and the situation in Ukraine stabilizes. Growth is especially likely to recover in Europe. This will support the euro, a dovish ECB notwithstanding. Chester Ntonifor, BCA’s Foreign Exchange Strategist, expects EUR/USD to end the year at 1.18. The Dollar is Overvalued The dollar’s ascent has left it overvalued by more than 20% on a Purchasing Power Parity (PPP) basis (Chart 49). The PPP exchange rate equalizes the price of a representative basket of goods and services between the US and other economies. PPP deviations from fair value have done a reasonably good job of predicting dollar movements over the long run (Chart 50). Chart 49USD Remains Overvalued

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 50Valuations Matter For FX Long-Term Returns

Valuations Matter For FX Long-Term Returns

Valuations Matter For FX Long-Term Returns

Reflecting the dollar’s overvaluation, the US trade deficit has widened sharply (Chart 51). Excluding energy exports, the US trade deficit as a share of GDP is now the largest on record. Equity inflows have helped finance America’s burgeoning current account deficit (Chart 52). However, these inflows have ebbed significantly as foreign investors have lost their infatuation with US tech stocks. Chart 51The US Trade Deficit Has Widened

The US Trade Deficit Has Widened

The US Trade Deficit Has Widened

Chart 52Net Inflows Into US Equities Have Dried Up

Net Inflows Into US Equities Have Dried Up

Net Inflows Into US Equities Have Dried Up

Dollar positioning remains stretched on the long side (Chart 53). That is not necessarily an obstacle in the short run, given that the dollar tends to be a momentum currency, but it does suggest that the greenback could weaken over a 12-month horizon as more dollar bulls jump ship. The Yen: Cheaper but Few Catalysts for a Bounce The trade-weighted yen has depreciated by 6.4% since the start of the year. The yen is 31% undervalued relative to the dollar on a PPP basis (Chart 54). In a nod to these improved valuations, we are upgrading our 12-month and long-term view on the yen from bearish to neutral. Chart 53Still A Lot of Dollar Bulls

Still A Lot of Dollar Bulls

Still A Lot of Dollar Bulls

Chart 54The Yen Has Gotten Cheaper

The Yen Has Gotten Cheaper

The Yen Has Gotten Cheaper

While the yen is unlikely to weaken much from current levels, it is unlikely to strengthen. As noted above, the Bank of Japan has no incentive to abandon its yield curve control strategy. Yes, the recent rapid decline in the yen is a shock to the economy, but it is a “good” shock in the sense that it could finally jolt inflation expectations towards the BoJ’s target of 2%. If inflation expectations rise, real rates would fall, which would be bearish for the currency. Favor the RMB and other EM Currencies The Chinese RMB has been resilient so far this year, rising slightly against the dollar, even as the greenback has rallied against most other currencies. Real rates are much higher in China than in the US, and this has supported the RMB (Chart 55). Chart 55Higher Real Rates In China Have Supported The RMB

Higher Real Rates In China Have Supported The RMB

Higher Real Rates In China Have Supported The RMB

Chart 56The RMB Is Undervalued Based On PPP

The RMB Is Undervalued Based On PPP

The RMB Is Undervalued Based On PPP

Despite the RMB’s strength, it is still undervalued by 10.5% relative to its PPP exchange rate (Chart 56). While productivity growth has slowed in China, it remains higher than in most other countries. The real exchange rates of countries that benefit from fast productivity growth typically appreciates over time. China holds about half of its foreign exchange reserves in US dollars, a number that has not changed much since 2012 (Chart 57). We expect China to diversify away from dollars over the coming years. Moreover, as discussed earlier in the report, the incentive for China to run large current account surpluses may fade, which will result in slower reserve accumulation. Both factors could curb the demand for dollars in international markets. Chart 57Half Of Chinese FX Reserves Are Held In USD Assets

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

A resilient RMB will provide a tailwind for other EM currencies. Many EM central banks began to raise rates well before their developed market counterparts. In Brazil, for example, the policy rate has risen to 11.75% from 2% last April. With inflation in EMs likely to come down later this year as pandemic and war-related dislocations subside, real policy rates will rise, giving EM currencies a boost. D. Commodities Longer-Term Bullish Thesis on Commodities Remains Intact BCA’s commodity team, led by Bob Ryan, expects crude prices to fall in the second half of the year, before moving higher again in 2023. Their forecast is for Brent to dip to $88/bbl by end-2022, which is below the current futures price of $97/bbl. Chart 58Dearth Of Oil Capex Will Put A Floor Under Oil Prices

