Gold

Recession is on track to start around year-end. Stocks usually peak shortly before recession begins. So, position defensively but be prepared for a few more months of the rally.

We build a four-stage business cycle framework based on economic growth and capacity utilization, and then analyze historical returns for most major asset allocation decisions for each stage. Given that we are in the early recession stage (negative growth coupled and an overheated economy), our framework recommends a defensive positioning across all asset classes.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

Once the debt ceiling soap opera ends, investors will likely turn their attention to some of the tailwinds supporting stocks. These include stronger earnings growth, diminished bank stresses, better housing data, early signs of an upleg in the manufacturing cycle, the prospects of an AI-driven productivity boom, and the fact that labor slack has managed to increase without rising unemployment. Investors should resist turning bearish on stocks for now but look to become more defensive later this year.

In Section I, we review the three possible economic scenarios over the coming year, and underscore that the “soft landing” scenario remains improbable. A “no landing” scenario could occur, but it would ultimately lead back to the recessionary path and thus is not a basis for investors to maintain pro-risk portfolio positions. US stock prices continue to be buoyed by rate cut expectations, but nonrecessionary cuts still appear to be a long way off. In Section II, we present our best estimate of the inflationary threshold that results in a positive or negative stock price / bond yield (SBY) correlation, and whether investors are likely to approach this level over the coming one-to-two years. US core inflation does not likely need to return to the Fed’s target in order for the SBY correlation to return to positive territory, but a move back to a positive correlation will very likely occur in the context of falling equity prices.

The crisis hitting regional and local banks in the US is adding to oil-price volatility and gold demand. The crisis arguably is fallout from the Fed’s aggressive monetary policy tightening, and contributes to the upending economic relationships that reliably informed policy, investments and forecasts in the past. This feeds into higher price volatility, which reduces liquidity in the short run, and impedes capex in the long run, which limits future supply growth.

In this volume of BCA Crypto we compare gold against bitcoin. We begin by dispelling some common misconceptions that investors have about gold, and why, at its core, gold is driven more by belief than by intrinsic value. We then proceed to explain why gold still serves an important role in our economy and how it differs from fiat money. Later, we explain how bitcoin is different from other cryptocurrencies, and why it could rival gold as a reserve asset in the future. Finally, we discuss the outlook for bitcoin, as well as which macro factors investor should watch.

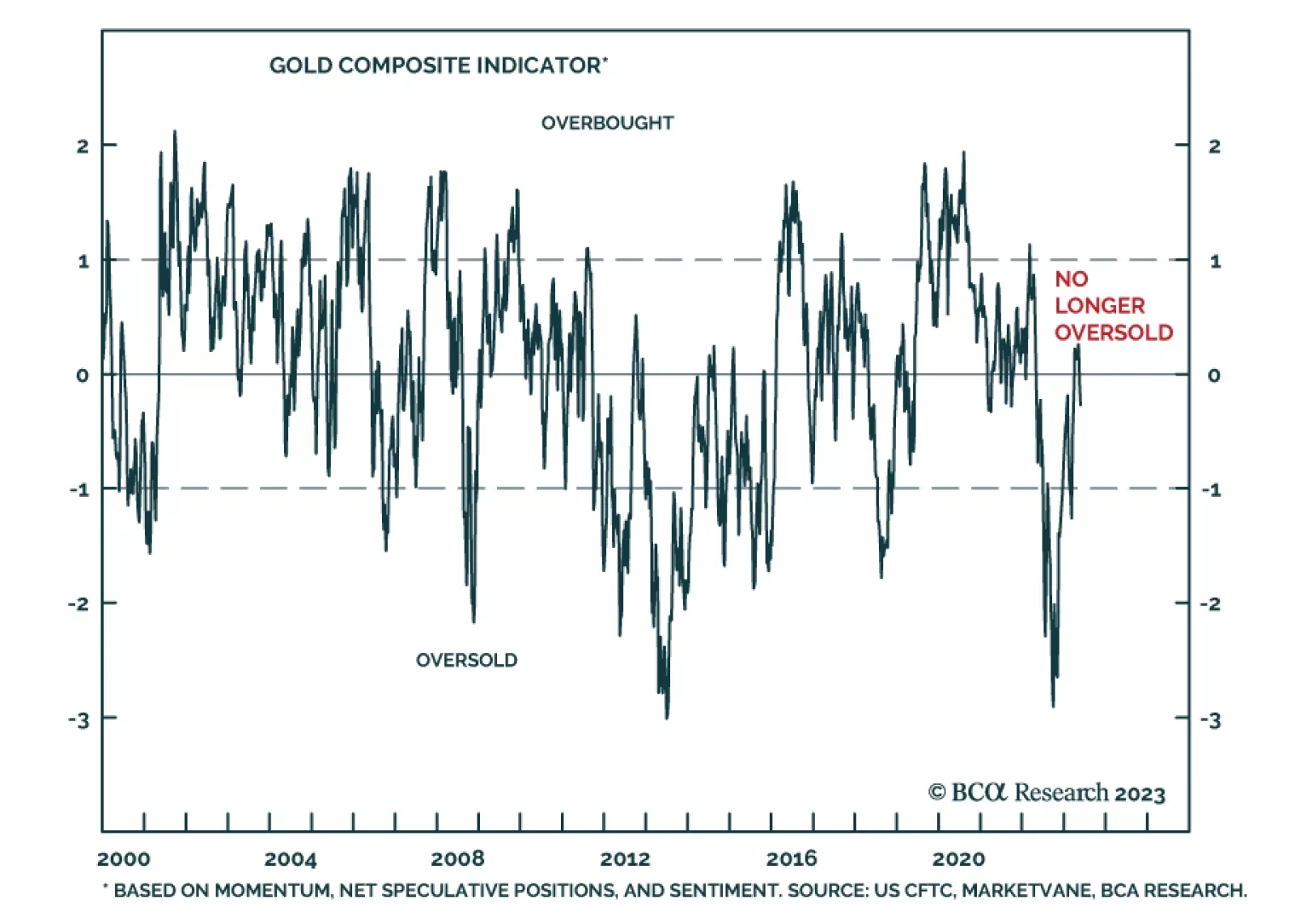

We are increasing our gold price target to $2,200/oz, given the increasing risk of fiscal dominance in the US, rising geopolitical risk, the return of trading blocs and currency debasement risk. These risks also will increase economic uncertainty, which also will be bullish for gold.

The dollar has entered a structural bear market. Although the greenback could get a temporary reprieve during the next recession, investors should position for a weaker dollar over the long haul.