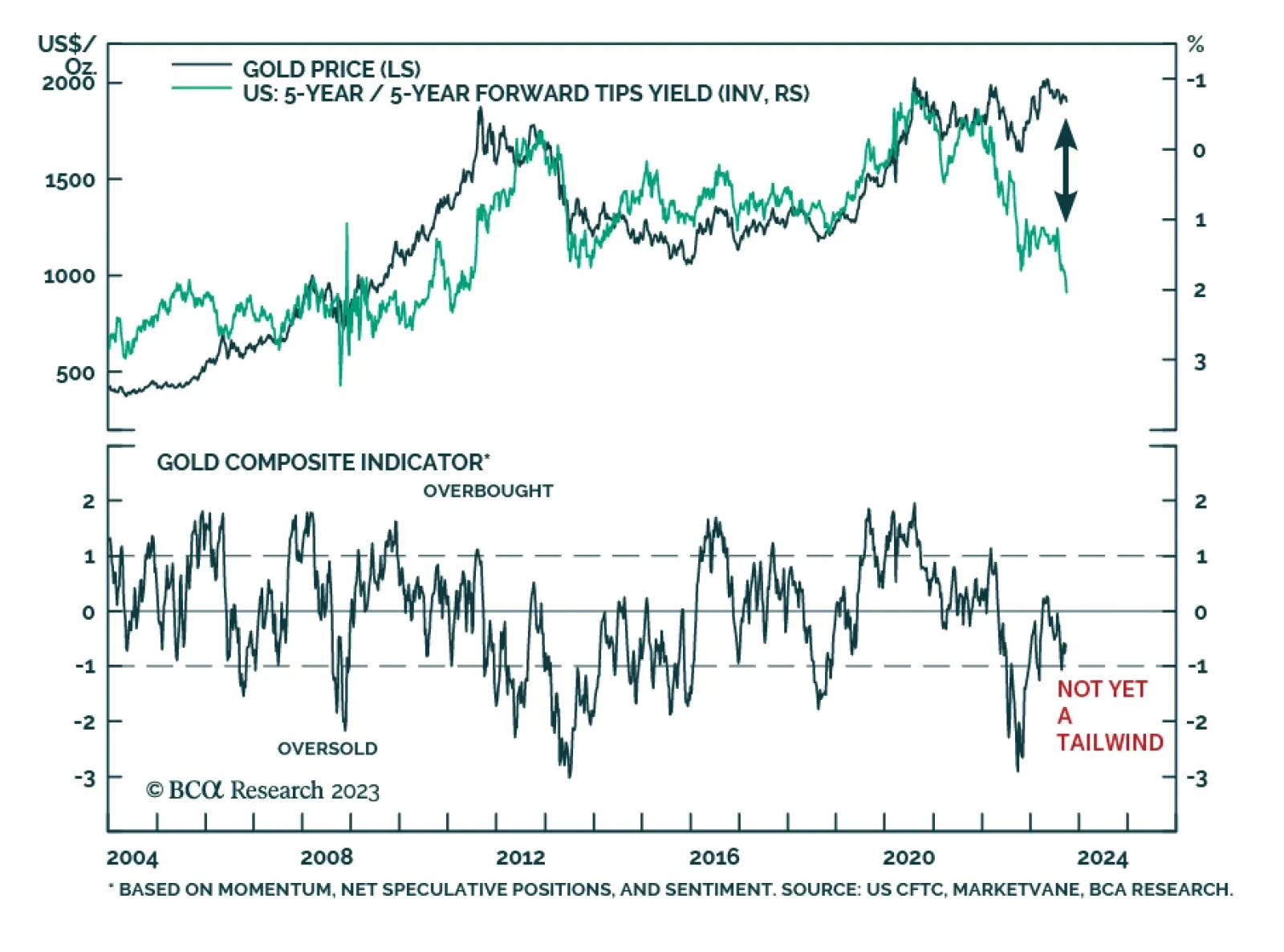

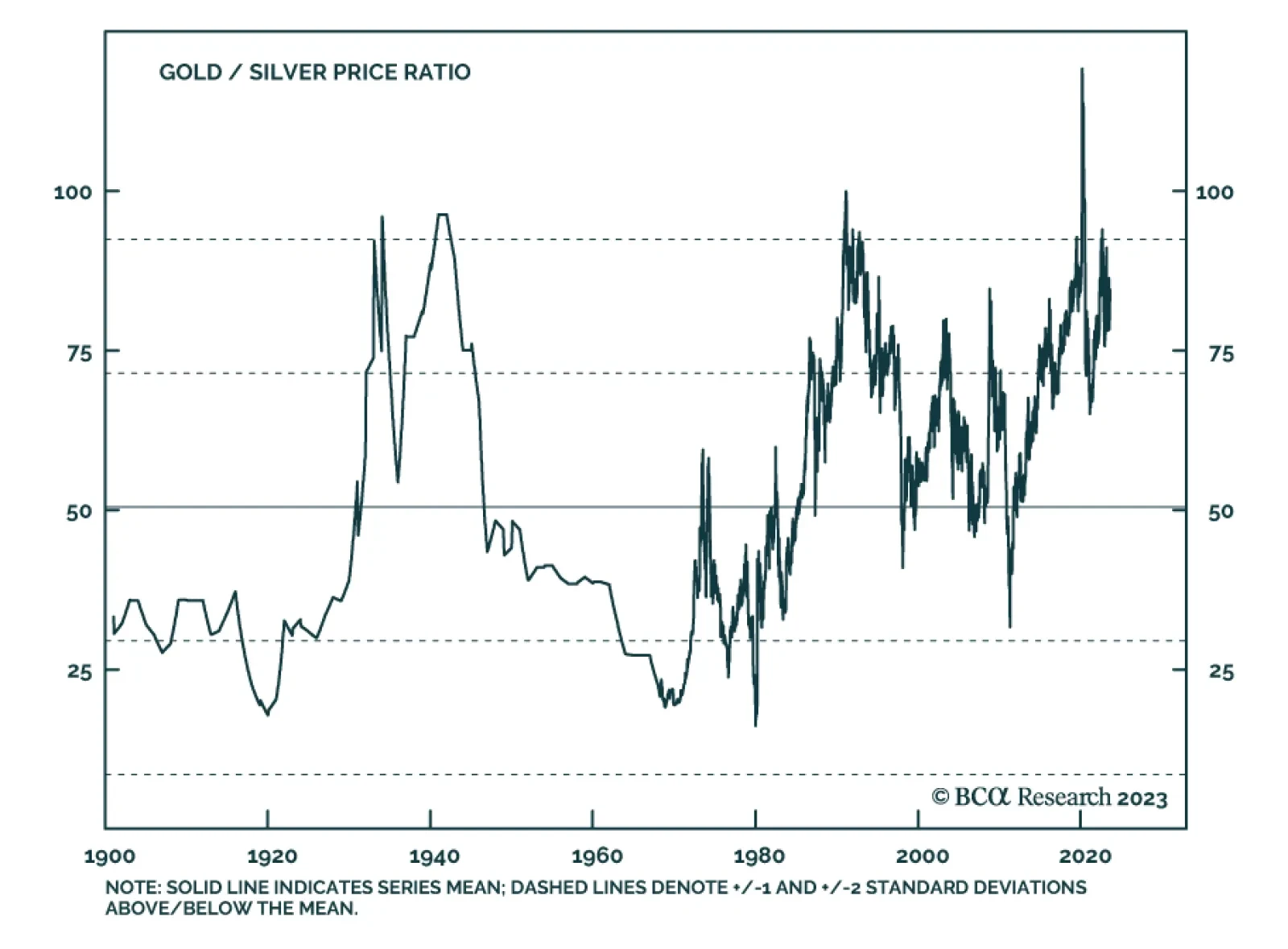

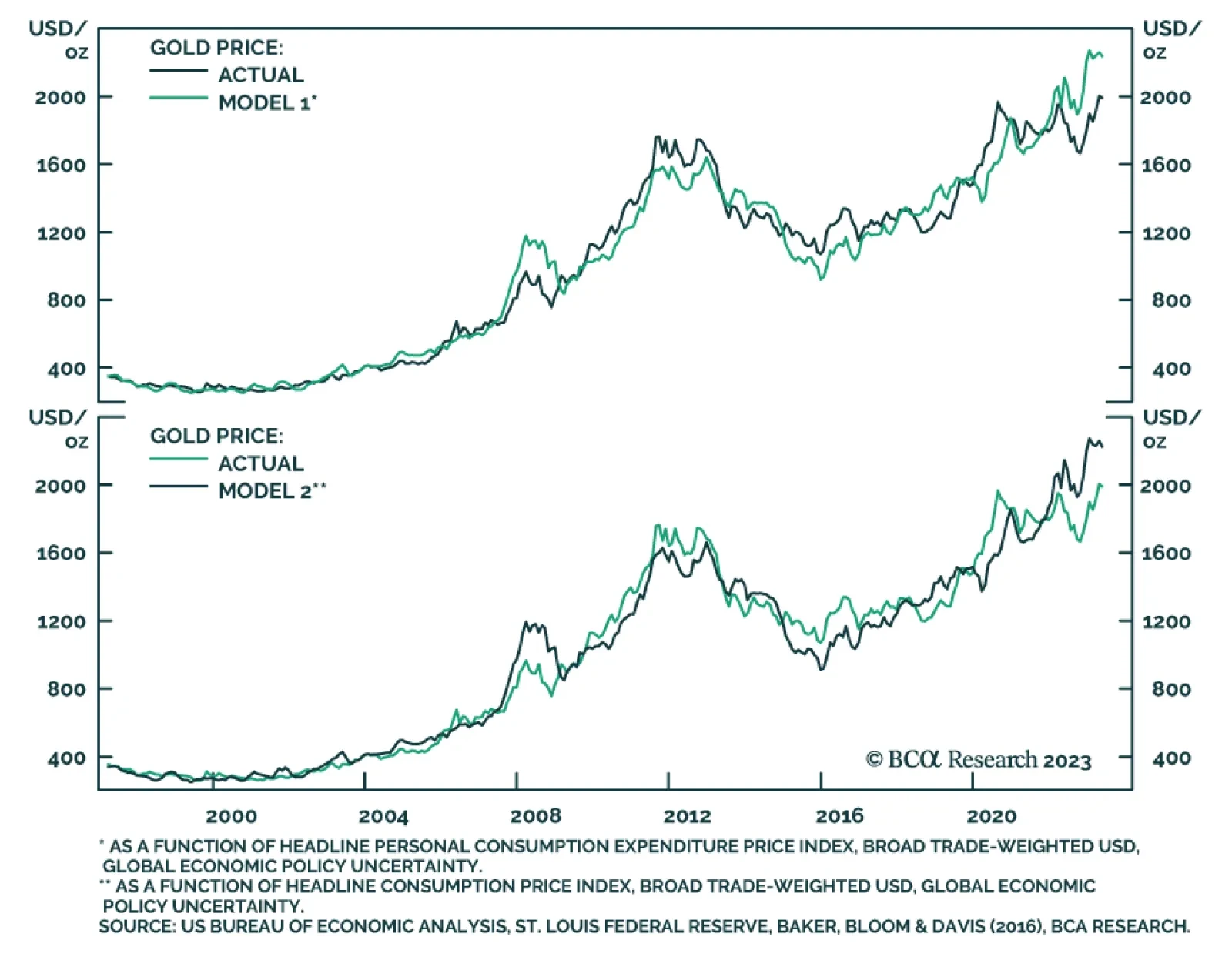

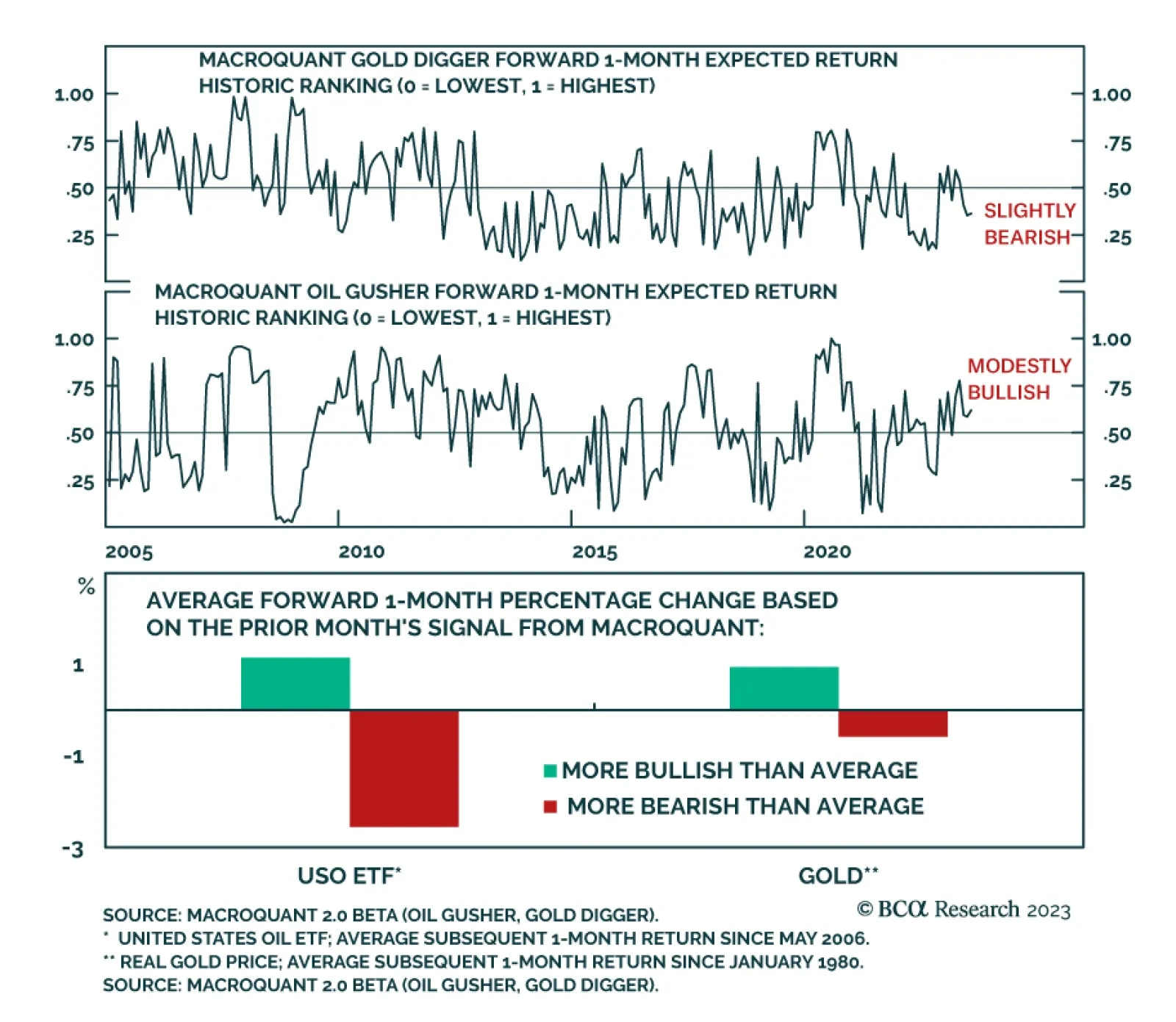