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

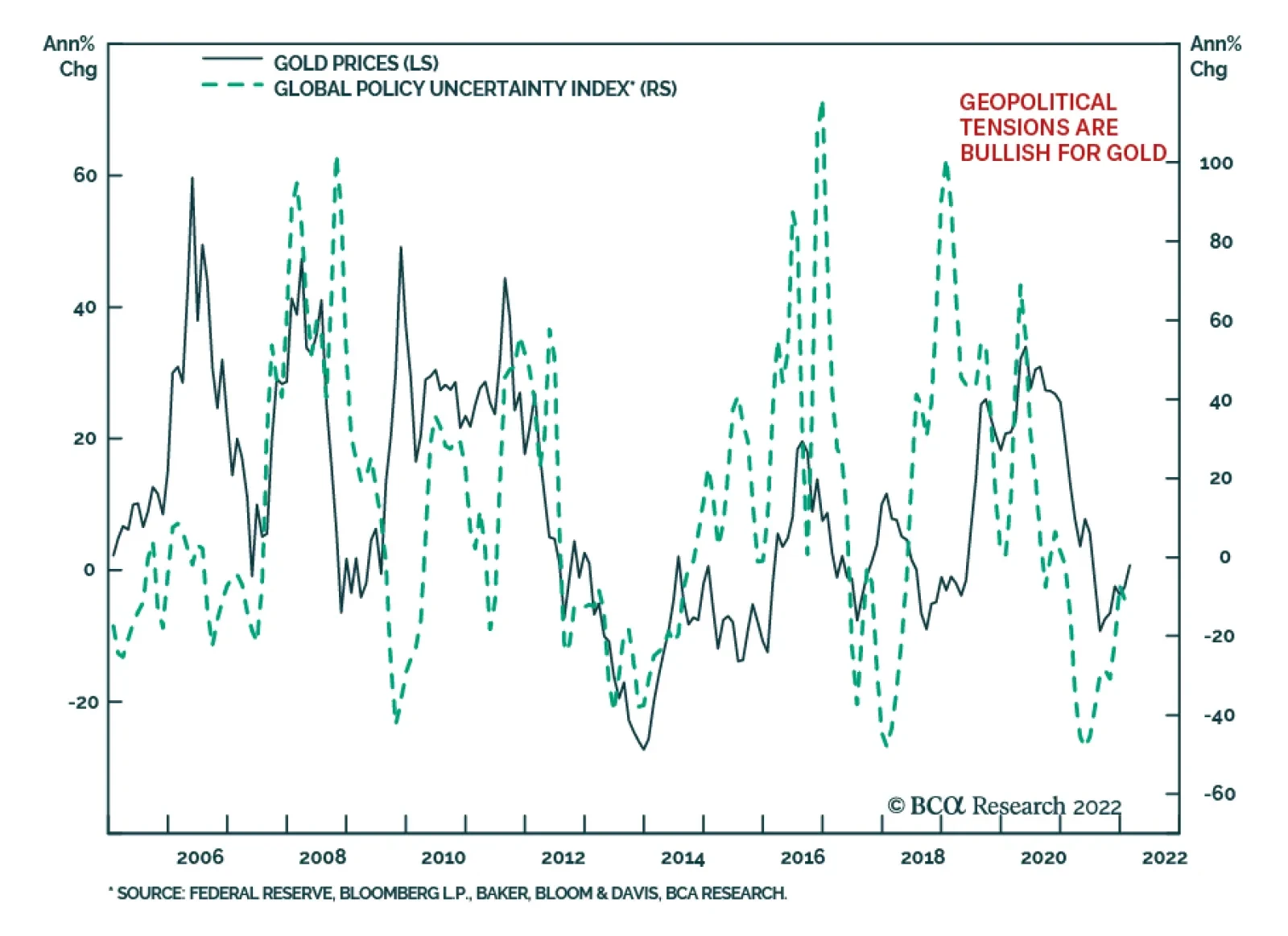

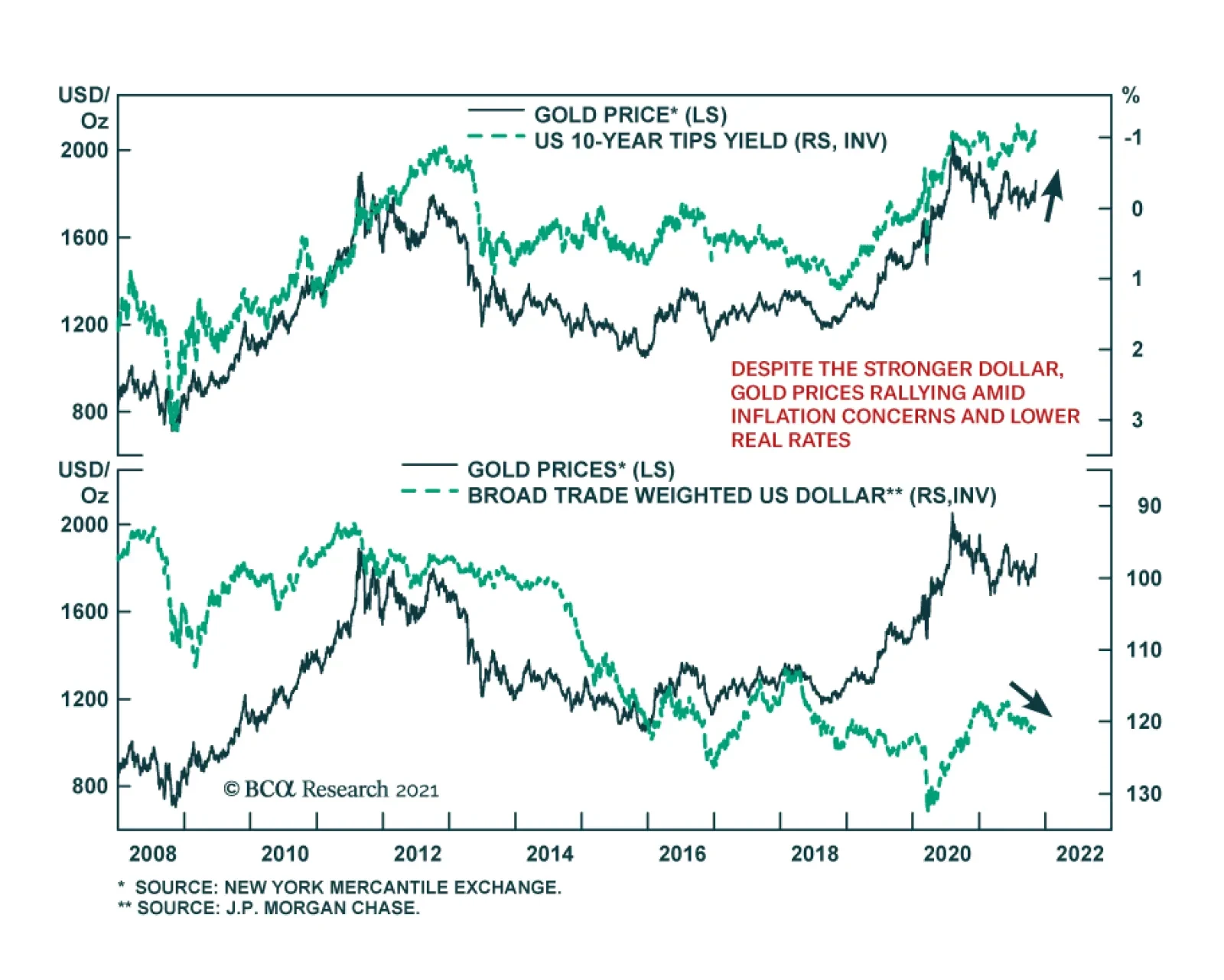

The risk to their end-2022 forecast is tilted to the upside. The relationship between the Saudis and the US has become increasingly strained. This could hamper efforts to bring more oil to market. Hopes that Iranian crude will reach global markets could also be dashed if, as BCA’s geopolitical strategists expect, the US-Iran nuclear deal falls through. A cut-off of Russian oil could also cause prices to rise. While Urals crude is being sold at a heavy discount of $30/bbl to Brent (compared to a discount of around $2/bbl prior to the invasion), it is still leaving the country. In fact, Russian oil production actually rose in March over February. An escalation of the war would make it more difficult for Russia to divert enough oil to China, India, and other countries in order to evade Western sanctions. Looking beyond this year, Bob and his team see upside to oil prices. They expect Brent to finish 2023 at $96/bbl, above the futures price of $89/bbl. Years of underinvestment in crude oil production have led to tight supply conditions (Chart 58). Proven global oil reserves increased by only 6% between 2010 and 2020, having risen by 26% over the preceding decade. Stay Positive on Metals As with oil, there has been little investment in mining capacity in recent years. While a weaker property market in China will weigh on metals prices, this will be partly offset by increased infrastructure spending. The shift towards green energy will also boost metals prices. The typical electric vehicle requires about four times as much copper as a typical gasoline-powered vehicle. Huge amounts of copper will also be necessary to expand electrical grids. Favor Gold Over Cryptos After breaking above $2,000/oz, the price of gold has retreated to $1,926/oz. In the near term, gold prices will be swayed by geopolitical developments. Longer term, real rates will dictate the direction of gold prices. Chart 59 shows that there is a very strong correlation between the price of gold and TIPS yields. If we are correct that the neutral rate of interest is 3.5%-to-4% in the US, real bond yields will eventually need to rise from current levels. Gold prices are quite expensive by historic standards, which represents a long-term risk (Chart 60). Chart 59Strong Correlation Between Real Rates And Gold

Strong Correlation Between Real Rates And Gold

Strong Correlation Between Real Rates And Gold

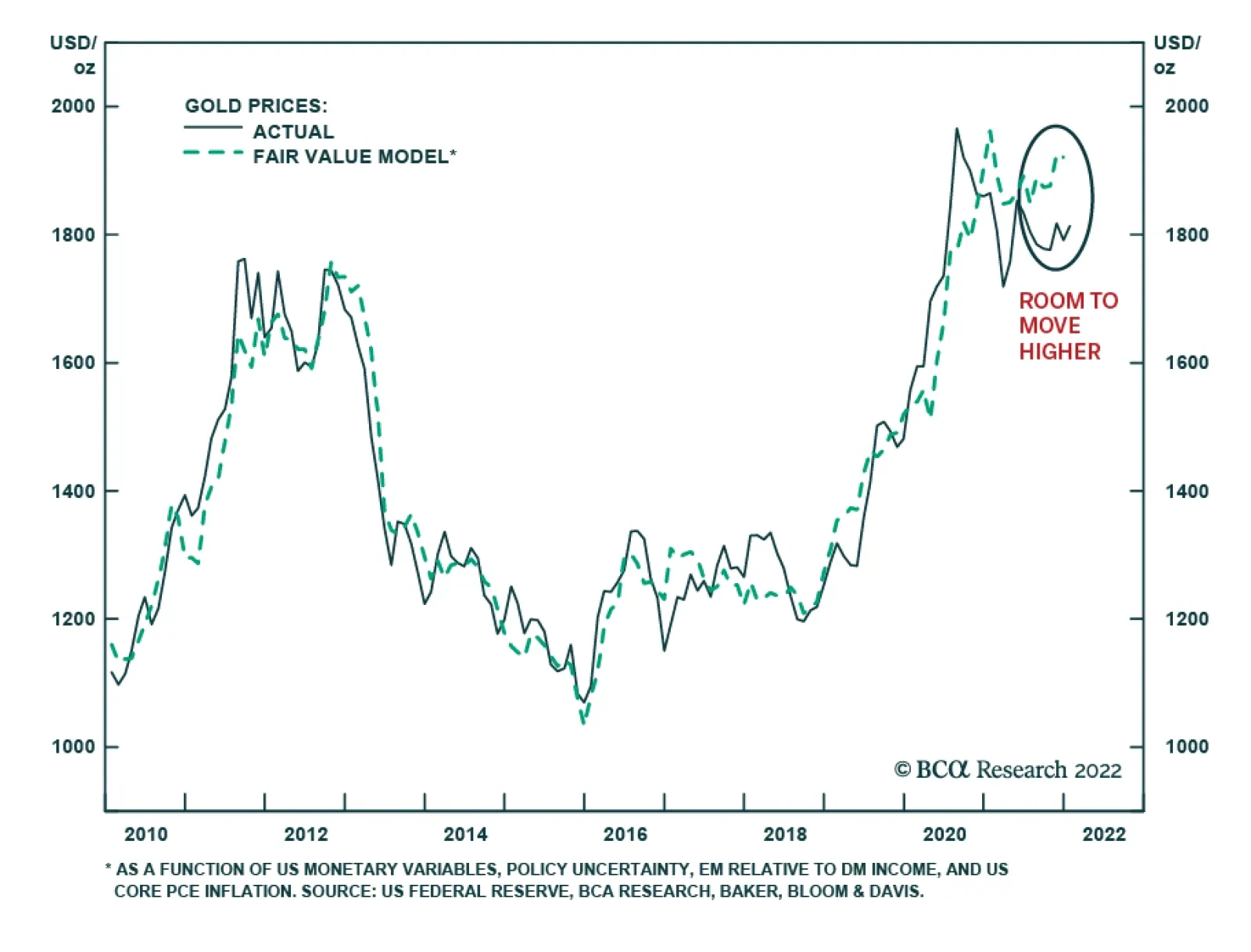

Chart 60Gold Is Quite Pricey From A Historical Perspective

Gold Is Quite Pricey From A Historical Perspective

Gold Is Quite Pricey From A Historical Perspective

That said, we expect the bulk of the increase in real bond yields to occur only after mid-2023. As mentioned earlier, the Fed will probably not have to deliver more tightening that what markets are already discounting over the next 12 months. Thus, gold prices are unlikely to fall much in the near term. In any case, we continue to regard gold as a safer play than cryptocurrencies. As we discussed in Who Pays for Cryptos?, the long-term outlook for cryptocurrencies remains daunting. Many of the most hyped blockchain applications, from DeFi to NFTs, will turn out to be duds. Concerns that cryptocurrencies are harming the environment, contributing to crime, and enriching a small group of early investors at the expense of everyone else will lead to increased regulatory scrutiny. Our long-term target for Bitcoin is $5,000. E. Equities Equities Are Still Attractively Priced Relative to Bonds Corporate earnings are highly correlated with the state of the business cycle (Chart 61). A recovery in global growth later this year will bolster revenue, while easing supply-chain pressures should help contain costs in the face of rising wages. It is worth noting that despite all the shocks to the global economy, EPS estimates in the US and abroad have actually risen this year (Chart 62). Chart 61The Business Cycle Drives Earnings

The Business Cycle Drives Earnings

The Business Cycle Drives Earnings

Chart 62Global EPS Estimates Have Held Up Reasonably Well

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 63Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

As Doug Peta, BCA’s Chief US Strategist has pointed out, the bar for positive earnings surprises for Q1 is quite low: According to Refinitiv/IBES, S&P 500 earnings are expected to fall by 4.5% in Q1 over Q4 levels. Global equities currently trade at 18-times forward earnings. Relative to real bond yields, stocks continue to look reasonably cheap (Chart 63). Even in the US, where valuations are more stretched, the earnings yield on stocks exceeds the real bond yield by 570 basis points. At the peak of the market in 2000, the gap between earnings yields and real bond yields was close to zero. Favor Non-US Markets, Small Caps, and Value Valuations are especially attractive outside the US. Non-US equities trade at 13.7-times forward earnings. Emerging markets trade at a forward P/E of only 12.1. Correspondingly, the gap between earnings yields and real bond yields is about 200 basis points higher outside the US. In general, non-US markets fare best in a setting of accelerating growth and a weakening dollar – precisely the sort of environment we expect to prevail in the second half of the year (Chart 64). US small caps also perform best when growth is strengthening and the dollar is weakening (Chart 65). In contrast to the period between 2003 and 2020, small caps now trade at a discount to their large cap brethren. The S&P 600 currently trades at 14.4-times forward earnings compared to 19.7-times for the S&P 500, despite the fact that small cap earnings are projected to grow more quickly both over the next 12-months and over the long haul (Chart 66). Chart 64A Weaker Dollar And Stronger Global Economy Are Tailwinds For Non-US Stocks

A Weaker Dollar And Stronger Global Economy Are Tailwinds For Non-US Stocks

A Weaker Dollar And Stronger Global Economy Are Tailwinds For Non-US Stocks

Chart 65US Small Caps Usually Fare Well When The Economy Is Strengthening And The Dollar Is Weakening

US Small Caps Usually Fare Well When The Economy Is Strengthening And The Dollar Is Weakening

US Small Caps Usually Fare Well When The Economy Is Strengthening And The Dollar Is Weakening

Globally, growth stocks have outperformed value stocks by 60% since 2017. However, only one-tenth of that outperformance has come from faster earnings growth (Chart 67). This has left value trading nearly two standard deviations cheap relative to growth. Chart 66Small Caps Look Attractive Relative To Large Caps