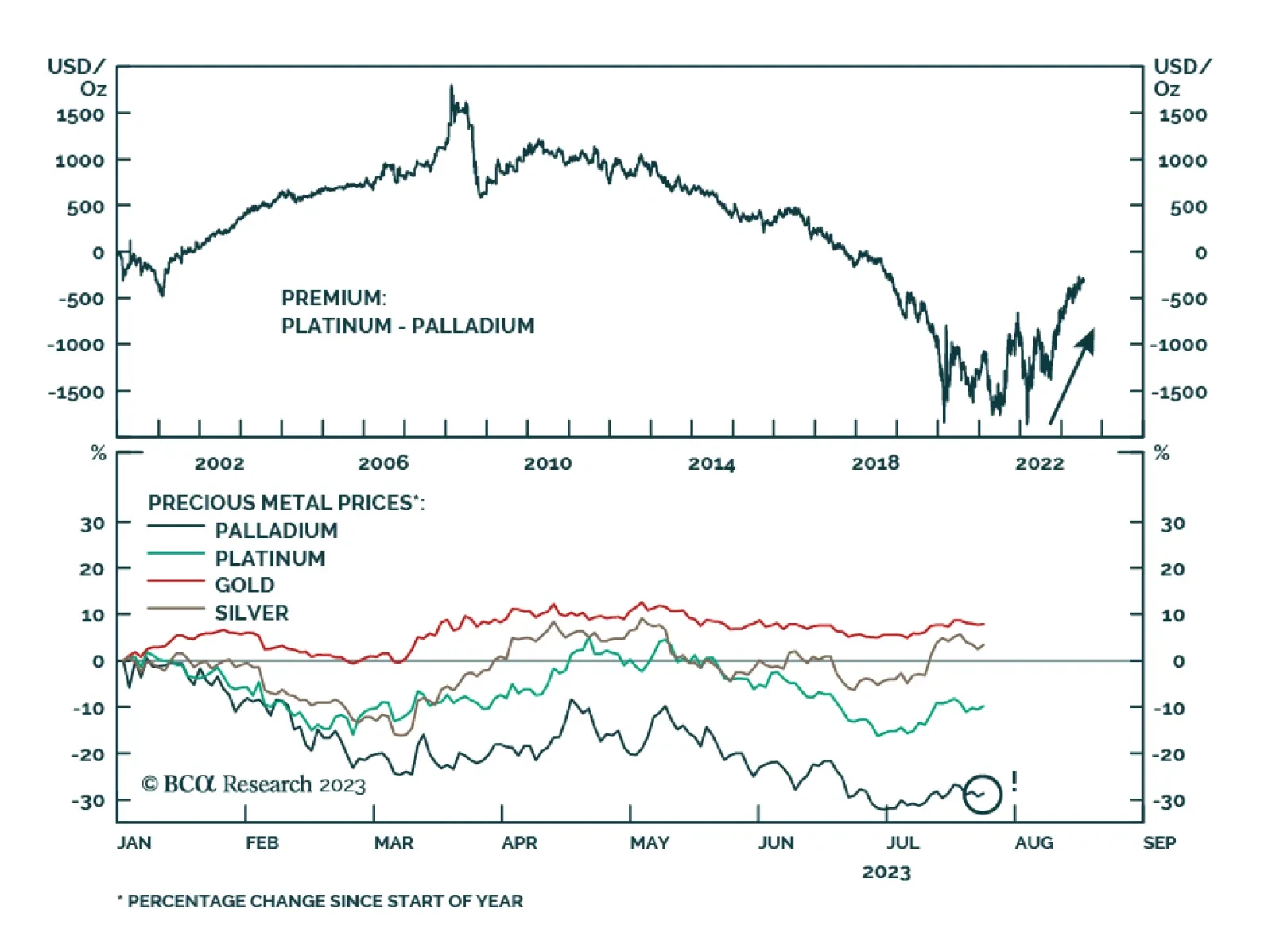

Gold

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

The downgrade of the US credit rating highlights the risk of fiscal dominance overriding the Fed’s long-standing monetary dominance focused on its dual mandate. This threatens to push inflation and long-term interest rates higher. It also will redound to the detriment of the USD, and governments’ and investors’ willingness to hold it. China’s liquidity trap will keep its inflation subdued in the short run, but not forever. We remain long gold as a hedge against fiscal dominance and USD debasement risks.

In this short weekly report, we review some of the most common questions clients asked us in the last few weeks.