Small Caps Look Attractive Relative To Large Caps

Small Caps Look Attractive Relative To Large Caps

Chart 67Value Remains Cheap

Value Remains Cheap

Value Remains Cheap

Chart 68Higher Yields Tend To Flatter Bank Stocks And Usually Weigh On Tech

Higher Yields Tend To Flatter Bank Stocks And Usually Weigh On Tech

Higher Yields Tend To Flatter Bank Stocks And Usually Weigh On Tech

Tech stocks are overrepresented in growth indices, while banks are overrepresented in value indices. US banks have held up relatively well since the start of the year but have not gained as much as one would have expected based on the significant increase in bond yields (Chart 68). With the deleveraging cycle in the US coming to an end, US banks sport both attractive valuations and the potential for better-than-expected earnings growth. European banks should also recover as the situation in Ukraine stabilizes. They trade at only 7.9-times forward earnings and 0.6-times book. On the flipside, structurally higher bond yields will weigh on tech shares. Moreover, as we discussed in our recent report entitled The Disruptor Delusion, a cooling in pandemic-related tech spending, increasing market saturation, and concerns about Big Tech’s excessive power will all hurt tech returns. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. 2 These savings can either by generated domestically or imported from abroad via a current account deficit. 3 Theoretically, there is a close relationship between trend growth and the equilibrium investment-to-GDP ratio. For example, if real trend growth is 3% and the capital stock-to-GDP ratio is 200%, a country would need to invest 6% of GDP net of depreciation to maintain the existing capital stock-to-GDP ratio. In contrast, if trend growth were to fall to 2%, the country would only need to invest 4% of GDP. Global Investment Strategy View Matrix

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Special Trade Recommendations Current MacroQuant Model Scores

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Executive Summary Oil Remains A Prominent Inflation Variable

WTI Futures Strongly Linked To US Inflation Expectations

WTI Futures Strongly Linked To US Inflation Expectations

Tight oil and metals markets will translate into persistently high inflation and inflation expectations over the next 5 – 10 years. High and volatile commodity prices caused by low capex will keep global inventories tight for years. This will keep the key 5-year/5-year (5y5y) CPI swap rates used by policy makers elevated, given the strong relationship between commodity prices – particularly longer-dated oil prices – and inflation expectations. Central banks will exacerbate this tightness if they follow through on more aggressive policy. This would increase the cost of capital for commodity producers and could induce a recession. All the same, commodity supplies still will remain tight, and will keep inflationary pressures emanating from the real economy elevated. Stagflation is the likely outcome. Gold is lagging as an inflation hedge vs. the average return of our commodity recommendations. We expect this to persist. Still, as a safe-haven and store of value during recessionary and inflationary periods, we continue to recommend gold as a portfolio hedge. Bottom Line: The dearth of capex in oil, gas and base metals markets makes persistently high inflation a foregone conclusion for the next 5-10 years. We remain long the S&P GSCI and the COMT ETF for direct commodity-index exposure, and the XOP, XME and PICK ETFs for exposure to commodity producers' equity. Feature That's all well and good in practice, but how does it work in theory? - Seen on a T-shirt at the University of Chicago1 Related Report Commodity & Energy StrategyCommodities' Watershed Moment Central banks are signaling they expect higher inflation and inflation expectations to persist, and now are communicating their collective resolve to deal with this aggressively, if needs be.2 As central-bank policy evolves, commodities – particularly oil – will become even more important as coincident and leading indicators used to assess the likely course of inflation and inflation expectations, particularly their persistence. The ECB notes oil prices have become more than just one of the input costs of manufacturing, or of mining, agriculture and the production of other forms of energy essential to powering modern economies, and delivering these goods globally. For the ECB, "oil is barometer of global economic activity as well as a financial asset."3 Likewise, the BIS stresses the importance of augmenting conventional Phillips curve models with commodity inputs to more accurately capture inflation dynamics.4 This Special Report follows our earlier report published on March 10, 2022 entitled Commodities' Watershed Moment. Here we explore the consequences of tightening commodity markets, especially as regards inflation and inflation expectations, and attempt to dispel some notions about commodities and markets that could lead to policy errors. We also evaluate our commodity recommendations' performance as inflation hedges compared to gold's performance. Modeling Inflation And Inflation Expectations Our own research and modeling broadly aligns with the ECB and BIS approaches. We periodically estimate cointegrating regressions of inflation expectations using WTI futures prices to forecast 5y5y CPI swap rates (Chart 1).5 Our results are strongest when we use 3-years forward WTI prices to forecast 5y5y CPI swap rates, but shorter-term futures also provide useful information and are cointegrated with inflation expectations discovered in the 5y5y market (Chart 2). The prompt-delivery WTI futures are cointegrated with the longer-dated 3-years forward futures contract, indicating that, over time, these different maturities are following a common long-term trend. This also explains why a similar equilibrium obtains using commodity indexes – the Bloomberg Commodity Index, the S&P GSCI, etc. – as regressors in estimating inflation expectations via the 5y5y CPI swap rates. Chart 1WTI Futures Strongly Linked To US Inflation Expectations