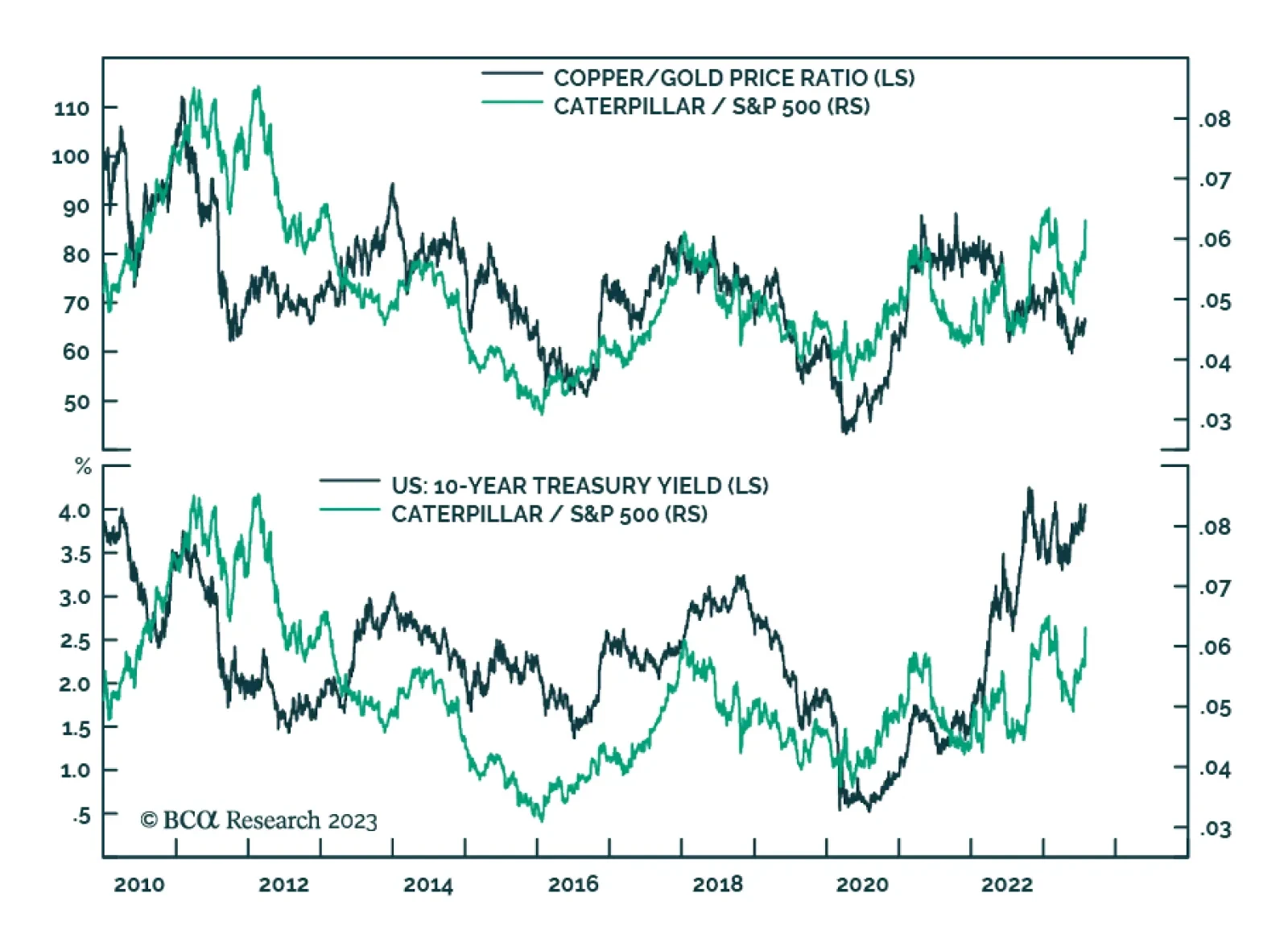

Markets continue to be tossed to and fro by central-bank policy, and risks of higher commodity prices. These are due to fiscal stimulus and exogenous weather and war-related risk, which could send food and energy prices higher this winter. We remain long gold outright, energy and metals producers via the XOP, XME and PICK ETFs, direct commodity exposure via the COMT ETF, and futures exposure to backwardation in copper (long 4Q23 copper futures vs. short 4Q24 copper futures).