WTI Futures Strongly Linked To US Inflation Expectations

WTI Futures Strongly Linked To US Inflation Expectations

Chart 2US Oil Output Slightly Higher

US Oil Output Slightly Higher

US Oil Output Slightly Higher

Globalization of production, distribution and consumption across markets weaves these markets together – e.g., global fertilizer markets experienced a supply shock this past winter when large consuming markets in Asia and Europe got into a bidding war for limited LNG supplies – and transmits shocks across commodity markets. This partly explains the common long-term trend commodities generally share. Another feature weaving markets together globally is the fact that most global trade is invoiced and funded in USD, which means that the Fed's monetary policy decisions reverberate around the world when rates are increased or dollar liquidity is reduced.6 Lastly, trading markets are global. Commodity markets have evolved – as the ECB notes – into asset markets as well as hedging markets. This means arbitrage across commodity and rates markets (interest rates, inflation rates, FX rates, etc.) accelerates the impounding of information into prices quickly. In this environment, cointegration is strengthened among physical and financial trading markets, creating prices that share long-term equilibria. This makes the current time especially fraught, as the Fed embarks on a policy-tightening course against the backdrop of war in Europe and global commodity shortages. These effects are experienced across geographies and across time, forming a dynamic system in which supply, demand and inventories are constantly adjusting to new information. This affects current and expected fundamentals and financial conditions, which arrives to markets instantaneously. It is not surprising, then, that prices in these markets are, for the most part, cointegrated over the long run.7 Policy Errors Likely On The Way Monetary policy is not well suited to dealing with commodity scarcity. Nor is fiscal policy – e.g., government subsidies to soften the blow of rising energy prices only encourage over-consumption of scarce resources, which accelerates inventory depletion and tightens markets further. The Fed, in particular, likely is reviewing its 1970s playbook for lessons learned in the last major supply shock to hit the world – the Arab Oil Embargo of 1973, which was followed by the Iran-Iraq war in 1979. Together, these events triggered a surge in real oil prices, which rose by 4.5x – from $21.55/bbl in 1970 to $116.11/bbl in 1980, according to the EIA (Chart 3). Chart 3Fed Will Look Back At 1970s Playbook

Tight Commodity Markets: Persistently High Inflation

Tight Commodity Markets: Persistently High Inflation

In setting policy, economists generally – at the Fed, the IMF, the World Bank and elsewhere – mistakenly view commodity forward curves as something of a forecast.8 This use of the futures curve is mistaken because it only reflects the price levels as which transactions occurred on any given day. So while a non-specialist might view a backwardated forward curve for Brent as a market-based forecast for lower prices in the future – since prompt prices are trading below deferred prices – a more accurate reading would suggest markets are tight and likely will remain tight. This particular term structure indicates physical inventories are tight, and will remain so until sufficient supply is brought to market to allow refiners to restock. Steep backwardations also predispose markets to higher price volatility, because because of low inventory levels: The market's shock absorber (inventories) is low, so volatility increases.9 Suppose policy makers are counting on lower oil prices – per a forward curve's "forecast" – to bring inflation down. In that case, they likely will be disappointed unless additional supplies arrive. Should the Fed act on the belief that backwardation is a forecast for lower prices and continue to provide forward guidance to markets suggesting inflation will be lower next year, e.g., any delay in its rate hikes will leave it behind the inflation curve. Additional policy errors can come from the fiscal side, for example, when governments provide subsidies to soften the blow of higher oil prices. This retards the function of the price mechanism, and incentivizes higher consumption, which will exacerbate price increases. This would be bullish for oil prices in the short and medium term (6 months – 2 years). Commodity markets are tight globally – at or near scarcity levels in many cases, as can be seen by the continually declining inventories in oil and base metals (Chart 4 and 5). Base metals markets are extremely tight, and are on the back foot – i.e., with physical deficits and low inventories – just as the world's largest economic blocks (EU, US, China) are launching massive buildouts of their renewable-generation fleets and electric grids, and embarking on massive military buildups. These applications will require huge increases in base metals supplies to pull off. Grain markets will tighten as the impact of the Russian invasion of Ukraine unfolds in the spring, when winter wheat crops in Ukraine will need to be fertilized and tended. Chart 4Oil Markets Remain Tight...

Oil Markets Remain Tight...

Oil Markets Remain Tight...

Chart 5…As Do Metals

Tight Commodity Markets: Persistently High Inflation

Tight Commodity Markets: Persistently High Inflation

Barring an extremely deep recession that sharply reduces aggregate demand globally, it is difficult to see how this is not inflationary for years to come. Nonetheless, even a deep recession will still leave markets massively short base metals, and, after core-OPEC producers Saudi Arabia and the UAE bring what left of their spare capacity to market, oil. Investment Implications In days gone by, gold served as a go-to inflation hedge. At present, gold is lagging as an inflation hedge vs. the average return of our direct and equity-related commodity recommendations (Chart 6). We expect this to persist. Gold has performed well against the broad-trade weighted USD, however (Chart 7). We continue to recommend gold as a portfolio hedge, as it remains responsive to policy and geopolitical shocks. And it remains a safe-haven and store of value during recessionary and inflationary periods. Chart 6Commodity Recommendations Outperform Gold

Commodity Recommendations Outperform Gold

Commodity Recommendations Outperform Gold

Chart 7Gold Outperforms USD

Gold Outperforms USD

Gold Outperforms USD

The dearth of capex in oil, gas and base metals markets makes persistently high inflation a foregone conclusion for the next 5-10 years, barring a steep recession. Such a turn of events diminishes in probability, as governments keep funneling subsidies to households to soften the blow of higher prices and stave off a recessionary contraction in GDP. These subsidies only succeed in retarding the price signal the market is sending to reduce consumption of scarce commodities, which means available inventories will be drawn down more quickly. We remain long the S&P GSCI and the COMT ETF for direct commodity-index exposure, and the XOP, XME and PICK ETFs for exposure to commodity producers' equity. These are long-term holdings, given our view the commodities bull market will run for years. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Footnotes 1 Please see That Works Very Well in Practice, But How Does It Work In Theory? Published by quoteinvestigator.com for a history of how this phrase made it to UChicago's T-shirts. 2 Please see Between A Rock And A Hard Place, published 21 March 2022 by our US Investment Strategy, which is led by Doug Peta, a UChicago alum. 3 For insight into how central banks assess inflation and inflation expectations vis-à-vis commodity markets, particularly oil, please see the ECB's September 2020 working paper entitled " Global financial markets and oil price shocks in real time," by Fabrizio Venditti, Giovanni Veronese. In it, the authors note, "The role that the price of oil plays in economic analysis in central banks and in financial markets has evolved over time. Oil is not seen anymore just as a (sic) input to production but also as a barometer of global economic activity as well as a financial asset." 4 The BIS recently noted augmenting standard Phillips Curve models with information from commodities and FX markets to reflect the profound changes wrought by globalization is critical for improving inflation forecasts, and explaining the dynamics of inflation and inflation expectations. Please see "Has globalization changed the inflation process?" by Kristin J. Forbes, published by the Bank for International Settlements in June 2019. She notes, "The results in this paper suggest it is necessary to incorporate additional “global” factors in models of inflation dynamics, including global slack, non-fuel commodity prices (as well as oil prices), the exchange rate, and global price competition" to accurately explain and forecast inflation. See below for further discussion. 5 In our modeling, the regressor with the best fit in our 5y5y CPI swap forecasts is the WTI 3-years forward futures contract. Both the 5y5y CPI swap rate and the WTI futures are non-stationary variables sharing a common long-term trend, meaning these are cointegrated random variables. The time series we use start in 2010, so post-GFC, which was a regime change for markets globally. The regression diagnostics are very strong, particularly for the ARDL model. We also find the 3-years forward WTI price is cointegrated with the prompt WTI futures contract, indicating these variables – one calling for delivery of crude oil in 3 years, the other in one month – are cointegrated. We get similar cointegration results using commodity indexes – e.g., the Bloomberg Commodity Index, and the LME base metals index – which tend to use futures contracts closer to delivery. This indicates commodity prices generally can be thought of as non-stationary variables vibrating randomly around a common long-term trend. We use cointegration models to avoid spurious relationships – e.g., regressing a stationary variable on a non-stationary variable. Statistically, cointegration is much stronger than simple correlation because it avoids the trap of spurious relationships. Please see Granger, C.W.J., Developments in the Study of Cointegrated Variables, Chapter 4 in Engle and Granger (eds): 1991, Long-Run Economic Relationships. Readings in Cointegration, Oxford University Press. This is an a article by Clive Granger, who received the Nobel prize in economics in 2003 for his pioneering work developing the mathematics of cointegration. See also Geman, H. (2007), Mean reversion versus random walk in oil and natural gas prices, in Advances in Mathematical Finance (pp. 219-228), for a rigorous discussion of random-walking oil and gas variables. 6 Please see Global Dimensions of U.S. Monetary Policy by Maurice Obstfeld, which appeared in the February 2020 issue of International Journal of Central Banking for an excellent discussion of the Fed's role in global trade. This is not all a one-way street, as Obstfeld notes, in that policy decisions can create "potential spillback onto the U.S. economy from the disproportionate influence of U.S. monetary policy on the outside world." 7 These cointegrating features of commodity markets, inflation rates and USD effects are not agreed by all economists. See, e.g., the Oxford Institute for Energy Studies report of August 2021 Is the Oil Price-Inflation Relationship Transitory? by Ilia Bouchouev. The paper notes, "In theory, the fundamental relationship that exists between short-term inflation and gasoline futures should be fading away with time, and for 5y5y breakeven it should indeed be close to zero. In practice, however, it is not." 8 Please see Forecasting the price of oil, which was published by the ECB in Issue 4 of its 2015. The Bank notes, "Oil price futures are frequently used as the baseline for oil price assumptions in economic projections. They are used, for example, in the Eurosystem/ECB staff macroeconomic projections and in the projections of many other central banks and international institutions. The main reason for using futures as a baseline for oil price assumptions is that they provide a simple and transparent method which is easy to communicate." (p. 90) 9 Please see Kogan, Leonid, Dmitry Livdan and Amir Yaron (2009), " Oil Futures Prices in a Production Economy With Investment Constraints," The Journal of Finance, 64:3, pp. 1345-1375. Investment Views and Themes Strategic Recommendations Trades Closed in 2021

Image

Tensions between the West and Russia are intensifying. Although Russian Foreign Minister Sergei Lavrov stated in a televised meeting with President Vladimir Putin that there is still a possibility that diplomatic engagement will succeed, US National Security…

Executive Summary Inflation Expectations Likely Too Low

Inflation Expectations Likely Too Low

Inflation Expectations Likely Too Low

Inverted term structures for industrial commodities likely are being interpreted as forecasts of lower prices. This leads investors to assume the real economy will not be a source of persistent inflationary pressure. This is misguided: Backwardations (i.e., inverted forward curves) are evidence of tight markets facing severe upside price pressures, not lower prices ahead. Oil and base metals prices share a stronger relationship with US 5-year/5-year inflation expectations than gold, which is more correlated with short-term inflation expectations. Increases in US permanent unemployment are positively correlated with 5y5y inflation expectations. This suggests markets price in a more accommodative Fed as permanent unemployment increases, and vice versa. US PCEPI realized core inflation is negatively correlated with permanent unemployment levels, suggesting markets are pricing lower inflation as permanent unemployment rises, and vice versa. Bottom Line: Markets generally exhibit well-anchored inflation expectations. We believe these will be undone by profound backwardations in industrial commodities, which point to steadily increasing inflation pressures from the real economy to end-2023. Thereafter, oil and metals demand will continue to grow faster than supply, as the renewable-energy transition picks up steam. We remain long commodity-index exposure, and industrial-commodity producers' equity via ETFs. Feature Backwardated forward curves for industrial commodities – oil and base metals, in particular – are clear evidence these markets are pricing to severe physical supply deficits, which presently are being covered by drawing down inventories.1 These inverted term structures for industrial commodities likely are being interpreted as forecasts of lower prices, which leads investors to assume the real economy will not be a source of more permanent inflationary pressure. This is misguided, in our view: Profound inversions in the term structure of commodities (i.e., backwardations) are evidence of tight markets facing severe upside price pressures. Persistently tight supply-demand balances are keeping the forward curves of industrial commodities backwardated, as inventories are drawn down to cover physical supply deficits. These deficits are dramatically evident in oil markets (Chart 1) and copper markets (Chart 2), both of which are widely followed by investors and corporates alike. Chart 1Tight Oil Markets

Tight Oil Markets

Tight Oil Markets

Chart 2Coppers Physical Deficits Will Persist...

Coppers Physical Deficits Will Persist...

Coppers Physical Deficits Will Persist...

Higher Commodity Prices, Higher Inflation In Chart 3, we show the difference between the forecast outcome of US 5-year/5-year (US5y5y) CPI inflation expectations drawn from the CPI swap markets as a function of our internal oil-price forecasts and commodity forwards reflecting futures-contract settlements. These curves show the model based on the futures curve understates the expected path of inflation expectations versus our oil-price forecasts. When we used our higher oil price forecasts – based on the scenario where OPEC 2.0 and the US fail to increase oil supply in 2022 and 2023 – US5y5y rates tracked the increase in oil prices. The results of these forecasts show that oil prices, and more broadly, the real economy, feeds directly into inflation expectations. We modelled the US5y5y rates as a function of additional commodity prices as well – namely, copper and gold (Chart 4). The coefficients for commodity prices associated with the levels equation was always positive, irrespective of the commodity, implying that commodity prices and inflation expectations share a long-run equilibrium. We ran these regressions with nearer term forward inflation expectation rates as well, and found the direction of the relationship held.2 Chart 3Inflation Expectations Likely Too Low

Inflation Expectations Likely Too Low

Inflation Expectations Likely Too Low

Chart 4Consistent Relationships Between Commodities and Inflation Expectations

Consistent Relationships Between Commodities and Inflation Expectations

Consistent Relationships Between Commodities and Inflation Expectations

Gold Hedges Shorter-Term Inflation Expectations Gold prices had a stronger relationship to nearer-term forward inflation expectation rates than WTI and COMEX copper prices, in our modeling. On the other hand, WTI and COMEX copper prices had stronger relationships with longer-term forward inflation expectation rates than gold prices. These results suggest different commodities can be used to hedge different segments of the inflation-expectations term structure, which is a novel outcome to our modeling. This strongly suggests a portfolio of gold, copper and crude oil – using futures, commodity indices or physical assets – can hedge the inflation-expectations term structure. Labor Markets And Inflation Expectations We also modelled realized monthly inflation and US5y5y inflation expectations as a function of permanent job losses, a series maintained by the US Bureau of Labor Statistics (BLS). The coefficient associated with permanent job losses was positive (Chart 5). Increases in US permanent job losses are positively correlated with 5y5y inflation expectations. This suggests markets price in a more accommodative Fed in the future as permanent unemployment increases, and vice versa. This positive relationship holds even when WTI and copper prices are added as regressors to the equation. We also find that realized US PCEPI core inflation – the Fed's preferred gauge – is negatively correlated with permanent unemployment levels, suggesting markets are pricing lower inflation as permanent job losses increase (Chart 6). This also is intuitively appealing in the model, as it points toward the markets' assessments of Fed policy functions. Chart 5Labor Markets Also Effect Inflation Expectations

Labor Markets Also Effect Inflation Expectations

Labor Markets Also Effect Inflation Expectations

Chart 6Lower Inflation When Permanent Job Losses Rises

Lower Inflation When Permanent Job Losses Rises

Lower Inflation When Permanent Job Losses Rises

Investment Implications In earlier research, we showed commodity prices generally feed directly into realized inflation and inflation expectations (Chart 7).3 In the current report, we also showed that different commodities are better suited for hedging inflation expectations at different points along the inflation forward curve, which is a novel finding. We continue to expect the global energy transition to keep industrial commodities well bid for at least the next decade, as markets are forced to reconcile increasing demand for hydrocarbons and base metals with flat to declining supplies. On top of this, as we have noted in the past, there is a growing list of exogenous threats to the supply side. Among them are the election of left-of-center governments in important commodity-producing states, which have campaigned on redistributionist agendas; climate activism at the board level at major energy suppliers and in the courtroom, and mounting calls for still-undefined ESG compliance. Chart 7Commodity Indices Move Closely With Inflation Expectations

Commodity Indices Move Closely With Inflation Expectations

Commodity Indices Move Closely With Inflation Expectations